MCAs Mentioned on SoFi’s Website

January 28, 2025Ever since SoFi launched a business loan marketplace last year, it has not been spoken about at length in its quarterly reports. It did not come up at all in its Q4 earnings call yesterday, for example. What is known is that it refers business owners to other sources for lines of credit, equipment financing, and more. However, there’s also an MCA screen on the scrolling window where it asks people to apply.

SoFi is notable in that it’s a bank, which is why it’s worth mentioning this at all. “Since acquiring our bank license in 2022, we’ve grown our deposits to $26 billion by iterating, learning, and iterating to make our product, marketing, and service better every day,” the company said yesterday.

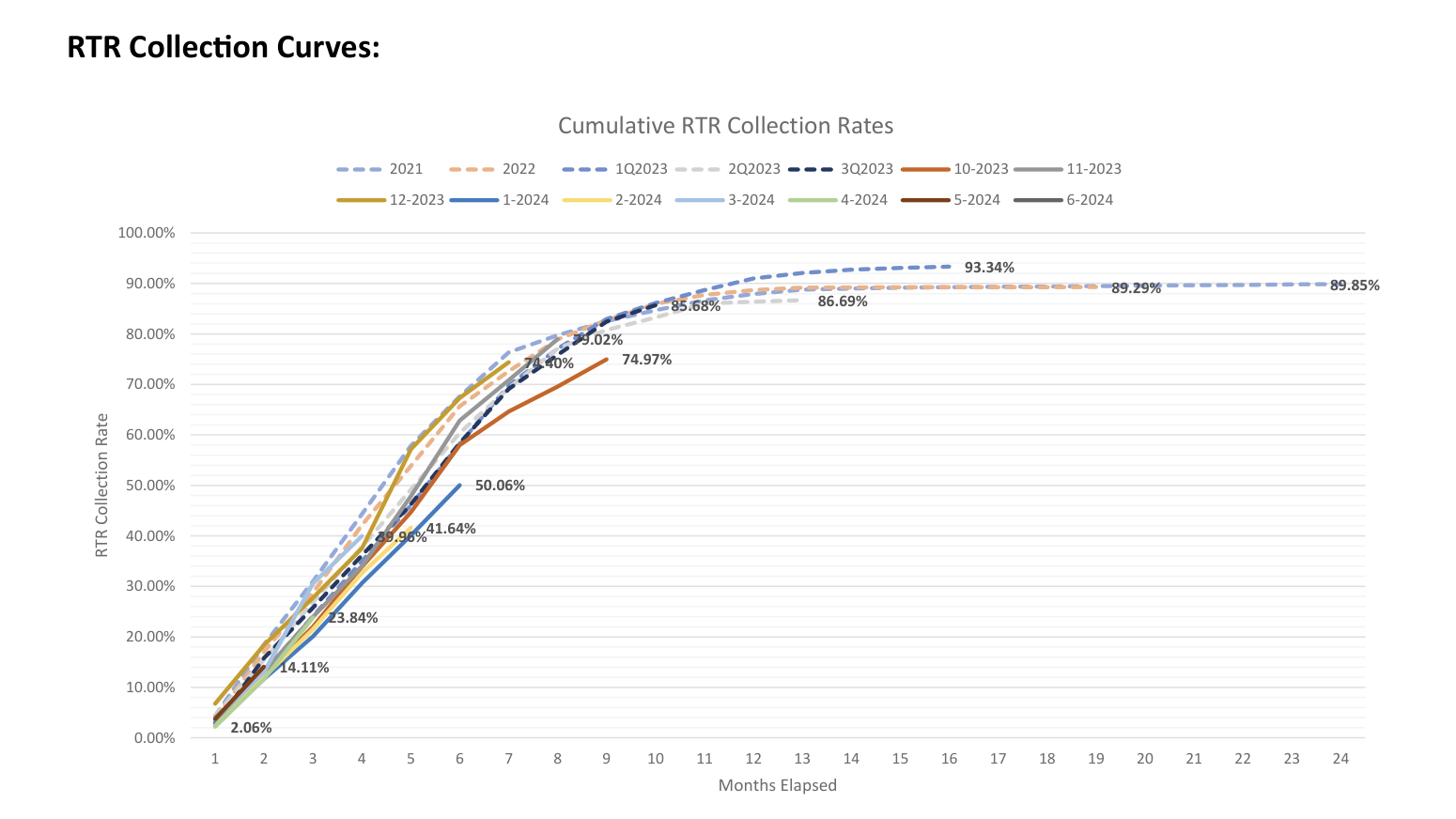

Are You Calculating Defaults Wrong?

January 22, 2025David Roitblat is the founder and CEO of Better Accounting Solutions, an accounting firm based in New York City, and a leading authority in specialized accounting for merchant cash advance companies.To connect with David or schedule a call about working with Better Accounting Solutions, email david@betteraccountingsolutions.com.

As we dive into tax season, it’s crucial for those involved in the merchant cash advance (MCA) industry to have a solid grasp of how to account for defaults. The way defaults are measured can significantly influence financial reporting and tax obligations, so understanding the different perspectives is essential.

There are several ways to evaluate defaults in the MCA industry, each offering different benefits depending on the context.

One common approach is the Right-to-Receive (RTR) perspective, which looks at the difference between the total payback amount agreed upon in a deal and what has actually been repaid.

For example, if a business secures $100,000 with a payback obligation of $150,000, and it repays $135,000, then there’s a remaining $15,000 that constitutes a default—a 10% shortfall from what was expected. This method is excellent for highlighting the gap between expected and actual returns, making it a valuable tool for financial modeling and long-term forecasting.

However, while the RTR method is strong for assessing contractual obligations, it can sometimes feel a bit too rigid. It often overlooks the real-world dynamics of cash flow and the impact of fees, which can give a skewed picture of a deal’s financial health.

Another method is the cash perspective. The approach simplifies things by focusing on whether the initial funding amount has been recovered. Using the same example, if the client repays $135,000, there’s no default recorded since the principal has been recovered. But if only $75,000 is paid back, that’s a 25% default based on the original funding. This approach is particularly handy for tax reporting because it zeroes in on principal recovery without complicating the picture with profit margins.

While straightforward, the cash perspective has its drawbacks. It tends to gloss over important details like origination fees and the overall financial implications of the repayment agreement, which can lead to an incomplete understanding of the deal.

Next, we have the wire perspective, which considers the actual amount transferred to the client after any deductions, such as origination fees. For instance, if a client gets $100,000 but pays a 10% origination fee, they effectively receive $90,000. If they then repay $75,000, the default is calculated based on the wired amount, leading to a 16.66% default rate. This perspective is particularly useful in syndication agreements, where understanding profitability post-fees is crucial.

Yet, like the cash perspective, the wire approach may miss the broader financial picture, focusing too narrowly on fees without accounting for total contractual expectations.

Each of these methods has strengths and weaknesses, but a comprehensive understanding of defaults requires a more detailed approach.

The percentage of payback perspective is the solution, calculating defaults based on the total percentage of the expected payback received.

In a scenario where the RTR is $150,000 and $135,000 is repaid, the default is 10% of the total payback amount. This method accounts for historical trends and repayment behaviors, offering valuable insights for portfolio management and financial forecasting. It allows us to estimate defaults based on historic defaults and post a percentage of the payback as the payments come as defaults. By incorporating both RTR obligations and cash flow realities, it balances the limitations of other methods.

For tax purposes, the cash perspective is practical, recognizing defaults as the shortfall between the funded amount and repayments. However, it oversimplifies the complexities of MCA financing by neglecting origination fees and RTR contracts. Similarly, the RTR perspective, while excellent for identifying contractual gaps, can be too rigid for broader financial analyses, as it does not consider upfront deductions or actual cash flow timing.

The percentage of payback perspective addresses these shortcomings, making it the most effective method for evaluating defaults across all scenarios.

A significant advantage of the percentage of payback perspective is its flexibility for financial projections.

Businesses can use past repayment data to estimate default rates across different portfolios, helping them align with long-term profitability goals. This is especially important in the merchant cash advance industry, where repayment patterns can vary widely. It also works well for situations involving origination fees or syndication agreements, ensuring those fees are factored into default calculations. By doing so, it avoids the distortions seen in cash- or RTR-focused analyses and provides clearer reporting for syndication partners on how their investments are performing. Although this approach requires more effort, its ability to offer accurate and nuanced insights makes it essential for MCA companies in today’s complex financial landscape.

This tax season, understand your accounting options, and leverage them to help you kick off an amazing 2025.

Revisiting the Merchant Cash Advance White Paper

January 21, 2025“Small and mid-sized businesses need cash flow to survive. A Merchant Cash Advance is a great tool to help them better manage and grow their businesses. But, like any other powerful tool, if used incorrectly, it can do more harm than good.”

That’s how the Industry White Paper, authored by AdvanceMe in 2007, began. At the time AdvanceMe was the largest such company in the industry. Some of the ideas and philosophies from this paper are timeless. If you’ve never seen it or want to retain a copy, you can download it here.

A Glimpse at Simply Funding

January 14, 2025 In around 2018 Jacob Kleinberger began calling merchants for a well known small business finance brokerage—a job he not only enjoyed but one that sparked his curiosity. “I always wanted to understand what my funders were doing,” Kleinberger says. He frequently asked questions to learn how decisions were being made across the board.

In around 2018 Jacob Kleinberger began calling merchants for a well known small business finance brokerage—a job he not only enjoyed but one that sparked his curiosity. “I always wanted to understand what my funders were doing,” Kleinberger says. He frequently asked questions to learn how decisions were being made across the board.

Though he worked closely with funders, being on the sales side didn’t give him the full picture. That changed in 2021 when an opportunity arose to join Simply Funding, a direct funder, as a partner. Today, he serves as Head of Operations.Transitioning from broker to funder was an eye-opener, leading Kleinberger to half-jokingly call the funders he used to work with to apologize for the challenges he had unwittingly created. Despite the learning curve, Kleinberger hit the ground running. Simply Funding, founded in 2017 by Bernard Mittelman, was a relatively small operation when he joined, but his mission was to help it grow. “We more than doubled the following year in funding and more than doubled the year after that,” Kleinberger says, reflecting the impact he’s been able to have with the team, which he’s said has been crucial to the success.

“We’re all a team, all here to show off each other’s strong points,” he says. For instance, the company already had a really good core foundation and underwriter in place when he got there.

The company describes itself as an A/B paper shop, with the majority of its revenue-based financing deals involving weekly payments, though they do daily payments as well. They also offer merchant processing splits.

Now a 28-person company, Simply Funding was originally located in Manhattan’s financial district but has since relocated to Jersey City. Kleinberger recalls the transition vividly, flying straight from the deBanked CONNECT Miami conference in 2023 to the new office to assemble all the furniture—an ordeal that lasted nearly 24 hours straight. One benefit of the move, he says, is access to a large talent pool in the area. But of course, it had to be accessible for the current team.

“A very big part [of the decision] was I had really good staff, and how would my staff come to work?” he says, since they make the whole operation hum. As a New York native from north of the city, Kleinberger is a commuter himself. The office now is just across the street from the PATH train station on the Hudson River. One can see the Simply team in person in the corporate high-rise there if they drop by.

“A very big part [of the decision] was I had really good staff, and how would my staff come to work?” he says, since they make the whole operation hum. As a New York native from north of the city, Kleinberger is a commuter himself. The office now is just across the street from the PATH train station on the Hudson River. One can see the Simply team in person in the corporate high-rise there if they drop by.

When asked about the importance of security at Simply, Kleinberger is unequivocal: “It’s the most important.” The company takes no chances with data access, even to the extent that Kleinberger himself refuses to store work-related information on a laptop. He also emphasizes the need for clear, unambiguous rules in business operations to ensure everyone understands expectations and outcomes.

The company has no inside sales force, so Kleinberger gets a thrill when an ISO seeks his help with merchant communication—it reminds him of his early days. However, he remains acutely aware that, since it’s the company’s funds on the line, transparency and directness with customers are non-negotiable. From his perspective, some brokers in the industry walk a fine ethical line, and he and the Simply crew are determined to ensure things are done the right way.

“I do feel like there needs to be something to help make brokers accountable,” he says. Despite the challenges, Kleinberger remains optimistic about the future and is excited about what lies ahead as Simply Funding continues to grow.

“I think 2025 is going to be a sick year,” he says.

Lightspeed: ‘MCAs continue to be popular’

December 10, 2024 “Lightspeed Capital revenue grew to $9.3 million from $4.2 million in Q2 of last year, up 121% year over year as the program continues to be popular with our customers,”” said Lightspeed CFO Asha Bakshani. “Lightspeed Capital offers fast access to capital and automatic repayment through Lightspeed Payments.”

“Lightspeed Capital revenue grew to $9.3 million from $4.2 million in Q2 of last year, up 121% year over year as the program continues to be popular with our customers,”” said Lightspeed CFO Asha Bakshani. “Lightspeed Capital offers fast access to capital and automatic repayment through Lightspeed Payments.”

“Overall, Lightspeed generated $277M in revenue for FY Q2 2025 of which only $9.3M was attributed to their MCA business (less than 3.5%). Still, the company says the extreme gross margins are creating a material impact for the business.

“We’re definitely seeing an impact from Lightspeed Capital,” Bakshani said. “I mean when we think about the numbers, and you’ll see them in our disclosure docs, we’re looking at high single digits per quarter in revenue. But because that comes in at 95% plus gross margins, it definitely has an impact already in offsetting both the residuals moving over to payments and also just more, more of our revenue coming in at Lightspeed Payments gross margin.”

Lightspeed is a publicly traded retail POS company with a current market cap of $3.68B CAD and $105M in MCAs on its balance sheet.

Smaller Funder? How to Get Fast Tracked With Big Investors

December 4, 2024Looking for big money? As a smaller funder your simple financial reports might not cut it when it comes to big investors. In fact, it’s a complaint frequently made by investment bankers and institutional funds looking to get capital deployed in the revenue-based financing space.

“Smaller originators face three key hurdles: first, the lack of institutional-grade portfolio performance and consistency; second, limited data operations and analytics capabilities; and third, a shortage of affordable resources and expertise to close these gaps and engage effectively with capital markets,” said Tomo Matsuo, Managing Partner of AdvanceIQ.ai., “AdvanceIQ.ai was launched to address these challenges head-on through tailored solutions like our new Portfolio Pulse product.”

The Portfolio Pulse is a simple yet robust tear-sheet product that delivers a high-level, third-party validated snapshot of portfolio performance. Designed as a cost-effective tool, it helps funders build credibility and engage institutional investors with confidence. Seamlessly integrating with most industry CRMs, it generates investor-ready metrics tailored for early-stage conversations, enhancing transparency and trust.

But Portfolio Pulse is just one piece of AdvanceIQ.ai’s broader suite of tools. From risk scoring and intelligent lead routing to dynamic portfolio analytics, AdvanceIQ.ai equips funders with the insights and resources to scale efficiently while building investor confidence. These offerings include tools like the SMB Risk Index (SRI), a proprietary scoring system designed for the SMB AltLending sector to predict and enhance asset performance.

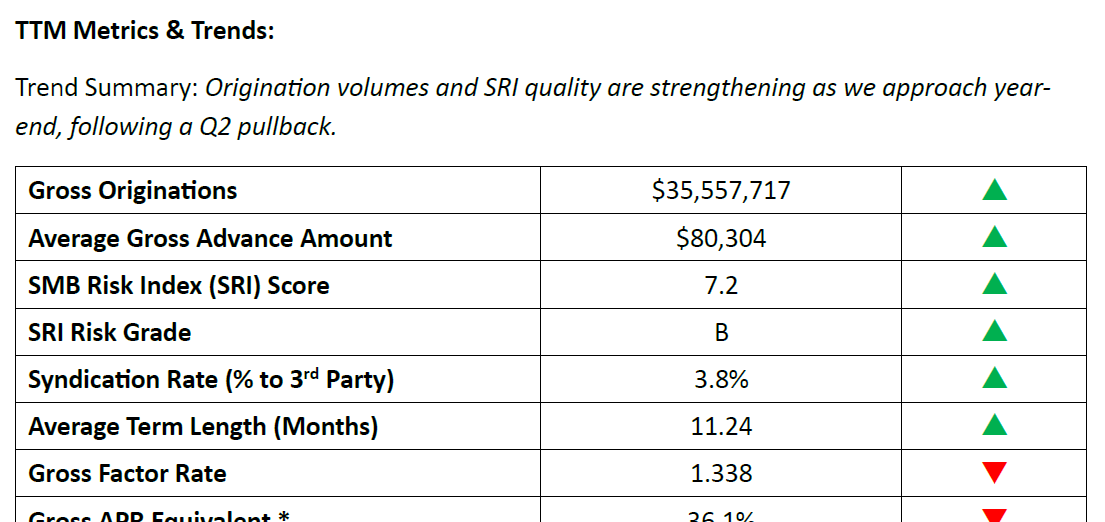

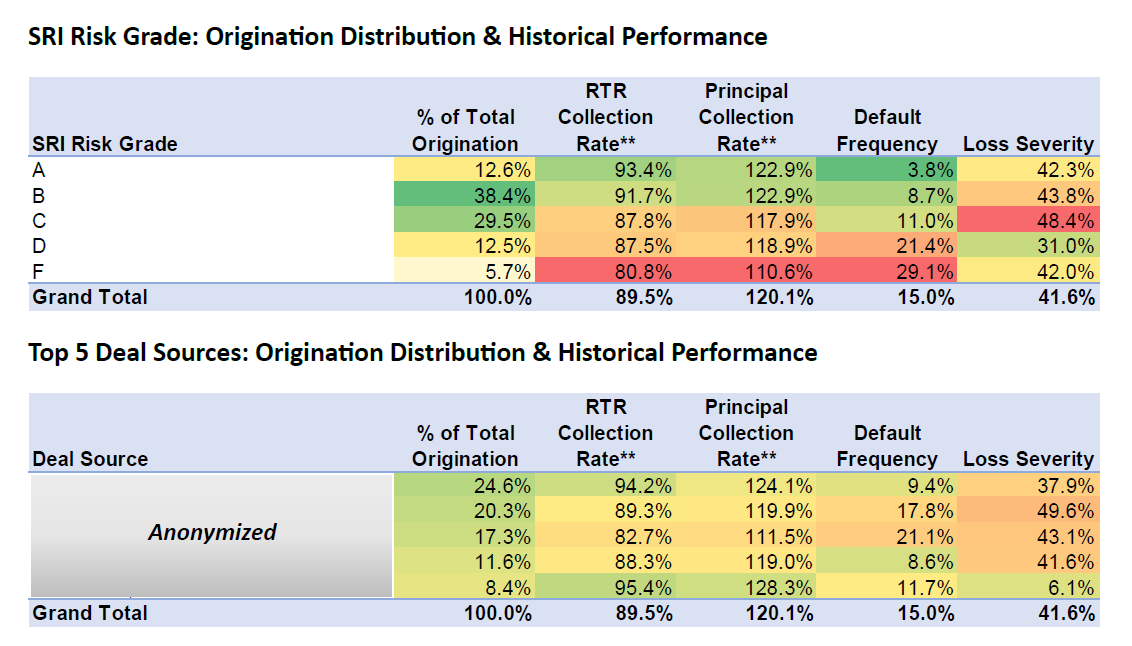

Excerpts from Portfolio Pulse:

• Trailing twelve-month (TTM) origination metrics and performance trends.

• Distribution and performance insights segmented by key attributes, including the proprietary SMB Risk Index (SRI).

• Historical repayment trends via collection curve analysis.

“High-quality reporting is an essential first step for smaller funders to break into institutional markets,” Matsuo noted. “Our goal is to provide the transparency and insights that empower them to succeed.”

With deep experience in the SMB AltLending space, Matsuo is no stranger to the challenges funders face. “Having been involved in raising and managing hundreds of millions of dollars in both debt and equity, I’ve seen how difficult it can be for smaller originators to stand out. AdvanceIQ.ai’s offerings are designed to remove those barriers and position them for growth.”

Rewarding Loyalty in Revenue Based Finance

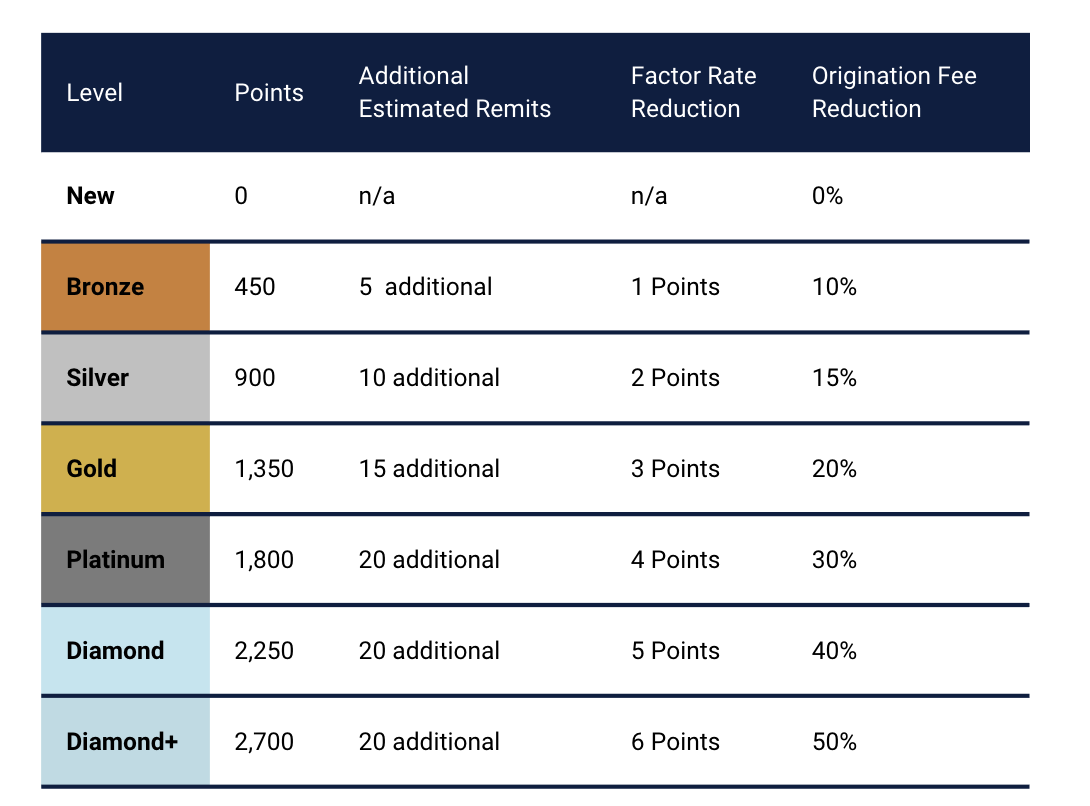

November 13, 2024 Everyone’s heard the pitch that if a deal goes well there could be better terms on the next one, but how much better are we talking about precisely? Well, after conducting an internal study, Pennsylvania-based Funding Metrics decided to actually codify incentives for success into a fully fledged loyalty rewards program that enables merchants to get a precise factor rate reduction, origination fee discount, and additional estimated remittances on subsequent advances.

Everyone’s heard the pitch that if a deal goes well there could be better terms on the next one, but how much better are we talking about precisely? Well, after conducting an internal study, Pennsylvania-based Funding Metrics decided to actually codify incentives for success into a fully fledged loyalty rewards program that enables merchants to get a precise factor rate reduction, origination fee discount, and additional estimated remittances on subsequent advances.

“Early 2023 we took a deep dive into our customer experience and how it directly correlated to merchant retention,” said Melissa Flagg, Vice President of Operations for Funding Metrics. “We listened to the pain points our ISOs shared, with customer retention always driving the conversation. Most ISOs we spoke with seemed to face similar retention challenges and were coming up short with solutions.”

The challenge is that merchants tend to shop around on subsequent deals even if they are happy with what they got the first time. The loyalty program was the eventual outcome of what they learned and it’s open to merchants funded by Lendini and Quick Fix Capital. As Flagg tells it, there are three ways for merchants to accrue points. First, points simply for opting in, which they must do in order to take advantage of it. Second, additional points for each 1% they remit toward the purchased amount, and third, points for each renewal. There are six total milestones that range from Bronze Level to Diamond+ Level. While the tiers, conditions, and corresponding discounts are published right on their website, merchants can easily track their points through the Funding Metrics mobile app.

“There’s no need for a redemption email or request,” said Flagg. “Points don’t deduct, they continually accrue as long as merchants continue to remit, and discounts automatically associated with the loyalty level apply on their next offer.”

She added that it’s quickly been recognized as a great way to incentivize a merchant not to shop around. It’s also been used to secure a renewal or win back an old customer that had left. This logically helps the ISOs involved.

Most readers are already familiar with the Lendini brand through their constant mix of on- and offline marketing. Members of their team usually show up in large numbers at major industry events, for example. Flagg said that 2024 has been a big year for the company. “In Q2, we successfully launched Instant Offers, and we’re proud to report that we’re now averaging a turnaround time of under 5 minutes for offers up to $75,000,” she said. Their new mobile app, while still in beta, allows merchants to track offers, remittances, and engage with the Resolutions Team.

“Over the past two years, we’ve prioritized elevating the customer experience by creating accessible tools that empower merchants to navigate the financing process with ease and transparency,” Flagg said. “This is only the beginning. Funding Metrics is dedicated to continuously enhancing these experiences that put merchants in greater control of their business financing and making every step from offer to origination as seamless as possible.”

OppFi Encouraged By Early Results With Bitty

November 10, 2024OppFi achieved a new record in Q3.

“The record quarterly net income was a result of credit initiatives that continue to drive strong loss payment and recovery performance, marketing cost efficiency and prudent expense discipline across the organization,” said OppFi CEO Todd Schwartz during the quarterly earnings call. One part of that organization is Bitty Advance, which it acquired a 35% stake in this past summer. “We are encouraged by the early results and potential opportunity of this platform and the strength of our relationship with Bitty,” Schwartz said of the progress so far. “We continue to explore similar opportunities that would be accretive and align with OppFi’s strategic vision.”

One analyst on the call inquired further about what similar opportunities Schwartz might be referring to on the M&A front. Schwartz responded with the following:

I mean I think whatever it is, it’s got to be something that’s highly accretive. I mean, OppFi’s vision is to be a platform for digital alternative financial service products where we see large supply-demand imbalances in large addressable markets. There’s definitely different profiles of business out there, different situations are pretty — it’s pretty bespoke, but we’re prepared to handle either-or. So it has to make sense for us, though. And obviously, we’re going to protect and mitigate risk with anything we do to make sure that it’s successful and make sure that we’re going to be getting a return on our capital and it’s highly accretive to shareholders.