Industry News

Breakout Capital Closes $20MM in Credit Facilities with Medalist Partners

July 8, 2020MCLEAN, VA / July 8, 2020 / Leading nationwide small business lender Breakout Capital announced today the completion of two senior secured credit facilities, totaling $20MM, with Medalist Partners, expanding and extending a current term loan facility and establishing a new term loan facility with attractive forward flow features with its long-time lending partner. This expansion of its successful ongoing partnership with Medalist further validates Breakout Capital’s vision and growth through product differentiation, innovative responses to small business needs and disciplined, long-term strategy. These facilities will allow Breakout to increase loan originations across all of its product offerings, including its highly regarded term-loan product, FactorAdvantage®, and its newest, well-received factor product, FactorBridge.

“I am pleased to continue our successful relationship with Medalist Partners. Medalist is a disciplined and engaged credit facility provider who shares our vision and believes in the strong value we bring to small businesses across the country,” said McLean Wilson, Breakout Capital’s CEO and Chief Credit Officer. “The expansion of this strategic relationship will accelerate the growth of our “white-hat” brand and the continued introduction of innovative new lending solutions to the market.”

John Slonieski, Director of Private Credit for Medalist Partners, added, “We are pleased to enhance our relationship with Breakout Capital in our asset-based lending strategy. Their high-quality underwriting and SMB-friendly lending solutions, coupled with their talented credit and management team, provide us confidence as we continue working closely with them to successfully scale their lending program.”

Given the deployment of these Medalist facilities and increased market demand from the rollout of FactorBridge and expansion of FactorAdvantage®, Breakout Capital has in parallel raised its loan size up to $1,000,000. It has done so while continuing to offer loan terms of up to 24 months, offering flexibility through FactorBridge to provide shorter-term solutions that bridge to these longer-term Breakout Capital loans.

“The increase in our maximum term loans provides much-needed additional liquidity to small businesses, enabling them to implement critical strategies and capitalize on time-sensitive opportunities during these unprecedented times,” Wilson stated. “It also facilitates powerful dual factoring-loan solutions where we provide critical working capital loans to SMBs in tandem with accounts-receivable based factoring platforms offered by our valued factor partners.”

About Breakout Capital

Breakout Capital, headquartered in McLean, Virginia, is a leading fintech company, offering innovative small business lending solutions across the country. Breakout Capital is committed to transparent and responsible lending solutions through product innovation, small business borrowing education, and advocacy against predatory lending practices and continues to empower small business through right-sized lending, suitability testing, improving terms and supporting the long-term financing objectives of small businesses.

About Medalist Partners

Medalist Partners is an SEC registered investment manager with approximately $2.4 billion in assets under management as of June 30, 2020. The New York based firm manages strategies in asset-based private credit, structured credit, and collateralized loan obligations. The business is led by partners Greg Richter, Brian Herr and Michael Ardisson, who were formerly part of Candlewood Investment Group and prior to that Credit Suisse.

PayPal Appoints New Chief Accounting Officer

June 17, 2020PayPal promoted Jeffrey Karbowski from Global Controller to Chief Accounting Officer. Karbowski is also the company’s vice-president. His new position takes effect on July 31, 2020.

Karbowski has been with the company since 2013.

The Commercial Finance Coalition Applauds Actions by the Federal Trade Commission and New York State to Thwart Bad Actors in Business Lending

June 11, 2020 The Federal Trade Commission (FTC) and the office of New York State Attorney General Letitia James have filed formal actions against two small business financing companies for allegedly using egregious and deceptive tactics to seize assets from small businesses, non-profits, religious organizations, and medical offices.

The Federal Trade Commission (FTC) and the office of New York State Attorney General Letitia James have filed formal actions against two small business financing companies for allegedly using egregious and deceptive tactics to seize assets from small businesses, non-profits, religious organizations, and medical offices.

“The Commercial Finance Coalition whole-heartedly applauds the efforts of the FTC and Attorney General James. As a coalition of responsible financial services companies committed to funding small businesses, the CFC believes there should be zero tolerance for bad actors and deceptive practices in our industry,” said Executive Director Dan Gans.

Gans added, “Hopefully this will serve as a warning to all companies in the business finance space to serve merchants through best practices centered on respect and integrity in compliance with state and federal law.”

The CFC is a not-for-profit alliance of innovative financial technology companies that are working together to deploy capital to help small and mid sized businesses grow.

Press Release

Contact

Dan Gans

626-755-6545

Release Date

June 11, 2020

CFG Merchant Solutions Enhances Partnership with Arena Investors and its Affiliates to Serve SMEs

May 29, 2020NEW YORK, New York., May 29, 2020 — CFG Merchant Solutions (“CFGMS”), a leading financier of small and medium-sized enterprises (“SMEs”), announced today that the company is building upon its partnership with Arena Investors, LP (“Arena”), in conjunction with Ceteris Portfolio Services (“Ceteris), an Arena servicing affiliate, in servicing and providing liquidity to Platinum Rapid Funding’s (“PRF”) merchant portfolio. CFGMS has been a leading capital provider to SMEs and an originator of advances to growing merchants, providing in excess of $400 million merchant cash advances since 2015. Arena has been CFGMS’s primary capital partner since 2016.

CFGMS and Arena are determined to prioritize the needs of PRF’s existing customers in the wake of the COVID-19 crises and its resulting impact on small businesses across the country.

“Arena is pleased to continue its partnership with CFGMS and its senior management team consisting of CEO, Andrew Coon, Chief Legal Officer and General Counsel, Robert Martini, and President, William Gallagher. Together, we remain deeply committed to serving the needs of PRF’s existing customers, particularly for ongoing financing and liquidity needs in an environment when even much larger businesses struggle to attract capital,” said Victor Dupont, who leads Arena’s investments in the financing of the SME sector. “We welcome further involvement with PRF’s customers and their affiliated ISOs and are committed to working collaboratively with all throughout the COVID-19 crises and beyond”.

“Arena and its affiliates have built a reputation as a group that combines uniquely flexible capital with broad-based expertise in servicing, resolutions, and SME finance,” said Coon. “So, while we excel at sourcing, originations, and underwriting, we felt that they brought a critical level of IP and know-how that is uniquely suited to benefit all parties in today’s environment. Combining forces to offer a broader set of servicing solutions to the MCA market segment made complete sense.”

Jonathan Pike, CEO of Ceteris, added: “Ceteris is excited to work with CFGMS and Arena by offering best-in-class servicing strategies and assisting merchants in a difficult economic environment.”

The Small Business Association (“SBA”) estimates that traditional banks still reject approximately 90 percent of SME loan applications. Since 2015, CFGMS has emerged as a proven platform that leverages sales partner relationships, analytics, and proprietary underwriting to provide SMEs with a straightforward and streamlined access to critical funding. The company addresses the fundamental capital needs of SME owners across a broad credit spectrum and through every stage of a business’s life cycle.

SMEs across a wide variety of industries that include restaurants, retail stores, salons, spas, dry cleaners, auto body shops, and professional offices. All of these businesses, and more, rely on CFGMS to secure the necessary capital they need to grow.

For questions or funding solutions, please contact:

– William Gallagher

– (646) 880-3817

– WGallagher@CFGMS.com

– Ryan Banda

– (856) 545-8322

– rbanda@ceterisassetsolutions.com

About CFGMS

Headquartered in New York, NY, CFGMS specializes in providing financing to support the growth and development of underserved small-to-medium sized businesses that lack access to traditional bank funding. Founded in 2010, CFGMS’s affiliated company, CapFlow Funding Group, provides factoring, purchase order finance, and asset-based lending solutions. CFGMS and CapFlow have together provided over $1 billion in liquidity solutions to their SME clients. For more information please visit www.cfgmerchantsolutions.com

About Arena Investors, LP

Arena Investors is a privately held, SEC-registered, global alternative investment firm which combines mandate flexibility, proprietary sourcing and systems-plus-servicing to enable solutions for those seeking capital. The firm was founded in 2015 and is headquartered in NewYork with additional offices in Jacksonville, London, and San Francisco. For more information, please visit www.arenaco.com.

About Ceteris Portfolio Services

Ceteris is a nationally licensed servicing company providing debt recovery solutions and other related services for consumers and commercial businesses across a broad range of financial assets. Ceteris provides first- and third-party revenue cycle management, business process outsourcing and portfolio backup servicing to heavily regulated, high volume industries including banking, automotive finance, credit card, equipment leasing, medical, telecommunications, utilities, retail and other industries. For more information please visit www.ceterisholdco.com.

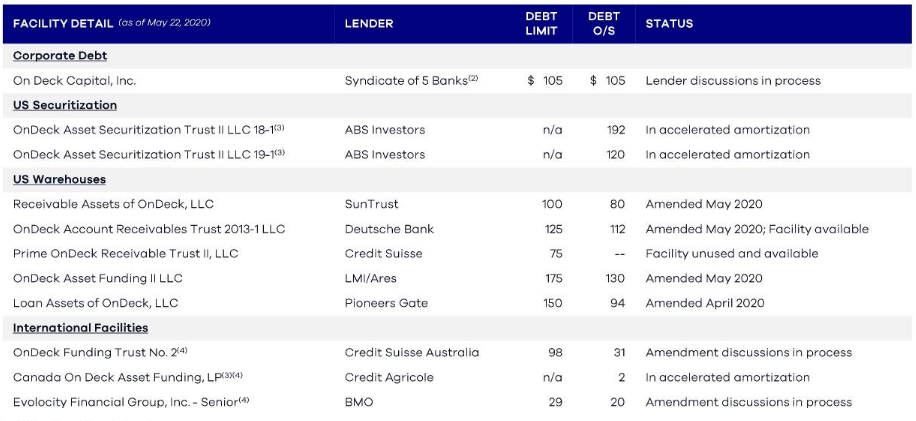

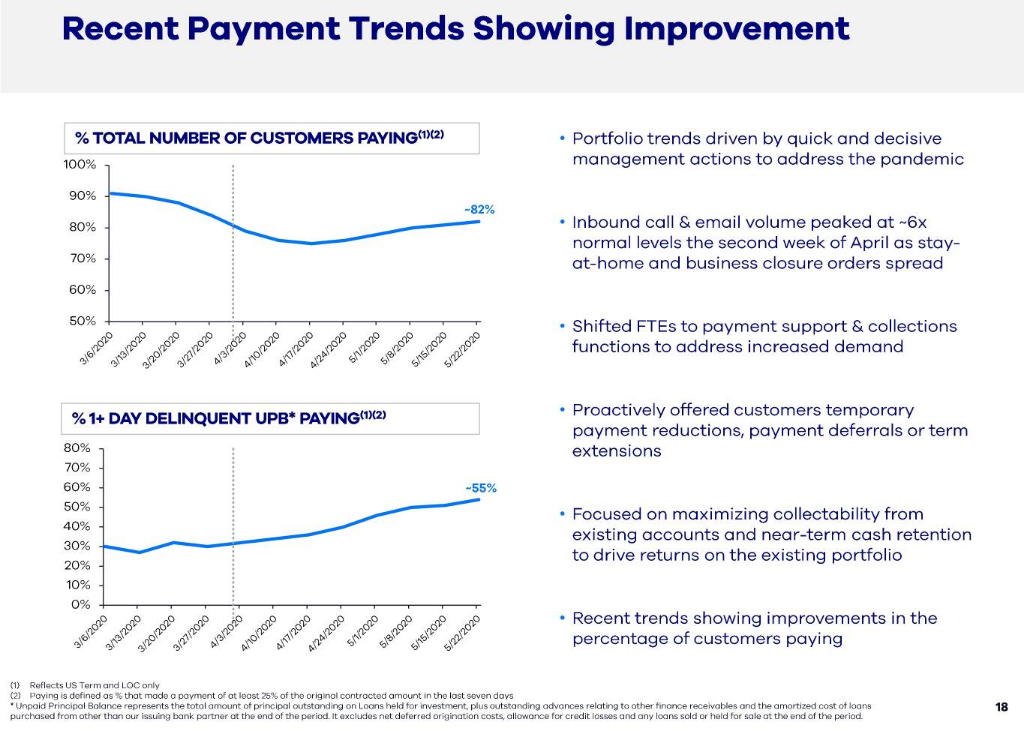

OnDeck Status Update

May 28, 2020

OnDeck submitted an unprompted mid-quarter update with the SEC early this morning on its status. Unlike previous submissions, the company prepared a visual of its debt situation. The bad news is that there is a good amount of negotiating with creditors left to be done. The good news was that there was an uptick in borrower payments. The attached graphics were pulled straight from their filing.

The company also said that it believes it is “well-positioned to benefit from economic recovery & market dislocation.” It based that belief on the below stated bulletpoints:

- Small business lending is a large market and will be critical in leading the economic recovery.

- OnDeck has deep experience from a 14-year operating history to increase originations with a targeted approach and reshape the portfolio.

- OnDeck is a scaled platform with demonstrated historical profitability and an established brand, unlike many competitors.

- Consistent with the last crisis, banks are likely to retrench further and only selectively serve SMBs.

- Expected consolidation of SMB lending industry will ultimately lead to improved unit economics and growth opportunities.

The full presentation, which is mostly a recap of the company’s Q1 earnings data, can be accessed here.

Most Brokers Plan to Minimize Use of a Central Office Post-COVID, Survey Suggests

May 26, 2020 A survey conducted by Overland Park, KS-based Strategic Capital revealed that only 36.8% of respondents plan to completely return to the office full-time after cities fully open back up. The vast majority of respondents were small business finance brokers.

A survey conducted by Overland Park, KS-based Strategic Capital revealed that only 36.8% of respondents plan to completely return to the office full-time after cities fully open back up. The vast majority of respondents were small business finance brokers.

44.7% selected that they would minimize office space or only use office space to house core team members while 18.4% planned to terminate their office lease altogether and adopt a work from home model permanently.

OnDeck Hits Payout Event Trigger on $105M Credit Facility

May 22, 2020Earlier today, OnDeck filed a status update to shareholders with the SEC. The company’s portfolio performance triggered an Asset Performance Payout Event (Level 1 they say) with a credit agreement that at present has an outstanding balance of $105 million.

The event triggers monthly principal repayments which, if not cured or amended, would commence with a $13 million payment on June 17, 2020. Subsequent principal payments are based on a percentage of the currently outstanding balance of $105 million until the Corporate Facility matures in January 2021. The Company is in active discussions with the Corporate Facility lender group to evaluate potential options with regard to this facility.

OnDeck was able to further modify agreements on two credit facilities (ODAF II and ODART) to which they had previously secured only interim relief of a few days.

Shares of OnDeck have hovered between 60 cents and 70 cents in the past week.

Broker Fair, Not a Webinar… A Virtual Reality Conference

May 21, 2020 Coming June 11th, Broker Fair in Virtual Reality. Much different from a webinar, Broker Fair Virtual will actually be a virtual world with a lobby, exhibit hall, networking lounge, and auditorium. Attendees will be able to interact with each other as well as visit and interact with sponsors at their virtual booths.

Coming June 11th, Broker Fair in Virtual Reality. Much different from a webinar, Broker Fair Virtual will actually be a virtual world with a lobby, exhibit hall, networking lounge, and auditorium. Attendees will be able to interact with each other as well as visit and interact with sponsors at their virtual booths.

There will be live video sessions too of course (see the agenda here), but if you’re there for the networking, get ready for a totally unique experience!

Broker Fair 2020 Virtual isn’t replacing the In-person event. That’s been rescheduled to 3/22/21 at the same location, Convene at Brookfield Place in New York City. All attendees registered for the in-person event are able to attend this virtual event on June 11th for free. If you never registered for that, you can still buy tickets that grant access to both at: https://brokerfair.org/register/

See you at Broker Fair!