Story Series: debt settlement

MCA Helpline, A Debt Settlement Company, is Sued For Tortious Interference

January 25, 2018

Debt settlement is under fire again. This time it’s a trio of defendants, namely MCA Helpline, LLC, Decision One Debt Relief, LLC and Todd Fisch individually, according to a complaint filed by plaintiff Everest Business Funding on Wednesday in Broward County, Florida.

Everest is seeking damages for Defendants’ tortious interference with at least a dozen of its merchant contracts.

“Defendants have engaged and continue to engage in the business practice of making misleading representations to Everest’s customers; namely, promising to save the merchants money on their existing contracts with Everest when they have no intention or ability to uphold such a promise,” the complaint states. “In so doing, Defendants tortiously interfere with Everest’s merchant agreements by inducing the merchants to breach their contractual obligations to Everest in favor of entering a new payment relationship with the debt relief company.”

Fisch is alleged to be the mastermind behind both MCA Helpline and Decision One Debt Relief.

Complicit ISOs were also put on notice. “To the extent any specific ISOs or their affiliates who have ISO Agreements with Everest have leaked information about Everest’s merchants to Defendants, or to any other third party, such conduct constitutes both a breach of the ISO Agreement and tortious interference with Everest’s merchant contracts,” it reads. “Through the course of discovery in this lawsuit, Everest plans to add as additional Defendants, as yet unidentified ISOs, which have been working with Defendants to target Everest’s merchant accounts in violation of their contractual agreements.”

Everest has been vigorously pursuing debt settlement companies. In September, they, along with Yellowstone Capital, filed a lawsuit against eight defendants (later amended to include 1 more) in New York.

Another lawsuit examining similar issues was also filed last year in New York. In Pearl Gamma Funding and Pearl Beta Funding v Creditors Relief, Pearl tacked on a defamation claim in addition to tortious interference. That case is still pending.

Law Firm or Law Fail? Debt Settlement Company’s Legal Footing Called into Question

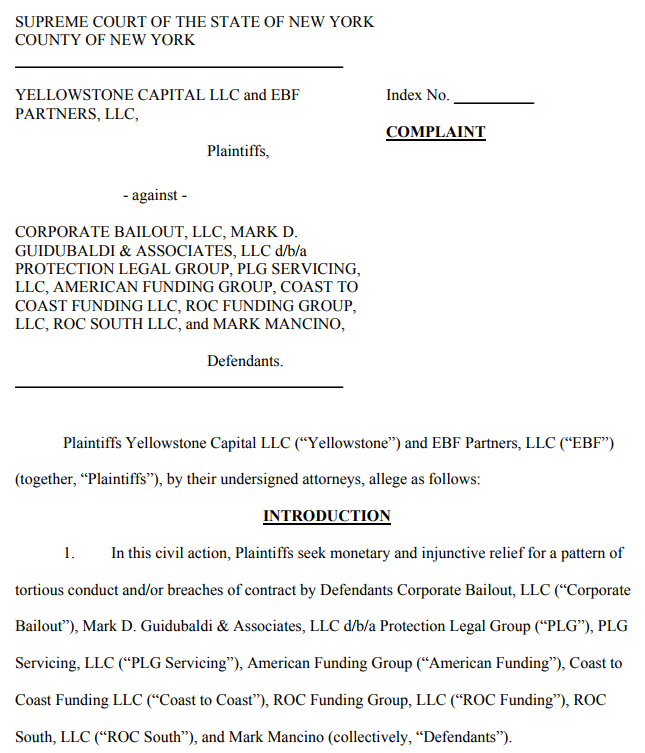

December 6, 2017The first major volley in the lawsuit filed by plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) against a debt settlement company and their alleged ISO partners has been exchanged. And it’s a doozy.

Three of the eight defendants, Mark D. Guidubaldi & Associates, LLC (d/b/a Protection Legal Group) aka PLG, Corporate Bailout, LLC, and PLG Servicing, LLC have sought to collectively dismiss the complaint on the grounds that they are attorneys “engaged in the practice of law with the Merchants as their clients.”

PLG, a self-described “multi-jurisdictional law firm that practices law in various jurisdictions nationwide,” argues in their motion papers that those employed by Corporate Bailout and PLG Servicing carry out certain administrative and support tasks for PLG. And it’s okay that no one at either of those companies are attorneys, they claim, because PLG supervises it all. That enables them to be covered as attorneys in an attorney-client relationship, they assert.

If true, they might want to try harder at supervising. As you might remember, Corporate Bailout, a telemarketing debt settlement firm, was featured on the cover of the New York Post earlier this year after being sued for running an operation “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street.’”

If true, they might want to try harder at supervising. As you might remember, Corporate Bailout, a telemarketing debt settlement firm, was featured on the cover of the New York Post earlier this year after being sued for running an operation “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street.’”

Corporate Bailout’s principal office is in New Jersey. PLG, the law firm, is based in Illinois. Can it really be that the former is considered a law firm through a relationship with the latter?

Whoa, not so fast, says an amended complaint filed by the plaintiffs on Tuesday, which argues that not even PLG is a legitimate law firm. “In fact, none of the Debt Relief Defendants is a law firm engaged in the provision of legitimate legal service,” they contend. “PLG is not even registered as a law firm in Illinois, as required by the rules of the Illinois courts,” they add.

If true, then this case could potentially have far-reaching consequences beyond simple tortious interference.

Some excerpts from this bombshell allegation:

PLG has one employee who is a lawyer, but does not as a rule advise or represent its customers. The advice those merchant customers receive is given by non-lawyers at Corporate Bailout and PLG Servicing, who approach and recruit merchants in ways no lawyer subject to the Rule of Professional Conduct 7.3 would ever be permitted to solicit clients. The non-lawyer personnel at Corporate Bailout and PLG Servicing are not supervised by the solitary lawyer at PLG, but by [Mark] Mancino and [Michael] Hamill, who are not lawyers – an arrangement that, if PLG were a law firm engaged in the provision of legitimate legal services, would violate Rule of Professional Conduct 5.3. To the extent that any of the advice the non-lawyers at Corporate Bailout and PLG Servicing give to merchants in furtherance of the Debt Relief Defendants’ tortious activity is legal advice at all, giving it violates the prohibition on the unauthorized practice of law. PLG orchestrates this activity, which damages the merchants as well as their Merchant Cash Advance Providers, in flagrant and deliberate disregard of the law.

[…]

Although the merchants are told that they are paying the funds into an “escrow account,” in reality PLG does not treat the funds like client escrow funds; it pays itself from them from the beginning, regardless of whether it is providing any services, and with no differentiation between client funds and funds payable to PLG. If PLG really were a law firm engaged in the provision of legitimate legal services, its practices with respect to client funds would be barred by the Rule of Professional Conduct 1.15.

– plaintiffs in the Amended Complaint (<-- click to download a copy)

Plaintiffs have also added Michael Hamill as an individual defendant. Fellow co-defendants Mark Mancino, American Funding Group, Coast to Coast Funding, LLC, ROC Funding Group, LLC, and ROC South, LLC did not file a response to the original complaint.

ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

September 28, 2017 ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

The debt settlement companies “mislead the merchants as to the services they will perform and the cost to the merchant, and they also conceal their relationships with the ISO Defendants and the fact that they or their affiliates are introducing these same merchants to merchant cash advance providers like Plaintiffs only to later induce those merchants to breach their agreements with their cash advance providers,” the complaint states.

Among the named defendants are:

- Corporate Bailout, LLC

- Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group

- PLG Servicing LLC

- American Funding Group

- Coast to Coast Funding, LLC

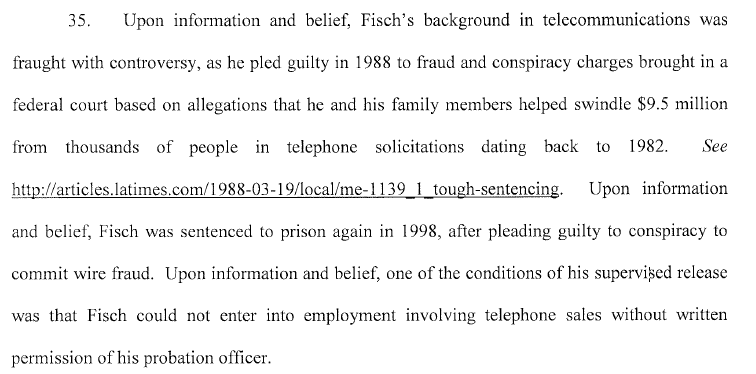

- ROC South, LLC

- Mark Mancino

Several defendants are already best known for running an office “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street,’” according to a salacious story that graced the back cover of the New York Post last month.

One paragraph of the complaint summarizes the allegedly collaborative scheme like this:

American Funding, Coast to Coast, […] (the “ISO Defendants”) are independent sales organizations (“ISOs”), companies that ostensibly support the merchant cash advance industry by brokering merchant agreements for companies like Plaintiffs. The ISO Defendants are anything but the proverbial “honest brokers.” As alleged below, they have partnered with companies that purport to offer debt relief services to merchants who have agreements with merchant cash advance companies like Plaintiffs. In practice, for these companies, “debt relief” is a code word for deceiving merchants to breach their existing agreements with Plaintiffs and to instead pay fees to these debt relief entities. In short, they scam merchants into believing that they can save them money when, in fact, they leave these merchants in financial shambles, while causing Plaintiffs to suffer millions of dollars in losses and future los[t] profits.

“’DEBT RELIEF’ IS A CODE WORD FOR DECEIVING MERCHANTS TO BREACH THEIR EXISTING AGREEMENTS”

Central to the plaintiffs’ claim is that they have ISO agreements with the defendants and that the defendants’ conduct is a breach of those agreements. The three causes of action alleged are tortious interference with contract, conversion, and breach of contract. Plaintiffs claim that 100 merchants with more than $3 million in outstanding balances are in breach of their contracts because of the defendants’ conduct.

The complaint was prepared and filed by attorneys at Proskauer, a 142-year old law firm founded in New York City.

Debt Relief Under Fire

The small business debt relief industry has been marred by scandal in recent years. In an unrelated criminal matter being handled in the Western District of New York, the owner of Corporate Restructure Inc. (no ties to Corporate Bailout) is currently residing in the Niagara County Jail awaiting trial on charges of conspiracy to commit mail fraud, wire fraud, bank fraud and money laundering for failing to deliver the debt relief services it charged for. In that case, United States vs. Sergiy Bezrukov, Bezrukov advertised that he could reduce a merchant’s short term debt by up to 75%. He is facing up to 30 years in prison. He was also previously a merchant cash advance ISO.

Two other MCA funding companies, Pearl Gamma Funding and Pearl Beta Funding, filed a lawsuit last November against another debt relief company that calls itself Creditors Relief. The complaint in that case also alleges tortious interference with contract and is still pending.

Meanwhile, a lawsuit filed in May by famous TCPA litigant Craig Cunningham against Corporate Bailout and Mark D Guidubaldi & Associates LLC went unanswered, according to court records. Cunningham, who alleged violations of telemarketing laws, filed for a default judgment against Corporate Bailout on September 12th.

Taking Advantage

Both Yellowstone Capital and Everest would not comment on the lawsuit they filed, citing pending litigation. Sources close to them, however, contend that both companies take matters that involve merchants being taken advantage of very seriously.

“When our own ISOs work directly in concert with companies that induce merchants to breach our contracts, that’s a problem,” said one source who did not wish to be named and was speaking generally about the recent introduction of debt relief service companies to the industry. “They’re taking advantage of businesses that can’t afford to be taken advantage of.”

An email sent by deBanked to Mark Mancino early Thursday afternoon, an individually-named defendant alleged to be affiliated with the other defendants, has not yet received a response. This story may be updated if a reply is received.

A COPY OF THE COMPLAINT CAN BE VIEWED HERE.

Is The End Near For This Debt Settlement Firm?

August 11, 2017 Corporate Bailout, a New Jersey based firm that purports to help businesses lower the monthly payments on their debts, is back in the news. This time it’s for allegedly running a sex-fueled office with stripper parties, sex dolls, and sexual harassment, according to the New York Post who published video footage of the debauchery. Warning: the New York Post link is not safe for work.

Corporate Bailout, a New Jersey based firm that purports to help businesses lower the monthly payments on their debts, is back in the news. This time it’s for allegedly running a sex-fueled office with stripper parties, sex dolls, and sexual harassment, according to the New York Post who published video footage of the debauchery. Warning: the New York Post link is not safe for work.

deBanked has written about Corporate Bailout previously, in one case recently where the company is alleged to be robo-dialing out of control. Corporate Bailout never responded to the lawsuit and the court entered a default against the company this past Monday, according to the docket.

Back in April, deBanked also received the recording of a call purportedly between a representative of Corporate Bailout and a small business owner. We had the lengthy dialogue transcribed and it appears below with the names between the parties changed.

Of note, the alleged Corporate Bailout representative in the call makes several references to a partner law firm named Protection Legal Group. There are several lawsuits pending against Protection Legal Group, one of which alleges the firm didn’t have a lawyer licensed to practice in the state they claimed to offer defense in. In that situation, a merchant had to hire another lawyer to sue his lawyer at Protection Legal Group.

| Person Answering Phone: | Hello. |

| Robo Agent: | Hello. How are you today? |

| Person Answering Phone: | I’m good. |

| Robo Agent: | Great! Can I speak to the business owner please? |

| Person Answering Phone: | Who is this please? |

| Robo Agent: | This is Alex from Corporate Bailout. Are they available? |

| Person Answering Phone: | Yeah. One second please. One second. |

| Robo Agent: | Thanks. |

| John: | Hello. |

| Robo Agent: | Can I speak to the business owner please? |

| John: | Speaking. |

| Robo Agent: | This is Alex from Corporate Bailout. I know your time is valuable. So, let me get straight to the point. We help small business owners eliminate their unsecured debts. If your business has taken a merchant cash loan or advance, a high interest credit card debt, accounts payable debt, or any other unsecured business debt, you are now able to settle your outstanding balances for just a fraction of what you owe. I just need to ask two qualifying questions. Okay? |

| John: | Sure. |

| Robo Agent: | What type of entity is your business registered as? LLC, Corp, etc.? Hello? |

| John: | LLC. |

| Robo Agent: | Do you have at least $25,000 in unsecured debt? |

| John: | Yes. |

| Robo Agent: | Great! It looks like you may qualify. Hold on one second while I get a specialist on the phone who can explain further. |

| [Phone Ringing] | |

| Derrick: | Hello. Hi. |

| Robo Agent: | Hi, I have someone here that is interested in moving forward. I will let you take it from here. |

| Derrick: | Thank you for that. My name is Derrick by the way. Who am I speaking with? |

| John: | John. |

| Derrick: | John, it’s a pleasure, John. So, John, go ahead and tell me a little bit. What kind of unsecured debt are you experiencing? Is this with cash advances? |

| John: | Yes. |

| Derrick: | All righty. And that’s our cup of tea. So, I wanna give you an example— |

| John: | What exactly— |

| Derrick: | …of exactly how this would work for you. |

| John: | Okay. Perfect. Yeah. |

| Derrick: | All right. Tell me how many advances do you have. Do you have one or a couple out there? |

| John: | I have 3. |

| Derrick: | 3. Okay. And what do you owe approximately in combined balances? |

| John: | About $85,000. |

| Derrick: | Okay. And lastly, what are they charging you daily? |

| John: | Total of about $2,000. |

| Derrick: | At this day? |

| John: | Yeah. |

| Derrick: | Okay. Obviously, they’re overextending you for sure. Now, you open these advances yourself? Is this your business, John? |

| John: | Yes. |

| Derrick: | Okay. What is it that you do? I just wanna get a better grasp of what’s going on. |

| John: | We’re a trucking company. |

| Derrick: | Oh okay. Yeah. Yeah. I work with a lot of trucking clients. All right. So, here’s the deal. I mean, at 85,000, knowing that these are cash advances, we’re able to reduce that down to about 63,000. Saving you well over 21,000 just on principal. |

| John: | How do I do that? |

| Derrick: | That’s very simple. I mean, what we do is we appoint you a power of attorney that represents the association. And what they’ll do is that by power of attorney they’ll contact your creditors in a form of hardship for you. Okay? And that’s the key word there because by law— And it doesn’t matter if it’s a cash advance or a Capital One Visa. Whoever that creditor is, whatever obligations you have to that creditor comes to an immediate halt. That means no more interest accruement. That means that whatever number I’m telling you by the time you hire us let’s say by today, that’s the number. Yeah. |

| John: | One second. Why does it come to a sudden halt if I have a contract with them? Like can’t they sue me for this? I mean, I signed a contract with them and everything. How is it legal to go and say that I can’t pay them? I’m not understanding you. |

| Derrick: | Well, #1, these are cash advances, which is highly unregulated. Everyone knows if you look into it. Okay? Everyone knows— |

| John: | I did. |

| [Crosstalk] | |

| Derrick: | Okay. Yeah. There you go. Well, they’re tiptoeing the line of legalities here by pressing [0:04:55][Inaudible] laws. That’s why we’re able to snatch them and nip them in the butt. Okay? When you are charging on a daily basis an overextended amount way past 25% APR, this is abuse. This comes to abuse now and we have to come at them in a form of hardship. By law, that’s what happens and everything comes to a halt right then and there. Now, they have to settle. Now, here’s the thing. I know you’re saying can they sue you. You know, they can. They can. Probability is very low. |

| John: | Why would I take the risk of getting sued? I mean, I’m just trying to understand. Is what you guys doing also legal? I mean, no offense, it sounds a little— |

| Derrick: | Oh yeah. |

| John: | This sounds a little less legal. What you’re doing sounds a little more illegal than what they’re doing because I really have a contract with them that I signed and I notarized. I mean, that is like legal documents. |

| Derrick: | Yeah. We give you a legal contract. It needs to be notarized and all that too. Okay? But here’s the thing. It is legal here. You’re working with the law firm. Okay? The law firm will then take that responsibility and make sure that they do reduce your debt size. Okay? It’s a cash advance. It’s a slam dunk every time. Who do you work with by the way? |

| John: | [0:06:15][Inaudible] I’ll give it to you in a couple minutes. Where did you get my information from? ‘Cause I usually get calls from them. Like this is the first call I’m getting from this type of company. Where did you guys get my information from? |

| Derrick: | So, we essentially look through UCC filings and UCC filings are only liens that are basic entry companies that normally take out cash advances. Normally. |

| John: | Right. |

| Derrick: | 9 times out of 10 when I see a UCC file that looks like yours and, you know, I’m usually right it’s a cash advance, so yeah. |

| John: | Which business were you referring to though? |

| Derrick: | I don’t know. I don’t know. Your phone call got transferred to me. So, we have several ways of finding new clients and one of them is that we have a database. People make outbound calls. I’m the one on the receiving end. I work with my clients one-on-one to get them enrolled, have them feel good about the program, and then I pass them along to the law firm. That’s my role here. So essentially, it happens like this, John. Right? Let’s say hypothetically today you’re like “You know what? This makes sense. I am in a hardship. I need to get out of this crap. All right, what do I need to do today?” I get you on board today just hypothetically. By Thursday because today is Tuesday— We need at least 48 hours. By Thursday, the law firm contacts you and they say, “You know, John, we reviewed everything. You know, you’re good to go. Let’s now help you stop making those payments so that way your bank no longer honors the ACHs you’re making daily. So essentially, by Thursday, we’ll put a stop, a complete halt to your payments. And then we can culminate maybe a week to 2 weeks before there’s any expense. And by the way, it will be a fraction of that cost. We’re talking at least 50% less in those payments. That’s how overextended they have you on. We don’t have to have that start for at least 2 weeks from today or whenever— |

| John: | So, in essence, I will still have to pay them. Just in a longer period of time you’re saying? |

| Derrick: | Right. Yeah. Well, we can work that out, but the whole point of this program is not to stress anybody. And that’s where the idea of a scam needs to be thrown out of the window. Okay? |

| John: | So, they’re scamming me you’re saying? |

| Derrick: | Yeah. I would say so. You don’t feel like you’re being highway robbed right now paying 2,000 a day? And I can give you even better numbers if I look at— you know, if I take a peek at the contract just to see the real numbers ‘cause on average they’re charging anywhere from 30 to 60 percent on a borrowed amount. That’s an average. I know you’re in that category. |

| [Crosstalk] | |

| John: | I understand, but I didn’t know about it that’s why I’m saying if I knew about all this, I can’t deny in court if they sue me. They do have a legal document against me. I mean, it is an issue. |

| Derrick: | Right. Well, here’s the good thing. I mean, people are in such a worse shape than you, John, that they’ll hire any company who’s gonna promise them that they’ll be able to negotiate, but the greater thing why this is such a more wise decision for you is that you’re not hiring a middle man. As a matter of fact, I can show you, okay, any agreements that we have. We provide litigation defense services on top of the settlement. So, if ever anything should happen, which being at 85,000 likely not, but if ever anything should happen, you have attorneys there that will show up in court for you, that will battle, that will counter lawsuit if we have to, whatever, drag out the process, whatever it takes. Whatever it takes. But at the end of the day if they wanted to sue you, you know how long a sue takes place or takes to convert? |

| [0:09:59] | |

| John: | I know, but— |

| Derrick: | It takes a long time. |

| John: | At the end of the day, I would still be found guilty that I did sign the contract. What defense could I possibly have for that? I’m just trying to understand what the legality is. |

| Derrick: | The defense is #1 it’s a hardship. If you look into that, hardships create a big deal in the law system. So, that’s #1. Number 2 is that this is technically not even a debt that you have. Check in on technicalities. They only purchase future receivables at expect it let’s say 2,000 a day. |

| John: | Yeah. And they also have a judgment against me though. |

| Derrick: | That is all scare tactics. That’s all. Confession of judgments you’re talking about, right? |

| John: | Yeah. Yeah. |

| Derrick: | Confession of judgment that you signed. Yeah. Yeah. Almost everybody signs a confession of judgment now. They just started implementing that the last 3 years. |

| John: | They can’t do anything with that? |

| Derrick: | Not when you have a power of attorney reaching out to them for settlement against the hardship cost. They can’t do that. |

| John: | Oh. |

| Derrick: | And if they use that– |

| John: | And also like with this document, they can like freeze accounts and they can freeze assets and stuff like that. But if you guys trick them and they can’t do that– |

| Derrick: | Yes. They won’t be able to. But if we need to take any preventative actions, your law firm, your adviser there will tell you to possibly change. |

| John: | So, you guys have a lawyer? You are the lawyer then? |

| Derrick: | I’m not the lawyer. I’m not the lawyer. I don’t do the negotiation. I told you my role here is just to get you on board so I can pass you to the law firm. That’s it. That’s my role. Give you the information– |

| John: | what’s your charge? |

| Derrick: | Okay. Good question, John. So, let me look at this number here again. I wanna give you something real. So let’s say it’s 85, right? 85,000 you owe. That gets reduced down to $63,340. That 63,000 is going to cover absolutely everything. That covers paying back your cash advances. That will cover for our services and fees all inclusive. Okay? The only reason why we’re able to do that, John, is because we are a nationwide law firm that does negotiations for cash advances specifically. That’s what Protection Legal Group does. And so, are you familiar with a class action lawsuit? Are you familiar with that? |

| John: | Yeah. |

| Derrick: | Okay. So, we approach settlements in that same format. Class action settlement is what we call it. So, essentially you’re one drop in the ocean. Right? And that’s why I wanted to ask you who you work with so I can give you references. But guaranteed we have, you know, up in the hundreds of clients in those cash advances that we have already control such a large portion of their funds. So, because we’re going to– Who do you have? do you have Swift? [inaudible] |

| John: | I’m not gonna reveal that information yet until I look into your company a little more only because it’s my first time hearing about this. I will look into this. I wanna speak with my lawyer about it and everything. But you were telling me it would be lowered to 63,000. That’s fine. |

| Derrick: | Yeah. That’s at most. |

| John: | What’s your fee? |

| Derrick: | Our fees are inclusive, John. I can’t tell you what it is until we submit everything, until we submit all the hard copies into the law firm |

| John: | What’s the percentage range? I mean, there’s gotta be some sort of number that I can go by. |

| Derrick: | Yeah. Yeah. I can give you a percentage. So, let’s say we reduce it down to 70 cents on the dollar, right? 42 cents of the dollar will go to your creditors. Okay? |

| John: | And the 28? |

| Derrick: | And 28 cents gets [0:13:58][Inaudible] up between the law firm and your attorney. It’s like 4 cents in a dollar to the attorney, 24 cents to the law firm. So, that’s how it works. Normally, that’s what they look to negotiate. |

| John: | So, you’ll get the 24, they get the 4? |

| Derrick: | That’s if they agree to that term. Yeah. The whole point is for your attorney to figure that out with the lender. At the end of the day– |

| John: | Isn’t that 24% on the dollar also? |

| Derrick: | No. No. On the 70 cents on the dollar that we reduce it. So, you have 85,000. Reduce it to 70 cents on the dollar let’s say. In that 70 cents, 42 goes to them. The remainder of the 28 is split. Right? 4 cents to your attorney, 24 to the law firm. So that’s the numerology of how it gets distributed. |

| John: | That’s 40% |

| Derrick: | Right. That’s how it gets– What is? |

| John: | The 28 cents on the 70 cents is 40%. |

| Derrick: | 40%? |

| John: | Yeah. |

| Derrick: | No. No. It’s smaller than that. |

| John: | Do the math. |

| Derrick: | If it were 40%– |

| John: | Do the math. You said 28. Do 28 divided by 70. |

| Derrick: | 28 divided by 70, 0.4. Yeah. 40%. So, what are we getting off here? |

| John: | So basically, you’re charging me 40% and they’re charging me the same 40%. So what’s the difference? I’m just trying to understand why– |

| Derrick: | No. Yeah. We’re making 40– Hold on. We’re making 40% of that 70%. They’re making 60% out of that 70 cents. I mean, if you wanna get in detail, that’s what it works down to. At the end of the day, the whole program cost for you is only 63,000. So, you make the decision whether you pay 63,000 or 85,000. |

| John: | And run the risk of getting sued. |

| Derrick: | No one touches–. No. You have a law firm that will fight and give you the litigation defense. |

| John: | Right. That’s not a–I understand that. I understand they’ll give it to me. But I also run the risk of losing. And if I lose, I would have to pay all their legal fees and that extra money that I know, you know, what trying to get out of. So, here’s what I’m gonna do. I’m gonna have to look into this a little more ’cause I’m not just gonna give all my information in a second. Can you send me some– |

| Derrick: | Yeah, that’s fine. |

| John: | …information so I can look it over? |

| Derrick: | What’s your best email, John? |

| John: | It’s [address redacted] |

| Derrick: | @gmail.com. Do you happen to be in front of a computer now? |

| John: | I do. Yeah. |

| Derrick: | All right. I just wanna make sure that you at least get it. I’m putting in the subject heading, ATTENTION John. This should be easy to find. So, you know, you can loo at– |

| John: | I just wanna make sure what it’s about. what is this for? What’s it called? |

| Derrick: | Debt relief I can put in there. Is that okay? |

| John: | Yeah. That’s fine. |

| Derrick: | I’ll put debt relief as well. Yeah. |

| John: | And this is from Mason & Hanger? |

| Derrick: | Mason & Hanger? |

| John: | Yeah. That’s where you’re calling from? |

| Derrick: | What’s that? No. No. Protection Legal Group is the name of the law firm. Protection Legal Group. |

| John: | Oh, it’s not Mason & Hanger? |

| Derrick: | No. I don’t know where you got that name. |

| John: | From the caller ID |

| Derrick: | Really? Mason & Hanger? I don’t know. That’s strange. You know, when I make calls out of the office, sometimes it comes out like– |

| John: | Are you gonna have your contact number over there or no? |

| Derrick: | Yeah, it’s in the email. Tell me if you have it now ’cause it says that it’s sent |

| John: | [Name redacted]? |

| Derrick: | [Name redacted]. Yup. that’s me. All right. So, there’s a summary of what we went over and then those things in bold would be what we need in order— if you wanna proceed forward, but the very first thing you’ll see in bold is the current cash advance agreement signed or unsigned. Very important. That’s what’s gonna help us approve you or not and see if we can fit you in the program. We have to look over the verbiage in there. You see one document attached. Right? |

| John: | Right. Right. |

| Derrick: | Do you see what’s in bold? Yeah, I have a few things in bold there that we require from you. Okay? The hardship letter is one of them that’s attached in there. But before all of that, we wanna take a look at a copy of the agreements you have with the 3 cash advances. It could be signed or unsigned. Your personal information is not gonna do us any good. We wanna see if we can approve you first. Okay? That’s all. It’s just by procedure. And then what we find in there, which only takes about 20 to 30 minutes to approve you, I can tell you, “Hey, John, you know, here are the real numbers, what we found based on your contract. Here’s what we can offer and here are your options.” And then we can come into an agreement together. The whole point of this is to get you off from paying— You’re paying 10 grand a week, man, you know. To get you off of 10 grand. Maybe down to 5,000. Whatever that number is that’s more comfortable for you and obviously is realistic for the law firm. Okay? |

| John: | You are basically just the broker for the law firm? |

| Derrick: | I’m their spokesman, you know. I’m their marketing arm. Not a broker or anything. If I were a broker, I’d have countless sources of different law firms that does this. |

| John: | I assume you have one law firm that you work with? |

| Derrick: | I only represent them. |

| John: | Who do you work with? |

| Derrick: | What was that? |

| John: | Who is the law firm that you work with? |

| Derrick: | Protection Legal Group. Protection Legal Group. You can put that down. |

| John: | Can you email me that information? I wanna make sure. It is in the email? |

| Derrick: | Yeah. It’s in the email. Yeah. Yeah. It’s all in there. |

| John: | Okay. Protection Legal Group |

| Call trails out into goodbyes… |

In the follow up email that came up from a corporatebailout.com address, Derrick said, “We have teamed up with nationwide law firm, Protection Legal Group, who will negotiate with lenders on your behalf. By enrolling in our program, we would reduce the total advance balances down to 70 cents on the dollar! But more importantly, we turn your daily payment into a ONCE a week payment, and reduce that amount by up to 50%!”

‘Debt Relief’ Company is Allegedly Robo-dialing Out Of Control

July 18, 2017 A lawsuit brought by famous serial TCPA plaintiff Craig Cunningham against defendants who allegedly robo-dial with offers for small business debt relief services, has a new twist, according to recent court records. That is that the defendants allegedly continue to robo-dial Cunningham despite having been served with the suit from him. All told, Cunningham says he has received at least 105 automated calls for the defendants’ business debt relief services despite the fact that he doesn’t even own a business.

A lawsuit brought by famous serial TCPA plaintiff Craig Cunningham against defendants who allegedly robo-dial with offers for small business debt relief services, has a new twist, according to recent court records. That is that the defendants allegedly continue to robo-dial Cunningham despite having been served with the suit from him. All told, Cunningham says he has received at least 105 automated calls for the defendants’ business debt relief services despite the fact that he doesn’t even own a business.

Cunningham filed an amended complaint that also added new defendants alongside Mark D. Guidubaldi, Corporate Bailout and Protection Legal Group. They include Sanford J. Feder and Cashflow Care, LLC.

Cunningham was one of several TCPA litigants referenced in a featured story deBanked published about TCPA lawsuits last October.

Protection Legal Group, meanwhile, was cited in another brief where a small business owner sued them for allegedly not providing the debt relief services promised. According to the docket, Protection Legal Group has yet to file an answer to it.

Debt relief and debt settlement services have become a booming business as of late, but it’s a risky endeavor. Earlier this year, four individuals were arrested when they did not actually attempt to negotiate the MCAs or business loans they were paid to assist with. One of those arrested is still in prison awaiting trial. He is facing a maximum of 30 years.

‘Debt Collection Terrorist’ Sues Protection Legal Group and Corporate Bailout

May 13, 2017 A new crop of supposed debt relief companies are beginning to take fire from all sides. In this latest case, Mark D. Giubaldi & Associates, LLC DBA Protection Legal Group and Corporate Bailout LLC, have once again found themselves on the receiving end of a complaint. On Wednesday, May 10th, Craig Cunningham, a once self-proclaimed debt collection terrorist and famous TCPA litigant, filed a lawsuit in the Northern District of Texas to seek out more than $1 million in damages for alleged unsolicited robocalls to his cell phone.

A new crop of supposed debt relief companies are beginning to take fire from all sides. In this latest case, Mark D. Giubaldi & Associates, LLC DBA Protection Legal Group and Corporate Bailout LLC, have once again found themselves on the receiving end of a complaint. On Wednesday, May 10th, Craig Cunningham, a once self-proclaimed debt collection terrorist and famous TCPA litigant, filed a lawsuit in the Northern District of Texas to seek out more than $1 million in damages for alleged unsolicited robocalls to his cell phone.

Cunningham, who goes by the screen name Codename47 on the fatwallet.com forum, previously authored a post titled, “TCPA enforcement for fun and for profit up to 3k per call” and is well known in the TCPA plaintiff community. In the complaint against Protection Legal Group and Corporate Bailout, he claims that they called him more than 50 times to ask about supposed “merchant cash advance loans” he had outstanding. The deeply troubling problem with that, according to the complaint, is that Cunningham doesn’t have any such thing.

When the calls connected to an agent, the Plaintiff was told that he was called by the defendants and told that according to UCC filings, they had noticed the Plaintiff had several merchant cash advance loans out. In reality, there are no UCC filings, and the Plaintiff has no merchant cash advance loans outstanding. In every call, the Plaintiff noticed a delay between answering the phone and the call connecting with a live person, which is characteristic of an automated telephone dialing system.

These are just some of many harassing calls the Plaintiff has received and as Defendants are just content to knowingly call what could be wrong numbers, or uninterested individuals and are blanketing the nation with these unsolicited calls.

[…]

Additionally, in the above referenced telephone calls, Defendants and their agents falsely claimed to have information regarding alleged UCC filings of Plaintiff, which don’t exist and were never made.

These calls were knowingly and willfully placed and the Defendants had or should have ascertained they were calling the wrong person.

Additional lawsuits currently pending against Protection Legal Group allege that the company is practicing law without a license in New York and interfering with merchant cash advance contracts.

Craig Cunningham v. Mark D. Guidubaldi & Associates LLC DBA Protection Legal Group, and Corporate Bailout LLC was filed in the United States District Court for the Northern District of Texas under case # 3:17-cv-01238-L.

A Tale of “Debt Restructuring”?

April 19, 2017 Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

The very next day, a merchant cash advance (MCA) company sued the merchant in New York for breach of contract, claiming that they were owed more than $300,000. And three months later, the merchant, represented by an attorney named Amos Weinberg, sued the first law firm that they hired. According to that complaint, filed on January 6, 2017, Protection Legal Group never even contacted the MCA company even though they were hired to negotiate with them specifically. Stranger yet, the merchant alleges that Protection Legal Group could not even have defended them in litigation because the MCA agreement’s jurisdiction was New York and Protection Legal Group has no lawyers that are licensed in that state. Naturally, the complaint further alleges that Protection Legal Group accepted payments anyway and has refused to return it.

The merchant’s new attorney, Amos Weinberg, is no friend to MCA companies, according to New York court records. Nevertheless, he offers harsh words for these new purported debt restructuring companies on his blog. “A growing industry that preys on people all over the country who are sued in New York is the debt resolution industry,” he wrote. “These companies promise to settle lawsuits for a portion of the sum sued by inducing the client to stop paying the creditor and instead pay sizeable weekly sums into an escrow account.” He then goes on to call out Protection Legal Group by name.

To summarize, a merchant hired a lawyer for an exorbitant fee to restructure their debts that weren’t debts, got sued and then had to hire a lawyer to sue their lawyer.

Protection Legal Group is also being sued by Forward Financing, an MCA company, for interfering with its contracts. That story has made the news in legal circles.

Court documents show that Protection Legal Group is fighting on another front as well since less than three weeks ago, a class action lawsuit (Case: 1:17-cv-02445) was filed against them for violating the TCPA. According to the complaint, they are allegedly marketing their services via pre-recorded voice messages to cell phones.

As an aside, most MCA contracts already permit merchants to have their payments lowered in the event that their revenues drop. Typically, they just need to send in their recent banking activity to demonstrate the drop and the MCA company will reimburse the merchant for anything collected above the specified percentage of sales. As this is a fundamental part of the agreement, the merchant shouldn’t require a debt negotiator or an expensive attorney to aid them with this.

Enrolling a Merchant’s “Debt” May Be Harmful… to the Merchant

March 29, 2017 How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

For merchants, the allure of a restructuring company’s help might just be payment terms tied to their monthly budget. That’s allegedly what one NJ firm’s agreement says, in fact. “I hereby authorize [the company] to negotiate my unaffordable business debts and to enter into affordable repayment terms on my behalf based on my monthly budget,” reads a document submitted in a New York Supreme Court case involving Creditors Relief. And based on the marketing materials deBanked has reviewed from several similar companies, their definition of debt is so broad that it can even include things that aren’t debt, like merchant cash advances, for example.

Even if the restructuring company held a critical view of MCAs and believed them to be loans, treating them as such for the purpose of negotiation might actually cause harm to their customers. That’s because a well-formed MCA contract already offers payment adjustments at regular intervals to appropriately match a merchant’s sales activity. Depending on what the language says, a merchant might just have to call their funder and ask them to reduce the debits to reflect their current sales activity. And yes this goes for ACH-only deals. Even ones that could appear to have fixed payments do not actually have fixed payments. This is basically how all MCAs work by the way, so if you are a broker or funder and this all sounds foreign to you, you need to take this course ASAP.

The point is this: a merchant need not pay a fee to an outside company to restructure anything when sales drop because a free remedy already likely exists and is a key benefit to MCAs in the first place. And yes, I’m talking about MCAs with daily ACH debits. If you’re confused by this, you need to take this course ASAP.

The best advice a restructuring firm can give a merchant struggling with an MCA due to slow sales is to tell them to look for a reconciliation clause in their contract that explains how to get the payments reduced. Once the merchant finds it, have them call the funder and execute it. There’s no need to enroll anything, negotiate anything, risk breaching a contract, or pay a broker tens of thousands of dollars in commissions. The debt restructuring firm might not want merchants to simply take advantage of what they’re already entitled to however, because they stand to make no money that way. In this regard, mischaracterizing future receivable sales as loans only serves to carry out their agenda to confuse merchants about what their rights might be under those agreements.

I myself, am occasionally contacted by merchants who claim to be facing hardship and in one instance where a merchant had spoken to a negotiator, the negotiator didn’t tell him that the remedy he sought was already a natural provision of his contract. I helped him find it. He didn’t have to pay any fees which would’ve gone to pay someone a huge commission or end up in some crazy situation where he’s being sued for breach of contract. Think about this the next time you encounter a distressed merchant. Not everything is debt and that can be very much to the merchant’s benefit.

If you work for a debt restructuring, settlement, or negotiation company, you should probably take this course too. It will help you understand MCA agreements and what remedies merchants already have at their disposal.

.JPG){kind=link}