Industry News

This So-Hot Robot Is Launching a Marketplace Lending Hedge Fund

January 26, 2017 LendingRobot has come a very long way since I first connected with them two years ago. Back then, CEO Emmanuel Marot was simplifying access to marketplace lending for individual investors by automating the decisions and executions. A year later, they were the first in the industry to introduce that technology via a mobile app. As someone who has used their service for a long time, one thing was always the same, the company helped you invest and monitor performance but they didn’t have custody of the actual money.

LendingRobot has come a very long way since I first connected with them two years ago. Back then, CEO Emmanuel Marot was simplifying access to marketplace lending for individual investors by automating the decisions and executions. A year later, they were the first in the industry to introduce that technology via a mobile app. As someone who has used their service for a long time, one thing was always the same, the company helped you invest and monitor performance but they didn’t have custody of the actual money.

That’s all changing with the announcement of their new hedge fund (“LendingRobot Series“), which will actually be separate and only open to accredited investors. The fund is managed by LendingRobot’s robo-advisor technology which scores, invests, and even manages secondary market activity without any need for human advisors. Basically the robots are doing the heavy lifting and they’re only investing in loan marketplaces such as Lending Club, Prosper and Funding Circle. Because of that, the fund only charges 1.00% of assets under management, and caps fund expenses at 0.59%.

The way Marot tells it, they’re taking the mystery out of a hedge fund. There’s no “black box,” he says. Instead, the fund uses Blockchain technology to deliver a public, unalterable ledger, so that LendingRobot Series investors see exactly which loans the fund is invested, where the defaults are, and exactly what the costs are across the fund.

![]() One of the biggest allures of investing in marketplace loans in this fashion is the liquidity offered. Investors don’t need to wait 3-5 years to wait for the loans to fully mature to take their money out. Investor money is converted to Units of ownership in these Series that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases.

One of the biggest allures of investing in marketplace loans in this fashion is the liquidity offered. Investors don’t need to wait 3-5 years to wait for the loans to fully mature to take their money out. Investor money is converted to Units of ownership in these Series that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases.

Marot said that the company only has 7 employees, yet they’ve managed to rack up more than 6,500 clients (myself among them) for their original service and have helped those clients deploy more than $120 million in assets along the way. They claim that they’ve been able to improve returns in alternative lending by more than 2.5%.

Founded in 2012, the company raised $700K in seed funding and $3M series A from Runa Capital.

As mentioned, LendingRobot Series is available to accredited investors only, and they’ll initially only allow 99 investors to participate in the fund with a minimum investment amount of $100,000.

Why Funding Circle Exited Spain

January 24, 2017

Funding Circle operates in the US, UK, Germany, and the Netherlands. Up until recently, they also counted Spain among its active European markets, but no longer. The timing is curious, right after the company raised $100 million through a round led by Accel, but upon a closer look, Spain was never really their thing to begin with.

“We inherited Spain following our acquisition of Zencap in 2015,” Funding Circle Samir Desai said. “We decided to pause new lending in June last year and we have now taken the formal decision to stop all new loans for the foreseeable future. We continue to invest in Europe in Germany and the Netherlands where we are growing fast, and expect to enter more countries in the future.”

Zencap was once said to be the fastest growing online lending marketplace in Continental Europe. In August 2015, Victory Park Capital had agreed to invest up to €230 million in loans originated by Zencap over a three year period. Funding Circle acquired them a mere two months after that, inheriting their operations in Germany, Spain and the Netherlands.

“Funding Circle will continue working on behalf of all investors to service the existing loan book,” the company said. “In total €16 million of loans have been completed in Spain, which is approximately 0.1% of cumulative global originations. Alternative roles in the company have been offered to the team and the company will retain part of the team to service the existing loans.”

“Funding Circle will continue working on behalf of all investors to service the existing loan book,” the company said. “In total €16 million of loans have been completed in Spain, which is approximately 0.1% of cumulative global originations. Alternative roles in the company have been offered to the team and the company will retain part of the team to service the existing loans.”

Ryan Weeks of AltFi, wrote of the decision to exit Spain, that it was a combination of limited awareness around P2P lending there and low quality loan applicants.

With more resources at their disposal now to focus on Germany and the Netherlands, the company also announced two new senior appointments. Thorsten Seeger has joined as Managing Director for Germany and Belkacem Krimi has joined as Chief Risk Officer for Continental Europe. Thorsten Seeger joins from Lloyds Banking Group, where he was Head of Financial Markets for SMEs and was responsible for driving and delivering access to financial markets for small businesses. Belkacem joins from GE Capital and brings extensive experience in credit risk and operational risk management, developed over 17 years across multiple countries in Europe and Asia. In his last role, he was the CRO for GE Capital France, based out of Paris – managing risk for over $10Bn consumer and commercial assets.

Desai, of Funding Circle, said, “We’re delighted to welcome Thorsten and Belkacem to the team. Both are hugely talented and have extensive experience and understanding of small business lending across Europe.”

But for now, it’s Adios to Spain.

The Top Small Business Lending Platform Finalists Named By LendIt

January 20, 2017The LendIt Industry Awards has named six finalists for the Top Small Business Lending Platform. They are:

- OnDeck

- Kabbage

- SmartBiz

- StreetShares

- Ascentium Capital

- iwoca

OnDeck you should know by now. They are publicly traded on the NYSE under ticker ONDK. We last sat down with them in October, shortly before they announced a $200 million credit facility with Credit Suisse.

Kabbage was one of the first online small business lenders to truly experiment with complete automation. In the last year the company has partnered with banking giants Santander and Bank of Nova Scotia.

SmartBiz ranked as the number one provider of non-Express, SBA 7(a) loans under $350,000 for fiscal year 2016. An online platform, they generated $200 million in funded SBA 7(a) loans through its bank lending partners during that period.

StreetShares has a strong focus on funding veteran small businesses. The company is also one of a very few to get approved for Reg A+ under the JOBS Act, which allows them to accept investments from unaccredited retail investors (with some limitations).

Ascentium Capital actually funded nearly $900 million to small businesses in 2016 and was acquired by PE firm Warburg Pincus just a few months ago.

iwoca is based in the UK but also operates in Germany, Spain, and Poland. They offer lines of credit to small businesses up to £100,000 with repayment terms of up to 12 months. Interest rates range from 2% to 6% per month. iwoca has raised £46 million through debt and equity.

According to LendIt, finalists for this category were awarded to the top small business lending platform based on a combination of loan performance, volume, growth, product diversity and responsiveness to stakeholders.

A similar category, the greatest Emerging Small Business Lending Platform also had six finalists. They include:

- ApplePie Capital

- Capital Float

- Credibility Capital

- Lendio

- Lendix

- Wunder Capital

More than 30 industry experts will judge and select award winners. You can view all categories, finalists and judges here.

You can also get 15% off the LendIt Conference registration with promo code: Debanked17USA.

Strategic Funding Source Integrates U.S. Operations of Capify

January 4, 2017New York, NY – Strategic Funding Source, Inc., today announced that it has entered into an agreement to integrate the United States operations of Capify into its adaptive proprietary operating platform. Both Strategic Funding and Capify have been providing non-bank financing options to small and mid-size businesses for over a decade. This integration enables Strategic Funding to expand its US operations by marketing to and providing capital to existing Capify customers who will, upon renewal of existing merchant cash advances or business loans, become part of the Strategic Funding family of customers.

“We are very pleased to have put together a deal with Strategic Funding that will provide our customers a future source of important capital. As a company that shares our values of providing simple, transparent and responsible access to capital for small and mid-sized businesses, it was a logical transition,” said David Goldin, Founder and CEO of Capify.

As part of the transition, many of Capify’s New York-based employees will become part of the larger and growing family of employees at Strategic Funding. The transition also allows Capify’s existing U.S. clients and partners the opportunity to take advantage of a larger variety of financing options, while still benefitting from the same standards of transparency and integrity that they have come to expect from Capify.

“It is rare that two companies in the same industry can come together and craft a synergistic deal that serves the best interests and strategies of each – but this integration does just that,” stated, Andy Reiser, CEO of Strategic Funding. “We have been friends of David and Capify for many years and have collaborated on and co-invested in the financing of many businesses over the years. We share the same focus on technology and quality underwriting that our customers, partners and the financial industry have come to expect from us. This transaction only strengthens the relationship between the two organizations”

ABOUT STRATEGIC FUNDING

Founded in 2006 and headquartered in NYC, Strategic Funding has been recognized by customers and the industry as one of the most reliable and respected names in small business financing. With flexible financing options, we have provided over 35,000 small businesses with the working capital they needed to take advantage of opportunities and grow. To learn more, visit www.sfscapital.com

Platinum Rapid Funding Group Originated $180 Million in 2016

January 3, 2017A social media post by Platinum Rapid Funding Group CEO Ali Mayar, revealed that the Long Island-based company had originated $180 million in deal flow in 2016. That’s almost twice their 2015 volume, and is a new record for the company.

In Mayar’s post, he wrote, “Thank you to everyone who’s a part of this unstoppable organization for an amazing year and the best is yet to come.”

deBanked’s Top 10 Most Read Stories of 2016

December 28, 2016

If 2015 was the year of the broker, well then 2016 was the year of readjusted expectations. The following are the top 10 most read stories of 2016 per our online analytics, some of which surprised even us. Either way, here’s what you read and shared on our website the most in 2016 in descending order:

10: Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

A 2015 story, it was the 10th most read in 2016. One thing the lending revolution has taught us is that a borrower’s bank statements can mean everything or nothing at all.

9: Should I start an ISO with only $2,000?

Even though this was published two full years ago, it managed to be the 9th most read story of 2016. The short answer to this question is no, don’t start an ISO with such a small budget especially not in 2016 or 2017.

8: Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

A big story early in the year was Madden v Midland, and the impact an appellate court ruling could have on marketplace lenders who rely on chartered banks to make loans for them in 50 states. This particular post and related ones attracted a lot of readers in 2016.

7: Business Loan Brokers and MCA ISOs Call it Quits

For the first time ever, brokers and ISOs began to say farewell to an industry faced with oversaturation.

6: Merchant Cash Advance Accounting – A How To Guide

Published two full years ago, the merchant cash advance accounting guide managed to be the 6th most read article on deBanked in 2016. The article is meant for MCA funders bookkeeping, not for merchants who use merchant cash advances.

5: Lending Club Borrowers Are Paying Off Really Early – And There’s Something Weird About It

Lending Club’s loan borrowers pay off their loans early at a freakish level. I pondered this in a blog post in February and the trend has not changed. To date, I’ve had 975 borrowers pay off early, nearly double since the time this was published.

4: Platinum Rapid Funding Group Sets Annual Funding Record

An astounding amount of visitors were interested in Platinum Rapid Funding Group’s 2015 origination volume. An announcement that the company had originated $100 million in deals was the 4th most read story of 2016.

3: Merchant Cash Advance Definitely NOT a Loan, New York Judge Rules

Yet another post referencing Platinum Rapid Funding Group, was a decision issued in a New York trial court. In it, a judge opined at length about the nature of purchasing future receivables.

2: Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

Despite being less than a month old, this story on its own was the 2nd most read of 2016, technically followed by this one and this one, both also about CAN’s recent issues. We combined them into one story for the purpose of this list since they were all related to the same event.

1: The Closer – Meet the Yellowstone Capital Rep That Originated $47 Million in Deals Last Year

The #1 most read story on deBanked in 2016 was a profile about a salesman at Yellowstone Capital. Juan Monegro, who originated $47 million worth of deals in 2015, was also recently reported to have matched that number again in 2016.

CAN Capital Shareholder Files Lawsuit

December 25, 2016Add an aggrieved shareholder to the list of CAN Capital’s recent messes. On December 19th, Deborah Clearman filed a motion for summary judgment in lieu of a complaint in the New York Supreme Court, alleging that CAN had failed to comply with a settlement agreement that stipulated she be paid $150,000 by November 14, 2016.

Clearman, who has been a shareholder of the company since 2003, is the owner of 83,362 shares of CAN Capital preferred Series A-1 stock and 48,078 shares of CAN Capital preferred Series A-2 stock, according to the settlement agreement now visible to the public because of New York State’s open court system.

The original dispute between the parties precedes the latest events rocking the company, though the alleged non-payment could be related to liquidity woes. CAN was only just served the summons on Wednesday the 21st and has not yet filed a response to the allegations.

CAN recently suffered a Rapid Amortization Event with their $200 million securitization, has suspended the funding of new deals and has laid off nearly half of their employees.

The lawsuit is registered as case number 656603/2016 in the New York County Supreme Court

CAN Capital’s Collateral ‘Adjustment’

December 24, 2016Last month, CAN Capital disclosed that they had “self-identified that some assets were not performing as expected” on the same day that three of the company’s top executives were put on leave. Since then it’s been reported that a discrepancy arose when CAN’s old systems were not equipped to handle the shift from variable payment advances to fixed payment loans. This is notable given that CAN began doing fixed payment loans all the way back in April 2010.

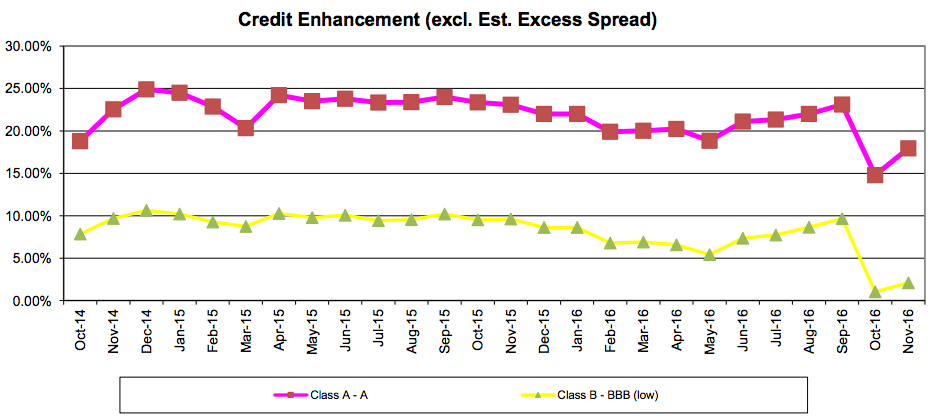

The discrepancy found its way into CAN’s 2014 securitization. S&P Global Ratings recently reported on this that “there was a correction of previously misclassified assets that affected the results of the calculation of [the] adjusted performing asset balance” on CAN Capital Funding LLC Series 2014-1.

Ratings agency DBRS illustrates the collateral dip on CAN’s securitization once the classifications were reported correctly on Series 2014-1 below.

This is the first public glimpse into what CAN’s old systems got wrong and by how much.

The drop triggered a rapid amortization event, potentially causing liquidity issues for CAN, hence why new funding may be paused. The principal balance on the $200 million notes has dropped by nearly $70 million in the last two months, indicating big payouts.

The process to manage a rapid amortization event is described in the original DBRS ratings report. The implications aren’t good given that this appears to be brought on by misclassifying assets rather than a natural deterioration of loan performance.

Last week, CAN laid off nearly half of its employees as it tries to correct course.

Update: On December 25th, deBanked published a brief of a newly discovered lawsuit filed against CAN Capital on December 19th by an aggrieved shareholder alleging the company had failed to pay her a $150,000 settlement payment.