Business Lending

Stripe Capital Originated 81,000 MCAs and Business Loans in 2025

February 25, 2026 Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe recently conducted a study to measure the impact of Stripe Capital on its customers and found that “businesses that accepted Capital offers grew 27 percentage points faster over the following year than comparable businesses that didn’t.”

“The averages conceal a wide spread,” the company said. “The fastest-growing decile of financed businesses grew more than 3× faster than comparable peers; the next decile grew nearly 100 points faster. A representative example: Xirsys, a server hosting business based in California, used financing from Stripe Capital to set up additional servers in China, India, and Japan, subsequently doubling its revenue. Notably, even businesses with low credit scores grew 11 to 18 percentage points faster after receiving financing.”

Stripe’s rumored interest in PayPal is also notable in the fact that PayPal also has a business loan program. Last year PayPal funded $2.2 billion to small businesses, down from $3 billion in 2024.

BHG Financial Originations Surge to $6.1B in 2025

February 20, 2026“With regards to BHG, that team down there just continues to deliver, you can see that with their performance in 2025,” said Pinnacle Financial Partners CFO Jamie Gregory on the company’s recent Q4 earnings call. Pinnacle owns 49% of BHG Financial. BHG’s average business loan is between $20,000 to $250,000. It also does personal loans. Combined they originated $6.1B in 2025, up from $3.7B in 2024.

Pinnacle has been very impressed with BHG’s performance and outlook going forward.

“I mean we’re talking 25% to 35% growth for the company,” said Gregory. “So they continue to perform. And I go through all that because it just shows that they are focused on their core business. They’re focused on growing it, adding value.”

In the earnings presentation, it says that BHG targets borrowers through direct mail and “other sophisticated marketing techniques using a wide range of proprietary marketing tools.”

Shopify Capital Finishes 2025 With $4.2B in MCAs and Business Loans

February 18, 2026Shopify revealed its full year MCA & business loan origination figures. $4.2 billion. That’s $1.2 billion over the previous year. Only 91.9% of these deals were considered “current” as of December 31, 2025. That’s down slightly from last year when 93.7% of deals were considered current at year-end.

For clarity, Shopify Capital offers funding in 8 total countries. The product is considered a value-add to its e-commerce platform and only offered to merchants who use it. Shopify Capital is in the same league as Square Loans and Enova in terms of origination volume.

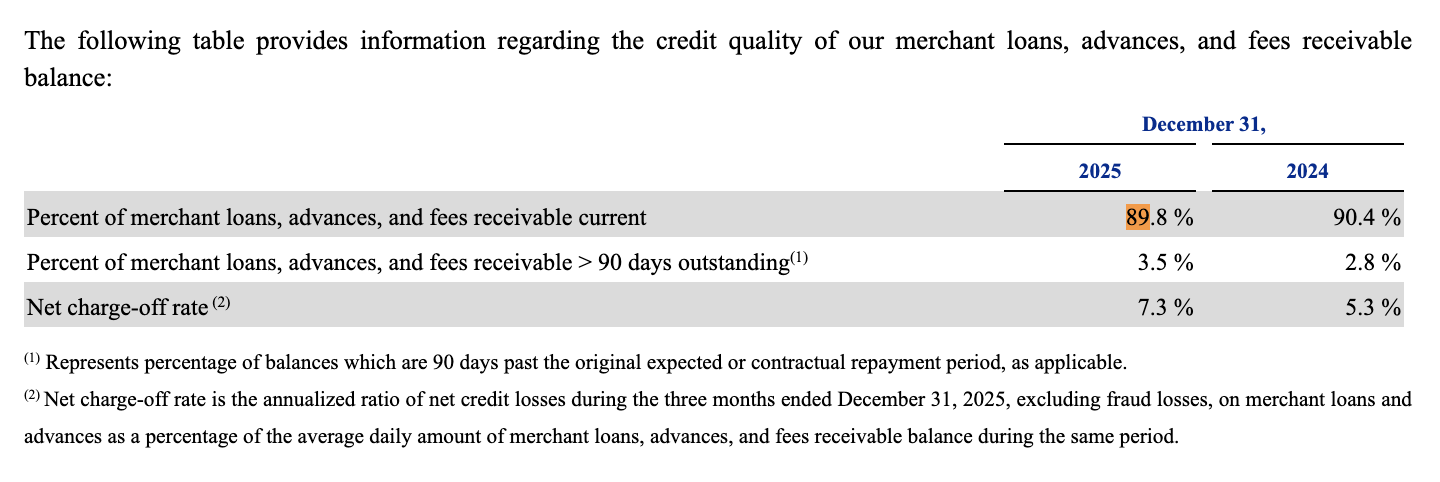

PayPal: > 10% Business Loans Not Current

February 4, 2026PayPal finished 2025 with ~$2.2B in business loan originations, down from $3B the prior year. As of December 31, 2025, only 89.8% of their portfolio was current, down slightly from the prior year.

Charge-offs, however, are up significantly. The percentage excludes “fraud losses.”

PayPal’s CEO was replaced this week after the Board was disappointed by the company’s overall trajectory. Enrique Lores, the former president and CEO of Hewlett Packard, is now in the top spot. The upheaval was enough to prompt commentary from PayPal’s former president of the 2012-2014 era, David Marcus. On PayPal’s lending business specifically, Marcus offered this critique:

“On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else.”

Enova: On the Ground, Small Businesses Optimistic

January 28, 2026Enova reported $1.6B in small business loan originations for Q4 2025, a big jump from the $1.4B in the prior quarter.

“There’s been a lot of noise over the year of 2025 around the impacts of tariffs and the macro economy and where we are,” said Enova CEO Steve Cunningham during the earnings call. “But I think what I wanted to highlight in my commentary is that it’s not quite as gloomy as it seems on the ground. It seems that small businesses are looking forward positively. And I think it’s reflecting in the demand that we’re seeing.”

On the ground that they see, credit quality and net charge-offs have also remained stable.

“Our internal and external data highlight that SMBs continue to express confidence in the economy and expect favorable operating conditions during 2026,” Cunningham said.

In its latest study and report it published with Ocrolus, they found that “Overall, growth expectations amassed an all-time high with 94% of small businesses projecting growth over the next 12 months.”

Enova also expects to close its acquisition of Grasshopper Bank in the 2nd half of this year and said that both companies are business as usual until that happens.

Fintech Small Business Lender Origination Volume Snapshot

January 16, 2026It was full speed ahead in 2025. Here’s how the origination volume stats were trending among the biggest fintech small business lenders for the first nine months of last year.

| Lender | First Three Quarters 2025 | All of 2024 |

| Square Loans | $5 billion | $5.7 billion |

| BHG Financial | $4.4 billion | $3.7 billion |

| Enova | $4 billion | $3.98 billion |

| Shopify Capital | $2.8 billion | $3 billion |

| PayPal | $1.6 billion | $3 billion |

deBanked tracks fintech small business lenders that publicly report (or privately report to us) their origination volumes. Square Loans became the largest in 2021 and has held on to the top spot ever since. Their advantage (and limitation) is that they lend only to merchants in their POS payments ecosystem.

A dark horse not listed, because precise origination volumes are not available, is Parafin, an embedded lender that works through partnerships with DoorDash, Amazon, Walmart, TikTok and more. At last report, the company said it had made more than $14 billion in offers.

California Partnered With a Revenue Based Financing Provider

January 13, 2026On the California Small Business Loan Match website operated by The California Infrastructure and Economic Development Bank (IBank), is a list of vetted partner small business lenders that the state guarantees loans for. One of those lenders is AltCap California which actually offers revenue based financing.

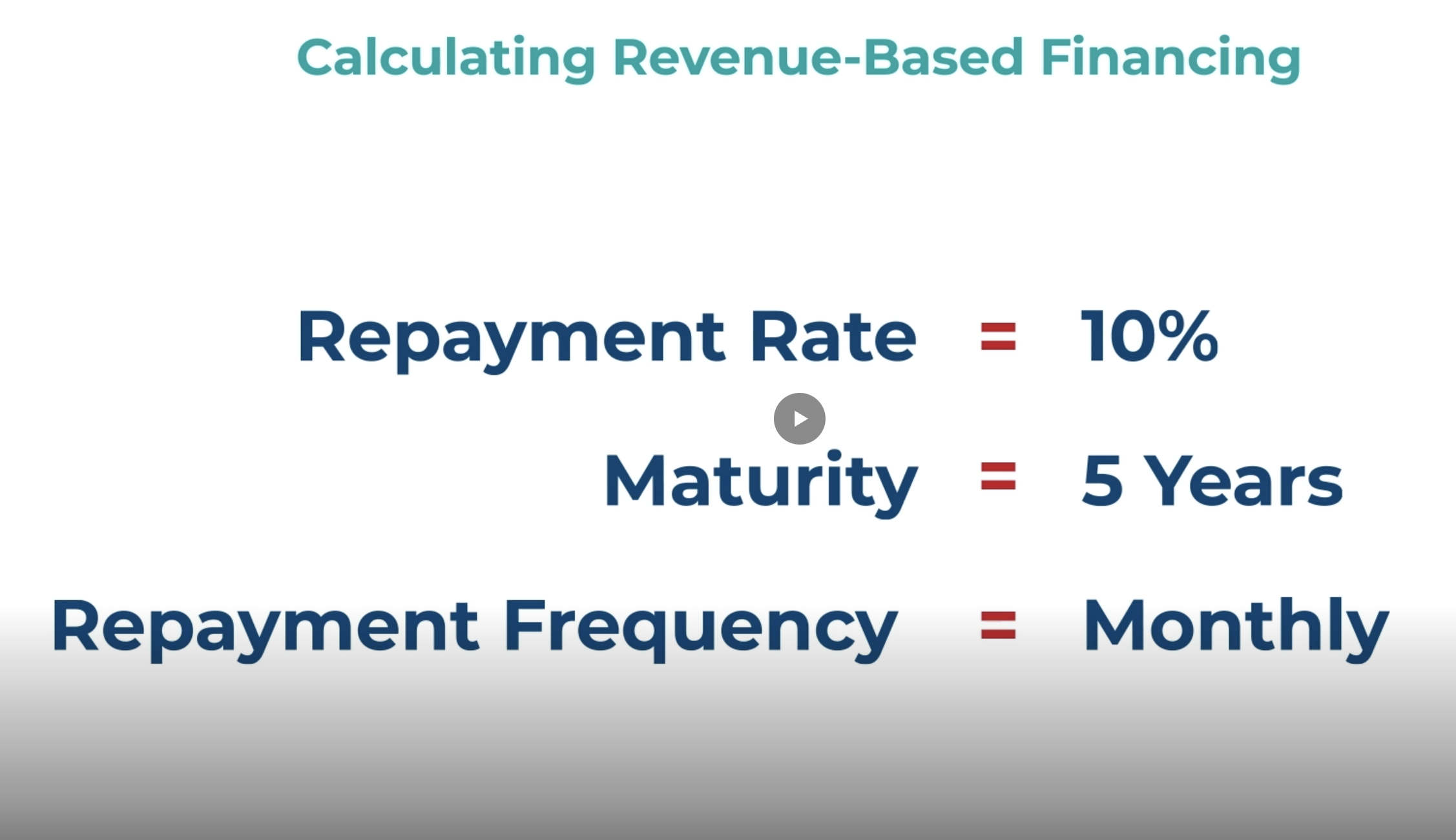

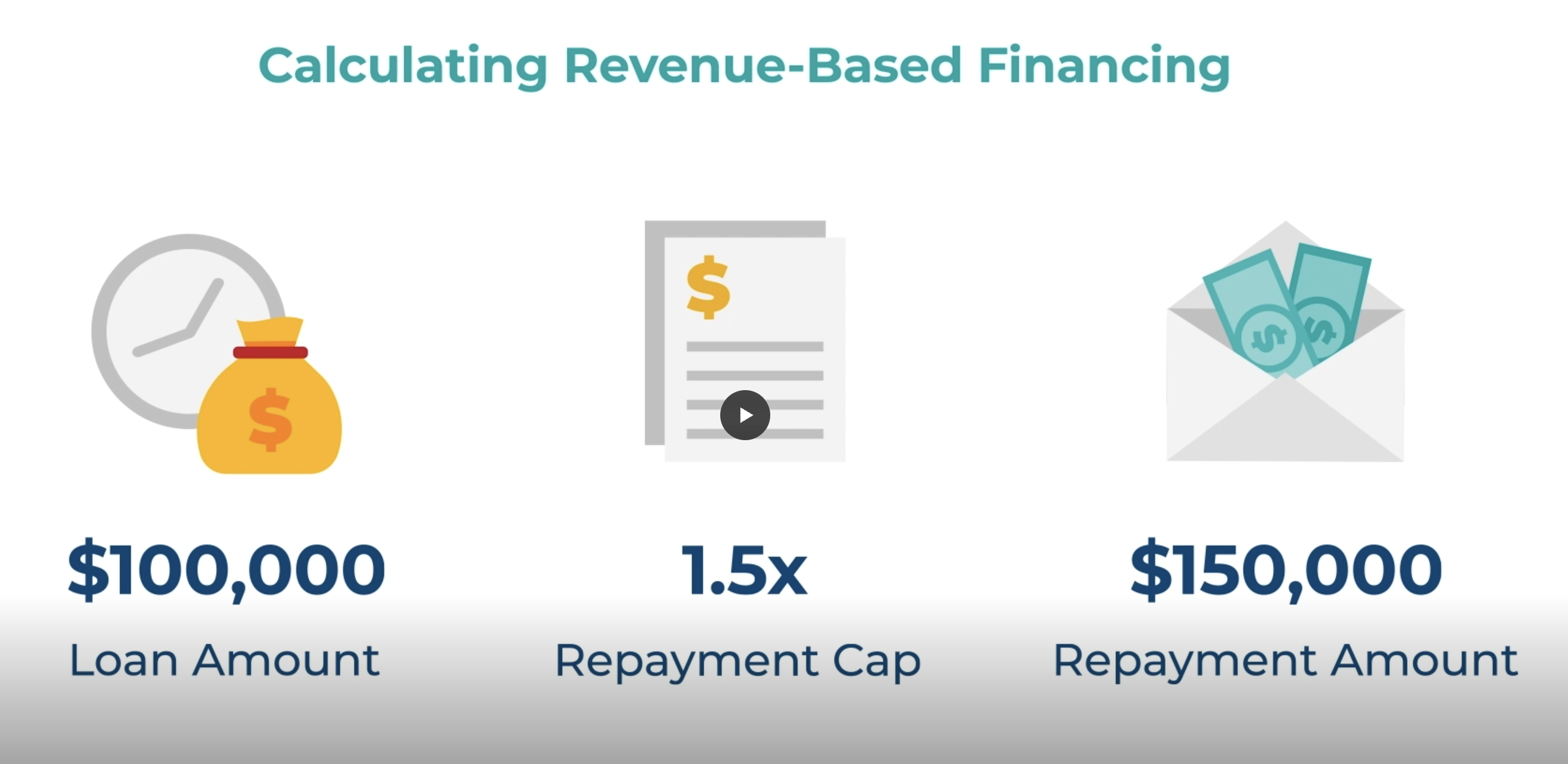

At face value, AltCap describes the cost of its revenue based financing as having to pay up to 7.5% of monthly revenue with a total cost of 1.4x to 1.5x. Its multi-part video education series describes revenue based financing costs as working in the following way:

Repayment Cap: Multiple of the total loan amount used to calculate the set dollar amount to be repaid. (Total Cost of Capital)

Repayment Rate: Share of revenue taken to repay the loan. (Holdback %)

It reinforces this in its Case Study example of Juice Boost (the 2nd video) where it explains that the metrics used to calculate the cost of Revenue Based Financing are the Repayment Cap (factor rate) and Repayment Rate (holdback %).

In its final video, the 4th video, it tells borrowers to inquire about APRs to make comparisons against companies like Square, Amazon, Stripe, and Shopify.

“Revenue-Based Financing allows small businesses to raise funds by pledging a percentage of future, ongoing revenues in exchange for capital provided by a lender,” the website says. “Revenue-Based Financing is different than debt financing. Interest is not paid on an outstanding loan balance and there are no fixed payments. Instead, payments are proportional to a firm’s performance, offering a flexible, patient source of financing.”

New Year, New Lenders?

January 5, 2026There’s a couple new lenders on the block to keep an eye on.

One of them is named Slope. Backed by both JPMorgan and OpenAI CEO Sam Altman, Slope offers revolving lines of credit up to $5 million. And they’re already out there. Seemingly overnight they’ve become capital providers for a number of large e-commerce platforms including Amazon and Walmart and are now listed alongside Parafin on both. When they announced their deal last year with JPM, they said that the US embedded financing market was worth $20 billion and that the B2B economy was $125 trillion. Slope is also offering a new AI underwriting tool.

Another is named Uncapped. Walmart says that Uncapped offers term loans while Amazon says that Uncapped offers lines of credit. The Uncapped website says that they offer loans from $10,000 to $2 million and that they accept business from business loan brokers. The company was technically founded in 2019, but in the UK.