Business Lending

OppFi: ‘Bitty is a Great Partner’

October 29, 2025Bitty generated $1.4 million in equity income for OppFi in Q3. OppFi, publicly traded, owns a 35% stake in Bitty.

“Bitty is a great partner that we have enjoyed working with and learning from in the SMB space,” said OppFi CEO Todd Schwartz during the company’s Q3 earnings call. “The company shares OppFi’s business principles and corporate values and consistently uses technology to enhance operations and the customer experience. Bitty has identified significant additional growth opportunities and continues to capitalize on the ongoing supply-demand imbalance in the small business revenue-based finance space.”

Overall, OppFi said it had delivered another strong quarter that had outperformed expectations. It raised earnings guidance for the third time this year.

‘Like Family’: How Critical Financing Became One of the Fastest Growing ISOs

October 17, 2025When Farmingdale, Long Island-based Critical Financing (CFI) showed up as the 2,671st fastest growing company on the Inc. 5000 list this year, it was a testament to the company’s many years of hard work. Founded in 2017 by its CEO Brandon Garcia, CFI connects small businesses with a variety of unsecured working capital products.

“[Getting that recognition] was great,” said Garcia. “And I think it’s also a testament to the group that we have. It excites the people that work here too. This is a very stressful job, it’s not easy.”

In CFI’s day-to-day, the sales team finds itself competing against multiple companies on almost every deal that comes across their desks. Small businesses regularly put the pressure on them to get the best rate, the fastest funding, or a combination of both. They say this only increases their drive.

“It has definitely helped us in a way,” Garcia said of it. “I mean who doesn’t want a deal that doesn’t have competition, you can kind of take your time with it, right? But I think when there’s urgency, our guys perform better.”

In the very beginning it was just Garcia himself who had worked in the industry since 2012. He was soon after joined by a former colleague, Robert Menzel, and the two set off to really build up a company. That’s easier said than done, especially in a business where trust is paramount. So they looked within their own circle of friends and family to create a solid foundation.

“I felt it was best that we take care of our own,” Garcia said. “Let’s take care of people that we know that are looking for a new opportunity, and we train them the way that we want them to be trained. We want to give that experience and push it over to them.”

Among those they’ve brought on board to their current headcount of sixteen has been Garcia’s own mother, who works as the company’s head processor. And while they are still actively looking to bring on more people, Garcia said that the number of employees isn’t the ultimate metric of success, but rather the abilities of the ones you do have and the relationships they have with everyone else is the key. On this point, CFI is on pace to surpass $100 million in funding this year. It’s because of their continuous progress and results that they finally got the confidence to apply into the Inc. 5000 and were successful in making it.

“To be able to put that Inc. 5000 sticker in your signature, on the website, it just has a different swag to it,” said Garcia’s partner Menzel, “where it just carries a lot of weight, and even the merchants see that.”

When asked if the end goal was to become a lender themselves, both Menzel and Garcia say they’re happy with what they already do now, which is connect the merchants to the most appropriate source.

“While many competitors chase the close, we lead with transparency and real strategy,” Garcia said. “We act as consultants first. Even if a client doesn’t move forward with us, we want them to walk away smarter and more prepared than when they came in.”

“When you are a lender, you don’t really have that close relationship with other lenders because you’re your own lender,” Menzel said. “You’re not talking to them about deals, how to get deals done, ‘what are they doing? What did they change this month compared to what they’ve been doing, what’s working, what’s not.’ I think having those relationships with the lenders and the lenders’ reps, it’s huge and it makes the job fun, because they’re really all great people that we deal with.”

That closeness is what it’s all about for them.

“We are a group of people who genuinely care about each other,” Garcia said. “We’ve celebrated marriages and welcomed new babies. We hang out on weekends, show up for one another, and create a work environment that doesn’t feel transactional.”

The outcome of that are months where the company is exceeding $10 million a month in funding, and they’re now even more fired up after the Inc. 5000 placement.

“You don’t need this massive shop to be successful in this industry,” Garcia reiterated. “It’s really that simple. You just need the right people. You need to be loyal and just really be truthful with everyone. And good things happen. That’s a big thing for us.”

That Fintech Business Loan Performance Should Help You: How Hansa is Giving Both Borrowers and Lenders a Powerful Tool

October 15, 2025“Business owners want to be reported on,” said Henry Magun, founder and CEO of Hansa. “When we do a lot of surveys around this and when we survey small business owners en masse, would they rather borrow from a provider that does report to the business credit bureaus or does not, 85% of business owners say that they would rather borrow from a provider that does report to the business credit bureaus.”

It’s a familiar story: small business borrows from a fintech lender, repays it perfectly, and later on down the road applies for financing elsewhere believing that their previous payment history will support an approval or more favorable terms, only to find out there’s no public record of it at all.

“We hear that all too often,” said Magun. “It’s a very common experience, and that is one of the reasons why we are extremely focused on not only building the back-end pipes to do the furnishment to the bureaus for the lenders and make that process effortless, but also creating a front-end product that makes it a transparent process for the SMBs.”

Hansa, headquartered in New York City, enables lenders to report payment history to the credit bureaus and access existing reports on their customers. The key here is that it’s business credit reporting, not personal. Although most people are familiar with Dun & Bradstreet, Experian and Equifax also have business bureaus specifically for business credit. There’s also consortium-based organizations such as the Small Business Finance Exchange, for example, that take in commercial credit data.

While term loans and cards for SMBs, two rapidly growing products in the fintech space, are their main focus, the Hansa platform can make reporting possible for just about anything.

“We realize that there is such a diversity of product-type in the SMB financing space,” Magun said. “Is it a term loan? Is it a card? Is it an MCA product? You know, are there daily payments, weekly payments, monthly payments? All across the board, we do it all.”

The benefits of reporting business credit are obvious. Lenders can claim that good performance will legitimately build business credit, borrowers benefit from actually building business credit, and lenders can rely on this highly relevant data to drive more informed decisions.

“It’s really about getting the fintech ecosystem towards the future in which companies are focused on supporting financial wellness, and we really view credit furnishment in the SMB space as core to that, ultimately being able to reliably build credit is extremely important for financial mobility, economic mobility because it enables people to [graduate] to bank products and things like that, and being able to take your history with you in order to progress. That’s really important for economic mobility.”

On the flipside, for lenders that have spent years fine-tuning algorithms to predict payment performance outside of traditional credit reports, one area that continues to remain cloaked in obscurity is payment performance with other fintech lenders. Alternative methods, at least within the fintech community, are commonly used to make a best-guess effort, such as employing automated tools to scan an applicant’s bank account deposits with a known list of lender names and then matching them to corresponding bank debits to predict the performance and status of those accounts. But even if one can assess with a high degree of confidence about how those credit lines are performing, it’s not exactly an official affirmation from the lender, and the transaction history might not go far back enough. Besides, these risk assessment methods are entirely personalized to the lender, and don’t necessarily give the business an asset (a universally recognized credit report), that it can furnish elsewhere and benefit from. A business could use a credit report for a trade line or a bank loan or in some other transaction where it could hold weight for them, for example.

On the flipside, for lenders that have spent years fine-tuning algorithms to predict payment performance outside of traditional credit reports, one area that continues to remain cloaked in obscurity is payment performance with other fintech lenders. Alternative methods, at least within the fintech community, are commonly used to make a best-guess effort, such as employing automated tools to scan an applicant’s bank account deposits with a known list of lender names and then matching them to corresponding bank debits to predict the performance and status of those accounts. But even if one can assess with a high degree of confidence about how those credit lines are performing, it’s not exactly an official affirmation from the lender, and the transaction history might not go far back enough. Besides, these risk assessment methods are entirely personalized to the lender, and don’t necessarily give the business an asset (a universally recognized credit report), that it can furnish elsewhere and benefit from. A business could use a credit report for a trade line or a bank loan or in some other transaction where it could hold weight for them, for example.

“It really is a ‘rising tide raises all ships’ scenario in the sense that in a more mature ecosystem where there’s higher ubiquity of reporting, everyone benefits,” Magun said. “It helps all the funders and creditors on their underwriting processes, and it helps the business owners, the applicants, because it increases the portability of your credit history.”

The usefulness speaks for itself. Hansa, for example, has increased the number of reports that they’re furnishing data on by more than 400x since the beginning of this year. And the lenders can show off to their borrowers what they’re reporting and where it’s being reported to in any manner they wish.

“We’ve started to see really great traction amongst these various players, and we’re really excited to be working with them and it works,” said Magun.

Already they are seeing improved payment rates and increased engagement rates between the borrowers and lenders.

“It’s really powerful,” Magun said, “and SMBs really do care about being able to build their credit.”

How Kaaj is Accelerating Small Business Lending

October 8, 2025Utsav Shah first met Kristen Castell at deBanked CONNECT MIAMI this past February. At the time, Shah and his partner Shivi Sharma were freshly promoting a new AI technology to simplify small business lending. It’s called Kaaj, described as a core intelligence layer that bolts into a lender or broker’s CRM and handles all of the early-stage application intake and underwriting work. Shah had been familiar with the fintech accelerator Castell directs, the Center for Advancing Financial Equity (CAFE), which she was speaking about at the conference, but he had never actually met her in person until then.

“That’s really when we learned deeply about what CAFE’s mission is and how it works with a lot of startups, a very unique mission and very unique approach to work with startups and bring the ecosystem together,” said Sharma. “So we loved it and decided to apply this Fall.”

They applied into the exclusive accelerator program and were one of six companies to be selected, an honor considering hundreds of companies apply for entry on a bi-annual basis. As previously noted on deBanked, it’s an eight-week program, some of which takes place on location at the Fintech Innovation Hub on the University of Delaware campus. The rest is virtual but there are in-person field trips like a recent one to Washington DC, for example. deBanked has sponsored the last three accelerator cohorts which in the most recent cohort includes headline names like JPMorgan, PNC, Discover, Barclays, Capital One, M&T Bank, WSFS BANK, BNY Mellon, Prudential, Fulton Bank, County Bank, Best Egg, United Way, NeighborGood Partners, and the Delaware Bankers Association.

Kaaj, based in San Francisco, was already getting noticed beforehand. The company won the Fintech Meetup Startup Pitch Competition in March and secured a $50,000 prize, for example. Their technology is especially suited for equipment financing companies, MCA providers, small business lenders, SBA lenders, factors, and more.

Kaaj, based in San Francisco, was already getting noticed beforehand. The company won the Fintech Meetup Startup Pitch Competition in March and secured a $50,000 prize, for example. Their technology is especially suited for equipment financing companies, MCA providers, small business lenders, SBA lenders, factors, and more.

“So imagine that you’re a lender, and you get hundreds of applications in a day, and you don’t really know where you want to focus your time on,” Shah said to deBanked. “‘What do these 100 deals mean for me, for my business? Are they even qualifying against my criteria, etc.’ So what Kaaj does, it provides very quick intelligence, within the first three minutes.”

Shah explained that as soon as someone submits a package with documents, they get analyzed from top to bottom, like KYC/KYB, the bank statements, and more. This helps lenders (and brokers) decide how to prioritize their time. Utsav’s background in technology has played a major role in building this out as he comes with a decade of AI experience and was building autonomous cars before building Kaaj.

“Time wins deals or time kills deals,” said Shah. “Either way that you want to look at it, if we can give that time back to them, if we can reduce that turnaround time on each individual deal and focus on those higher profitability deals for these companies or these lenders, then they can start really feeding the top line and the bottom line, because they’re not having to hire a bunch of folks.”

Sharma said that equipment finance is slightly more complex than MCA, for example, but that as a $1.4 trillion industry, it’s a market that’s ripe for innovation. Sharma used to work in commercial lending herself and has seen firsthand how manual processes and outdated technology slow things down and hurt not only the lenders but the borrowers in the process.

“I have worked on small business lending, commercial lending, payments fraud, onboarding fraud, a lot of that,” Sharma said. “I spotted a lot of challenges in that space and a clear lack of good technological solutions that really help these lenders scale efficiently.”

Shah, meanwhile, said that ultimately it’s about helping the end-user, the business borrower.

“We are very focused on solving for small businesses, because the final mission of the company is to get better access to capital for small businesses,” he said.

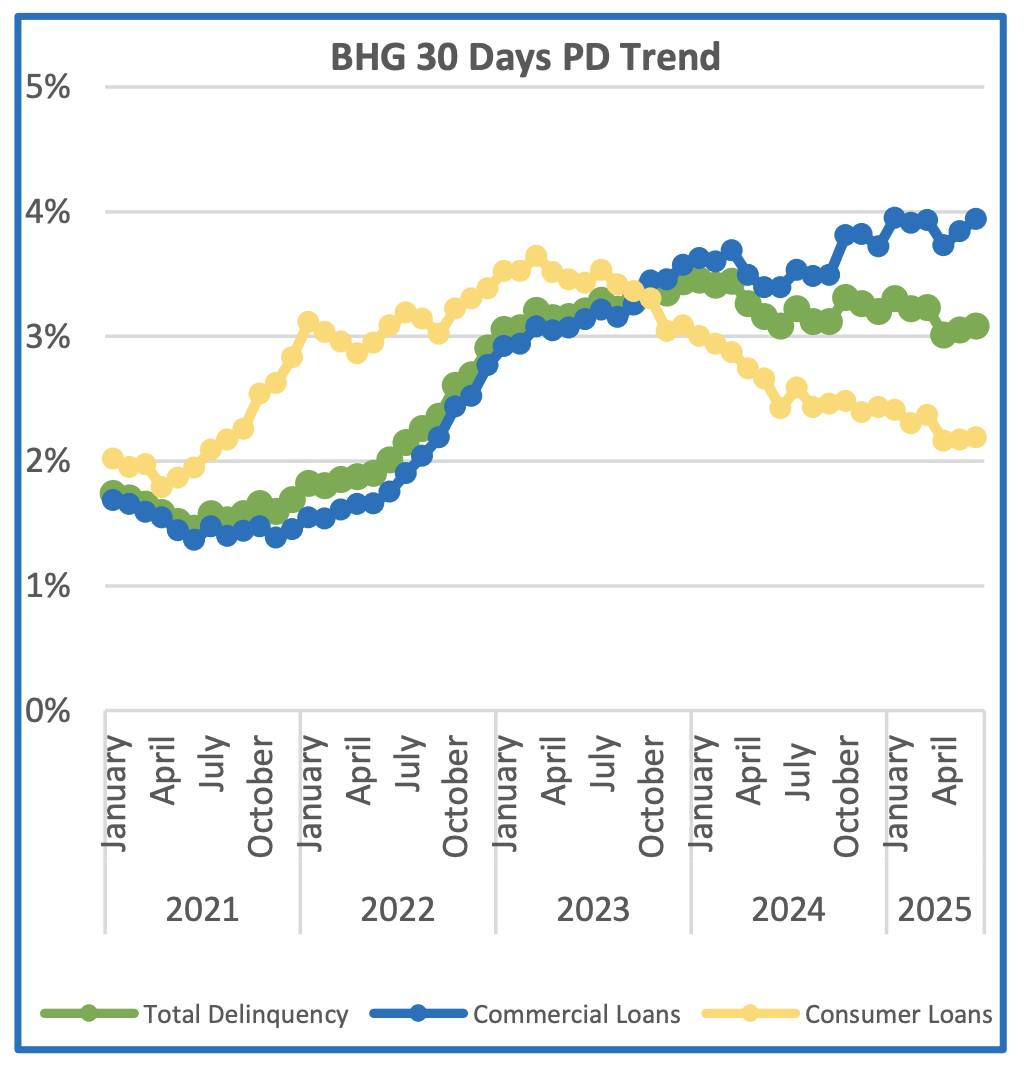

BHG Financial Had a Strong Second Quarter

August 22, 2025 BHG Financial had loan originations of $1.5B in the 2nd quarter of 2025, up from 1.2B YoY. The company is 49% owned by Pinnacle Bank.

BHG Financial had loan originations of $1.5B in the 2nd quarter of 2025, up from 1.2B YoY. The company is 49% owned by Pinnacle Bank.

The company’s trending 30-day commercial past-due rate has been hovering at around 4% since the same time last year while past-due rates on their consumer loans have been in a consistent decline since Summer 2023.

During the Q2 earnings call, Pinnacle CFO Harold Carpenter, said that both production and credit growth have been good this year.

“I think credit has really been the bigger surprise for the year,” said Carpenter, “and we feel like that it looks like it’s pivoted and hopefully, it will continue to pivot.”

BHG primarily serves as a full-service commercial loan provider to healthcare providers and other skilled professionals for business purposes but also makes consumer loans for various purposes.

Business Finance Brokers in 2025

August 15, 2025

We’re now ten years out from the original “Year of the Broker” article in deBanked Magazine. Brokers are still here, the business has just changed slightly. Here’s some of the top line differences vs. 2015:

Cold Calling: 12% of merchants say they started their search for business funding options from a cold call.

Google Search: Organic search rankings beginning to diminish in favor of AI Q&As.

Training: AI can now listen to every call and grade you on every component of it.

CRMs: Pen and paper are over. Every touch on a deal should be traced and automated and deal tracking organized in a system.

Competition: Every POS solution and merchant fintech software now has a funding button embedded into it.

Commissions: Still high.

Funding Options: Lines of credit, term loans, MCAs, SBA, equipment financing, real estate lending, and more.

Regulations: There are now numerous state registration and disclosure requirements. (See the map here).

Leads: Referral networks are now more valuable than ever. Referrals from CPAs, lawyers, trade associations, chambers of commerce, and more.

Gates: You may have to go through a super broker to get access to a top tier funder.

Startup Costs: The registration requirements in several states has significantly increased the cost of starting a new broker shop today.

Business Finance Companies on Inc 5000 List in 2025

August 12, 2025Here’s where small business finance companies rank on the Inc 5000 list for 2025 (and if we’ve missed you, email info@debanked.com):

| Ranking | Company | 3-Year % Growth |

| 15 | Parafin | 9594 |

| 206 | businessloans.com | 1862 |

| 669 | Pinnacle Funding | 626 |

| 831 | SBG Funding | 508 |

| 1215 | Essential Funding Group | 359 |

| 1240 | Clara Capital | 352 |

| 1417 | Backd | 306 |

| 1705 | Kapitus | 256 |

| 1719 | Channel | 255 |

| 1756 | Fundible | 248 |

| 2027 | 4 Pillar Funding | 214 |

| 2117 | Biz2Credit | 203 |

| 2293 | Byzfunder | 187 |

| 2671 | Critical Financing | 156 |

| 3081 | Lendzi | 131 |

| 3226 | eCapital | 124 |

| 3508 | ApplePie Capital | 111 |

| 3545 | SellersFi | 109 |

| 3901 | Splash Advance | 95 |

| 3973 | Fora Financial | 92 |

| 3993 | Capital Infusion | 91 |

| 4076 | Expansion Capital Group | 88 |

| 4162 | Shore Funding Solutions | 85 |

| 4206 | Direct Funding Now | 83 |

| 4712 | ROK Financial | 63 |

Square Loans Originates $1.64B in Small Business Loans in Q2

August 8, 2025Block’s merchant financing division, Square Loans, continues to lead the competition. The company originated $1.64B in small business loans in Q2, up slightly from $1.59B in Q1. That puts them on pace for $6.5B for the year and allow them to maintain their top position among small business finance companies that deBanked tracks. Square Loans’ advantage is that its customers repay their loans automatically through their daily Square POS transactions.

Overall, Block CEO Jack Dorsey announced that the entire company is “Back on offense.”

“We had a strong second quarter,” wrote Dorsey in his shareholder letter. “Square GPV grew 10% year over year and Cash App gross profit grew 16% year over year, accelerating as we exited Q2.”