Story Series: sb1235

Hearing on Commercial Financing Disclosures Scheduled in California State Senate

May 7, 2018Update: Link to the LIVE stream is here

The Senate Judiciary Committee for the State of California will convene for a hearing on the commercial financing disclosures bill at 1:30 PST on May 8th. SB-1235, as its known, previously survived the Senate Committee on Banking and Financial Institutions when it was debated and contested on April 19th. (a video of that hearing is available here)

The Senate Judiciary Committee for the State of California will convene for a hearing on the commercial financing disclosures bill at 1:30 PST on May 8th. SB-1235, as its known, previously survived the Senate Committee on Banking and Financial Institutions when it was debated and contested on April 19th. (a video of that hearing is available here)

deBanked will attempt to stream the hearing or provide a link to it when it begins. Check back here for more details.

Despite Movement of Negative Bill for MCA and Factoring Industries, Hope for a Solution

April 23, 2018Last week, California State politicians gathered for a hearing on SB 1235, a bill that would require the disclosure of an Annual Percentage Rate (APR) for all loans and non-loans, including MCA and factoring products. This is very problematic because APR (which includes interest rate) cannot be calculated for most MCA and factoring products for one reason: time. What makes merchant cash advance and factoring unique is that the timing of payments is flexible, and therefore unknown.

“It’s impossible to compute,” said veteran factoring lawyer Bob Zadek about calculating APR for most MCA and factoring products. “Interest = principal x rate x time. Since [they] cannot determine how long the advance will be outstanding – since repayment is a function of the borrower’s cash flow – the algebra doesn’t work.”

The bill, introduced by California State Senator Steve Glazer, moved out of the Senate committee on Banking and Financial Institutions and is headed to the Judiciary committee – closer to potential passage. Yet advocates of the MCA industry, one of whom testified in the assembly room in Sacramento, are hopeful.

“There were a number of state senators who clearly understood the problems with applying an APR to a commercial transaction and to a purchase and sale of receivables transaction,” said Katherine Fisher, a partner at Hudson Cook, LLP who spoke on behalf of the Commercial Finance Coalition (CFC). CFC is an alliance of financial companies that educates government regulators and elected officials on issues related to non-bank commercial finance. CFC Executive Director, Dan Gans, told deBanked that he believed the committee really understood what Fisher was trying to convey.

Another major advocacy group is the Small Business Finance Association (SBFA). They brought Joseph Looney, COO and General Counsel of RapidAdvance, to testify against SB 1235, and SBFA Chief of Staff Steve Denis sounded optimistic, saying that they have a very good relationship with State Senator Glazer’s office.

“To me, despite the fact that they moved [on] a bill that we’re opposed to through the process,” Denis said. “I think the folks that we’ve been meeting with out there – the senators – they’re all very open to our industry and open to having broader discussion about how to [best] disclose these terms and how to make sure we’re doing what’s in the best interest of small business owners. That’s a real positive, and I’m optimistic that we can get something done.”

As for concern about the bill moving forward, Denis said it’s what he expected.

“It’s just the way the process works in California,” Denis said. “If you look at committee history, they don’t really reject a lot of bills. They like to move bills forward so they can be discussed and negotiated.”

As of this story’s publication, SB 1235’s Judiciary committee hearing had not yet been scheduled.

Update 4/26/18: The hearing is scheduled for May 8, 2018 at 1:30 p.m. PST in Room 112.

Full video of the April 18th hearing below:

What Got Said in The California Senate Hearing About Commercial Loan Disclosures

April 19, 2018

California State Senator Steve Glazer was the reason that representatives from small business finance trade associations were in Sacramento on Wednesday. Glazer’s bill, SB 1235, calls for mandatory APR disclosures on loan and non-loan products alike, even if the transaction is business-to-business and even if the transaction assesses no interest charges and even when no such APR can be calculated or exists.

That proposal caught the attention of several interested groups, including those whose members offer short term small business loans, factoring, and merchant cash advances. Among those who testified in front of the Senate Committee on Banking and Financial Institutions on Wednesday was Joseph Looney, COO & General Counsel of RapidAdvance, who spoke on behalf of the Small Business Finance Association, and Katherine Fisher, Partner at Hudson Cook, LLP, who spoke on behalf of the Commercial Finance Coalition. Each of them were there representing separate constituents with their own individual views.

Transcripts of their testimonies are below:

“Chairman Bradford, Vice Chair Vidak, and Members of this committee. I am Joseph Looney and I am the General Counsel for a commercial finance company named RapidAdvance. We are a California Finance Lender licensee and have provided more than $200,000,000 in capital to thousands of businesses in California. Today I am providing testimony on behalf of the Small Business Finance Association or SBFA, which is the leading association for companies that provide funding to Main Street businesses. The SBFA is in opposition to Senate Bill 1235 as currently drafted. While there are various issues with the Bill, the overarching concern we have is that it treats small businesses like consumers. States and the federal government have generally refused to treat small businesses the same as consumers when it comes to financing disclosures for two reasons. First, there is a significant concern that imposing consumer disclosures and regulation on small businesses would reduce the flow of capital and negatively impact the economy. Second, small business owners are sophisticated and do not need the same protections provided to consumers. Business owners hire and fire employees, handle taxes and payroll, negotiate with customers and vendors, arrange financing, handle litigation and execute on business strategies every day. Also, businesses look at money differently than consumers. A business gets capital and uses it to make more money or solve a problem in their business. In this scenario, the most important item to the business owner is how fast can they get the money and what are the conditions for getting it. The APR disclosure included in the Bill is problematic as it will create confusion. The CFPB has recently concluded the APR is confusing, does not provide as much value as thought and is extremely complicated for creditors to calculate. In fact, the CFPB is making the APR less important by moving it to the end of some disclosures and completely removing it in some cases. The APR is so complicated to calculate there are numerous pages in the Code of Federal Regulations devoted to explaining the calculation. Additionally, there are pages of guidance on how to handle various consumer products and payment types and what assumptions should be made for various products as well as shielding creditors from liability for minor calculation errors. This Bill does not address any of these issues. It simply takes an APR disclosure requirement for fixed monthly payment consumer finance transactions and concludes it should apply to materially different commercial products. While we do not support the Bill as it imposes consumer disclosures such as the APR on small business transactions, we are supportive of the idea of providing businesses with cost disclosures. Thank you.” |

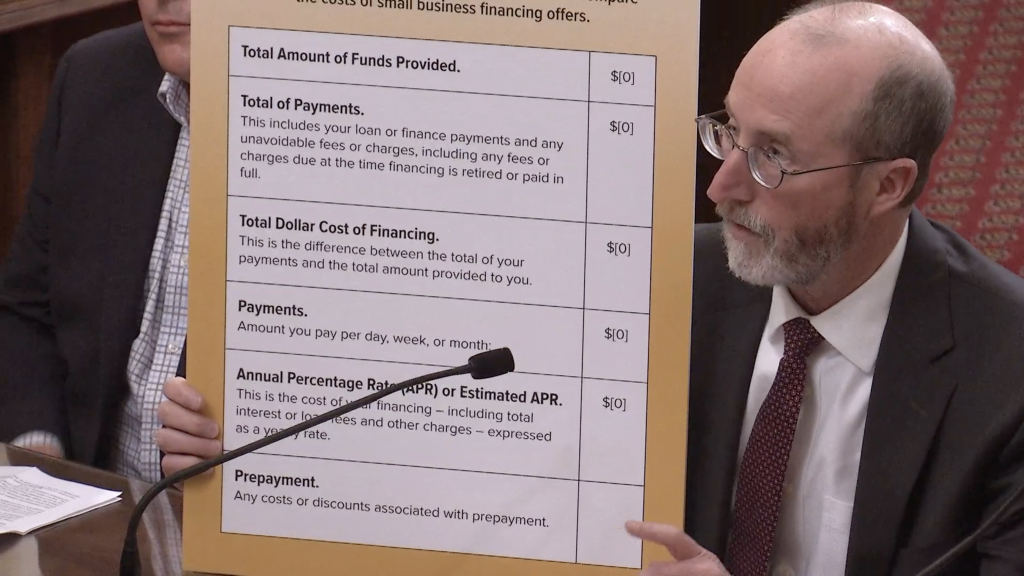

“Chairman Bradford and committee members: Thank you for the opportunity to present testimony today regarding SB-1235. My name is Kate Fisher and I am here today on behalf of the Commercial Finance Coalition, a group of responsible finance companies that provide capital to small and medium-sized businesses through innovative methods. Small businesses face a gap in credit availability. Commercial Finance Coalition member companies are trying to close this gap and help spur entrepreneurship so more Americans and Californians can own and operate their own businesses. I also am a lawyer who works with providers of commercial financing on complying with state and federal law. The Commercial Finance Coalition supports California’s efforts to make business financing more transparent. Businesses benefit from having different types of financing available, and being able to comparison shop. SB 1235 would require commercial finance providers to disclose the cost of capital by providing the following helpful disclosures: The Total Amount of Funds Provided These three disclosures will help a California business owner understand and compare the cost of financing across different products. However, the Commercial Finance Coalition opposes requiring an APR disclosure. It’s important to note that SB 1235 aims at providing comparable disclosures across very different financing types. Commercial Finance Coalition members mostly engage in “accounts receivable purchase transactions.” These transactions are also known as merchant cash advance or factoring, and involve a business selling its receivables at a discount. For example, if a business’s sales go down, the business can pay less. If a business’s sales go up, the business can pay more. And if a business is burned down in a fire, the business can pay nothing until it can reopen its doors. SB 1235 would require disclosure of an Annual Percentage Rate (or APR). There are two problems with requiring an APR disclosure or even an “Estimated APR”: First – SB 1235 fails to address the complexity of calculating APR for different types of commercial finance transactions. This creates a significant litigation risk and minefield for finance providers making a good faith effort to disclose APR, and may stifle small business financing in California. Second – Requiring an Estimated APR disclosure creates an unfair disadvantage for offers of “accounts receivable purchase transactions” – or factoring. Again, these transactions are purchases, and do not need to be “paid back” unless the business has sufficient sales. Also, this disclosure could confuse a business owner who is looking for alternatives to lending. I’m very optimistic that California can lead the way in providing businesses with disclosures that are helpful – and not confusing. |

In response, Senator Glazer deferred to the experts who testified but he was not willing to make a key concession in the moment. At Glazer’s prodding, the bill made it out of committee with enough votes, and with the goal of continuing to fine tune the details particularly with respect to APR.

More information surrounding the bill and it’s progress will be made available soon.

Full video of the hearing below:

Industry Representatives to Testify at California Hearing

April 18, 2018

Several people will be testifying in front of the Senate Committee on Banking and Financial Institutions in California today. Among them are Joe Looney, COO & GC at RapidAdvance, who will be speaking on behalf of the Small Business Finance Association, and Katherine Fisher, Partner at Hudson Cook LLP, who will be speaking on behalf of the Commercial Finance Coalition.

At issue is SB 1235, a bill that would require providers of commercial financing to provide disclosures about the cost of that financing to the recipients of the financing.

Industry analysts believe the bill could have implications not just for small business lending but also for factoring and merchant cash advance.

Update: Full video of the hearing below