Business Lending

LendingClub Expects Modest Growth of its Commercial Lending Business

May 1, 2022 Fintech bank LendingClub expects its commercial loan business to grow modestly, according to Sameer Gokhale, Head of Investor Relations. Gokhale made the comment briefly during the company’s Q1 earnings call. “These commercial loans are largely secured by collateral or cash flow and should continue to be a good source of revenue and credit quality diversification,” he added.

Fintech bank LendingClub expects its commercial loan business to grow modestly, according to Sameer Gokhale, Head of Investor Relations. Gokhale made the comment briefly during the company’s Q1 earnings call. “These commercial loans are largely secured by collateral or cash flow and should continue to be a good source of revenue and credit quality diversification,” he added.

LendingClub had $615M worth of commercial loans and equipment leases on its balance sheet as of March 31st. That excluded the $185M worth of PPP loans it still held.

The company’s overall lending business is still consumer-focused. Auto lending is expected to increase, but not to such an extent that it catches up to Lending Club’s personal loan business.

Overall, the company reported a net income of $40.8M on $289.5M in revenue for the quarter.

CUNA to Congress: No More Direct Lending From the SBA, Please

April 28, 2022 On Tuesday the Credit Union National Association wrote letters to the House and Senate Small Business Committees stating that it is in the best interest for small business entrepreneurs to partner with a financial service provider, rather than the Small Business Administration directly. CUNA addressed their role in supporting emerging businesses and argued for policies that would block the SBA from serving as a direct lender. The letters will be brought forward at an oversight hearing to examine the SBA on Wednesday.

On Tuesday the Credit Union National Association wrote letters to the House and Senate Small Business Committees stating that it is in the best interest for small business entrepreneurs to partner with a financial service provider, rather than the Small Business Administration directly. CUNA addressed their role in supporting emerging businesses and argued for policies that would block the SBA from serving as a direct lender. The letters will be brought forward at an oversight hearing to examine the SBA on Wednesday.

CUNA stated, “… we strongly support legislation – such as S. 3382 and H.R. 6037 – that would prohibit the SBA from directly making loans under the 7(a) Loan Program and oppose any efforts in the FY 2023 Budget to fund a direct lending program.”

As the SBA became a direct lender during the COVID-19 pandemic, relationships between small businesses and financial service providers have not been able to form.

“… when working with local lenders, small businesses are likely to benefit from guidance and experience from a lender with a stake in helping the borrowing business succeed. By becoming a direct lender to small businesses, the SBA is likely to harm local financial institutions’ relationships with businesses and possibly hamper these businesses from establishing important banking relationships that can only help their business survive and flourish.”

At the small business committee hearing, Congressman Stauber questioned SBA Administrator Guzman on how the Biden administration is helping both the middle class and small businesses with inflation.

Guzman discussed how the President is taking action on energy costs, “he has made available a million barrels a day, to try to control some of the gas costs which we know are affecting our small businesses…”

Stauber responded, “…the strategic petroleum reserve really should be held for national emergencies not failed policies…” He further mentioned his concerns as he believes the administration is not acting quick enough as inflationary costs are rising for small businesses.

IOU Financial Originated $59.6M in Loans in Q1 2022

April 27, 2022 IOU Financial is experiencing tremendous growth. The small business lender revealed that it originated $59.6M in loans in just the first quarter of 2022. In its quarterly earnings report, it set a target range of $220M to $260M in originations for the whole year of 2022. This would be a massive increase over its loan originations last year when it set a personal record of $161.5M.

IOU Financial is experiencing tremendous growth. The small business lender revealed that it originated $59.6M in loans in just the first quarter of 2022. In its quarterly earnings report, it set a target range of $220M to $260M in originations for the whole year of 2022. This would be a massive increase over its loan originations last year when it set a personal record of $161.5M.

Separately, the company is profitable. IOU achieved net earnings of $3.7M on an IFRS basis. It also had $119.5M in loans under management as of year-end 2021.

“The Company attributes a significant portion of its strong growth in loan originations to its successful transition from a balance sheet strategy (under which the Company traditionally funded loans to its balance sheet) to a marketplace strategy under which new loan originations are primarily being sold to institutional purchasers,” IOU said in its official announcement.

“IOU’s marketplace strategy allowed the Company to originate significantly more volume in 2021 than would have previously been possible under the financial limitations of a balance sheet strategy,” said Robert Gloer, President and CEO of IOU. “This has proven to be a win-win that has in turn given us the financial latitude to repurchase approximately $3.7 million in convertible debentures in 2021 and invest in strategic growth initiatives as part of our Post-Pandemic Growth Plan.”

Lendistry and Obtaining a Small Business Lending Company License

April 26, 2022

On April 19th B.S.D. Capital, Inc. dba Lendistry (“Lendistry”) announced that Lendistry SBLC LLC, its wholly-owned subsidiary, was granted a Small Business Lending Company license from the US Small Business Administration. With the license, Lendistry SBLC will now be able to offer SBA 7(a) loans of up to $5 million nationwide.

SBLCs are regulated, supervised and examined by the SBA, except for the small portion of SBLCs defined as Other Regulated SBLCs. As defined in 13 CFR 120.10, SBLCs are non-depository lending institutions that are authorized only to make loans pursuant to section 7(a) of the SBA and loans to Intermediaries in SBA’s Microloan program. Lendistry is now among one of only 14 non-depository lending institutions nationwide to hold a spot of this kind and is the only African American-led lender to hold an SBLC license. The company says it’s even “more rare to be an SBLC licensee that can also offer loans under other community development programs.”

“We believe there’s a huge demand there for our existing clients and some small businesses that are already familiar with Lendistry, but also those who are not familiar with it yet, but require or need access to capital that can’t get it from a traditional lender, we believe that we will be able to serve them during this pandemic time,” said Kerrington V. Eubanks, SVP, Strategic Partnerships at Lendistry in a call with deBanked.

The company says it has recently seen an uptick in interest for loans and lending products as small businesses move forward post-pandemic. Lendistry says it will work to do its part in the recovery. “By supporting them with our lending products, by supporting different partners with leveraging our platform as a service,” Eubanks explained.

Lendistry has provided just over 8.5 billion in capital deployed to about 570,000 businesses across the country. The company’s goal is to double their current number in capital.

Business Loan Seekers Likely to Consider Numerous Options, Study Says

April 25, 2022 New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

Though this study focused on the Canadian market, it may partially explain a finding in the US, that more small business owners seeking capital are seeking out a merchant cash advance as a potential option than ever more. (A Federal Reserve study said that 10% of SMB capital seekers sought a merchant cash advance in 2021). That would make sense if business owners are obsessively applying to multiple sources for the sake of making more comparisons.

But even while they shop, they might not always be satisfied with what they learn, nor the outcome. Smarter Loans reported that only 60% of business loan seekers felt informed about their options while 40% of business owners that went forward with a business loan were not satisfied with their loan provider.

When examining both the business loan and consumer loan market, Smarter Loans says that loan seekers are more likely to receive their funds the same day they apply than ever before. (53% of those surveyed received funds within 24 hours of applying.)

Click here To view the full 2022 FinTech Lending Study published by Smarter Loans.

New Domain Name Gold Rush Sets Up Possible Battle for Future of SMB Finance

April 25, 2022 If you could have businessloan.com or businessloans.com as your website, would you jump on the opportunity to get it?

If you could have businessloan.com or businessloans.com as your website, would you jump on the opportunity to get it?

It’s evident that the market for keyword-based domains has evolved over time. Couldn’t get the .com? You could’ve tried to get the less coveted .net or .org. Don’t like those? Today, you can get the .business, .deals, .financial, .loan, .loans, or hundreds of other customized tlds. With so many to choose from, most experts in the field would advise that if you don’t own the .com version, to not even bother getting cute with customizations for your brand or keyword because customers will just get confused.

But recently, another domain name market has quietly been gaining steam. It’s for something called a .eth, an Ethereum blockchain-based crypto address shortener by the Ethereum Name Service. It’s not necessarily something one could use to build a website with, at least not yet. Originally envisioned as a way to condense long impossible-to-remember crypto wallet addresses into memorable words, users have started to buy up a bunch of keywords that may be familiar to deBanked readers. Just to name a few:

- businessloan.eth

- businessloans.eth

- smbloans.eth

- merchantcashadvance.eth

- ach.eth

- syndication.eth

- lending.eth

- ppploan.eth

- underwriting.eth

- brokers.eth

- loanbroker.eth

- mca.eth

- factoring.eth

- funding.eth

- backdoored.eth

At face-value, this might appear to be a vanity crypto play, one in which one could send crypto to your-name-here.eth instead of trying to type out a long address like: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. But an ENS domain name holds much more potential than just that. It’s moving towards becoming the backbone of one’s identity in the upcoming era of the web called web 3.0 (web3 for short). Instead of having to remember passwords for hundreds of websites, identity can be validated through one’s digital wallet. Such a concept is not theoretical. It’s already being used.

Take seanmurray.eth for example. You could send eth, bitcoin, litecoin, or dogecoin to it, but at the same time it’s connected to an email address and a url (this one). Plus it’s linked to an NFT avatar (broker #7 from The Broker NFT collection) which is in that wallet. I can use it to do an e-commerce online checkout in 5 seconds without ever needing to enter any payment information even if I’ve never visited the site before. It’s faster than PayPal and with less steps involved. I can connect it to my twitter account, OpenSea, or use it to vote in an official poll without ever having to create an account on something. The wallet is the identity verification. The .eth name, therefore, has the potential to become the defining baseline of who or what one is on the internet. Not theoretically. It’s already happening.

Take seanmurray.eth for example. You could send eth, bitcoin, litecoin, or dogecoin to it, but at the same time it’s connected to an email address and a url (this one). Plus it’s linked to an NFT avatar (broker #7 from The Broker NFT collection) which is in that wallet. I can use it to do an e-commerce online checkout in 5 seconds without ever needing to enter any payment information even if I’ve never visited the site before. It’s faster than PayPal and with less steps involved. I can connect it to my twitter account, OpenSea, or use it to vote in an official poll without ever having to create an account on something. The wallet is the identity verification. The .eth name, therefore, has the potential to become the defining baseline of who or what one is on the internet. Not theoretically. It’s already happening.

Crypto is already starting to creep into the small business finance industry. In August, a funding company announced that it would begin offering commissions and fundings in crypto because of the speed potential. Far from being a gimmick, brokers started to choose crypto payments over ACH or a wire because of how fast it would be. There’s also no chargeback risk with crypto.

Currently, the owner of mca.eth has listed the domain for sale on OpenSea at a price of 20 eth (approximately $60,000). That’s less than what MerchantCashInAdvance.com sold for in 2011. Perhaps the value of an Ethereum Name Service domain holds less promise than a website that ranked well on Google in 2011. But then again, being well ranked on Google is not as important as it used to be. It’s impossible to say what, if any impact web3 will have on the small business finance industry long term, but for now there are those out there quietly buying up names like ach and funding and syndication on the chance that they will become something.

Ten Percent of Small Businesses That Sought Financing in 2021 Sought a Merchant Cash Advance

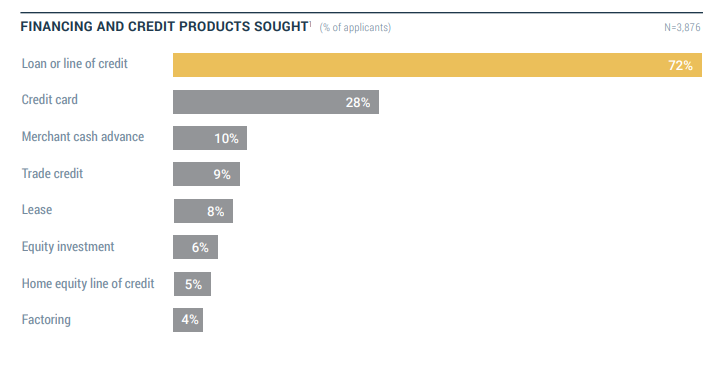

April 18, 2022A whopping 10% of small businesses that sought financing last year sought out a merchant cash advance, according to the latest study published by the Federal Reserve. That figure was up from 8% in 2020 and 9% in 2019. For the the preceding years, that figure had held fairly consistent at 7%. [See 2015, See 2017]. Market penetration, therefore, has arguably increased by about 40% since 2015.

Meanwhile, the percentage of applicants that sought out leasing has gone down over the last seven years: from 11% in 2015 to 8% in 2021. Factoring has hovered around 3-4% consistently.

The pursuit of of loans and lines of credit decreased dramatically from 89% in 2020 to 72% in 2021. And approvals have gone down across the board. Approvals on business loans, lines of credits, and MCAs hit a peak of 83% in 2019 and plunged to 76% in 2020, the first year of Covid. The figure fell even further in 2021, down to 68%. Online lenders and large banks had the lowest approval rates overall, at 51% and 48% respectively.

Small Business Finance Industry Mulls What’s in The Rearview, Is Optimistic For Rest of 2022

April 14, 2022 The small business finance industry is looking ahead to anticipated growth for the remainder of the year, despite new challenges ahead. With massive government aid fading in the rearview, some industry players now have had the time to consider what the impact of it was as they move onward into the future.

The small business finance industry is looking ahead to anticipated growth for the remainder of the year, despite new challenges ahead. With massive government aid fading in the rearview, some industry players now have had the time to consider what the impact of it was as they move onward into the future.

Bob Squiers of Meridian Leads expressed his view on the topic, “a lot of our customers, mostly the ISO shops, many of them converted and started selling and pitching the government programs. So in that sense it kind of helped keep those guys afloat, helped keep our business going. A lot of what we do in the marketing side, translated for those government programs. But then it did also squash the demand for the cash advance.”

In some cases, government funding has helped merchants pay off pre-existing obligations in a timely manner. Matthew Washington, founder and CEO of Moneywell GRP, noted, “An educated business owner is using the financing options available as they see fit for the timing. Someone that is waiting to get an SBA or an EIDL is more susceptible to take a bridge product to get them through that time gap,” he said. “As long as you’re working with the merchant and pushing out good products and you know what is on the rise, I think it has done nothing but help in some cases.”

Trucking became one of the number one fields that made up a large percentage of submissions during the pandemic, industry insiders say. However, with gas prices increasing, business with trucking could go down. Other businesses such as restaurants, where only a third received funding last year from the government, are desperate for funding.

“There’s tons of restaurants left that haven’t yet received their funding. So we could be seeing a lot of exposure in that industry,” stated Michael Yunatan of Specialty Capital. “But overall, I definitely do feel that we’ll be seeing an uptrend in our numbers across the board.”

“We definitely do think the industry is growing as a whole,” said Yunatan. “Even though we are a new player in the space we have been growing.”

Chad Otar, founder and CEO of Lending Valley, said, “We need to keep monitoring the interest rates that are coming up from the Federal Reserve, we need to make sure we’re not heading towards a recession, we need to make sure that we’re able to fully have the capital ready, in order to be able to deploy at a reasonable rate.”

Otar acclaimed the indirect benefit of large tech companies operating in the space with a competing product, arguing that the presence of PayPal and Amazon are helping to bring exposure to the industry overall.

“And now that Kabbage is back as well, since they partnered up with American Express, it’s gonna help us out to be able to push the product more into the mainstream,” said Otar. “So I believe there will be a growth in the industry.”