Fintech

LendIt China 2019 is Canceled

October 23, 2019 LendIt Fintech has officially announced that there will be no conference in China this year after 3 long years in the country. A blog post written by LendIt Fintech co-founder Peter Renton explained that calamitous events engulfing the peer-to-peer lending industry there, namely the abundance of fraud, and the government’s waning tolerance, has led them to believe that no lending companies will be interested in speaking, sponsoring or even attending this year.

LendIt Fintech has officially announced that there will be no conference in China this year after 3 long years in the country. A blog post written by LendIt Fintech co-founder Peter Renton explained that calamitous events engulfing the peer-to-peer lending industry there, namely the abundance of fraud, and the government’s waning tolerance, has led them to believe that no lending companies will be interested in speaking, sponsoring or even attending this year.

“We will regroup in 2020 and hopefully will be able to bring our unique event back to China,” Renton wrote.

The decision only applies to their Lang Di Fintech China event. Their US event is scheduled to take place in New York this year on May 13-14 at the Javits Center. That event will be immediately followed by deBanked’s Broker Fair 2020 at the brand new Convene at Brookfield Place on 225 Liberty Street in New York on May 17-18.

Federal Judge Rules New York’s “Win” Against OCC’s Fintech Charter Nullifies The Fintech Charter Concept Entirely

October 21, 2019 The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The outcome is a byproduct of a ruling issued on May 2nd where the OCC had sought to dismiss the challenge from the onset. DFS was somewhat victorious then in that the case was allowed to proceed, be litigated, and eventually tried. But the OCC felt the case was lost before it had begun because “the Court [had already] ruled on the issue of the law at the heart of the case: whether, under the National Bank Act, OCC has the authority to issue special purpose national bank charters to financial technology companies that do not accept deposits.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

As a result, OCC negotiated with DFS to reach an agreed upon final judgment in DFS’s favor. The only remaining question was to what level of defeat the OCC would concede. OCC argued a judgment should preclude only New York companies from applying for a fintech charter while the DFS argued it should apply beyond New York’s borders to all 50 states.

On Monday, the judge went with DFS’s version, pointing out that ordinarily prevailing on an Administrative Procedure Act claim, as OCC had indeed consented to judgment on, would mean that the agency’s order would be vacated, not that the plaintiff would win some special relief.

It is hereby ordered, adjudged and decreed that:

OCC’s regulation 5 C.F.R. 5.20(e)(1)(i), is set aside with respect to all fintech applicants seeking a national bank charter that do not accept deposits.

DFS Superintendent Linda A. Lacewell issued an official comment on the ruling:

This decision makes the financial well-being of consumers from New York and around the country a priority. It reflects the rational conclusion that DFS and other state banking regulators have the expertise to provide the strict supervisory oversight and enforcement of anti-money laundering and consumer protection statutes and regulations that non-depository financial service providers are required to follow. The decision stops OCC’s attempt to usurp state authority by establishing a federal fintech regulatory framework at the expense of consumers. Going forward, DFS will continue to be a fierce advocate for consumers in New York and nationwide.

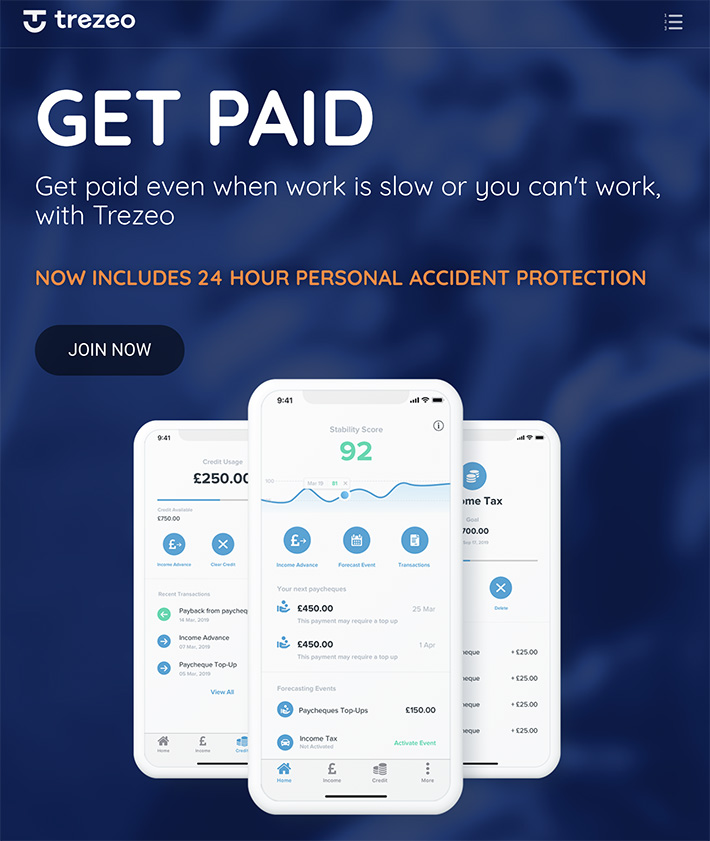

Salaries For All, Even For Gig Workers

October 16, 2019 “If we don’t solve the problems, there’s just a nightmare coming.”

“If we don’t solve the problems, there’s just a nightmare coming.”

This is how Trezeo’s CEO and Co-founder Garrett Cassidy views the work that he and his company are doing. Created in 2016 with the aim to provide support to self-employed people via income smoothing, Trezeo offers workers whose income streams may be irregular the opportunity to have structured and regular paydays similar to those who earn a salary. And with the number of self-employed in the UK currently at approximately five million, as well as projections showing that the majority of US workers will be freelancers by 2027, the company sees its efforts as essential to solving future problems. “There’s a lot of noise around the gig economy,” Cassidy asserted. “But the world is moving that way and we’re very much like ‘that’s fine, you can push back all you want, it’s going that way and we need to create the services that will work for these people.’”

The way it works is that Trezeo serves as an alternative lender, offering regularly paid funds to the customer’s account in exchange for their income that comes in at a later date. A major difference between it and other alternative lenders though is that Trezeo does not charge interest on these advances, instead collecting its revenue from a weekly membership fee of £3.

“We want to allow them to build their own financial resilience and also start looking a bit more useful for traditional financial institutions to engage with,” Cassidy explained. “Our ultimate vision is if you choose to be freelance or self-employed why should you cut yourself off from financial security, why should you trade flexibility for security, and, therefore, that’s the whole ethos of the income smoothing.”

Beyond this service Trezeo has plans to include additional features, such as an income verification system that would help workers be approved for large loans, like mortgages, from banks; as well as an opt-in pension, where instead of being committed to paying a fixed amount each pay cheque, customers could pay 5% of their total income for that period. Trezeo has already gotten the ball rolling with such expansions with the release of its personal accident and disabilities insurance, which covers customers for £300 per week for six months in the case that they are unable to work.

While it may sound as if self-employed and freelance workers are signing up for Trezeo to be their surrogate employer, Cassidy is quick to emphasize that this is instead a new system built to reflect the opportunities presented by technology, distant but reminiscent of the employment structures that came before.

“We’re trying to recreate [the structure] in a way so that a self-employed person controls it and over time can decide what they want … We’re not trying to make them employees, we’re very careful about that, but we’re trying to make it an employee-like experience for them so that they can very easily manage their finances and see them like an employee traditionally would … Platforms are making it easier for people to take the choice of flexibility.”

Speaking to Cassidy in Trezeo’s Irish office in the National Digital Research Centre, an early stage investor in tech companies, we’re snuggly located close by St. James’s Gate Brewery, where the cobbled streets are filled with the nutty and barley-laden smell of Guinness being brewed.

From here is where the development team operates, whereas the risk, sales, and marketing teams work from their London office, with the UK being their only market at this time. However Cassidy assured me that the company is looking interestedly abroad to Western Europe and America with plans to expand.

“This is a very big niche globally,” Cassidy remarked. “And as we’ve gone along, we’ve realized how much of an impact we can have.”

A Tough Neighborhood: Ashton Kutcher-Backed Startup Can’t Pay Employees

October 9, 2019 Neighborly, a San Francisco-based startup backed by Kutcher, announced yesterday that it won’t be able to pay its employees for the foreseeable future. In an internal memo that was viewed by Bloomberg, the decision to cut pay was described as “needed” due to the company’s current phase of change it is experiencing as it pivots from one marketplace to another.

Neighborly, a San Francisco-based startup backed by Kutcher, announced yesterday that it won’t be able to pay its employees for the foreseeable future. In an internal memo that was viewed by Bloomberg, the decision to cut pay was described as “needed” due to the company’s current phase of change it is experiencing as it pivots from one marketplace to another.

The business was founded in 2012 with the intention to connect investors to local projects through municipal bonds available in small increments. In July Neighborly announced its intentions to move away from this industry and cut 25% of its workforce, while in August CEO Jase Wilson wrote a Medium blog post discussing the company’s plan to shift into the information infrastructure market. Due to the municipal bonds market being “less reliable” than originally thought, Neighborly would no longer aid the raising of funds for projects such as a new fire truck in Lawrence, Kansas or new bike paths in Burlington, Vermont, instead it would prioritize the expansion of fiber-extensive broadband to communities it classifies as ‘under-connected.’

Or at least that was the plan. “As of tonight, we are not in a position to compensate you,” wrote Wilson in the internal memo before notifying employees that they wouldn’t be required to work going forward. Asked by Bloomberg whether or not this meant that Neighborly would be applying for bankruptcy protections, Wilson declined to comment but said that he didn’t see closure on the horizon. Instead, he asserted that the business’s investors “are all aligned on what we need to do, but this still comes with another difficult period of reorganization.”

Currently, Neighborly has projects in South Portland and Katahdin, Maine, as well as Stockton, California. It was reported that its previous efforts to develop Cambridge, Massachusetts using municipal bonds was not impactful, with the company only being credited by local authorities as a Senior Manager on 12 municipal bond transactions, most of which being under $20 million.

Kutcher’s Sound Ventures was part of a $5.5M funding round in 2015.

To Niche or Not to Niche, That Is the Fintech Question

October 1, 2019 A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

In the past decade, the fintech industry has followed this model to a tee. Whether it was B2B or B2C, fintech startups broke the banking business into narrower segments, offering singular niche services for various finance needs, e.g. credit card refinancing, small business loans, student loans, P2P payments, mortgages and more. From this model, big banks became the TGI Fridays of financial offerings (where you go to experience a full spread of financial services), and fintech platforms became the speciality grilled cheese shops (where you go to get the one thing you really crave).

Fintech Niches Fill Big Gaps

Many startups went niche not only because it was a business model that worked, but because the legacy banking industry model was out of date and there was room for true disruption. With these opportunities, niche fintechs could hone in on services that fulfilled singular needs, and they could do it with a focus, passion and dedicated customer service that most general banks couldn’t provide—and the results of this have been mostly positive. Globally, financial inclusion of unbanked people has improved. According to The World Bank, 69 percent of adults or 3.8 billion people now have an account at a bank or mobile money provider. In the U.S., niche fintechs made it easier for small businesses to get a loan post-recession. A host of online lenders stepped in to fill the gap, understanding that without access to relevant capital, small businesses struggle, which ultimately affects economic growth, jobs and inflation.

Can Fintechs Stand up to Tech Giants?

Tech giants thrive when users treat their platforms/offerings as a one-stop shop, something that is already commonplace in China, where millions of people use Tencent’s WeChat app to do almost everything—pay bills, book medical appointments, chat, play games, read news and pay for meals. Although this is not at the same level of activity in the U.S., it is a trend likely to continue.

The winds have been shifting as fintech companies question whether it makes sense to stay true to their niche or offer additional services as a path to scalability and profitability. By taking the latter path, former niche startups are now either a) building out and offering more financial services or b) partnering with more established companies/banks. Some recent examples include eBay and Square Capital, Venmo and Uber and KeyBank and HelloWallet. These partnerships seem to be a win-win—for the niche companies hoping to solve for scale and revenue stream issues, and for the established companies looking to offer complimentary services their core customers already use—but they also have fintech startups standing at a crossroads. Will working a niche be sustainable in 2020 and beyond, or is becoming a jack of all trades the only means of survival?

Beware of Diluting the Brand

For starters, the only means of survival for any fintech company is to solidly define what the company brand is and what it stands for. For example, many small business lenders are deeply passionate about fueling the American dream through helping business owners unlock their financial potential. Supporting small business is key to our country’s economic fabric. Dynamism and the ability to recover from an economic downturn are both dependent on startups’ ability to grow quickly, and in most cases, the only way for them to do so is through access to capital. For a fintech lender to become a trusted brand to small business owners, it must remain devoted to them as a company that has the financial wellbeing and vitality of small businesses in mind. This means facilitating the right loan for them, right when they need it.

The key for fintech companies is to be careful about diluting the brand. When companies stray too far from what they are passionate about, their core audiences suffer. Tech giants enter new spaces every day, whether from R&D or acquisitions. A strong brand (and the loyalty its customers have to it) will not only insulate a fintech company from the tech giant threat, but make its mission and voice stronger by comparison. Think about this the next time you are eating at In-N-Out Burger (sorry, East Coasters!). The humble hamburger shop became a cultural phenomenon through its razor-sharp focus on simplicity, quality and consistency.

Always Consider the Human Factor

Innovation and automation are both critical to survival in the fintech space. But how much tech can a fintech leverage in its solutions to avoid becoming too niche? The answer lies in understanding the core customers’ needs and how much technology can be used to fulfill those needs. For an e-wallet app, the key needs of customers are frictionless payments and transfers happening in real time; it is not a solution (when it’s working) that needs a lot of human interaction. A fintech company such as this can use technology and machine learning to automate most of its services.

Conversely, the human factor is still a huge part of the equation in some fintech services. For example, a person’s livelihood is at stake when a small business takes on a loan or another capital solution for its growth needs. This is a very personal and consequential decision for a business owner. In fact, in the majority of cases, they don’t want to rely solely on a technology-powered platform to deliver the most appropriate loan options for their needs, not to mention address their specific concerns and questions. A fintech lender can leverage technology at every touchpoint to optimize the application and loan approval process; but ultimately, many business owners will desire interaction with a live representative, not a chatbot. The human factor is crucial in business lending, and something that could become lost as a result of brand dilution. While scalability is important, customer service is equally so.

In the end, the decision to offer niche services or to go wide will depend on what’s at the core of a fintech company. Indeed, the pressures to scale, grow and earn returns for investors are huge for any business, but decision-makers must keep their perspective on the market they serve and the problems they solve best. If expanded offerings and partnerships with other service providers enhance your brand and what it stands for, then this approach makes sense for growth and customer satisfaction. If not, then serving up the best grilled cheese sandwiches around, to the folks who really crave them, may well be the best path.

New SoFi Stadium To Host Rams, Chargers, Super Bowl & Olympics

September 15, 2019 SoFi’s appetite to reach NFL viewers is going above and beyond just Super Bowl commercials. The fintech company that started with student loan refinancing, has secured the naming rights to a new professional football stadium in Inglewood, California. SoFi Stadium, which opens in 2020, will host both the Rams and the Chargers. The stadium will also be home to Super Bowl 56 in 2022 and will serve as the venue for the opening and closing ceremony of the 2028 Summer Olympics.

SoFi’s appetite to reach NFL viewers is going above and beyond just Super Bowl commercials. The fintech company that started with student loan refinancing, has secured the naming rights to a new professional football stadium in Inglewood, California. SoFi Stadium, which opens in 2020, will host both the Rams and the Chargers. The stadium will also be home to Super Bowl 56 in 2022 and will serve as the venue for the opening and closing ceremony of the 2028 Summer Olympics.

Anthony Noto, SoFi’s CEO, served as CFO of the NFL for almost 3 years from 2008 – 2010.

In an interview with CNBC, Noto explained that the naming rights are more than just people coming to a game and seeing their brand there and that it will also give them a TV broadcast platform for all types of events the stadium hosts. It’s the ultimate advertising campaign, which the company believes they need to market their new products such as SoFi Money.

“Now that we have a complete suite of financial services […] we have to build awareness of those products, which requires us also to build trust, so being part of this iconic destination, allows us to elevate and accelerate how quickly we can get there,” Noto said.

The move could be perceived as too flashy or premature given how young and new SoFi is, but Noto says that the naming rights only make up about 10% of their marketing budget.

A single night of football, they estimate, would put them in front of 10-15 million unique potential customers, equal to all of their other total sponsorships they’ve done combined.

LA Rams Chief Operating Officer Kevin Demoff said during a separate CNBC interview, “I think when you look at someone like Anthony Noto, who was in part of the NFL, who understands the allure of football and what it brings to people on sundays, and throughout the nation and helps bring people together, but also right there the entertainment factor when you think about what can happen, on this field right below, I think it’s something that gives everybody a point of pride.”

PNC Bank Launches Fintech Startup numo

September 3, 2019 Last week, PNC Bank announced its latest venture, numo, which aims to function as an internal startup, developing apps and other services to expand PNC’s operations.

Last week, PNC Bank announced its latest venture, numo, which aims to function as an internal startup, developing apps and other services to expand PNC’s operations.

The first such app is indi, a bank account for gig workers that is exclusive to mobile phones. Offering customers tax calculators, tax savings goals, and dynamics adjustments that react to how much they’ve saved, PNC is joining the list of financial institutions which are doubling down on banking apps. The numo accounts are FDIC-insured, are held at PNC, and include a Visa prepaid debit card.

Speaking on the benefits of indi, numo CEO David Passavant said, “How do you estimate your tax liability when you don’t have an employer doing it for you? We built a system with intelligence to estimate what you should set aside for taxes.”

Beyond indi, numo has two other projects in the pipeline. One of these is unknown as of yet, but the next to be launched will be a service for companies that run portfolios of retail properties.

Not the only announcement to come from PNC last week, the bank also revealed its partnership with the RippleNet blockchain network. Joining together to offer swift cross-border payments for PNC’s commercial clients, the news comes almost a year after the bank stated that it planned to partner with RippleNet in September 2018.

“The speed of doing business continues to accelerate,” explained PNC Treasury Management Executive Vice President and Head of Product Chris Ward in 2018. “And the efficiencies of RTP [real-time payments] allow our clients to not only keep pace, but stay ahead.”

Apple Card Partnership Sees Goldman Sachs Lending to Subprime Borrowers

August 25, 2019 Apple Card launched this month, and with it have come some complaints over the unforeseen damage that wallets can do as well as an official guide from Apple on how to tend to and clean your new credit card. But aside from aesthetic and hygienic concerns, the card’s release to the wider public has raised eyebrows with news of subprime borrowers being approved.

Apple Card launched this month, and with it have come some complaints over the unforeseen damage that wallets can do as well as an official guide from Apple on how to tend to and clean your new credit card. But aside from aesthetic and hygienic concerns, the card’s release to the wider public has raised eyebrows with news of subprime borrowers being approved.

Forged from a partnership between Apple and Goldman Sachs, a bank known for dealing with corporations and the rich, the move seems out of character for the 150-year-old institution.

Rolled out initially to Apple employees as a test, rumors began to circulate of early adopters expressing surprise at being approved despite having FICO scores in the middling 600s. Then, upon Apple Card’s wider release, Ed Oswald came forward and spoke to CNBC about receiving his card, along with a credit limit of $750 and an interest rate of 23.99%, despite having a credit score of around 620.

But this is not the bank’s first foray into FICO’s less than 700. Since its launch, Goldman’s Marcus has issued $4.75 billion in personal loans, 13% of these going to borrowers with a FICO of 660 and under.

This 13% and the partnership with Apple are indicative of David Solomon’s tenure as CEO of Goldman Sachs, who has sought to expand into consumer finance following years of declining trade revenues.

And while this contrasts the bank’s history, the push for more access to credit is aligned with Apple’s values. In fact, in the 1990s, when the tech company was in talks with Capital One over a potential card partnership, Steve Jobs “had an aversion” to rejecting any customers who wanted to sign up. Such yearning for openness and ease of access has reportedly scared off other banks. According to CNBC, Citigroup was in advanced talks with Apple prior to Goldman Sachs’s confirmation, but pulled out of the deal due to concerns over the profitability of the partnership. Similarly, JPMorgan Chase, Barclays, and Synchrony all allegedly bid on the deal.

But what does such access mean? Well opening up credit to those with a less-than-proven track record increases the risk of losses due to unpaid loans. The speed with which funds are made available, the application and approval process takes two minutes, means that Apple Card could rival payday loans and alternative finance for those customers looking for more modest funding. And as well, the commodification and attention paid to the appearance of the card by Apple has led to it being viewed as the latest gadget from the company rather than a tool to use when financially necessary, as pointed out by Macworld, raising questions over how credit cards should be marketed.

On the topic of access, Ian Kar, the author of the Fintech Today newsletter said that “Apple is only making one card, so they have to target everyone … It’s not like they’re Chase with multiple cards like Sapphire Reserve to target a higher demographic and other cards for lower segments.”

This singular approach to credit joins Apple’s growing collection of services. Likely being pushed to account for the falling sales of the iPhone, Apple Card is the latest in a line of launches that includes Apple News+, Apple TV+, Apple Pay, and Apple Arcade.

This year, iPhone sales saw a drop of 12%, making up 48% of total Apple sales. While Apple services rose by 13% from 2018 to become the second largest segment of the company’s sales portfolio, being 21%.

When discussing Apple Card and its role in the bank’s ecosystem in an internal Goldman Sachs memo, Solomon, hinting at further partnerships, said “Apple Card is big, but it’s also a beginning.”