Starting a Business – Read First

August 22, 2011Jerry had a business plan and some money set aside for startup capital. He assumed that’s all he needed, but six weeks later he was already out of business. What went wrong?

Starting a business is exciting and some entrepreneurs even describe getting an adrenaline rush as they approach opening day. But this impulsivity forward can lead to major mistakes, careless decisions, and ultimately put you on the path to failure. If you’ve got a lease on a storefront that opens May 1st, you should aim to open the business on May 1st. But if you are not prepared to handle the demands of your customers or conduct operations most efficiently, then you shouldn’t open just for the sake of opening.

- What can go wrong the week before opening – April 24th

1. Choosing vendors out of convenience or because they can meet an arbitrary deadline

Example: You’ve spoken to two advertising agencies about your startup. Both have quoted the same price. Company A can put together a promotional campaign by May 1st, your opening day. Company B can put together a promotional Campaign by May 18th, but it will be much more effective and reach a larger audience. Company B’s campaign is far more likely to bring in customers for the same price.

Believe it or not, with all the stress and time against their side, many entrepreneurs would rather pick Company A just for the immediate relief. It coincides with their opening day and it would feel great to have one less thing to worry about. But Company B would generate more revenue for them and thus would probably be the smarter decision.

2. Looking at the process like a checklist

Let’s say you’ve created a series of basic steps that must be completed before May 1st. In the last week, you go back to check and make sure they’re all done or to find out what you have left.

Example:

1. Create business plan

2. Raise capital

3. Lease store space or office space

4. Choose vendors for inventory, supplies, and equipment

5. Advertise

If your list is as basic as this, you’ve already failed. Each step should have a series of substeps.

Example:

1. Create business plan

– Survey prospects to determine if there is demand for this product (Don’t ask your family. They don’t count)

– Obtain a 2nd opinion from a qualified business advisor on your business plan

– Locate 10 weaknesses or shortcomings of your business plan (if you can’t find 10, you’re giving yourself too much credit)

– Find proof that a similar business model has worked before and dissect their plan

2. Raise capital

– Determine how much equity you are willing to sacrifice

– Set realistic goals for when your business will be able to start making payments, how often you can make payments, and how much you can afford in each payment

3. Lease store space or office space

– Determine several locations that would be ideal to reach your target market, whether or not there is space available there

– Determine if there is a way to obtain space in that area (sublease, a landlord looking to replace a tenant etc.)

– Determine which locations are actually available to lease

– Determine if any of them are suitable for your business (if none, DON’T open!)

– Determine if the costs justify the level of success you can achieve in that location

4. Choose vendors for inventory, supplies, and equipment

– Seek out terms on inventory as opposed to COD (very difficult for a startup to attain but it would be a huge difference in cash flow)

– Choose reputable vendors (don’t pick the cheapest just because cash is tight in the beginning. Low quality goods may turn your customers away)

– Choose how you will pay for supplies and equipment (lease or purchase. Leasing may be less expensive now but far more costly in the long run)

5. Advertise

– Shop around and learn about all the different ways these firms intend to help you reach your target audience

– Choose the company that will produce the most bang for your buck

– Use common sense (A 3 AM TV commercial is probably not suitable for a toy store etc.)

If you didn’t go through this whole list, there’s a good chance you’ll fail. And just when you think you’re sure you’ve got a handle on everything, buy a few books by people who have been in your shoes. Find out what they did, what challenges they faced, and how they succeeded or failed. We’re not talking about a short article like ours, but rather a full story that shares every detail, thought, and emotional feeling that you can expect to go through. There’s nothing like being prepared and it may even inspire you to modify your business plan as it currently stands. Don’t end up like Jerry. Doing things right is much better than doing things quickly.

The Merchant Cash Advance “Don’ts”

August 22, 2011In sales training, young men and women are taught to negotiate with positive language to close a deal. For example: “We can’t meet the deadline” is replaced with “We can achieve the objective, but we may need to extend the deadline.” Or “We don’t offer that service” is transformed into “We offer many services that can add value to your business but that particular one is a challenge.”We apply a bit of that psychology when developing resources for business owners. People are a lot more open to input when you cast out the negativity. So it’s a bit ironic then that we created a printable reference form, titled The Merchant Cash Advance “Don’ts”. Though it may be perceived as a little condescending, this little banker/business pep talk can protect you from making a major mistake that could cost your business money. So keep it handy even if you don’t plan on applying in the near future.

1. Don’t wait until the last minute to apply for funding.If a firm is advertising funding in 3-5 days, don’t put yourself in a position where you MUST have the funds in 5 days or less. The underwriting process may take longer than you anticipate. The advertised timeframes generally describe a perfect situation. For example: If all documents are received by day 1, all references checked out by day 2, you could potentially receive funds by day 3 assuming the technical setup is already completed. There are situations where business owners have spent 10 days waiting to obtain a copy of their lease from their landlord, which piggybacks onto the 3-5 days. Additionally, supplemental paperwork may be asked for, a trade reference might be unreachable, or your method of card acceptance might require more time to integrate. Anything can happen so don’t wait until the last minute!

2. Don’t lie about your business ownership percentage.This might be seem like silly advice but underwriters report that it’s a growing trend. People with low credit scores tend to assume that they will be declined for their score alone. Therefore they may feel inclined to state that a partner, friend, or family member with excellent credit is the owner of their business and not them. This is bad for several reasons:

- Credit score isn’t the sole determining factor for a Merchant Cash Advance. So why lie?

- Misrepresentation of ownership will be discovered and the application declined.

- Misrepresentation to obtain financing constitutes fraud and is a crime.

3. Don’t lie to the underwriter or your account rep.The liar loans of the mortgage boom ultimately led to the financial crisis and lending shortage. That means the days of declaring whatever you want to obtain the deal you want, are gone. If you state that you generate $100,000 in sales per month, be prepared to show documentation that backs up that claim. Your sales agent or account rep is probably compensated if you close on financing. That doesn’t mean they will help you get there at all cost. They are bound by a certain code of ethics and all applicable laws. If they become aware of any misrepresentation or intended misrepresentation, don’t expect them to be an accomplice to your dishonorable act. If you put them at risk, they will inform the underwriter and terminate your application.

4. Don’t alter any documents.Changing the expiration date on a lease, editing out the embarrassing withdrawals from the bank statements, or any other more or less blatant alteration will result in a rejection. Merchant Cash Advance underwriters are extremely adept in detecting alterations and fraud. Altering documents in an attempt to secure financing is a crime. You are well advised not to try this, no matter how harmless you may perceive the alteration to be.

5. Don’t over shop for a deal.You are entitled to obtain quotes from multiple sources, but don’t press your luck. Too many credit inquiries can spook an underwriter. For one, it tends to drive down the margins that will be earned because competition, thus making the deal less profitable for them and less attractive to put on the books. On the other hand, they may suspect that the other firms declined you and therefore they are being picked as a last resort. When underwriters start to feel this way, your approval may be retracted and it can be a tough battle to convince them to change it back.

We promise next time to provide a guide full of “Do’s”! But for now, we’re making it a point that Merchant Cash Advance is a serious business. The process may be fast and easy, but don’t get too comfortable and make claims you can’t back up. That will lead nowhere good…

– The Merchant Cash Advance Resource

http://www.merchantcashadvanceresource.com

Deja vu? Merchant Cash Advance in Wall Street Journal

August 10, 2011 Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

It was just a couple months ago that we published a scathing editorial on the failure of the Merchant Cash Advance (MCA) industry to reach mainstream acceptance. (See: The Colossal Marketing Failure of the Merchant Cash Advance Product – June 28th, 2011). Most of our readers acknowledged the shortcomings but were at a loss for suggestions to overcome them. ISO&Agent Magazine quickly added their two cents by claiming that MCA was waiting for its big moment (See: Cash Advances: Negotiating a Maturing Market – July 26th, 2011) but completely missed the mark when they identified cost as the obstacle holding it back. It’s not cost, it’s communication.

How often is MCA cited in mainstream news publications? Wall Street Journal? New York Times?

-direct quote from our piece on June 28th

Today we can say that Merchant Cash Advance got its mention in the Wall Street Journal. :::Applause::: Though it’s only in their blog section, most people today get their news online anyway. The article features AdvanceMe, the largest and oldest player of the bunch. So how does the glorification of one company carry over to the industry as a whole? There were a bunch of good messages in there that describe the product itself: The article title implies it’s becoming more popular: “Cash-Advance Demand Rising” A description of how it works: “Merchant cash advances, which first appeared about a decade ago, provide capital in exchange for a share of future debit or credit-card sales. As such, they tend to be used by retailers, restaurants and other small businesses where a large number of customers pay with cards.”The common uses for it: “Business owners use the cash to buy new equipment, restock inventory or pay off debt” Yes, Yes, and Yes. Good for AdvanceMe and good for the MCA industry but this is only the beginning.

Every business owner should be aware of MCA, not just the ones that read the Journal today. It is Un-American (Yeah, that’s right) to withhold information from business owners that may enable them to capitalize on opportunities. With no bank loans available, most projects in this country are on hold. It’s simply not fair. We badly want to take the credit for today’s Journal mention, especially since we delivered our two previous articles on this topic to their editors in July. But the real hero here is AdvanceMe. Their press release the day before clearly caught the attention of the mainstream media. Great job guys. And we’d be remiss if we didn’t point out they forecasted an increase in funding by $1 billion in the next 2 years. That’s about equal to the industry’s entire volume combined. Is Merchant Cash Advance about to hit its growth spurt? AdvanceMe seems to think so. If they’re about to have their ‘moment‘, they’ll likely pull everyone else along with them.

– deBanked

https://debanked.com

Small Business Lending Faces Extinction

August 4, 2011

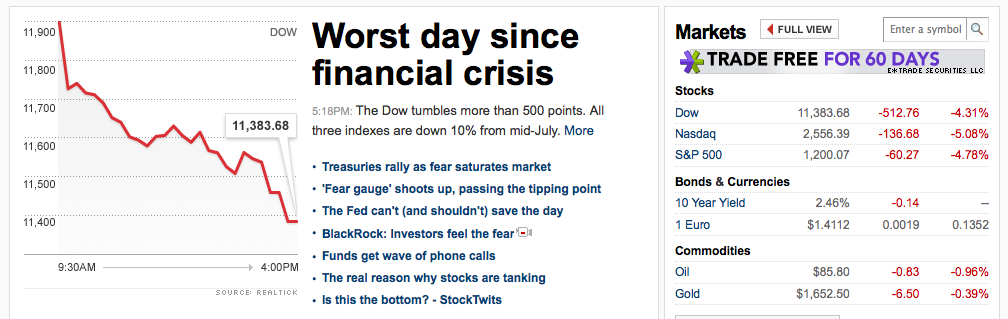

Small Business Lending is about to drop even further. It has to. Today’s 512 point kick to the groin was less about fear of the future and more about the issues we’ve been unwilling to acknowledge in the past. Let’s not water down the facts:

The economy is not growing.

There is no recovery.

There is no improvement.

That is it. There’s been far too many “growth is slow but…” rationalizations in which dismal results are chalked off as seasonal, aberrational blips, just because they don’t fit in line with our delusions of recovery. We all saw today coming, let’s not kid ourselves. See our evidence:

Seasonally Adjusted Weekly First Time Unemployment Insurance Claims:

Figures that fall below 400,000 are considered to be conducive to hiring and growth.

3/26/2011 392,000

4/02/2011 385,000

4/09/2011 416,000

4/16/2011 404,000

4/23/2011 431,000

4/30/2011 478,000

5/07/2011 438,000

5/14/2011 414,000

5/21/2011 429,000

5/28/2011 426,000

6/04/2011 430,000

6/11/2011 420,000

6/18/2011 429,000

6/25/2011 432,000

7/02/2011 427,000

7/09/2011 408,000

Source: Department of Labor http://www.dol.gov/opa/media/press/eta/ui/current.htm

News outlets have published more recent figures, with the data indicating claims above 400,000 for each of the last three weeks of July. Seventeen straight horrible weeks show no signs of improvement in the job market.

Small Business Loans Drop by $15 Billion in Q1

Greece Has 100% Chance of Default

http://blogs.wsj.com/source/2011/06/20/greece-will-default-but-not-yet

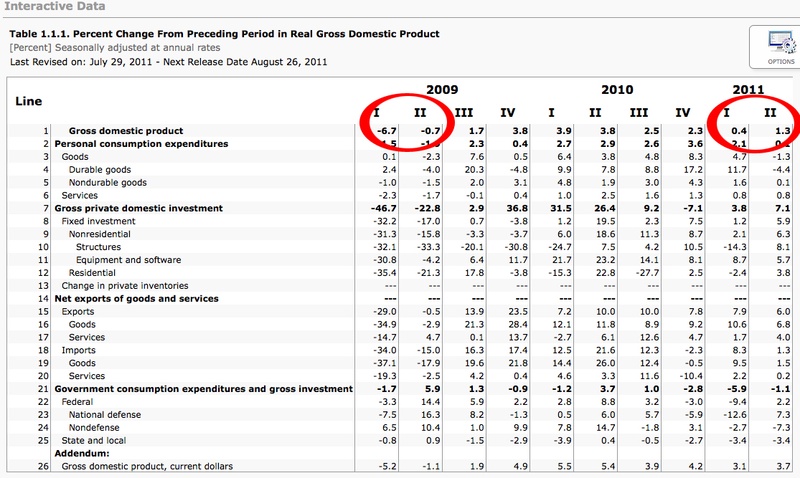

GDP is Shrinking

Rate of GDP growth is declining. The first quarter was dangerously close to a recession.

SOURCE: http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1

U.S. Still at Risk for Debt Downgrade

http://www.reuters.com/article/2011/08/03/us-markets-forex-downgrade-idUSTRE7725ZK20110803

Food Stamp Use Rises to Record 45.8 Million

“Nearly 15% of the U.S. population relied on food stamps in May, according to the United States Department of Agriculture.”

ADDITIONAL INFORMATION: http://money.cnn.com/2011/08/04/pf/food_stamps_record_high/index.htm

Stock Market Experiences Ninth Worst Single Day Drop in History on August 4th, 2011

SOURCE: CNN Money

———

Where is the good news? There isn’t any. For the first time in a long time, the media isn’t able to keep up the recovery lie any longer. And the Federal Reservce is powerless to help. Interest rates have been kept near 0% for the past couple years and the $14,000,000,000,000+ deficit hinders their ability to issue more stimulus. Yikes!

Small business lending has been on the decline for awhile but the lack of fear in the market has kept the dirt tucked under the rug. Bankers were under the impression that there was a recovery in motion and now that they’ve become aware otherwise, it’s about to get really ugly.

To illustrate what’s already happening, a friend of ours manages the retail underwriting department for a large national bank. He spoke to us under the condition of anonymity and had this to say about their recent shift in policies:

“We are still lending but we’re using a ‘1:1 cash collateral rule’. What that means is, if a business wants to borrow $100,000 they must already have at least $100,000 in cash or cash equivalents on their books. The cash itself isn’t the collateral, it’s just a prerequisite to ensure they are especially equipped for a future cash-flow crisis. $100,000 of real collateral is still required but at this point we don’t ever want to be put in the situation where we’re chasing down a borrower to sell off their assets. Our loans don’t yield nearly enough to survive even just one default. People always joke that banks won’t lend unless the borrower doesn’t need the money. Now we won’t lend unless you already have the money!“

And so we’re entering a dark age, a slow approach back into a recession that we never actually came out of. There’s no reason to think that this will cause banks to increase lending and it is highly doubtful that it will remain at its current levels.

=====================

* Recently added. These poor creatures need your help!

=====================

So what’s the prognosis? The Merchant Cash Advance industry may soon have it’s so-called ‘Moment‘, but not because the small business community demands it, but because there won’t be anything else left…

– The Merchant Cash Advance Resource

Merchant Cash Advance Applicant Fraud on the Rise

July 24, 2011

Fraudulent Applications are becoming more commonplace in the Merchant Cash Advance industry. Scott Griest, the CEO of American Finance Solutions had this to say about it:

- Hard fraud is when outright crooks are submitting applications for businesses that do not exist, have stolen a business’ identity or a desperate actual owner has altered his financial documents to qualify for more favourable terms.

- Soft fraud is when a legitimate business has submitted actual documentation, but is still not being truthful about his or her business.

- All funding companies should become members of NAMAA.

- In AFS’s first month of membership they detected more than $20,000 in submitted fraud deals.

Bad debt has dropped by 50% over the past 12 months due to fraud detection.

– The Merchant Cash Advance Resource

Planning a Payoff Just Right

July 17, 2011

According to Scott Griest, the CEO of American Finance Solutions, paying off a competitor is more complex than writing a check to pay off the balance. In his latest blog post, he explains this:

- When calling too early for a balance, the funding provder risks tipping off the competitor that they are about to get bought out of a deal. If its a good, profitable client (which is most often the case) the competitor will often “instantly approve” the renewal and offer to wire funds that day and beat the offer.

- It’s best to wait until the day of funding to receive the payoff instructions. That is unless the sales agent has grossly underestimated their outstanding balance or account performance.

- Sometimes you’ll find out the reason that the client cannot renew is because of collections issues, fraud (altered payoff letters) or trying to get double funded on the same day by the old and the new MCA company.

- Sales partners need to know their clients. Find out the funding date of their current advance and deal terms. If the contract payback amount is $50,000 and they got the advance six months ago and the balance is over $30,000, then there’s an issue with payback.

To read the full article, visit Scott Griest’s Blog