Industry News

In This Online Lender’s Earnings Report, Profits, MCAs and Term Loans

March 22, 2017Limited details were offered when Enova, a publicly traded company, acquired The Business Backer (TBB) in June 2015. For one, the Cincinnati Business Courier had the exclusive, which one might not describe as the typical go-to source for online finance news. But TBB was not typical. Based in Blue Ash, Ohio as opposed to New York City or San Francisco, the company had originally focused on offering merchant cash advances before eventually expanding their suite of solutions to include other products.

According to Enova’s earnings report, TBB had been purchased for $26.4 million with an estimated contingent $5.7 million of that being based on future earn-out opportunities. There was a caveat though. If future operating results exceeded expectations, that contingent amount could increase over time, but not beyond where the total consideration paid for the company exceeded $71 million. As of 2016’s year-end, that contingent amount had increased by $3.3 million.

Enova’s report makes several mentions of their merchant cash advance business or as they call them, receivable purchase agreements (RPAs). For the most part, they obscure the financial metrics of this aspect by lumping it in with installment loans. These installment loans are described as “multi-payment unsecured consumer installment loan products in 17 states in the United States and in the United Kingdom and Brazil” with repayment periods of two to sixty months, so yeah, they’re pretty different.

Their RPA customers, however, “average approximately $1.5 million in annual sales and 10 years of operating history while those who obtain an open line of credit account average approximately $450 thousand in annual sales and 7 years of operating history,” the report says. These lines of credit are primarily offered through a business lending subsidiary called Headway Capital.

While companies like Lending Club and OnDeck grab all the headlines, Enova describes itself as a “leading technology and analytics company focused on providing online financial services.” And in 2016, they extended nearly $2.1 billion in credit to borrowers and had a net income of $34.6 million.

On the company’s Q4 earnings call in February, Company CEO David Fisher said, “There currently seems to be a bit of a shakeout occurring in the non-bank small business lending and financing industry. A number of our competitors have either ceased funding or completely shut down over the past several months. From the intelligence we were able to gather, this is largely due to credit issues and their portfolios. As we mentioned last quarter, we have taken a more methodical approach than some to growth for our small business products. And we’re now seeing the benefits of that approach. Recent advantages of our small business book are performing well and the unit economics continue to improve especially as acquisition costs have dropped following the shakeout I just mentioned.”

Enova’s small business financing portfolio only constituted 12% of their loan portfolio at the end of last year. And at $13.70 a share, the company’s current market cap is larger than OnDeck’s.

Prosper Lost A Whopping $119 Million in 2016

March 20, 2017 Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

| Year | Revenue | Profit (Loss) |

| 2012 | $7.6M | ($16.0M) |

| 2013 | $18.3M | ($27.0M) |

| 2014 | $81.3M | ($2.6M) |

| 2015 | $204.2M | ($26.0M) |

| 2016 | $136.0M | ($118.7M) |

General and Administrative was the largest line item expense at $102.7M, which consisted mainly of employee compensation. The second largest expense was Sales and Marketing at $70.1M.

The company originated more than $2.2 billion in loans for the year, down from $3.7 billion last year.

“The decrease in originations we experienced during the year ended December 31, 2016 were primarily driven by a number of our largest investors pausing or significantly reducing their purchases of Borrower Loans beginning in the second quarter of the year,” their earnings report said. “We believe these investors have paused or reduced their investment activity because of an increase in their cost of capital; negative actions and publicity at competitors; and our limited use of investor rebates, which have become more prevalent in the industry.”

To try and correct course, Prosper offered to sell up to 35% of their company to a consortium of Wall Street’s elite who have the right to buy up to $5 billion of their loans over the next 2 years.

WebBank Releases Earnings, Market Valuation

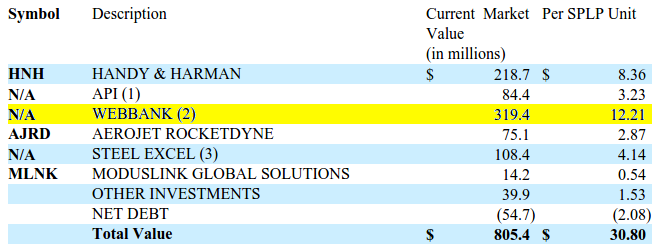

March 20, 2017 WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

“Despite significant declines in a number of WebBank’s key programs, caused by capital market disruptions, WebBank successfully added new partners, new products and began holding more assets to maturity in 2016,” the report read.

Although Steel Partners also owns businesses in energy, defense, logistics, food products and more, WebBank is its most valuable segment with a market valuation of $319.4 million. That number, according to the release, is 12x the company’s after-tax net income.

Steel Partners got in on WebBank early, making their initial investment in the bank more than 20 years ago in 1996.

“WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank’s products,” the report says.”Revenue is largely derived from these loans, which provide fee and interest income.”

Brickell Capital Finance Inks Deal with Liquid FSI Convert2Pay™

March 16, 2017Miami, FL. March 16, 2017—Brickell Capital Finance, Inc., a leader in providing consumer facing loans to the healthcare industry, will offer Liquid FSI’s Convert2Pay™ through its 75 sales reps nationwide.

Eli Mualin, President and CEO of Brickell said, “We believe that Convert2Pay is a ‘game changing’ Fintech product for the healthcare industry. It allows providers to convert their existing insurance claims on-demand. It will change the way healthcare professionals access business capital and Brickell wants to be part of that.”

“Convert2Pay is a user directed revenue cycle management tool that allows providers to open a gateway to low cost spot liquidity. It is designed to replace higher-cost offerings like business advances and complicated factoring products,” said Frank Capozza, President and CEO of Liquid FSI developer of Convert2Pay™.

“Brickell is a good distribution partner because they have a strong reputation with healthcare providers. Our goal is to drive liquidity into the healthcare ecosystem,” Capozza said.

For more information contact:

Frank Capozza

Liquid FSI, Inc.

www.liquidfsi.com

646-620-6088

Mel Chasen, Founder of Rewards Network and a Merchant Cash Advance Visionary, Has Died

March 15, 2017 Melvin Chasen passed away on Monday. He was 88. Chasen founded Rewards Network in 1984 as Transmedia Network, Inc. and it went on to become the world’s largest dining rewards program. As part of that, the company pioneered the use of future sales to facilitate working capital to restaurants.

Melvin Chasen passed away on Monday. He was 88. Chasen founded Rewards Network in 1984 as Transmedia Network, Inc. and it went on to become the world’s largest dining rewards program. As part of that, the company pioneered the use of future sales to facilitate working capital to restaurants.

Transmedia became iDine Rewards Network in 2002 but was later shortened to just Rewards Network in 2003. While Chasen had an incredibly accomplished career, a newspaper obituary paying tribute to his life says that Transmedia, a specialized restaurant financing company, was his biggest business success.

A 1991 New York Times article explained the business model as follows: “It gives the restaurant $10,000, a debt that is paid off by providing $20,000 worth of meals to Transmedia customers. The customers pay Transmedia $15,000, a 25 percent discount from face value. If the restaurant goes out of business before Transmedia’s customers eat enough meals, or if customers do not patronize a restaurant, Transmedia suffers the loss.”

To think that concept was not only being applied 26 years ago, but was already a big hit, undoubtedly makes Chasen a top player in merchant cash advance lore. He will be greatly missed.

A service will be held on Thursday, March 16 in North Miami Beach. Memorial donations may be made to the ALS Recovery Fund.

Brief: New York’s Attempt to Over-Regulate Lenders Downgraded to Doubtful

March 14, 2017 The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The passage of this proposal now looks doubtful. The Assembly, one of two branches of the State’s legislature, introduced their own version of the budget on March 13th and removed the language.

“The Assembly rejects the Executive proposal granting DFS regulatory authority over any online lenders doing business in New York State,” the bill says. Notably, they also rejected “the Executive proposal to authorize enforcement of Insurance, Banking, and Financial Services Law against unlicensed individual or businesses, including bringing a civil action.”

The Senate echoed same. “The Senate denies the Executive proposal to authorize the Superintendent of the Department of Financial Services to expand the regulation of small loan lenders,” their bill states.

Industry trade groups, namely the Commercial Finance Coalition (CFC), had mobilized quickly to tell their members’ stories up in Albany two weeks ago. One of the group’s concerns was that they had not been consulted in advance, nor given any time to engage in a discussion about the proposal.

“They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director. With the proposal’s chances of making it through the final budget by the March 31st deadline waning, the group and others may finally get an opportunity to do just that at some point later in 2017. According to The CFC, they are looking for additional companies to support them in that endeavor. Anyone interested in finding out how they can help should contact Dan Gans at dgans@polariswdc.com.

Brief: Former CAN Capital CFO Moves On

March 9, 2017According to the WSJ, Aman Verjee, who was CAN Capital’s CFO up until late last year, has taken the COO position at 500 Startups. The company has invested in more than 1,800 startups across more than 60 countries. According to the website, “500 Startups was founded in 2010 by former PayPal and Google alumni Dave McClure and Christine Tsai, along with many other friends and supporters.”

CAN Capital has not yet named a replacement CFO.

Letter From the Editor – Jan/Feb 2017

March 4, 2017When deBanked first launched online in 2010, I thought it was too late, that perhaps all the exciting changes in alternative finance had already taken place and that aside from a few obsessed geeks, there wasn’t that big of an audience to write for. It certainly felt a bit out-of-style, especially since I had been working in the industry for more than four years by that point. The only publication that was dedicated to the scene at the time had already come in to the public eye and vanished. Many alternative financial companies had met the same fate, thanks to the financial crisis.

In a way, deBanked started off as a post-apocalyptic diary, an accounting of the industry’s survivors and their roles in the new world order. Primitive, my reporting may have been then, but interest quickly grew. By mid-2011, I was already forced to change web hosts to keep the website from slowing down. In my day job as a commercial finance broker, I continued to talk to small business owners all the over the country about a common theme, that banks just weren’t lending. And maybe they never would again, some predicted anyway. Or maybe the way loans were made in general would just never be the same.

Looking back among my old 2011 stories, I discovered that I had written a personalized review of Square’s payment technology and had given it high marks. Back then however, I saw Square as a payments toy. It was innovative and sexy, but unrelated to lending. Fast-forward to 2016 and Square’s capabilities have expanded. I should know, they funded my business exactly five years after my review. In this issue, I’ll walk you through what it was like to play the role of borrower, and put marketplace lending up to the ultimate test. Thanks to Square Capital, my journey has come full circle or more appropriately, full square.

This issue is the first of 2017. For alternative finance, it fortuitously feels like the beginning, not the end. If our descendants far in the future stumble upon these stories, I pray they will enjoy our accounts of the transformation, when entrepreneurs dared to look at the world in front of them and boldly decided to change it. It was the early 21st century, historians will say, when mankind dared to de-bank and change everything we knew about finance. In the here and now, you are a part of it all…