Merchant Cash Advance Industry is Waiting for its Big Moment

August 25, 2011Originally Posted 7/28/2011

According to an article in ISO&AGENT Magazine, the Merchant Cash Advance (MCA) industry has had significant success but “the companies that fund them acknowledge the cash-advance market is still waiting for its big moment.” This echoes our earlier opinion that a lack of collective marketing is keeping this financial tool from reaching its true potential.

How is it that in an ultra tight credit market that small businesses have not heard of MCA? With lax credit score standards, fast turnaround, minimal documentation, and a flexible method of repayment, it’s absurd that the industry has not reached so many that are looking to borrow. ISO & AGENT points to a negative image crisis and fingers the costs involved as a possible culprit.

The costs are a non-crisis. MCAs would be less expensive if they required collateral, perfect credit scores, fixed terms, ten years in business, and a 3 month underwriting process. If a small business meets those requirements and does not have a time sensitive opportunity they are looking to capitalize on, they should be going to their local bank. But most small business owners either do not meet that criteria or need the funds for a project they have going on today. Hence the product has to be more expensive for it to make sense for the firms providing the funds.

ISO&AGENT claims the industry has been compared to payday loans, an untrue characterization. In fact, that comparison has so rarely been made, that we can pinpoint the exact place they got that from. Inc.com published a very unflattering article on April 1, 2008 titled ‘Thanks, But No Thanks‘, in which they explain MCAs as “the business equivalent of a payday loan.” That was three and half a years ago! The article was not only biased and unfair, but was also written at a time when everything related to Wall Street, banks, or lending was being demonized as the nation sat on the verge of the Great Recession and economic collapse.

Still one can’t help but notice that buried deep within their criticism, is the answer to why MCAs are a tad bit more expensive:

The fact that collateral isn’t necessary is another important part of the MCA providers’ pitch. Entrepreneurs sometimes risk losing their homes if they can’t repay a bank loan, but they have no legal obligation to repay merchant cash advances if their companies fail, as long as they strictly follow the terms of the contract. They can’t encourage customers to pay in cash, for example, and they cannot switch credit card processors (typically, the MCA provider gets paid directly by the processor, rather than by the merchant). “If Diane’s Bistro goes out of business because Lauren’s Bar & Grill opens up across the street, we have absolutely no recourse to Diane, none whatsoever — as long as she follows the clearly defined covenants in our contracts,” says Glenn Goldman, AdvanceMe’s CEO.

And if you had any more reason to suspect MCAs are not as bad they tried to make it out to be, Inc.com published that article on April Fools Day. Case closed.

But there is indeed an image crisis and it’s that many businesses haven’t been exposed to the concept of MCA and thus cannot consider the pros and cons at all.

For instance: Most people can make the case for or against consumer payday loans. They’ve already got loads of information from the media, newspapers, banks, and lawmakers on which to base their argument. It’s become a well known household accepted form of financing. Whether or not payday loans can help the consumer is a separate debate.

That’s the difference. MCA is rarely spoken about by newspapers, banks, or lawmakers. Its presence in the media is limited and as a result we’re referring to stories published over three years ago. We have many friends employed as small business loan officers across the country and the only reason they’re aware of how MCAs work is because we told them. It’s embarrassing. And for an industry that funded over $500 Million last year alone, it really makes no sense.  We blamed antiquated marketing techniques: cold calling, junk mail, useless internet marketing, and spamming. The industry has gotten lazy and has a propensity to market their financing to small businesses that have already secured a MCA. This comes with bold promises of lower rates and other gimmicks. This inner competitiveness leads to both smaller margins and lower conversion rates. It does nothing to grow the industry as a whole.

We blamed antiquated marketing techniques: cold calling, junk mail, useless internet marketing, and spamming. The industry has gotten lazy and has a propensity to market their financing to small businesses that have already secured a MCA. This comes with bold promises of lower rates and other gimmicks. This inner competitiveness leads to both smaller margins and lower conversion rates. It does nothing to grow the industry as a whole.

That’s complemented by carpet bombing the public with an approach their customers learned to ignore a long time ago. Cold calls and junk mail. Really? Yes, really. There will always be a sliver of effectiveness from these methods and the firms that employ them will defend their success to the death. These methods may score some deals and perhaps even work well enough to grow a MCA firm, but it will not lead to the industry’s ‘big moment.’ Same goes for internet spam, poorly constructed articles that serve no purpose other than to boost some company’s SEO, and useless blogs kept by both respectable firms and no-name websites set up to harvest leads. Sure that’s the way of things on the internet these days but there isn’t anything beyond that. There are no mainstream media articles about MCA, forums for business owners where it is actively discussed, nor any public endorsements by anyone of high political or business stature.

Sounds like we have an image crisis on our hands. The Merchant Cash Advance Resource (the site you’re on right now) has been in existence for 1 year. In that time, we’ve made significant additions to the information that can be accessed here. We constantly receive emails from business owners and MCA brokers alike with the hope that we can provide them with an unbiased answer. And guess what? We do just that. By having no commercial affiliation, we give the best advice we can. The e-mail volume has gotten so heavy that our volunteer editors have trouble answering them all. But we try anyway.

And along the way we’ve managed to get some formal offers to convert this resource into a commercial site to generate sales leads. A six figure buyout offer here and there coupled with some lengthy, legalese filled non-disclosure agreements. We say ‘no’ every time. The Merchant Cash Advance Resource is designed to provide information, opinions, critiques, data, guides, and an independent ‘thumbs up’ to an industry that’s destined to do great things for small business.

Why do we spend the time, money, and effort to provide this service? We’re looking at the big picture of MCA. Big picture… Big moment…

And we’re on our way.

deBanked

https://debanked.com

Top 10 Merchant Cash Advance Funders for 2010

August 24, 2011

According to data compiled by infoUSA, this is a breakdown of marketshare by the top 10 funders:

Chart by:

Max Alewel

Senior Account Executive

Direct Toll Free: 1-866-322-3708

Fax: (402) 836-4914

max.alewel@infousa.com

credit.net

Relatively close to what our own analysis proved, the chart has some flaws:

- Advance Restaurant Finance is a licensed lender, not a provider of Merchant Cash Advance or purchaser of future credit card sales.

- We estimate there to be at least 37 active funding providers. A breakdown of marketshare between 10 of them doesn’t represent the share of the overall market, just between eachother.

- There are no quantifications, # of deals, dollar amounts etc.

We still appreciate Max’s work as it serves to complement and back up the claims we have made. If you still haven’t seen the data, check it out

Full 2010 Merchant Cash Advance Industry Statistics

1st Quarter 2011 Merchant Cash Advance Industry Preview

-The Merchant Cash Advance Resource

How Not to Grow Your Merchant Cash Advance Business

August 23, 2011

Advertising and marketing are tricky in any industry. The Merchant Cash Advance space has certainly experienced its fair share of trial and error over the past several years. What works for one company, doesn’t for another.

Many argue that there are no virtually no barriers to entry and this causes problematic issues in competition. Some representatives don’t know what they’re selling, how to sell it, or what can and can’t be said when they’re selling it. There are so many fly by night resellers, that states are running out of LLCs to issue. “Merchant funding capital advance now approved accredited finance business source solutions, LLC” is the going fast! Better Organize it now.

For ones that make it, they have the good leads.

Blake: These are the new leads. These are the Glengarry leads. And to you they’re gold, and you don’t get them. Why? Because to give them to you would be throwing them away. They’re for closers.

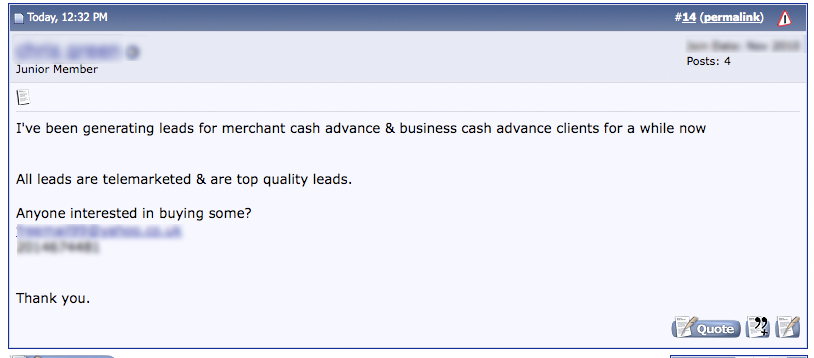

But there is good way to not grow your Merchant Cash Advance business and that is to be so desperate, that you buy actual piles of garbage. These leads are obtained through sources that advertise in this manner:

You can find stuff like these in forums, along with a shady hotmail address, no website and a promise of ‘top quality.’ If your business model is to buy leads, then make sure to have your Ch. 11 papers handy before you purchase these TOP QUALITY LEADS!!!

Also watch out for ‘try before you buy’ schemes: Get 5 trial leads for $50. if you like them, you can purchase a minimum of 100 at a time for a cost of $20 per lead. There are no refunds when you buy them. The 5 trial leads are real. The $2,000 bulk purchase is a flaming pile of crap.

Shelley Levene: The leads are weak.

Hope that helps. I would love to share more insight right now but a payday loan company with a predictive dialer is calling my phone and I’m eager to talk to someone in India who can provide a vague description of the product and have my information sold to 5 companies who swear I had completed a contact form online for car insurance because that’s what their lead sheet says.

-The Merchant Cash Advance Resource

Keep a Watchful Eye on Your Merchants Until New Years

August 23, 2011

If you work in the Merchant Cash Advance(MCA) business, November and December should be your favorite months. Holiday sales translate into enormous surges in both cash advance and processing residuals. If you don’t know what residuals are or don’t have them included in your compensation structure then OOPS! (Your employer won’t like us too much).

A struggling ISO can rise out of the red on the coattails of their merchants and have a very black friday themselves. But proceed with caution for clients that have an outstanding MCA balance. The surge in sales can be all too tempting to keep for themselves.

A photo we took at a store on Black Friday

A photo we took at a store on Black Friday

Did your retail store client process a big fat ZERO on Black Friday? Did that liquor store do less business in the days leading up to Thanksgiving than in prior weeks? If so, the merchant may be hijacking your future receivables and with that, your largest residual paycheck of the year.

It is not uncommon for stores to hire temporary workers and open additional lanes and cash registers to accommodate increased foot traffic. It is also the time when their secret backup credit card machine they never told you about rears its ugly head. While we can sympathize with a business for needing extra terminals, we don’t condone the use of ones that breach their MCA contracts.

What to do? If you haven’t already, now is the time to call your clients to find out if they need additional equipment. It can’t hurt to make the first move before they act on their own and intentionally or unintentionally use another merchant processing service.

Additionally, some small business owners may try to process all sales in excess of their monthly average through an alternate machine. So a mall retail store processing $10,000 month on average continues to process that same $10,000 in November and December, leaving you completely unsuspecting that an additional $30,000 was processed elsewhere. Monitor the retail, food service, and liquor store accounts on a daily basis from now until New Years.

Treat your clients right and work with them to ensure they don’t miss a beat. Out of receipt paper? Ship them extra rolls! Processing an unusually large sale? Get the signed invoice or receipt to ensure funds are not held.

Veterans in the Merchant Cash Advance business have come to expect this last month and half of the year to be the most rewarding. But make sure the merchants are equipped to handle the sales, monitor their activity, and keep an eye on them. Happy Year End.

-The Merchant Cash Advance Resource

https://debanked.com/merchantcashadvanceresource.htm