Business Lending

Square Loans Originated $594M in Business Funding in Q3

November 5, 2021 Square Loans, formerly known as Square Capital, originated $594M in small business funding in Q3, bringing the company to $1.6B originated YTD. Square had already been recognized among the largest small business lenders this year so far.

Square Loans, formerly known as Square Capital, originated $594M in small business funding in Q3, bringing the company to $1.6B originated YTD. Square had already been recognized among the largest small business lenders this year so far.

The Q3 figure boils down to 83,000 individual loans.

Overall, Square Loans was mentioned very little in the company’s quarterly earnings call. Company CEO Jack Dorsey said “…there’s still a lot of opportunity for us to open more of our products in more of the markets that we’re already in, such as Square Loans in more of the places that we already exist.”

The coming of Hyperinflation, a prediction made by Dorsey on Twitter just weeks prior, went completely unmentioned in Square’s official reports.

On October 22, he tweeted, “Hyperinflation is going to change everything. It’s happening.”

Mississippi Fintech is Innovating Small Business Lending with Brokers in Mind

November 3, 2021

Vergent, a loan management software, is creating a space where brokers and lenders alike can manage all aspects of a deal in one place. Based in Ridgefield, Mississippi, Vergent is trying to innovate the industry with brokers in mind, pairing the small town values of interpersonal engagement and getting to know your customer with the big city ideas of fintech and automation.

“Really what we provide is the technology infrastructure for lenders to reach their end user,” said Bradley Tompkins, Chief Information Officer at Vergent. “Whether that be a small business looking for a loan, we facilitate that acquisition, the origination of that loan, and the servicing of that loan. That could mean recurring payment setups, based upon the lender’s requirements, communication with that customer via email, text, however that is facilitated, and all the different payment options.”

Tompkins talked about how his software is one of the few that brokers in his area are already utilizing to start making deals smoother. With access to all aspects of the deal, Vergent provides an all-in-one suite of options that can turn the process of analyzing a deal or checking out a deal post-funding into a couple of clicks.

“We actually have brokers who use our software to accept applications, originate loans, and then we can either transfer that to a separate portfolio that the lender then manages for servicing, or sometimes we have brokers that service the loans themselves,” Tompkins said. “So there are really a lot of options on how to set that up in the platform, so the lender can have a separate site where they accept applications from multiple brokers, or really any combination of those things.”

The value of a direct relationship with the customer is top-tier according to Tompkins, as he spoke about the next great innovations in fintech not being how to weed the human interaction out, but finding its role that will find the balance between human touch and AI power. “Once you know your customer, you can give them the option to pay you back in the easiest way possible. Understanding how they get paid, their pay cycles, when they have money and being flexible to accept that money when they have it, and giving them those repayment options is the next great innovation.”

When talking about the ability to market his product to a wide audience, Tompkins acknowledged the difficulty due to the size of the industry itself, but touched on the value of networking events like Money 20/20, where Tompkins was pitching Vergent to an international audience.

“We’ve been pleasantly surprised by the amount of lenders we’ve seen, and the amount of opportunities that have come our way from [Money 20/20]. We came here pretty open minded, maybe talk to some payment processors and other vendors that may be able to integrate to us and kind of help expand our network, but really it’s just getting our name out, seeing a little bit of a different segment than what we normally see, and looking at other market opportunities.”

Appalachian Crowdfunder Gives Take on Business Lending

November 2, 2021 View from outside of Pittsburgh, PA

View from outside of Pittsburgh, PAGeorge Cook, whose family has been running a small community bank in rural Appalachia for over 130 years, has grown up in a world surrounded by banking in some of the most rural parts of America. Now the CEO of Honeycomb Credit, Cook has taken to a crowdfunding platform to start lending to businesses in his area. Cook shared his thoughts with deBanked about the state of lending, and how his product competes with ones already available on the lending market.

Cook spoke about how when he growing up, he always had a fascination with the relationship between the consumer and their banks combined with the difficulties for those consumers to get access to capital. “I spent a lot of time thinking about community banking, especially local capital,” said Cook.

When discussing competing products in the lending space, Cook thinks that his product will innovate his area with a style of lending that benefits both the borrower and investor. It appears that he thinks products like MCAs have become partially antiquated.

“I think the downside of [MCA] is inherently when your value proposition is fast money, you’re going to have a negative selection,” said Cook, when asked about fintech’s role in innovating small business lending. “You’re going to have a lot of desperate businesses who need money fast, which means you inherently have to charge a high interest rate and that has [deterred] a lot of business owners.”

George Cook, CEO, Honeycomb Credit

George Cook, CEO, Honeycomb CreditCook referenced how the complexity of some MCA deals prevent small businesses from using them. “We talk to a lot of business owners who really don’t understand what a merchant cash advance is, they get caught in a debt trap, and it’s not a good situation. For me, I think the next evolution is, not saying merchant cash advances are going away, but I think they’ve been over extended. I think they’ve been overapplied in places where they don’t make sense.”

Cook hinted at new fintech loan products that have elements of MCA popping up in the lending world, as fintech innovates the industry.

“I think now we’re going to see the fintech space start to right the issue, come up with other capital solutions that make sense for small businesses for longer term capital. I think we’re going to see a lot of term loan products that act with different data and different attributes coming to bear, [thus] being able to bank these businesses.”

After working in fintech building big data credit analytics products prior to starting Honeycomb, Cook claims he saw a major issue with small businesses having access to capital long ago. He saw that the qualifications needed for business loans were the same as ones needed for consumer loans, and many small businesses just didn’t qualify for the capital they needed.

“[The system] didn’t work as well for small business lending because you know, small businesses don’t have as much operating history, they don’t have clean data sets, they’re not keeping their books really well, there’s not really a good data aggregator of small business data.”

Cook continued to speak about the issues with banks evaluating a small businesses’ credit and how this was causing a low approval rating. “A coffee shop looks a lot different than a fitness studio and those look a lot different than a manufacturing plant,” he said. “We were actually seeing a really large decrease in small business lending across the country.”

According to Cook, his company allows investors to take their money and put it right back into the community. He also claims that each one of his customers can expect returns ranging from six to twelve percent on an investment.

Honeycomb makes money on success fees, which are the closing costs on the loan. There’s also an investor fee to get a foot in the door.

“One of the things we’ve found is whenever you have retail investors, you have local people in the community voting with their wallets on these small business loans,” said Cook. “So we’re able to do small business loans in a way that no one else has been able to.”

OnDeck originated $462M in Small Business Loans in Q3

October 28, 2021 Enova, through OnDeck, originated $462M in small business loans in Q3, according to the company’s earnings call. That was up from $400M the quarter before.

Enova, through OnDeck, originated $462M in small business loans in Q3, according to the company’s earnings call. That was up from $400M the quarter before.

“…as we’ve been predicting, small businesses have been beneficiaries of the pent-up consumer demand and the resulting increased spending,” said Enova CEO David Fisher.

Fisher also touched upon the CFPB regulatory inquiry disclosed in the earnings release, downplaying it somewhat as “routine.”

“I want to touch on the CID that we announced in our press release,” he said. “The CFPB is investigating a handful of issues several which were self reported by Enova. We have been cooperating fully with the CFPB as we always do. This is a routine process with the CFPB, particularly in our industry. We’ve been through it with them in the past. As a result, we anticipate being able to work with the CFPB to expeditiously complete this investigation.”

This story has been updated to fix typos

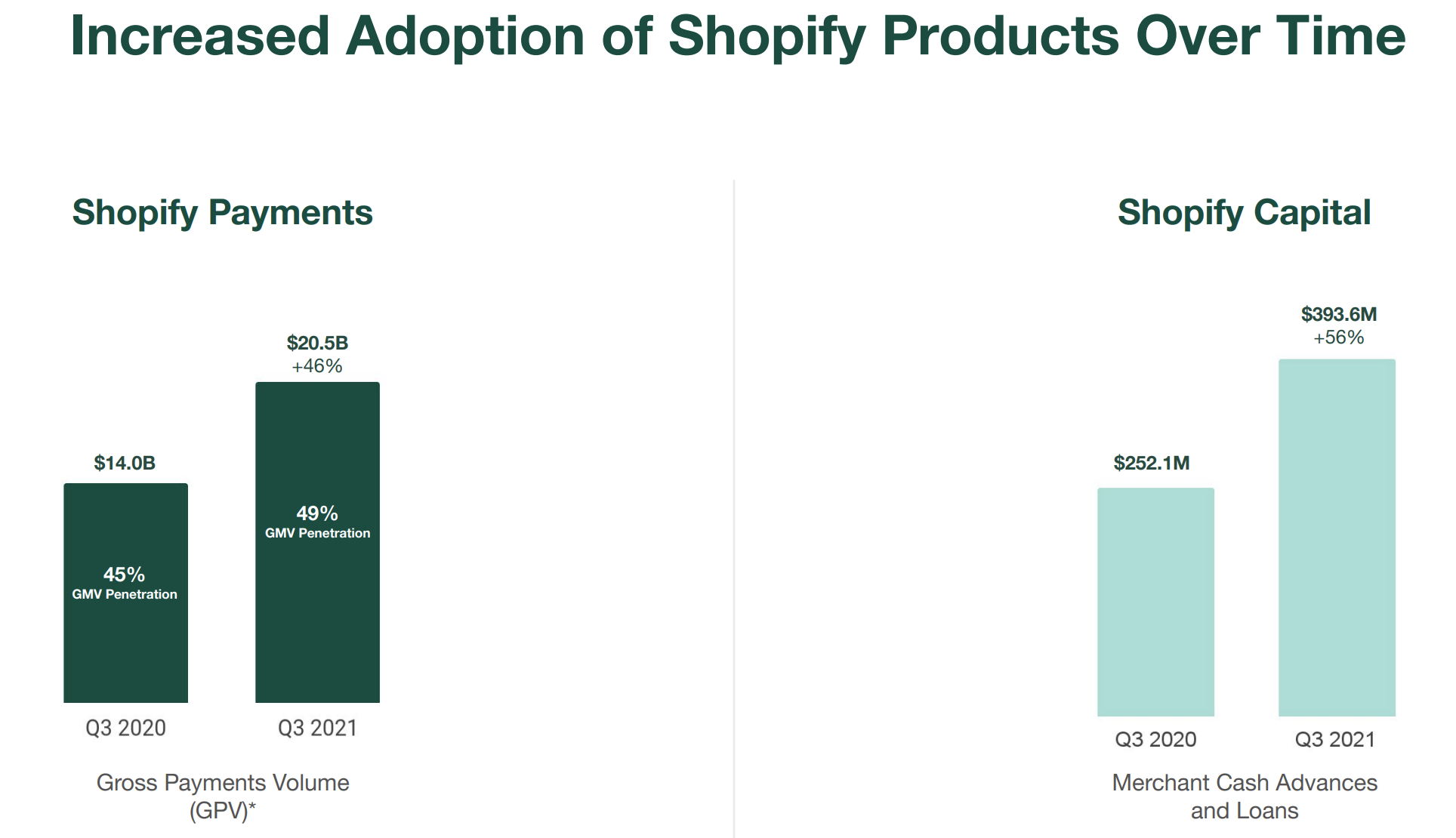

Shopify Capital Originated $393.6M in MCAs and Business Loans in Q3

October 28, 2021Shopify Capital, the funding arm of e-commerce giant Shopify, originated $393.6M in merchant cash advances and business loans in Q3, the company reported. That’s up from the $363M in the previous quarter.

Covid was a boon to Shopify Capital given its dependence on e-commerce businesses. Its 2020 funding volume was almost double that of 2019.

“Shopify Capital has grown to approximately $2.7 billion in cumulative capital funded since its launch in April 2016,” the company announced. The large volume and continued success has landed the Shopify Capital division in the company’s “core” bucket of “near-term initiatives” that will build the company for the long term, according to a presentation accompanying Q3 earnings.

Slava Rubin, Founder of Indiegogo, to Keynote Broker Fair 2021

October 22, 2021 Broker Fair announced that Slava Rubin will be its keynote speaker for its 2021 conference on December 6th in New York City.

Broker Fair announced that Slava Rubin will be its keynote speaker for its 2021 conference on December 6th in New York City.

REGISTER HERE FOR BROKER FAIR 2021

Who is Slava Rubin?

Slava Rubin is an entrepreneur and innovator in the fintech space for nearly 20 years. Slava built an alternative investment platform, a venture fund, an equity crowdfunding platform, a perks crowdfunding platform, and an angel investment portfolio. Slava is a founder of Vincent, a company which has developed the largest database of alternative investments (crypto to NFTs, trading cards to art, real estate to venture and debt) and is changing how people access them. He is also founder & managing partner at humbition, a $30M early-stage operators venture fund built by founders, for founders. Slava also founded Indiegogo, a company dedicated to empowering people from all over the world to make their ideas a reality. As CEO for over 10 years from inception in 2006, Slava grew Indiegogo from an idea to over 500,000 campaigns and more than $1B distributed around the world. While at Indiegogo, Slava launched one of the nation’s first equity crowdfunding businesses. Slava’s angel portfolio includes 4 unicorns – Carta, Hedera, GOAT, & Turo. He is also a founding advisor to multiple companies including Hedera Hashgraph – a top 60 blockchain protocol.

Prior to Indiegogo, Slava was a strategy consultant working on behalf of clients such as MasterCard, Goldman Sachs and FedEx. He is also the founder of “Music Against Myeloma,” a charity that raises funds and awareness for cancer research in partnership with the International Myeloma Foundation. Slava is currently a member of the board for NYSE traded (WSO) Watsco Inc., and privately held, Indiegogo.

Slava represented the crowdfunding industry at the White House during the signing of the JOBS Act under the Obama administration and has helped navigate bringing equity crowdfunding to the American public. He also pioneered security tokens in the United States – having been a catalyst for selling fractionalized ownership of the St. Regis hotel in Aspen using blockchain technology. He has made many TV appearances including being a regular guest commentator on CNBC. He has also been often quoted in NYTimes and Wall Street Journal.

Slava has received numerous awards including Fortune 40 under 40, Observer 20 Heros under 40, and the Wharton Young Leadership award for 2015.

Slava holds a B.S.E. from the Wharton School of Business

SBA Task Force Set to Begin Campaign

October 19, 2021 In response to an unprecedented economic situation, a mixed group of regulators, bankers, small business owners, funders, attorneys, and social media representatives are coming together in a task force to work with the SBA, members of Congress, small businesses and entrepreneurs to transition small business into a “new phase.”

In response to an unprecedented economic situation, a mixed group of regulators, bankers, small business owners, funders, attorneys, and social media representatives are coming together in a task force to work with the SBA, members of Congress, small businesses and entrepreneurs to transition small business into a “new phase.”

Dubbed the SBA Task Force at last week’s Bipartisan Committee summit on small business recovery, the group’s goals are to address the state of small business in the U.S., how the current economical and political climate is impacting the practices of merchants across the country, and to address concerns from interested parties directly to the federal government.

“The SBA is at a crucial moment: its laudable performance during the COVID crisis has thrust upon the agency new expectations and new responsibilities,” said Pradeep Belur, former COO of the SBA and co-chair of the committee. “To fulfill those, [the] SBA needs not only enhanced capacity but also modernization to enable it to execute effectively. I’m honored to help chair this task force and pursue measures that will support the agency and help the heart of America’s economy.”

Alongside Belur as co-chair of the committee is Ann Marie Mehlum, a Senior Advisor at FS Vector with almost four decades of experience in banking. Much like Belur, Mehlum is committed to continue the largely unfinished project of improving the operating conditions for small businesses.

“The work of assisting small businesses is never finished—the SBA has continually sought to respond to new needs and reach more types of small companies,” Mehlum said. “The members of this task force, which I’m delighted to help chair, are committed to working with the agency and Congress to improve the ways in which that work is carried out.”

The founder of the committee, Angela McIver, is the owner of an after-school math program for children based in Philadelphia. When faced with pandemic related troubles, McIver pivoted her business from a brick and mortar learning program into a fully virtual, nation-wide learning platform.

“One of the smartest things I did was develop a relationship with a community bank” said McIver, when asked what advice she would give to small businesses at the BPC’s summit. “We didn’t have a lot of the challenges that small businesses had because we had a relationship with a small bank that knew who we were, knew our challenges, and [they] were able to step in when it was necessary.”

Other members of note on the force are Christopher R. Upperman, a Manager & Team Lead in the Governance Organization at Facebook, Jessica Johnson-Cope, President, Johnson Security Bureau and co-chair of the 10,000 Small Businesses Voices National Leadership Council, and Ryan Metcalf, Head of U.S. Public Policy and Global Social Impact at Funding Circle.

“Our participation in the BPC’s task force reflects our ongoing commitment to advocate for government policies that are in the best interest of small business owners” said Metcalf, exclusively to deBanked. “We truly believe that the strongest path forward for the SBA involves leveraging the proven capabilities of fintechs to quickly and efficiently reach typically underserved communities through a modernized approach to government-backed small business lending.”

Metcalf and his company seemed to be excited to take part in the committee, having a direct impact on the space in which their business operates. “On behalf of Funding Circle, I look forward to working with stakeholders across the lending landscape to support an effective bipartisan SBA reauthorization that best prepares the agency to help small business owners,” he said.

Members of the committee are confident that the group will help modernize the practices of the SBA while also empowering them. “The government agency dedicated to supporting [small businesses] must do the same and adapt its systems and programs to support that evolution,” said BPC Board Member and former Senator and Chair of the Committee on Small Business and Entrepreneurship Olympia Snowe. “I’m confident that this task force will successfully develop ideas and recommendations to enable the SBA to do that.”

Pandemic-Induced Pivot Results in Innovative Lending Software

October 15, 2021 “What the hell are we going to do now?”

“What the hell are we going to do now?”

Kunal Bhasin, CEO of 1West, saw the light at the end of the tunnel for his business in March of 2020. Instead of closing his doors and pursuing other options in finance, Bhasin held strong and began developing a product that was merely an idea prior to his business’s abrupt halt.

“I made the decision at that point when everyone was running, I hired two full time engineers. I said hey, I’ve had this idea for a long time, the whole company has had this idea for a long time, we just never had the time to implement, and then all we had is time because we [weren’t] closing that many deals.”

The idea, a software called ABLE (Automated Business Lending Engine) is a platform that minimizes the lapsed time that occurs in the funding process. “There were deals all over the place in different people’s inboxes. And then those people would have to put those deals into our processors, which created huge gaps of time,” said Bhasin.

“We needed to centralize the deal flow. Whether the deal is coming from a partner, or the deal is coming from a customer, [we needed] a centralized place where a customer could land and start completing the process.”

With the help of his former college roommate, engineers, and staff, Bhasin put his idea to fruition— and ABLE took off. “We rolled up our sleeves and spent the better part of the last 16 months building it, and now the largest percentage of my time devoted to running 1West is on the software and the platform.”

Bhasin claims that his product gives his company a huge competitive advantage, as he is able to use AI to evaluate, process, and determine the type of funding and through which lender is best on an individual basis.

“[ABLE] really shrinks that entire gap time so when the lenders get in early morning, when the funders get in early morning, our stuff is always in queue, and it’s created really nice returns on the amount of customers we’re getting and the amount of deals we’re funding.”

The automation of the application process has allowed potential borrowers to not only find the ideal package for their needs, but allows them to apply for different types of capital streams, something that would take tons of manpower and time without the ABLE software.

“Greater than 90% of the customers who come into ABLE apply for more than one product,” said Bhasin.

When asked about if there were any plans to license the product in the future, Bhasin was hesitant to give a definite answer for the future of his creation. ABLE is already white labeled by 1West for brokers.

“Maybe,” he said, I want 1West to reap the benefits of it for 6-12 months and fix all the tweaks we have to make. We have a lot going on.”