Industry News

Letter From the Editor – May/June 2015

May 1, 2015 Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

New financial products can be just as intimidating to the professionals working within the wider industry as they are to the customers they’re being offered to. I’ve blogged often of my experience investing in Lending Club and Prosper notes, something I assumed everyone in the business finance world could relate to. Alas, I find that usually raises more questions with readers than it does answers.

Are you just nodding your head and smiling when your peers talk about their alternative lending portfolios? There’s no better way to understand today’s loan marketplaces than being an investor in them, even if it’s just a small amount. Whether it’s merchant cash advances, real estate loans, student loans, or credit card debt, there are plenty of opportunities and worlds to explore. You should conduct research, diversify, and be smart of course. You don’t want to be trapped in a bubble.

Outside the knowledge bubbles, we have regional enclaves. There are entire city neighborhoods being overrun by small business financing startups. In New York City, it had long been Midtown, but some shops started moving south and before anyone realized what was happening, Wall Street had been overrun by a new breed of broker. The culture in lower Manhattan is different than you might find in Midtown or in the next two largest industry hubs, Miami and San Francisco.

In this issue, we’ll begin to explore the industry’s bubbles, both geographically and structurally.

–Sean Murray

Ready to Trade ONDK and LC?

November 16, 2014 On November 10th, OnDeck Capital finally made their S-1 public. Immediate reactions from inside the industry were mixed. The bears criticized the years of losses while the bulls pointed out that the tide is turning. With a profitable 3rd quarter, OnDeck’s bet on the long game might finally be proving itself.

On November 10th, OnDeck Capital finally made their S-1 public. Immediate reactions from inside the industry were mixed. The bears criticized the years of losses while the bulls pointed out that the tide is turning. With a profitable 3rd quarter, OnDeck’s bet on the long game might finally be proving itself.

And without delving into their S-1 for now, the industry should be bracing itself for change. The mysterious world of daily funders (financial companies that deal in daily payments) is about to come under the scrutiny from another body, stock analysts.

Unlike journalists which have bruised the industry with sensational headlines and surface level criticism (high costs, light regulation), analysts will be tasked with truly understanding the fundamentals of nonbank business lending. Not to mention that everyday retail investors looking for an edge will want to learn more about the industry than what a single company’s quarterly financials will tell them.

Daytraders might make decisions based on melodramatic stories but those buying and holding for the long run will be conducting something that’s rarely taken place in this industry, research. Expect these questions to be asked and deeply considered:

- Who are OnDeck’s competitors? (and not just the top 3, but the hundreds that follow them)

- What are ISOs/brokers and how do they operate?

- How do they generate deal flow?

- What is Merchant Cash Advance and how is it similar or different to OnDeck?

- What is the real regulatory environment? (Because there are actually applicable regulations despite articles that say there aren’t any)

- Why does OnDeck collect payments daily?

- Why is OnDeck’s model so much different than Lending Club’s?

Look for the last bullet point to be explored greatly. If OnDeck and Lending Club are both innovative small business lenders broadly targeting the same market, why is OnDeck charging an average of 50% APR paid daily over 6 months and Lending Club charging as low as 5.9% APR paid monthly up to 5 years?

Their products couldn’t possibly be more different. And while Lending Club’s IPO path has curiously stalled, there is nothing to indicate that it will not proceed. That means we should expect comparisons between the two upcoming tickers LC and ONDK, a lot of them.

Details about commissions, closing fees, marketing practices, and transparency will be talked about in open forums by the general public. If it’s controversial, it will be debated. If it’s unique, it will be scrutinized. To an extent, OnDeck, Lending Club, and many of their competitors will cede control of their destiny to the general investing public.

There are folks in the industry giddy over the chance to buy and sell stock in both companies. They have years of experience on the front lines. But just as they’re gearing up to trade ONDK and LC, so too is everyone else.

Get ready for major change…

Rapid Capital Funding Acquires American Finance Solutions

October 8, 2014 Miami, Florida-based Rapid Capital Funding will acquire Anaheim, California-based American Finance Solutions today in perhaps one of the most significant deals in merchant cash advance history.

Miami, Florida-based Rapid Capital Funding will acquire Anaheim, California-based American Finance Solutions today in perhaps one of the most significant deals in merchant cash advance history.

Rapid Capital Funding, not to be confused with RapidAdvance, is led by the company’s founder Craig Hecker. Hecker and AFS’s CEO Scott Griest broke the news to me on a call together. “It’s a roll-up,” Griest said. AFS will continue to operate under their brand name for the time being and Griest will remain a leader in the company.

Meanwhile, the operations of the two companies will begin to merge, with Hecker confirming already that their head underwriter, Andrew Hernandez, was in California getting up to speed on AFS’s operations.

The news comes less than five months after American Finance Solutions struck an equity deal with CapFin partners. I am unsure if CapFin is still involved in the company.

Griest and Hecker were both excited about working together. “Griest has done a great job managing the sales partner channel,” Hecker said. Griest will continue to develop those relationships for the company.

Griest and Hecker were both excited about working together. “Griest has done a great job managing the sales partner channel,” Hecker said. Griest will continue to develop those relationships for the company.

This is the first major merger in the industry. Historically, just about all of the equity deals in merchant cash advance have been acquisitions by institutional investment groups. This is a consolidation.

RCF, while based in Miami, has an office in New York City. The AFS deal puts them on the ground in the 3rd major industry hub.

The two executives hinted that this deal was just the beginning.

OnDeck Already Filed Form S-1

September 27, 2014 Back on August 14th, the Wall Street Journal reported that OnDeck was preparing to file for an initial public offering. Since then, industry insiders have been bustling with anticipation to see the S-1 filing, the document that would reveal once and for all their true financial standing.

Back on August 14th, the Wall Street Journal reported that OnDeck was preparing to file for an initial public offering. Since then, industry insiders have been bustling with anticipation to see the S-1 filing, the document that would reveal once and for all their true financial standing.

Update 11/18/14: Click to see OnDeck’s Public S-1 Filing

In between then and now, Lending Club, their rival in the business loan market, filed their S-1 on August 27th. The peer-to-peer lending world went nuts and merchant cash advance veterans such as AmeriMerchant’s David Goldin were asked to comment on BloombergTV.

And then… things quieted down. OnDeck went radio silent on August 14th, despite the SEC requiring such only after the S-1 form had actually been filed. Speculation began to build as to whether or not the WSJ report in August was a false alarm or misinformation. And with no word from the industry’s beloved charismatic superstar Noah Breslow, something seemed to be amiss.

And then the Financial Times dropped the bombshell that the registration documents had already been filed… last month… confidentially.

Admittedly, I didn’t even know a company could file confidentially, a process done offline so that it is not recorded electronically. Thanks to the JOBS Act, companies with less than a billion dollars in revenue can submit draft versions of their registration documents to the SEC, allowing the SEC to review, revise, and agree on a final version that will ultimately have to be made public. The takeaway here is that an OnDeck IPO is in the process and the registration documents will eventually be released. The law states that OnDeck must make the documents public at least 21 days prior to pitching investors.

The New Yorker walked readers through confidential registrations back when Twitter was planning their IPO, noting that it was not uncommon to choose this method, “Twitter is much like its peers: most small companies that have gone public since the passage of the JOBS Act have filed their S-1s confidentially,” the New Yorker said.

So why be secretive? The New Yorker continues to explain:

From the perspective of companies, the new rule has a couple of virtues. First, it allows companies that are thinking about going public to test the waters—they can gauge investor reaction, get feedback from the S.E.C. on their filings, and so on—before deciding if they want to go ahead with an I.P.O. If a company goes through that process publicly, and then decides to abandon the offering, its reputation gets damaged, even though it often makes sense for a company not to go public. Do it privately, and no one gets hurt.

-Source: http://www.newyorker.com/business/currency/the-virtues-of-twitters-confidential-i-p-o-filing

OnDeck’s biggest critics are their competitors, naysayers convinced that they are recklessly undercutting pricing to acquire market share. Indeed FT reported that OnDeck posted annual losses of $16.8m and $24.4m in 2012 and 2013, and losses of $14.4m in the first half of 2014.

With $1.3 billion funded since 2006, an independent report cited in the registration by Oliver Wyman estimates the untapped market to be between $80 billion and $120 billion.

With $1.3 billion funded since 2006, an independent report cited in the registration by Oliver Wyman estimates the untapped market to be between $80 billion and $120 billion.

There’s plenty of runway left, but OnDeck has yet to turn a profit. In An Insider’s Perspective, I wrote, “What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market.”

If the IPO goes through, we can all place actual monetary bets on the company’s future. What a trip that will be. I expect the stadium of insiders to get loud once the public documents are released. Good luck OnDeck.

Lend360: The Industry Event of the Year

September 5, 2014It’s being called the full circle of lending. Non-bank business lenders, merchant cash advance companies, peer-to-peer lenders, consumer lenders, lead generators, and Wall Street tycoons are descending on New Orleans from October 14th to 17th to attend Lend360. I’ve partnered up with the event through the DailyFunder name.

From the governmental arena, Governor Bobby Jindal (left) and U.S. Senator David Vitter (right) are speaking at the conference.

On the business side, here are some speakers you might recognize that are definitely confirmed.

- Brendan Carroll, Victory Park Capital

- Brendan Ross, Direct Lending Investments

- Scott Termini, Direct Media Power

- Bob Coleman, Coleman Report

- Heather Francis, Merchant Cash Group

- Nick Owens, Magnolia Strategic Partners

- Sean Murray, DailyFunder (myself)

- Ken Rees, Elevate

- Mark Curry, Sol Partners

- Sasha Grutman, MiddleMarch advisors

- Al Wild, Crest Financial

- Mark Doman, eBureau

- Tim Madsen, PartnerWeekly

- Dickson Chu, Ingo

- John Hecht, Jeffries

If you’re involved in MCA or business lending, you NEED to be there.

Here’s the most recent version of the agenda:

October 14-17, 2014 New Orleans, LA

In Partnership with

| REGISTER TODAY |

IFA Tells Merchant Cash Advance Companies to Get Lost

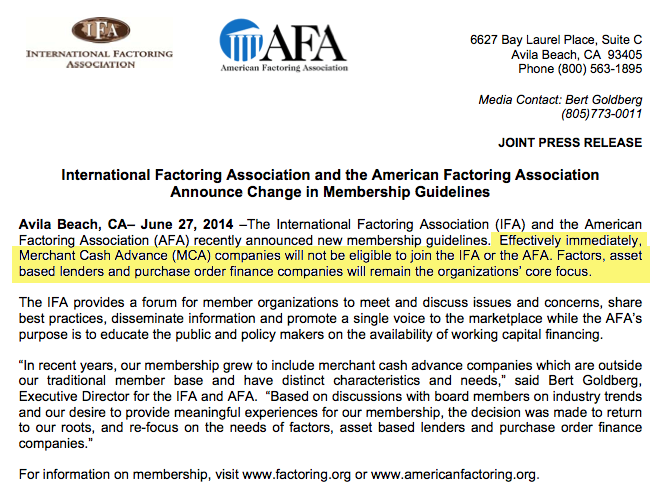

August 22, 2014On June 27, 2014, the International Factoring Association (IFA) and the American Factoring Association (AMA) publicly announced their decision to ban merchant cash advance companies from obtaining memberships. The nature of just how public that announcement was is questionable since nobody in the industry seemed to be aware of it, including a dozen plus merchant cash advance companies who have been longtime members of the IFA.

The timing of the ban is leaving a few companies unsettled since it was announced immediately following the IFA’s annual factoring conference in which merchant cash advance companies not only exhibited but were also amongst some of the event’s featured speakers.

To illustrate just how awkward the timing was, the IFA had just begun to thank everyone for attending the conference in the May/June issue of their magazine and in practically the same breath revealed that all merchant cash advance companies were banned going forward:

The IFA annual conference has grown to become the number one industry event for the factoring and receivable finance industry. The IFA convention is now the largest and most relevant event of the year, and as the attendees of San Francisco conference can attest to, it has become the must attend event of the year. Thank you to everyone that attended and helped the IFA achieve this unprecedented growth.

… … …

Due to the number of complaints that have been received, both the IFA and the AFA have voted to bar Merchant Cash Advance companies from membership in each organization. The boards of both associations felt that the model for this type of financing has changed and that there are a number of MCA companies that are not operating in an upfront manner. Given that the goal of both organizations is to assist the factoring community, we found it best to dissociate ourselves from this type of financing.

It is unclear if the IFA’s current merchant cash advance members were immediately terminated or if the rule only applies to new applications going forward. This is especially confusing since the feedback we’ve gotten from their members so far is that nobody knew this had even taken place.

Hopes for a peaceful breakup between the two industries has possibly weakened after a story was spotted in the July/August issue of the IFA’s Commercial Factor magazine aimed at attacking and discrediting merchant cash advance companies.

Hopes for a peaceful breakup between the two industries has possibly weakened after a story was spotted in the July/August issue of the IFA’s Commercial Factor magazine aimed at attacking and discrediting merchant cash advance companies.

The article by factoring attorney Steven N. Kurtz alleged that tortious interference, regulatory scrutiny, and rampant disorder were reasons to steer clear of merchant cash advance companies. A more detailed breakdown of his arguments can be found on dailyfunder, but it fails to mention the way he concludes the story:

At the moment, there seems to be too many new players in the merchant cash advance industry, with no experience and loose underwriting standards. There is likely going to be a shakeout because the industry segment has a high default rate and investors who lose money will lose their appetite for the deals. Before the market corrects itself, the factoring industry will have to ride out the storm by adjusting their business practices to effectively compete.

Did you catch his last sentence about riding out the storm? He’s saying to adjust, hold on, wait for a shakeout, and hopefully business for factoring companies will go back to normal. The reason it’s not normal now is because merchant cash advance companies are killing them competitively.

I guess if you can’t beat ’em, ban ’em? They should’ve just said that was the reason from the beginning…

On Deck Capital IPO, An Insider’s Perspective

August 16, 2014It was August 23, 2011, the day the Virginia Earthquake could be felt all the way up in New York City. The four of us were enjoying outdoor seating at a restaurant on the Upper East Side. The ground shook, my drink spilled and Ace looked at each one of us and said, “Okay so I’m putting you down for five deals this month.” OnDeck Capital’s relationship managers were aggressive. If you were a small Independent Sales Organization (ISO), they didn’t expect to get all of your dealflow so they roped you in little by little. It was hard to say no. If five deals was too much, Ace would say three and if three was too much, then he’d put you down for three anyway. Zero was not in the cards. OnDeck owned a specific niche and if you didn’t send your premium credit clients to them, then any ISOs you were competing against would. That was a death knell in those days. Just a few years earlier I would’ve shrugged them off, but public sentiment was changing. Merchants were embracing the fixed daily payment methodology and the merchant cash advance industry would never be the same.

OnDeck Capital is now going public. Will you buy stock?

I’m in a unique position to discuss OnDeck. I started my career in this industry before they even existed. I’ve competed against them as an underwriter at a rival firm, worked with them as a referral partner when I was in sales, and covered them in my capacity as Chief Editor of an industry trade publication.

I’m in a unique position to discuss OnDeck. I started my career in this industry before they even existed. I’ve competed against them as an underwriter at a rival firm, worked with them as a referral partner when I was in sales, and covered them in my capacity as Chief Editor of an industry trade publication.

I left my post as Merchant Cash & Capital’s Director of Underwriting in late 2008. I was 25, about a year or two older than the average employee in the industry. Several of MCC’s rivals got demolished in the financial crisis but OnDeck wasn’t one of them. They also weren’t much of a competitor either. Struggling to define themselves as the anti-merchant cash advance, their product ran counter to the spirit of the industry’s rise. The single biggest allure of a merchant cash advance wasn’t that it was easy to obtain but that there was no fixed repayment term. The funds came with a pre-determined net cost but no specific date on when the delivery of future sales would be due.

Outsiders like the news media aren’t exactly sure what separates merchant cash advance from OnDeck except for maybe the cost of funds. Cash advance just sounds expensive, doesn’t it?

Outsiders identify the company by three characteristics.

1. They’re a non-bank business lender

2. They’re more expensive than a bank

3. They’re a tech company

These bullet points gloss over the fact that OnDeck’s loans require payments to be made every day. Can you imagine a credit card company forcing you to send a payment every day of the month? Or your landlord asking for rent on the 1st of the month, the 2nd, the 3rd, 4th, 5th, and so on every day until your lease is up?

This is not to say that this system is necessarily bad for borrowers, but that it is quite possibly the most unique and important part of what makes OnDeck different. It’s their secret sauce. It is why OnDeck gets lumped in with merchant cash advance companies in many conversations. OnDeck and the legion of copycats they have spawned are part of a broader industry that includes merchant cash advance companies. I call them daily funders. Daily funders provide financing on the condition that payments are made daily. I don’t call them daily lenders because traditional merchant cash advance products are not made by lenders, but by a unique group of investors that purchase future revenue streams.

Transition

Under company founder Mitch Jacobs, OnDeck had established themselves as the de facto loan option.

The merchant’s not biting on merchant cash advance? Send it to OnDeck. The merchant doesn’t accept credit cards? Send it to OnDeck.

They were every merchant cash advance ISO’s frenemy. They’d solicit you for your deals and then throw you under the bus to journalists as evil purveyors of expensive financing. They needed us to source dealflow and we needed them to maximize closing ratios but neither was quite satisfied with the arrangement.

When the company’s first employee took over as CEO in June 2012, the rhetoric changed. While still happy to be portrayed as the anti-merchant cash advance, OnDeck transformed their image from a niche Wall Street lender to a Silicon Valley-esque tech company. Noah Breslow was a curious choice. He has a BS from MIT and an MBA from Harvard Business School. He’s tall, charismatic, and he introduced vocabulary words such as algorithm to an industry that relied entirely on manual human underwriting.

At a recent lending conference, the younger crowd characterized Breslow as the Steve Jobs of business loans. He commands a cult-like following inside and outside the company, and in 2013 was embraced by New York City’s Mayor Bloomberg.

Breslow fast tracked OnDeck. With only $43 million raised in the first 5 years, the company went on to raise more than $300 million in the first 24 months under Breslow’s leadership.

This was their plan all along

In November 2012, OnDeck entertained a buyout offer from UK-based payday lender Wonga in which they reportedly received a $250 million valuation. The deal fell apart in the late stages but at the time I believed the negotiations were all a ploy for OnDeck to get a true market valuation. With a solid offer on the table, they knew both where they stood and where they needed to go. Last week the WSJ reported that preliminary IPO discussions valued them at $1.5 billion, six times higher than where they were two years ago.

With stock options being offered to new employees at least as far back as 2012, the plan to go public should come as no surprise. Later this year, those employees may actually get to do something very few startup workers ever get to do, convert those options into real shares.

So will OnDeck ride off into the sunset of billion dollar bliss? Not so fast say several industry insiders, some of whom are itching to short the stock on the first day they can.

Smoke and mirrors?

Smoke and mirrors?

As OnDeck took advantage of the swing in public consensus (that fixed terms were better and lower costs increased the attactiveness ), insiders began to ask an important question. Why weren’t merchant cash advance companies collectively countering with lower prices to remain competitive? Greed was fingered by journalists especially in the wake of the financial crisis. But greed is a weak prerogative if you consider that merchant cash advance companies were filing for bankruptcy left and right in 2009.

And oddly or perhaps even ominously, an entire segment of merchant cash advance companies began to raise their prices just as OnDeck was lowering theirs. When I wrote The Fork in the Merchant Cash Advance Road in April 2011, I said:

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

Risk was and still is the number one reason that merchant cash advances cost so much. While it’s true that OnDeck serviced higher credit businesses, insiders speculated that the spreads were too thin. For years, OnDeck’s merchant cash advance competitors have doubted the soundness of their model.

It’s a debate that continues even to this day and yet OnDeck has secured hundreds of millions in investments from companies like Google Ventures, Goldman Sachs, Peter Thiel, and Fortress Investment Group. Their notes got an investment grade rating from DBRS. And as far as volume is concerned, they have likely eclipsed the industry’s all time reigning giant CAN Capital. If they had reached none of these milestones, OnDeck would have little credibility to convince critics of their sanity.

It’s a debate that continues even to this day and yet OnDeck has secured hundreds of millions in investments from companies like Google Ventures, Goldman Sachs, Peter Thiel, and Fortress Investment Group. Their notes got an investment grade rating from DBRS. And as far as volume is concerned, they have likely eclipsed the industry’s all time reigning giant CAN Capital. If they had reached none of these milestones, OnDeck would have little credibility to convince critics of their sanity.

With a mountain of circumstantial evidence through big name backing in OnDeck’s favor, it seems to be indicative that the skeptics are wrong. But maybe they’re not. Could their model be both seriously flawed and superior at the same time?

It’s all about eyeballs

Going back to the 1990s, Internet companies have been judged, valued, and made famous by the price of eyeballs and the number of site visits. It’s a measure that’s never disappeared and according to USA Today is making a comeback. And while OnDeck Capital has always been based in New York City, true to their Silicon Valley form, their model has been to conquer market share first  and take on profitability second. In their case, it’s not eyeballs or site visits, it’s loan origination volume.

and take on profitability second. In their case, it’s not eyeballs or site visits, it’s loan origination volume.

Five months ago Breslow was quoted in the WSJ as saying OnDeck is “imminently profitable“. With seven years in business, it’s proof that their critics have been right all along, that their model doesn’t make money.

What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market. Disbelievers in this long term wildly risky strategy are salivating at the opportunity to inspect the company’s financial statements in the IPO.

In When Will the Bubble Burst?, RapidAdvance CEO Jeremy Brown, whose company became part of the Quicken Loans family last winter, fired shots at OnDeck, “To accomplish high growth rates, which may be driven by a desire or need for an IPO or to raise investment or to sell to private equity, assets are being overpaid for through higher than economically justified commissions (I’ve heard 12-15 points upfront from the more aggressive companies) and stretch the repayment term of the MCA or loan even further (On Deck24, I am talking about you).”

Insiders testify that OnDeck’s strategy has not so much been about lower costs but about growth at all costs. Among the evidence is the sudden removal of an industry-wide practice of verifying the business owner is current on their rent. Repayment terms are getting stretched out, commissions have shot up, and for a while they ran a program that allowed applicants to get funding with the submission of just a single bank statement.

Merchant cash advance companies look at their own default figures and scoff at the notion that OnDeck’s aggressive practices could produce low single digit defaults as they’ve publicly claimed.

Imminent

Through it all, there remains the fact that OnDeck has never claimed their methodologies to be profitable, at least not yet. Red ink at IPO time might reward their detractors with a certain delicious satisfaction, but what will they say if and when they become profitable?

Through it all, there remains the fact that OnDeck has never claimed their methodologies to be profitable, at least not yet. Red ink at IPO time might reward their detractors with a certain delicious satisfaction, but what will they say if and when they become profitable?

I’m reminded of The 20 Smartest Things Amazon Founder Jeff Bezos ever said. Below is a few of them.

- “There are two kinds of companies: Those that work to try to charge more and those that work to charge less. We will be the second.”

- “Your margin is my opportunity.”

- “We’ve done price elasticity studies, and the answer is always that we should raise prices. We don’t do that, because we believe — and we have to take this as an article of faith — that by keeping our prices very, very low, we earn trust with customers over time, and that that actually does maximize free cash flow over the long term.”

- “If you never want to be criticized, for goodness’ sake don’t do anything new.”

- “Invention requires a long-term willingness to be misunderstood. You do something that you genuinely believe in, that you have conviction about, but for a long period of time, well-meaning people may criticize that effort. When you receive criticism from well-meaning people, it pays to ask, ‘Are they right?’ And if they are, you need to adapt what they’re doing. If they’re not right, if you really have conviction that they’re not right, you need to have that long-term willingness to be misunderstood. It’s a key part of invention.”

I wonder if the executive team at OnDeck would share these philosophies.

They’ve always claimed themselves to be a tech company, much to the bewilderment of their competitors. Will technology come through for them?

The data available on businesses has changed. Bank statements and a credit report might’ve been all there was to go on when the company first started, but in Automated Intelligence Breslow said, “the fact is most businesses operating today, in 2014, are already technology focused to one degree or another. They have computers, they have online banking, they use credit card processors, their customers are reviewing them online, there are public records, etc. All this electronic data helps paint a deeper and more accurate picture of the health of a business.”

With such easy access to important data, it might be possible that through the use of 2,000 data points, OnDeck doesn’t need to do all the manual investigations that their competitors still place high values on. The available data might be able to predict loan repayment success just as well as a human analyst.

And if that’s true, then they can reduce the cost of overhead as they scale. As their predictive algorithms get fed more data, they might be able to eliminate humans altogether. At the May 2014 LendIt conference, Breslow admitted that 30% of their loans were still manually underwritten but said that “if customers want full automation, we are prepared to deliver it.”

By that charge, a sustainable model should not be that far out of reach. Through advanced data analysis and decreasing fixed costs, profitability may indeed be imminent.

Winner

If the story of the merchant cash advance industry has been a race to the top, then OnDeck might be declared the winner in a successful IPO. It would be an ironic achievement for the company that positioned itself as the anti-merchant cash advance. In their wake today are hundreds of daily funders offering fixed payment products.

OnDeck’s critics are in a paradoxical position because a successful IPO is good for them too. They want to believe OnDeck’s model never worked, can’t work, and have it be proven a failure. But if it goes the other way, the legitimacy of the daily funder universe will be solidified in the mainstream. What’s good for the goose is good for the gander.

OnDeck’s critics are in a paradoxical position because a successful IPO is good for them too. They want to believe OnDeck’s model never worked, can’t work, and have it be proven a failure. But if it goes the other way, the legitimacy of the daily funder universe will be solidified in the mainstream. What’s good for the goose is good for the gander.

As AmeriMerchant CEO David Goldin said to Inc, “the OnDeck IPO shows that Wall Street is now taking this industry seriously.”

So does that mean he’d buy stock? Somewhere out there at a restaurant in New York City, an OnDeck relationship manager is probably putting Goldin down for five shares.

Cue the earthquake, the industry will never be the same.

Curious how it will change it exactly? Read my magazine published prediction, The Retail Investor.