Shopify Capital: $1.4B in Business Loans and MCAs in Q1

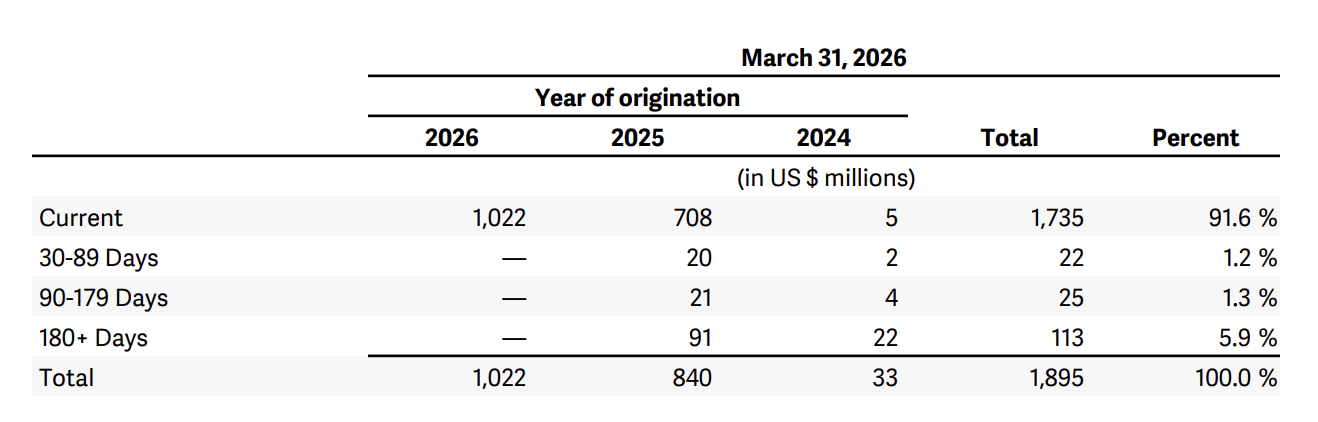

May 5, 2026 Shopify’s business loan and merchant cash advance offerings continue to increase. This follows a consistent decade-long rise with no down years. In Q1, the company originated $1.4 billion in business loans and merchant cash advances, up from $821 million YoY. Based on the weight of the respective receivables, the product mix is roughly 82% loan-based and 18% MCA.

Shopify’s business loan and merchant cash advance offerings continue to increase. This follows a consistent decade-long rise with no down years. In Q1, the company originated $1.4 billion in business loans and merchant cash advances, up from $821 million YoY. Based on the weight of the respective receivables, the product mix is roughly 82% loan-based and 18% MCA.

Of the loans it originated in 2025 that still have an outstanding balance, 10.8% were more than 6 months behind on their original payment schedule as of March 31, 2026.

Delinquency chart in in the Q1 docs:

Merchant Cash Advances Excluded From CFPB Small Business Loan Data Collection

May 1, 2026Merchant Cash Advances are now excluded from the CFPB’s small business loan data collection requirements. In the final rules filed by the agency on April 30th, the previous proposal to exclude MCAs from Section 1071 is now deemed approved and final.

“Since MCAs are not covered credit transactions under this final rule, no MCA providers will be required to report,” the docs say. The rationale is discussed across the 314 pages that comprise the final decision. However, the agency did leave open the possibility to reconsider the inclusion of MCAs years down the road.

But for now after more than a decade of debate and confusion over the matter, MCAs will not be considered a covered credit transaction for the purpose of Section 1071 of the Wall Street Reform and Consumer Protection Act. You can read the final rules here.

What the Velocity Capital Group Announcement Revealed

April 21, 2026 Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

The firm says it operates in all 50 states and is actively preparing to extend its model globally, with origination volumes projected to continue accelerating through 2030. As part of that, VCG has hired Michelle Melo as Director of Financial Operations & Capital Markets.

deBanked has been covering VCG’s expansion since 2018, starting with a profile that captured CEO Jay Avigdor’s rise from solopreneur to a large office on Long Island. At the time, Avigdor told deBanked: “We crawl before we walk before we run.” The company now appears to be in a full sprint as it looks globally.

This past February, Velocity Capital Group’s booth at deBanked CONNECT MIAMI included a surprise guest appearance from NBA All Star Bam Adebayo. Now with its recent big hire of Melo, Avigdor says, “VCG’s tech- and data-powered platform is scaling faster and more efficiently than nearly any peer in our category, and Michelle is here to institutionalize that advantage. She will drive pre-securitization discipline, standardized reporting, and the investor relationships we need to remove scaling friction and enable the next generation of growth. With Michelle on board, VCG is significantly closer to achieving our target of $1 billion in annual originations.”

Audit Season Is Coming: How to Get Your MCA Books Ready Before the Panic Starts

April 20, 2026David Roitblat is the founder and CEO of Better Accounting Solutions, an accounting firm based in New York City and a leading authority in specialized accounting for merchant cash advance companies. To connect with David or schedule a call about working with Better Accounting Solutions, email david@betteraccountingsolutions.com.

Audits do not create problems. They reveal them. This distinction matters more than most funders realize, because the panic that accompanies audit season rarely stems from the auditor’s requests. It stems from the gap between the order a company believes it has and the order it actually keeps.

Audits do not create problems. They reveal them. This distinction matters more than most funders realize, because the panic that accompanies audit season rarely stems from the auditor’s requests. It stems from the gap between the order a company believes it has and the order it actually keeps.

A funder in Chicago learned this one March when his auditor sent a routine request: ten funded deals, their supporting documents, and the corresponding bank activity. He expected the ask. What he did not expect was how long it took his team to assemble everything. Three merchant applications were missing pages. One deal had two payoff letters saved under different names. A renewal had been recorded without a clear link to the original advance. Nothing was catastrophic, but everything took longer than it should have. He looked around the conference table and saw the same realization on everyone’s face. The audit had not made the mess. It had simply exposed it.

This is how most MCA shops encounter audit season. The good news is that readiness does not require special software or a large finance team. It requires discipline in daily habits long before the auditor appears.

Reconciliation of RTR balances is a natural starting point. Many funders assume their balances are accurate because the CRM shows a clean number. In practice, reconciliation depends on tight alignment between the CRM, processor reports, and the accounting ledger. If any of these sources lag by even a few days, mismatches will begin to form. A merchant’s payment might fail on Friday, get resubmitted Monday, and post to the ledger Tuesday. Without consistent reconciliation, the funder sees one story while the auditor sees another. A steady daily or weekly routine of matching processor deposits to merchant balances prevents these gaps from widening into explanations nobody wants to give.

Wire activity demands the same attention. Funding wires, collections wires, reserve transfers, syndicator payouts: each touches different parts of the books. A company that does not document these movements as they occur eventually faces a stack of transactions labeled simply “funding” or “payout,” requiring backward reconstruction that consumes hours. One funder discovered that three wires recorded as syndicator payouts were actually renewals paid in error from the wrong account. Small mistakes, but they created lengthy explanations. A simple internal rule that every wire must carry an attached note and supporting detail at the moment it is sent eliminates that uncertainty before it takes root.

Syndicator splits introduce their own complications. When multiple investors participate in a deal, the funder becomes responsible for tracking each share of principal and returns with precision. Problems arise when the initial split is entered inconsistently, or when renewals process without correctly updating the syndicator’s residual balance. During audits, these discrepancies stand out immediately. One company maintained a separate spreadsheet for syndicator participation because their CRM could not display multi-party splits cleanly. The spreadsheet worked until the team member who managed it went on leave. No one else understood the logic. The audit revealed not a major error, but a process built around one person instead of a system. Auditors look for evidence that the company can reproduce its numbers without depending on any single employee.

Default classification is another area where funders frequently fall behind. A delayed payment can linger in active status for weeks because no one wants to mark it as default prematurely. But when the auditor reviews the file, unclear classification becomes a problem. The funder must show when the merchant became delinquent, what outreach occurred, and how the remaining balance is being treated. A restaurant in Texas once stopped paying for three weeks. The collections notes lived in the account manager’s personal notebook instead of the CRM. The auditor flagged the discrepancy because the books still showed the merchant as active. Proper classification helps the funder understand portfolio behavior and demonstrates to the auditor a clear, consistent process.

Underlying all of this is documentation quality. Merchant applications should align with the funded terms. Bank statements should be complete. Contracts should be saved with names that make sense across the team, not names that make sense only to the person who downloaded them. Renewals should show the payoff, the redeployment of capital, and the new terms in one complete package. Missing pages, duplicated files, and vague naming conventions do not cause financial harm directly, but they slow the audit and weaken the impression of professionalism. A well-organized document library is one of the simplest ways to make an audit move smoothly.

Internal controls play a larger role than many funders expect. An auditor does not expect a small MCA company to maintain the same segregation of duties as a large financial institution, but they do expect clear responsibilities. If the same person initiates payments, reconciles bank accounts, and approves adjustments, the company has created unnecessary risk. Even a small team can separate duties by establishing checkpoints. One person prepares the payout. Another reviews it. A third reconciles the bank activity. These controls do not exist to catch wrongdoing. They exist to make wrongdoing difficult in the first place.

The habits that lead to a smooth audit cannot be assembled the month before it begins. They must be woven into ordinary operations throughout the year. A weekly ten-minute review of aging reports reveals shifts early. A monthly check of syndicator exposure confirms whether splits were entered correctly. A simple rule that every merchant contact must be logged before the end of the day prevents confusion when questions arise later. At Better Accounting Solutions, we encourage clients to think of these routines not as audit preparation but as as the proper way to run a business. The audit simply confirms what healthy habits have already produced.

Audit readiness benefits the team in ways that extend beyond the audit itself. When systems are disorganized, staff spend more time defending their work than improving it. When information scatters across folders and inboxes, no one feels fully in control. A clean, disciplined financial environment reduces stress for everyone. New employees learn what good work looks like because the system teaches them. Managers spend less time searching for answers and more time interpreting what the answers mean.

Audits also shape how capital partners view the company. Syndicators and institutional investors frequently request audit reports before deepening their commitments. A clean audit signals stability and transparency. A messy one does not automatically disqualify a funder, but it raises questions that take time and credibility to resolve. A funder who treats the audit as part of their annual rhythm presents a stronger case to partners than one who treats it as an interruption to be survived.

Many funders approach audits with dread. The dread usually fades once the process begins, because audits do not invent problems. They surface them. And once surfaced, problems can be fixed. Funders who treat findings as guidance rather than criticism tend to grow faster. They catch issues earlier. They build stronger infrastructure. They develop habits that improve performance year-round rather than only during preparation season.

In an industry where capital moves quickly and margins shift without warning, reliability becomes a competitive strength. A company with clean books makes better decisions. It moves faster because it spends less time reconciling its own history. It communicates more clearly with partners because its numbers are organized and honest. Audit readiness has less to do with pleasing an auditor and more to do with strengthening the structure that supports every advance.

The calmest funders during audit season are not the ones with perfect portfolios. They are the ones who built habits long before the auditor arrived. They did the small things consistently. They documented what they did. They noticed discrepancies and addressed them. Audit season becomes a checkpoint instead of a crisis. And the company emerges stronger each year because clarity became part of how it operates.

229 Companies Now Registered as Sales-Based Financing Providers in Virginia

April 20, 2026Almost four years since Virginia’s sales-based financing provider law went into effect, the state now lists 229 registered parties. That’s an increase of only 27 companies since last year.

Both funders and brokers are required to be registered if they intend to transact with Virginia-based merchants, subject to some exceptions. Registrants on the list include some big recognizable names like eBay Commerce, First Data Merchant Services, PayPal, and Wal-Mart.com USA, but dozens of smaller known MCA broker shops also appear.

If you are a broker or funder in MCA and are not registered to do deals with Virginia-based merchants, you should contact a knowledgeable industry attorney to get set up right away. The law went into effect in 2022.

Don’t Get Sued in Merchant Cash Advance. Christopher Murray to Speak at Broker Fair 2026

April 16, 2026

The highly acclaimed industry attorney Christopher Murray will be speaking at Broker Fair on June 1 in New York City for a special solo session. As one of the most seasoned litigators in MCA, Murray stands to bring especially unique insights.

Work in MCA? You won’t want to miss this! REGISTER HERE!

Christopher Murray’s bio:

Christopher Murray is a graduate of SUNY Buffalo Law School (JD, cum laude) and University of Delaware (BA). He is admitted to practice law in the states of New York, Pennsylvania, and Connecticut, the United States District Courts for the Southern and Eastern Districts of New York, and the United States Second Circuit Court of Appeals. Mr. Murray is a founding member of the Alternative Finance Bar Association and a member of its board of directors. Prior to founding Murray Legal, PLLC, he represented commercial creditors at two prominent boutique commercial litigation firms in New York.

Mr. Murray has litigated over one hundred cases on behalf of non-bank commercial finance companies. Mr. Murray regularly represents clients with regard to loans, factoring, receivables purchases and merchant cash advance transactions. He is also an experienced appellate litigator, having litigated and defended against multiple appeals in state and federal courts.

Mr. Murray regularly represents: commercial clients in litigation, mediation, and arbitration; receivables purchasers and commercial lenders against breach of contract, fraud, UDAAP, and RICO claims; merchant cash advance clients pursuing breach of contract claims; claims against former employees and contractors for breach of non-compete and non-solicitation agreements; and creditors in actions and special proceedings challenging collections and judgment enforcement. Mr. Murray also represents clients in various corporate and regulatory matters.

Speed to Lead, Closing the Deal, and Running an ISO Shop

April 15, 2026 I sat down with Nicole Cruz, CEO of Redline Capital Inc, a brokerage based in in Secaucus, New Jersey. Cruz spilled some of the secret sauce, including what happened when she tried lead sources that her peers and competitors adamantly claimed weren’t good. Cruz started in the industry in 2018 and worked as a sales rep and ISO rep before trying her hand at starting her own company. One of the signature elements of their sales culture is the daily “power hours” they have. When I arrived on site, they were in the middle of one. She explains it all and more in our talk.

I sat down with Nicole Cruz, CEO of Redline Capital Inc, a brokerage based in in Secaucus, New Jersey. Cruz spilled some of the secret sauce, including what happened when she tried lead sources that her peers and competitors adamantly claimed weren’t good. Cruz started in the industry in 2018 and worked as a sales rep and ISO rep before trying her hand at starting her own company. One of the signature elements of their sales culture is the daily “power hours” they have. When I arrived on site, they were in the middle of one. She explains it all and more in our talk.

You can follow Cruz on her Instagram here.

While we’re posting some short video snippets across social media, you can listen to the full thing on Spotify while you’re on your commute.

Also, make sure you’re registered for Broker Fair, coming up on June 1 in New York City! Brokerfair.org.

Pipe Originated $300M in MCAs in Last Two Years, Bouncing Back

April 9, 2026 Pipe originated $300M in merchant cash advances in the last two years, the company revealed. The figure was presented in its announcement that it has raised a fresh $16M round of capital. The $300M in MCAs was spread across 15,000 merchants.

Pipe originated $300M in merchant cash advances in the last two years, the company revealed. The figure was presented in its announcement that it has raised a fresh $16M round of capital. The $300M in MCAs was spread across 15,000 merchants.

“Pipe has built the infrastructure that small business financing should have had from the start; AI-native, partner-embedded, and easily accessible for the tens of thousands of businesses that have been told for too long they’re not worthy of capital,” said Pipe CEO Claurelle Rakipovic in the official release. “Pipe has kept its ambition while operating with a clear focus on the customer and fiscal discipline. That combination puts us in a powerful position. This new capital gives us the fuel to move faster on what’s already working as we continue to create a better future for small businesses.”

Pipe’s funding volume is actually lower than it used to be. In 2021 they shared that they had originated $1.2B in MCAs in a single year. At the time Pipe marketed itself as the “Nasdaq for revenue” and called its employees “plumbers” instead of sales agents, underwriters, and engineers. After raising $300M at a $2 billion valuation, fintech reporter Jason Mikula shared that the company had generated only $7.1M in revenue in 2024. Layoffs followed.

The new announcement says that revenue tripled in 2025 and that its “embedded financing” product relaunched in 2024. With the $16M round and several new board members, the company appears to be on a corrective return back up.