The Most Common Mistakes MCA Companies Make Early On, and How to Avoid Them

February 27, 2026David Roitblat is the founder and CEO of Better Accounting Solutions, an accounting firm based in New York City and a leading authority in specialized accounting for merchant cash advance companies. To connect with David or schedule a call about working with Better Accounting Solutions, email david@betteraccountingsolutions.com.

Most MCA companies that fail do not do so dramatically. They erode. The founder looks back after eighteen months and wonders how a business with so much early momentum ended up struggling for liquidity and chasing syndicator trust it somehow lost. Half its energy goes toward untangling records that should have been clean from the start. The answer is almost never a single catastrophic decision. It is a sequence of small ones, each reasonable in isolation, that compound into structural weakness.

Most MCA companies that fail do not do so dramatically. They erode. The founder looks back after eighteen months and wonders how a business with so much early momentum ended up struggling for liquidity and chasing syndicator trust it somehow lost. Half its energy goes toward untangling records that should have been clean from the start. The answer is almost never a single catastrophic decision. It is a sequence of small ones, each reasonable in isolation, that compound into structural weakness.

I think of a young funder in New Jersey who reviewed his first ten funded deals about three months in. Several merchants were falling behind at nearly the same point in their terms. His underwriting notes, scattered between email threads and a spreadsheet he kept meaning to organize, offered no explanation. Nothing was broken exactly. But nothing lined up either. He had volume. He had brokers sending files daily. He had energy. What he did not have was a process that could teach him anything. The warning signs were already there, small and easy to dismiss, expensive to ignore.

This is how early lessons arrive. Not as crises, but as patterns that take shape slowly and reveal themselves only in hindsight.

The most common early mistake is stretching advances to win deals. A new funder feels pressure to grow, to prove they belong in the market. A merchant asks for more than the bank statements justify. A broker insists the file is clean, that steady work is lined up for next month, that the deal will perform. The funder approves the higher amount, reasoning that a larger fee compensates for the added risk. Weeks later, repayment starts slipping. By the time the weakness becomes undeniable, the funder realizes the pricing never reflected reality. This does not happen once. It happens across a dozen files, each approved with the same hopeful logic. Stretching becomes a quiet bleed on cash flow that can destabilize a young portfolio before anyone fully understands what went wrong.

Reserves present a related trap. Many funders hear performance benchmarks from brokers or peers and assume their own book will behave similarly. They reserve lightly because they want capital moving, or because early merchants seem stable. Then the first real default arrives, followed quickly by two more. The funder scrambles to cover obligations from operating cash, and suddenly the business has no cushion. Adequate reserves are not pessimism. They are acknowledgment that early portfolios behave unpredictably. A new company must protect itself long enough to learn the patterns unique to its own underwriting. That learning takes time, and time requires liquidity.

Syndicator relationships suffer their own form of neglect. Many companies treat outside capital as fuel, assuming the relationship will sustain itself as long as returns look acceptable. Reporting gets delayed because the funder is busy elsewhere. A few numbers fail to reconcile, and the explanation comes later, once there is time. A question sits unanswered for days because the team is stretched thin. None of this feels catastrophic in the moment. But syndicators notice. They remember which funders communicate clearly and which require chasing. A company that cannot deliver timely, organized information will struggle to attract the deeper commitments that make real scaling possible. Trust, once damaged, rebuilds slowly.

Recordkeeping is another early fragility, and perhaps the most underestimated. Companies store documents wherever convenient. Underwriting notes live partly in one CRM field, partly in a manager’s notebook, partly in an email thread nobody can find. Bank statements get downloaded twice under slightly different names. Merchant calls get logged sporadically or not at all. This scatter creates a version of the portfolio that cannot be reconstructed when questions arise. When a renewal decision needs context, or a payment dispute requires history, the funder spends more time searching than thinking. The real cost is not inconvenience. It is the loss of insight. Without organized records, the business cannot learn from its own decisions. It repeats mistakes because it cannot see them.

A subtler confusion appears around accounting itself. Early funders often rely on a basic bookkeeping setup that captures revenue and expenses for tax purposes but reveals nothing about deal-level behavior. They know how much was deposited in their account last month but they don’t know how much they have actually earned. They do not know how much came from renewals versus new advances. They cannot see aging by cohort or measure actual recovery on RTR. This blindness forces leadership to operate on instinct precisely when the business needs measurement. Tax accounting satisfies the IRS. Performance accounting informs the funder. They are not the same thing, and treating them as interchangeable is a mistake that catches up with everyone eventually. At Better Accounting Solutions, we see this confusion regularly across companies at all stages, and it is one of the most correctable problems a company can have once they recognize the distinction.

Manual processes create their own problems. A new funder typically handles underwriting, approvals, and collections all on their own. While volume remains small, this works well enough. When growth accelerates, the lack of automation creates bottlenecks nobody anticipated. Payments get entered inconsistently. Renewal dates slip. Collections follow-up happens later than it should because attention is elsewhere. Automation is not about removing human judgment. It is about preventing predictable errors and preserving time for decisions that actually require thought. A company that waits too long to automate finds itself perpetually behind its own workload, reacting instead of directing.

Internal communication frays in predictable ways. In the early months, everyone assumes mutual understanding. An underwriter mentions a concern casually, expecting the broker to remember. A collector flags a struggling merchant without copying the person handling renewals. Leadership assumes processes are clear because the team is small and motivated. As volume increases, these assumptions collapse. Files pass between hands without context. Merchants receive contradictory messages. Renewals go out to customers whose repayment problems were never properly documented. Misalignment produces errors that compound quietly until they become visible as losses.

There is also a tendency for growing companies to chase volume without asking whether the volume fits their identity. A broker steers them toward certain merchant types because those deals are easier to place. The funder accepts, thinking refinement can come later. Soon the portfolio fills with merchants whose cash flow patterns the funder never intended to specialize in and does not fully understand. Course correction grows difficult. A successful MCA company chooses its portfolio deliberately. Companies that let the market dictate their mix often end up managing risks they never planned to carry.

Avoiding these mistakes does not require slowing down. It requires shifting from improvisation to intention. The early months of an MCA company can be both energetic and disciplined. Strong companies grow quickly while pricing risk honestly, rather than optimistically. They communicate with syndicators as though every interaction affects future capacity, because it does. They build recordkeeping habits that allow decisions to be understood weeks or months later. They create performance reports that reveal the truth of the business even when the truth is uncomfortable. They automate early so people can think instead of chase.

A company that adopts this mindset gains more than stability. It gains clarity. It learns quickly which brokers bring consistent files and which bring chaos. It sees which underwriting patterns produce reliable merchants and which produce headaches. It discovers which segments renew and which vanish after one cycle. That clarity becomes confidence. Instead of guessing what next month holds, leadership understands why the portfolio behaves the way it does.

The early years set the character of the business. They determine whether growth happens under control or in crisis. Companies that take early structure seriously build foundations that can support scale. They do not fear velocity because they understand it. They do not scramble for liquidity because reserves were planned properly. They do not lose partners because communication stayed steady. And they do not spend their future cleaning up their past.

No MCA company avoids every mistake. The goal is avoiding the predictable ones. The first years offer a choice: chase speed and let structure catch up later, or build habits that make growth sustainable from the start. Companies that choose structure rarely regret it. They discover, often sooner than expected, that clarity is the real competitive advantage.

Stripe Capital Originated 81,000 MCAs and Business Loans in 2025

February 25, 2026 Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe recently conducted a study to measure the impact of Stripe Capital on its customers and found that “businesses that accepted Capital offers grew 27 percentage points faster over the following year than comparable businesses that didn’t.”

“The averages conceal a wide spread,” the company said. “The fastest-growing decile of financed businesses grew more than 3× faster than comparable peers; the next decile grew nearly 100 points faster. A representative example: Xirsys, a server hosting business based in California, used financing from Stripe Capital to set up additional servers in China, India, and Japan, subsequently doubling its revenue. Notably, even businesses with low credit scores grew 11 to 18 percentage points faster after receiving financing.”

Stripe’s rumored interest in PayPal is also notable in the fact that PayPal also has a business loan program. Last year PayPal funded $2.2 billion to small businesses, down from $3 billion in 2024.

Richmond Capital Leaves MCA Space With Negative Case Law On the Way Out

February 24, 2026“Substantive unconscionability is clear from the MCAs’ exorbitant and criminally usurious interest rates, among other things.”

– Appellate Division, First Judicial Department, Supreme Court of New York, February 19, 2026

Richmond Capital Group was never part of the mainstream merchant cash advance industry. The company made headlines for years for its alleged connection to Jonathan Braun, who is now back in prison. After landing in the crosshairs of the FTC, a federal court permanently banned the company and its owner from working in the MCA or debt collection industries ever again in June 2022. The New York State Attorney General piled on with its own legal action and secured a $77 million judgment against Richmond and affiliated entities in February 2024.

But the New York judgment was appealed and earlier this month the Appellate Division of the First Department issued its decision, ruling heavily in favor of the Attorney General. Some of its conclusions, while Richmond-circumstance specific, ought to be examined with a wider lens. Snippets of the Court’s rulings are as follows:

On Reconciliations

“Although the MCAs have mandatory reconciliation provisions, no reconciliation was performed in practice, even though it was supposed to be performed on a monthly basis, and daily payments were fixed and did not represent a good faith estimate of receivables; there is no persuasive evidence of any ad hoc incidents of reconciliation (upon a merchants’ request), which were subject to respondents’ “sole discretion,” and there is evidence that such requests were denied; bankruptcy was an express event of default in some of the MCAs, but even where it was not, repeated nonpayment was, as was breach of the MCAs, which was the case where a merchant “interrupt[ed], suspend[ed], dissolve[d] or terminate[d]” its business; and in the event of any of these circumstances, the full uncollected amount became due and respondents were empowered to enforce the personal guarantees they required the merchants to provide.

Usurious intent is also clear as a matter of law, as, absent reconciliation, the usurious interest rates can readily be calculated based on the information provided on the face of the MCAs.”

On Unconscionability

“The MCAs were also procedurally and substantively unconscionable. Substantive unconscionability is clear from the MCAs’ exorbitant and criminally usurious interest rates, among other things. As to procedural unconscionability, it is not dispositive that many, although not all, of the merchants were sophisticated businesspeople and all had prior experience with MCAs, and respondents misrepresented the terms and nature of the MCAs and used other high-pressure tactics.”

deBanked is not a law firm. To understand the implications of this legal decision, consult with attorneys experienced with the subject matter. For example: Hudson Cook, LLP, Murray Legal PLLC, or others listed here.

Shopify Capital Finishes 2025 With $4.2B in MCAs and Business Loans

February 18, 2026Shopify revealed its full year MCA & business loan origination figures. $4.2 billion. That’s $1.2 billion over the previous year. Only 91.9% of these deals were considered “current” as of December 31, 2025. That’s down slightly from last year when 93.7% of deals were considered current at year-end.

For clarity, Shopify Capital offers funding in 8 total countries. The product is considered a value-add to its e-commerce platform and only offered to merchants who use it. Shopify Capital is in the same league as Square Loans and Enova in terms of origination volume.

Lightspeed: ‘our largest use of cash will be growing our merchant cash advance business’

February 10, 2026 Lightspeed Capital originated $257M in merchant cash advances in the last 9 months of 2025, up from $207M over the same period in 2024. The company has repeatedly talked up the healthy profit margins earned on MCAs and last quarter called them a “super popular upsell.” Lightspeed operates in the POS and e-commerce space, competing against companies such as Shopify, Square, Toast, and Clover. Lightspeed Capital is its MCA business.

Lightspeed Capital originated $257M in merchant cash advances in the last 9 months of 2025, up from $207M over the same period in 2024. The company has repeatedly talked up the healthy profit margins earned on MCAs and last quarter called them a “super popular upsell.” Lightspeed operates in the POS and e-commerce space, competing against companies such as Shopify, Square, Toast, and Clover. Lightspeed Capital is its MCA business.

“Aside from potential buybacks, our largest use of cash will be growing our merchant cash advance business,” said Lightspeed CFO Asha Bakshani during the company’s recent quarterly earnings call. “There are currently $106 million in merchant cash advances outstanding, and we intend to continue to grow this high-margin business over time.”

Lightspeed MCAs are typically satisfied by merchants within seven months, but they want to shrink that timeframe even more. “Our goal is to target a shorter remittance time frame, and we are making great progress towards that end,” said Bakshani. The average factor rate is a 1.14.

Industry’s Mystery Fraudster Extradited to the United States

January 30, 2026A primary suspect in the small business finance industry’s long running mysterious fraud has been extradited to the United States. Saul Shalev, indicted this past August under seal (and unsealed in October) had eluded authorities for years but was finally arrested in Spain. On January 23, 2026, he was extradited to the United States and appeared before a US Magistrate Judge.

Shalev faces a nine-count indictment.

Between approximately December 2019 and November 2022, Shalev defrauded more than 20 small and medium-sized businesses (“SMBs”). As part of the scheme, Shalev obtained information about commercial loans received by the SMBs and offered the SMBs the opportunity to refinance the loans or to obtain additional financing, either from the original lender or from a new lender. Shalev, using stolen identities and making fraudulent representations, acted as a broker between SMBs and potential lenders. After obtaining new or additional financing for an SMB from a commercial lender, Shalev provided fraudulent payoff instructions to the SMB with respect to a prior loan, causing the SMB to send all or part of the loan proceeds to an account he controlled. Shalev also fraudulently received a commission from the lender.

No, Texas Did Not Ban Merchant Cash Advances

January 28, 2026 When Texas passed HB 700 last June, deBanked was among the first to point out that its most notable component was a prohibition on automatic debits of a recipient’s deposit account by a commercial sales-based financing provider unless they had a perfected first position. Some observers were quick to tell us that we had it all wrong, that MCAs had effectively been “banned” entirely and that we should have reported it that way. This was premised on a belief that perfecting a true first position on a recipient’s deposit account was a near-insurmountable obstacle (for MCAs that rely on ACHs instead of credit card splits) and thus a nuanced discussion of how to comply with the new law a moot debate.

When Texas passed HB 700 last June, deBanked was among the first to point out that its most notable component was a prohibition on automatic debits of a recipient’s deposit account by a commercial sales-based financing provider unless they had a perfected first position. Some observers were quick to tell us that we had it all wrong, that MCAs had effectively been “banned” entirely and that we should have reported it that way. This was premised on a belief that perfecting a true first position on a recipient’s deposit account was a near-insurmountable obstacle (for MCAs that rely on ACHs instead of credit card splits) and thus a nuanced discussion of how to comply with the new law a moot debate.

But if the state legislature had intended to ban sales-based financing outright, it simply could have done so. Instead, it codified a framework for how to legally provide sales-based financing. It provided guidance on registration, disclosure, and oversight. And it even went as far as to say that the Finance Commission of Texas cannot “adopt a maximum annual percentage rate, finance charge, or fee for commercial sales-based financing transactions.” This was an incredible signal: No cost cap on sales-based financing.

The Texas Office of Consumer Credit Commissioner (OCCC) even held an open forum this past November to hear from impacted parties on the best way to craft and enforce the rules going forward. And so while they’re now busy promulgating those precise rules, collective minds have returned back to the original language surrounding that “certain automatic debits” are “prohibited.”

CERTAIN AUTOMATIC DEBITS PROHIBITED.

A provider or commercial sales-based financing broker may not establish a mechanism for automatically debiting a recipient’s deposit account unless the provider or broker holds a validly perfected security interest in the recipient’s account under Chapter 9, Business & Commerce Code, with a first priority against the claims of all other persons.

This language does not say that merchants cannot pay sales-based financing providers entirely. Others agree. deBanked spoke with one company, MCA Pay, which analyzed what the law says and they created a tool for merchants to pay sales-based financing providers in an orderly easy manner so that funders do not in fact have to automatically debit a recipient’s deposit account at all. Though there are some layers to how it’s done, merchants are, on their own volition, setting up a system to initiate payments to whichever funder they choose. They’re in control.

Far from theoretical, this methodology is already being used by merchants in Texas to pay sales-based financing providers, according to MCA Pay.

“We’re comfortable from a regulatory perspective, but I encourage everybody who uses this platform to run this by their counsel,” a representative said. “We’re putting the control back into the merchant’s hands.”

The two main partners at MCA Pay, Gavriel Kalfa and Moshe Klar, do not hail from within the industry, but they worked with experienced operators in the industry while building out the system. MCA Pay is not the payments provider or a law firm, they’re just the platform that loops the pieces together.

“Hopefully we’ve made a product here that’s going to allow MCA to continue in Texas compliantly for everybody,” they said.

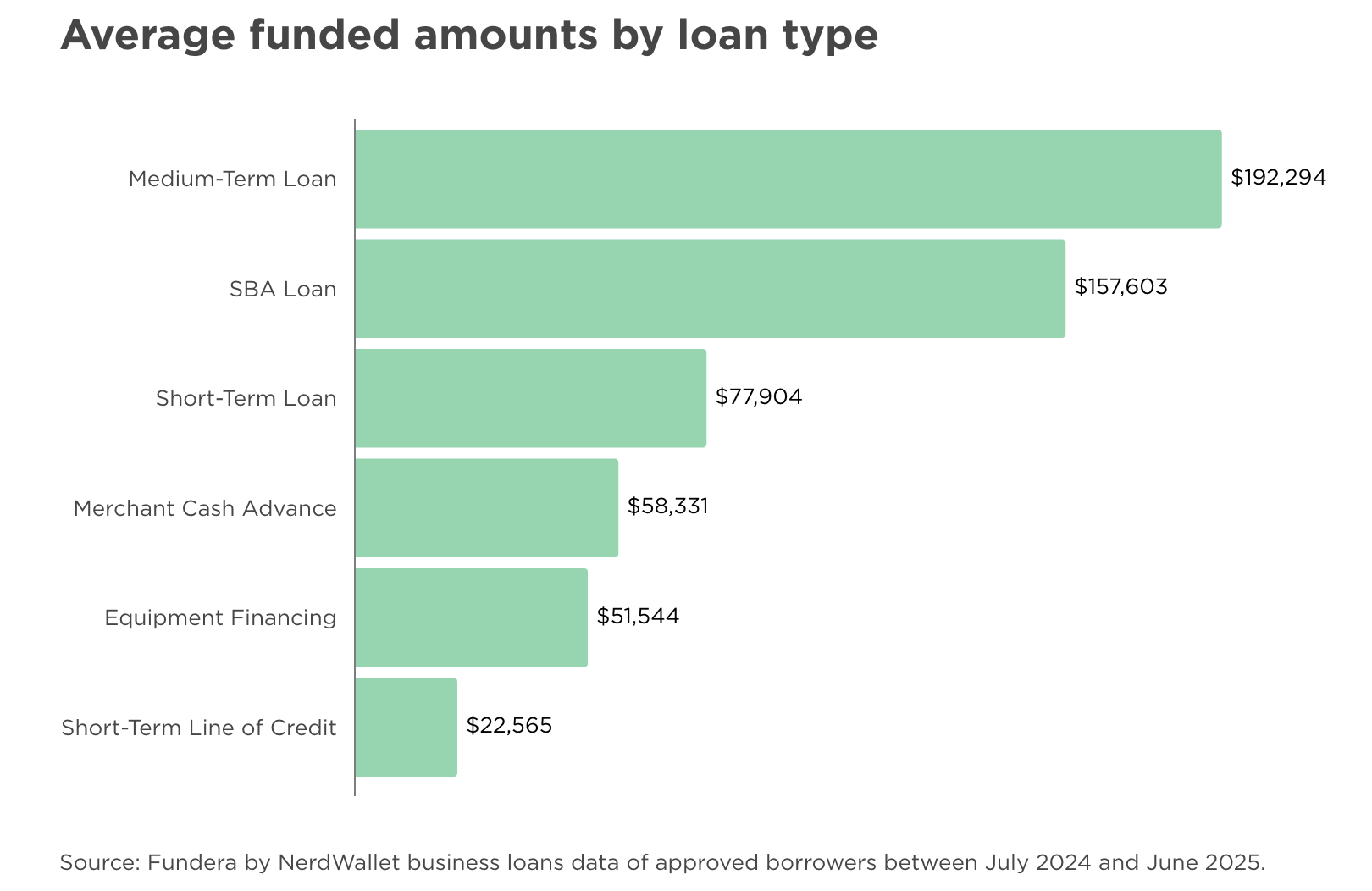

The Average MCA Deal? $58k Report Says

January 26, 2026According to NerdWallet, a leading business loan matching marketplace, the average funded amount of an MCA deal is $58,331. That’s based entirely on the company’s own internal data from July 2024 to June 2025.

Medium-term loans (2-5 years) came in with the highest average of $192,294 and short-term lines of credit produced the lowest average of $22,565.

NerdWallet depends heavily on web traffic to generate leads so this is potentially representative of merchants who use Google or ChatGPT to find financing versus all possible channels.