Business Lending

Failure to Prove Damages Dooms Usury Claim

July 27, 2015 A recent decision in an adversarial bankruptcy proceeding demonstrates how important it is to prove each and every element of a claim of usury. In the case, the court refused to award relief–despite the rate being conceded as usurious–because the debtor had failed to plead all of the required elements of the claim.

A recent decision in an adversarial bankruptcy proceeding demonstrates how important it is to prove each and every element of a claim of usury. In the case, the court refused to award relief–despite the rate being conceded as usurious–because the debtor had failed to plead all of the required elements of the claim.

The litigation involved long standing business partners whose relationship had soured. When one partner filed bankruptcy, the other filed a plethora of proof of claims for money allegedly owed.

The debtor countered with usury as a defense. While the creditor conceded that the rate alleged in its proof of claims exceeded the maximum rate in Texas, it argued that the filing of a proof of claim did not constitute a “charge” under Texas’ usury statute. Therefore, the creditor believed it was not subject to the usury penalties.

The court rejected the creditor’s contention and cited to a number of cases that had construed proof of claims as “charges” under Texas’ usury statute. These holdings, coupled with the creditor’s admission, led to a quick finding of fact that the alleged rate was usurious.

The court then turned to the element of damages. The Texas code provides that:

A person who violates this subtitle by contracting for, charging, or receiving interest or time price differential greater than the amount authorized by this subtitle is liable to the obligor for an amount equal to:

(1) twice the amount of the interest or time price differential contracted for, charged or received; and

(2) reasonable attorney’s fees set by this court.

Texas Finance Code § 349.001(a).

Despite the finding of a usurious rate, the court held that the debtor had failed to present any evidence or testimony to prove the amount of interest that was usurious under Texas law. Rather, the debtor had merely made conclusory statements that the interest rate charged was usurious. The court held these statements to be insufficient evidence to justify an award of damages.

Ali v. Merchant (In re Ali), 2015 Bankr. LEXIS 2443 (Bankr. W.D. Tex. July 23, 2015)

A Square IPO Would Be Alternative Lending’s Third

July 26, 2015 First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

Square’s merchant cash advance arm, Square Capital, reportedly funded $100 million to small businesses in 2014, a figure large enough to earn them a spot on the deBanked leaderboard.

While often reported as a lending program, Square’s own website describes their working capital transactions as sales of future credit card receivables. At face value, and aside from what their contracts might actually say, it’s a textbook merchant cash advance.

While some publicly traded companies have dabbled in merchant cash advances, the financial product is one of Square’s two major products, the first obviously being payments.

And while OnDeck offers loans that are very similar to merchant cash advances, Square could potentially be the first true merchant cash advance IPO.

Also on the IPO watch list is CAN Capital, a company that offers both loans and merchant cash advances. In November of last year, Bloomberg and WSJ claimed the company was already working on it. While it has been eight months since that news came out, word on the street is that a CAN Capital IPO is still very much a possibility.

Unfortunately, because of the same JOBS Act provision that allowed Square to file an S-1 (if they actually did) also applies to CAN Capital. There is no way to know what’s going on behind the scenes until the filing is made public or leaked to the media.

Either way, the end of 2015 will likely end in at least one more IPO for the commercial side of alternative lending.

Could Jack Dorsey and his wacky beard be the future face of the merchant cash advance industry?

BREAKING: JACK DORSEY’S BEARD pic.twitter.com/Quv8nVG9PZ

— Nicholas Carlson (@nichcarlson) June 12, 2015

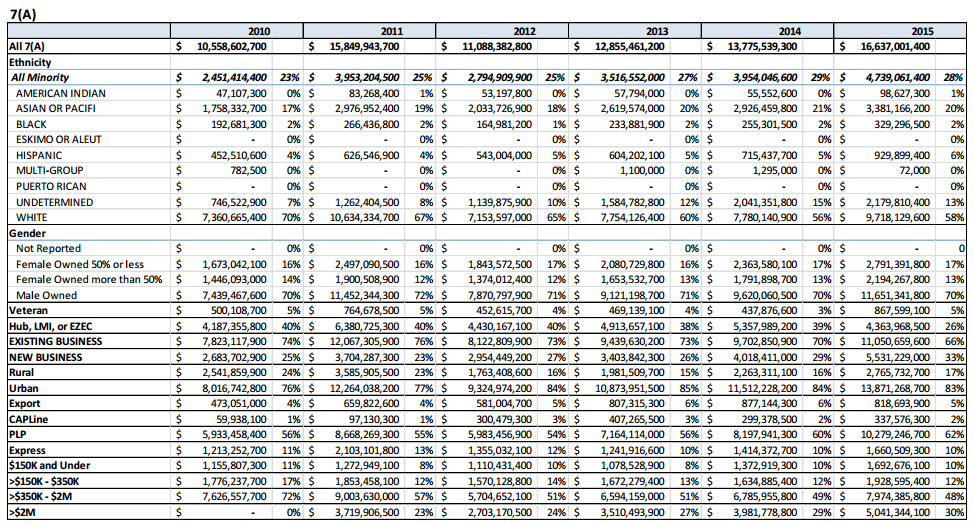

SBA’s 7(a) Loan Program is Shutting Down (For Now)

July 23, 2015 As mentioned on the Coleman Report, the SBA’s 7(a) loan program has experienced overwhelming demand this year, so much so that the SBA is being forced to shut the program down until October 1st when the fiscal year cap on loan approvals resets. At present, their loans are effectively sold out.

As mentioned on the Coleman Report, the SBA’s 7(a) loan program has experienced overwhelming demand this year, so much so that the SBA is being forced to shut the program down until October 1st when the fiscal year cap on loan approvals resets. At present, their loans are effectively sold out.

One has to wonder how disruptions like this will affect tech-based platforms such as SmartBizLoans.com whose business model depends on the SBA’s 7(a) loan program. Evan Singer, SmartBiz’s General Manager was a panelist at the AltLend Conference in NYC a few days ago.

The SBA has approved over 45,000 loans this year so far totaling more than $16.5 billion, a 25% increase year-over-year. $1.69 billion of that (as of July 11th) was for loans under $150,000.

Last year, the SBA funded $1.86 billion worth of 7(a) loans under $150,000 to small businesses, narrowly making it the top small business funder in the industry. OnDeck was a close second.

Generating Leads and Acquiring Borrowers Not Easy in Business Lending

July 21, 2015 “Banks are almost always losing money on small business lending,” said Manish Mohnot, TD Bank’s Head of Small Business Lending, on a panel at the AltLend conference in New York City. It’s a loss leader within the small business segment, he explained, because banks want to bring in deposits.

“Banks are almost always losing money on small business lending,” said Manish Mohnot, TD Bank’s Head of Small Business Lending, on a panel at the AltLend conference in New York City. It’s a loss leader within the small business segment, he explained, because banks want to bring in deposits.

Funding Circle’s Rana Mookherje concurred. “Banks just can’t make a loan under $500,000 profitably,” he said.

It’s a conundrum few outside banking think about. When consumers and businesses picture banks, they might think of loans, but when banks think of consumers and businesses, they think of deposits. The sentiment amongst the experts at AltLend was that traditional banks and alternative business lenders were not competing with each other for the same customers because each party was after a different objective.

And even when banks think about loans, because obviously they do, they just don’t approach them the way that alternative business lenders do. To that end, ApplePie Capital CEO Denise Thomas said, “Most community banks are looking to make loans backed by an asset. They just don’t want to underwrite [loans] one by one under a million dollars.”

Bankers are genuinely surprised by how alternative lenders subjectively or manually approach business loans, a subject covered just yesterday here on deBanked. Charles Green, the Managing Director of the Small Business Finance Institute and moderator of the New Pioneers panel said he never saw banks use bank transaction history to make underwriting decisions in his 35 years of banking.

The factors paraded as being more important above everything else in alternative lending today have apparently been non-factors in traditional lending for years. “There is no substitute for banking information when reviewing a client for approval,” said Andrew Hernandez, a co-founder of Central Diligence Group, in Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree. These kind of statements are mind-blowing in traditional lending circles.

Nevertheless, banks watch in awe as alternative lenders not only make small commercial loans, but do it profitably. But how they source borrowers isn’t rocket science. Jim Salters, the CEO of The Business Backer pointed out that some alternative lenders are marketing on a large scale by running TV or radio commercials. But that level of investment isn’t for everyone, especially younger companies.

“Direct mail isn’t sexy, but it converts,” said Candace Klein, the Chief Strategy Officer of Dealstruck. She also said that her company is doing radio advertising.

Matt Patterson of Expansion Capital Group is well versed in digital marketing and incorporates SEO and online paid advertising such as Facebook in his strategy. There’s a difference in the conversion rate in advertising on Facebook versus something like Google, he explained. On Google, business owners are looking for something whereas on Facebook they stumble across it.

Everyone agreed that Pay-Per-Click marketing such as Google Adwords was very expensive in this competitive landscape.

Jim Salters, CEO of The Business BackerBut where can funders and lenders reliably turn to acquire deal flow cost effectively? Salters revealed the industry’s worst kept secret, brokers. The Business Backer acquires about half of its volume from brokers and the other half directly, according to Salters.

“The broker channel is one of the most cost effective channels for us,” said Klein, who would not say on the record exactly how much of Dealstruck’s total business was from brokers.

Patterson agreed with the favorable ROI of using brokers, but saw benefits to communicating with small businesses directly. “Everything about that relationship is better when you’re talking directly to that merchant,” he said. And yet, “our direct leads convert much lower than our broker leads will,” he added.

The panelists generally agreed that this was because brokers have essentially already gathered the documents and closed the deal by the time the lender or funder is finally seeing it.

But aren’t brokers and humans the antithesis of tech-based lending?

Brett Baris, the CEO of up-and-coming lender Credibility Capital said, “We were actually a little surprised by how much a human is needed.” Baris’ company acquires most of its leads through a partnership it has with Dun & Bradstreet. Most of their borrowers are prime credit quality.

“The human element is very important to get the higher quality borrowers to the finish line,” Baris noted. TD’s Mohnot was not surprised. For applicants doing $5 million to $6 million a year in revenue, they want somebody to walk them through the loan process, he opined.

“Merchants love talking to people,” Patterson said. “Some of that comes from the frustration of calling their bank and not being able to talk to people.”

But would that mean the assumptions about automation are wrong? Not quite, explained Mohnot. It’s the younger business owners who have the impulse desire to do things fast or online, he said.

And Klein said that observing merchant behavior at least at her company has shown that those all too eager to apply for a loan in an automated online fashion are typically looking for smaller amounts like $20,000 to $40,000. Meanwhile Dealstruck’s loan minimum is $50,000.

Not everyone is as fortunate as Baris, who is able to generate leads through the trust inherent in a conversation that originated with a D&B rep, but real actual bank declines are making their way to alternative lenders. They’re not the holy grail that everyone thinks they would be though.

“Conversions tend to be lower from bank leads because they’re expecting 6% and are insulted when they hear [a higher %],” said Klein. And Salters who refers to his company as a “turndown partner of choice for upstream lenders,” shared how hard it is for a bank to partner with an alternative lender in the first place. Years ago, banks were aghast by his hands-on, manual underwriting approach that he felt was his company’s core competency. The banks were afraid their regulators would freak out over something so subjective.

And yet Merchant Cash and Capital’s founder, Stephen Sheinbaum and Credit Junction’s CEO Michael Finkelstein both told an audience that they saw banks as collaborative partners.

Meanwhile, Dealstruck actually has a graduation system where merchants graduate out of their loan program and become eligible for a real bank loan. Klein explained that a small business could be referred to them by the bank and then after a couple of years of good history, they’ll refer it back to them.

The acquisition secret however seems to be in finding your strength. ApplePie is focused exclusively on franchises. Expansion Capital Group has formed relationships with several trade organizations. Credibility Capital goes hand-in-hand with D&B.

Still, there is no doubt that the broker channel is alluring, but it can be a slippery slope. Raiseworks CEO Gary Chodes cautioned that “brokers are incentivized to follow the money.” Klein also expressed concern. She knows firsthand how challenging brokers can be since she’s had to terminate some in the past for bad behavior.

“Transparency is extremely important,” Finkelstein proclaimed in regards to the customer experience. This means that lenders can’t simply work off the ROI metric alone. But that ROI is the envy of banks nationwide.

Banks want to refer their clients to alternative lenders because if they get approved, then the lender is going to deposit those funds at their bank, Mohnot alluded.

It would seem that there is not one particular methodology that works better than all the others to acquire a borrower and that’s okay. Alternative lenders struggling to maximize their ROI can take comfort in the fact that banks, with all the resources they have at their disposal, accepted a long time ago that it was impossible to even make money at all in small business lending.

If you’re at least in the black, you’re probably doing just fine…

Alibaba Teams Up with Capify to Make Business Loans

July 21, 2015 Hours after AmeriMerchant announced it had been rolled up into an international business lending conglomerate known as Capify, The Australian Financial Review released a story that said Alibaba (NYSE:BABA) would already be teaming up with them. The partnership’s goal is to offer small business loans to 1.9 million Australian customers.

Hours after AmeriMerchant announced it had been rolled up into an international business lending conglomerate known as Capify, The Australian Financial Review released a story that said Alibaba (NYSE:BABA) would already be teaming up with them. The partnership’s goal is to offer small business loans to 1.9 million Australian customers.

The story quotes Alibaba executive Michael Mang. “The purpose of the collaboration with Capify is to increase traffic and encourage more people to buy things on the internet. We’re not competing with banks and we’re not trying to create competition here. Buying and selling is the core of our business,” Mang told the Financial Review.

John De Bree, the former Managing Director of Australia-based AUSvance is now Australia’s Managing Director of Capify. De Bree reportedly said, “while there is technically no limit to SME’s access to capital, it expects to lend around $40 million to Australian SMEs over the next 12 months.”

AmeriMerchant joined UK-based United Kapital, Australia-based AUSvance, and Canada-based True North Capital to be a “global provider of alternative finance solutions, including business loans and additional working capital products, to small and medium-sized businesses.” AmeriMerchant’s founder David Goldin became the conglomerate’s CEO and President.

Capify Consolidates Four Companies Including AmeriMerchant Under One Umbrella

July 21, 2015 What do US-based AmeriMerchant, UK-based United Kapital, Australia-based AUSvance, and Canada-based True North Capital all have in common? They’re now all under the Capify Umbrella. According to a press release issued earlier today,”Capify will now operate under one unified name to serve as a global conglomerate provider of alternative finance solutions, including business loans and additional working capital products, to small and medium-sized businesses. Capiota, United Kapital’s business loan product provider, will also be included in the global rebrand as a part of Capify’s UK office.”

What do US-based AmeriMerchant, UK-based United Kapital, Australia-based AUSvance, and Canada-based True North Capital all have in common? They’re now all under the Capify Umbrella. According to a press release issued earlier today,”Capify will now operate under one unified name to serve as a global conglomerate provider of alternative finance solutions, including business loans and additional working capital products, to small and medium-sized businesses. Capiota, United Kapital’s business loan product provider, will also be included in the global rebrand as a part of Capify’s UK office.”

The consolidation of an Australia-based funding company is notable since that country’s commercial financing landscape is the subject of an upcoming magazine feature story of deBanked’s July/August issue due to be distributed in a couple weeks. In that story, AUSvance’s John de Bree said of American interest over there, “I’m very surprised, the American market’s 15 times the size of ours.”

But as our readers will learn when the story is published, that market is just beginning to heat up.

David Goldin, the founder and CEO of AmeriMerchant will continue to be the consolidated company’s CEO and President. For those not familiar with his background, the release states:

Goldin created this business enterprise with no outside capital or funding and grew the company to more than 200 employees combined globally in all four offices. He entered the alternative lending space in 2002, after previously selling his startup company to Winstar Communications, a multi-billion dollar publicly-traded company at the time of the sale. Goldin has overcome many business obstacles including winning a ground-breaking patent lawsuit that threatened to end the U.S. alternative finance industry in its infancy stages. Via its proprietary underwriting technology platform, the company has demonstrated low default rates especially during the 2007-2009 global recession, a challenging time that resulted in the collapse of many alternative funding companies.

You can check out the full press release here.

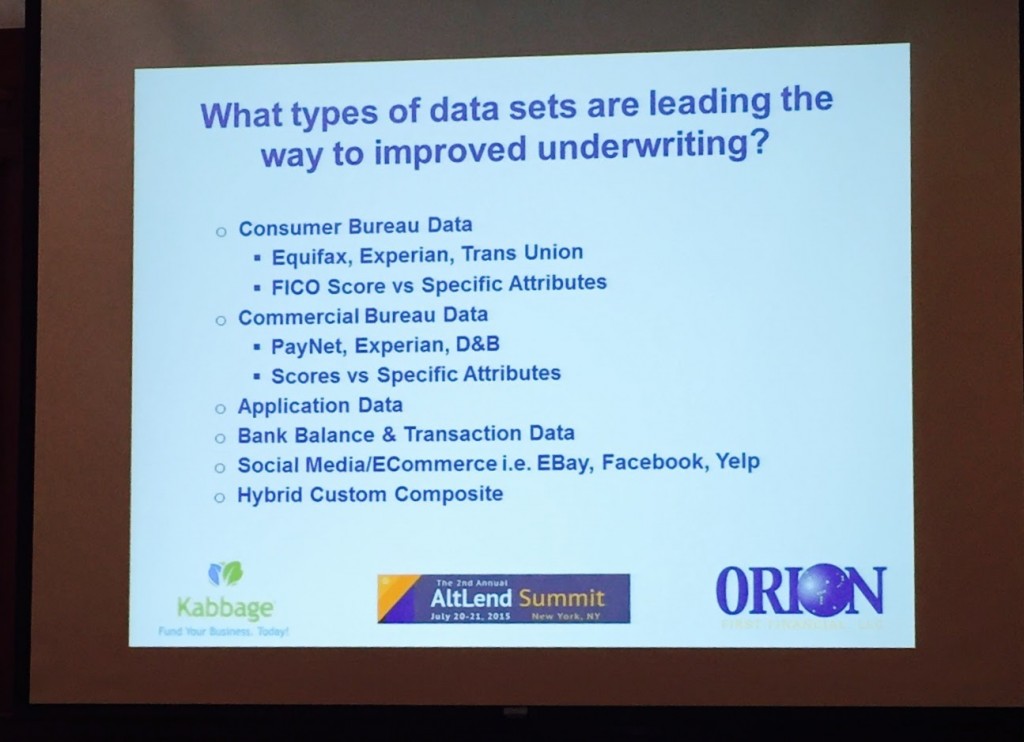

Manual Underwriting Still Dominates in Tech-based Lending Environment

July 21, 2015For all the talk that technology is changing the way people lend and borrow, the commercial side appears stubbornly reluctant to relinquish control to algorithms. At the AltLend conference in NYC, business lenders and merchant cash advance companies alike were mostly united on the idea that somebody needs to be double checking the computers.

“I like eyes on a deal,” said Orion First Financial CEO David Schaefer. He discussed why an entirely manual underwriting process had weaknesses however through an experiment he conducted years ago when he sent the same deal to six underwriters. “Three said yes and three said no,” he explained.

“I like eyes on a deal,” said Orion First Financial CEO David Schaefer. He discussed why an entirely manual underwriting process had weaknesses however through an experiment he conducted years ago when he sent the same deal to six underwriters. “Three said yes and three said no,” he explained.

Like most of the others that spoke on the topic, Schaefer was in favor of a scoring model and he believes an automated underwriting system creates consistency when assessing risk. He was steadfast in his assertion though that humans had to be the last line of defense in fraud detection.

“We’ve got guarantors that have nothing to do with the business,” he said, offering an example of an applicant that was more than 80-years old, yet was passing themselves off as a hands-on construction worker.

“I’m still a big believer in the review and subjectivity,” he concluded.

Funding Circle’s Rana Mookherje expressed similar views. “[Humans] pick up things that an algorithm really can’t do,” he told the crowd.

“We have an experienced underwriter sitting there and calling every borrower that we give money to,” he added.

Mookherje said that their borrower profile differs from those that tend to use merchant cash advances. For instance, their average client has been in business for 10 years, does $2.2 million in annual revenue, and has 700 FICO. They also offer 1-5 year loans, where as merchant cash advance transactions tend to be satisfied in under twelve months.

Mookherje said that their borrower profile differs from those that tend to use merchant cash advances. For instance, their average client has been in business for 10 years, does $2.2 million in annual revenue, and has 700 FICO. They also offer 1-5 year loans, where as merchant cash advance transactions tend to be satisfied in under twelve months.

“If you need money in an hour, we’re not the right place for you,” Mookherje stated.

Funding Circle’s reliance on manual reviews may have to do with the loan terms being extended so long. Even Schaefer had said earlier, “I think it’s a lot easier to determine the behavior of a loan that’s less than twelve months as opposed to one that’s sixty months.”

But do other companies feel differently? Kabbage’s Alan Reeves said that 95% of their customers are 100% automated since there are merchants who get stuck trying to connect their bank account in the online application process.

When Kabbage was asked over a year ago how much of a role computers should play in the underwriting of a deal, COO Kathryn Petralia responded, “Huge.” She also went on to say then that, “it is not going to be like the “Matrix” where machines are making all the decisions. You won’t see an underwriting world without humans.”

It’s ironic however that while Alan Reeves was introduced at the conference as the Head of Risk Analytics, both the printed agenda and his LinkedIn profile cite his title as being the Head of Manual Underwriting. It’s a telling title for a company that is often heralded as the pinnacle of automation and computational decisioning.

But why can’t lenders simply give in entirely to the machines? Mookherje said at one point that, “those that live and die by their underwriting are going to be the ones that survive.” And if that’s the case, then relinquishing control to the computers perhaps risks the chance of death if things don’t work properly.

But humans, with all their natural flaws and imperfections pose the same risk. “Banks want to know that underwriting is consistent, that for any given customer, that you would underwrite them the same,” said Sam Graziano, CEO of Fundation. “And it’s not just having written policies and procedures,” he added. “But having programs in place to ensure these policies are upheld.”

The widespread dependence on humans to tie up loose ends in assessing risk may seem both practical and prudent, but to some traditional bankers, that system carries nightmarish implications.

Jim Salters, CEO of The Business Backer for example shared an experience his company went through years ago when trying to partner with a bank. Salters placed a high value on the manual review process, explaining that it was basically a strength of their core competency. The problem however, was that the bank said that would totally freak out their regulators.

The recurring message from the event’s panelists was that banks not only want, but may actually require a firm credit model to make decisions. They need to be able to explain to regulators why some loans got approved and others got declined in a perfectly uniform and consistent manner.

Schaefer and Reeves were aligned on the importance of consistency in underwriting. You basically can’t have a system where you arrive at three yeses and three nos on the same loan Schaefer explained.

Schaefer and Reeves were aligned on the importance of consistency in underwriting. You basically can’t have a system where you arrive at three yeses and three nos on the same loan Schaefer explained.

But building an automated system and telling the humans to take a hike isn’t an easy process. There’s a high upfront cost associated with development and it can take years to generate statistically relevant conclusions. And a multivariate decline issued by an algorithm can potentially worsen the customer experience, especially if the customer asks for the specific reason they were declined. Reeves said it can be difficult to explain to the customer that their FICO score was too low relative to their sales volume but that their FICO score on its own was good enough.

And yet once an automated underwriting system is developed, the cost of underwriting should drop significantly according to panelists. With that comes a decision consistency that the company can rely on and a system that bankers can get comfortable with.

But despite it all, Credit Junction CEO Michael Finklestein bluntly stated, “We’re never going to approve a $2 million loan with an algorithm.”

The unifying concept that everyone seemed to agree on was that although credit models were undeniably important, human review would remain a complementary part of the process for the foreseeable future at least in the commercial finance space.

“At the end of the day, it all comes down to underwriting,” said Mookherjee.

Less Regulated, Non-bank Lenders? Never Heard of ‘Em

July 20, 2015 Recently, two journalists for the Wall Street Journal sat down with Senator Chris Dodd and former Congressman Barney Frank to ask their thoughts about the Dodd Frank Act five years later.

Recently, two journalists for the Wall Street Journal sat down with Senator Chris Dodd and former Congressman Barney Frank to ask their thoughts about the Dodd Frank Act five years later.

The WSJ asked Frank specifically, “Do you have concerns that Dodd-Frank rules are driving more activity into the shadow banking system (less-regulated, nonbank lenders), sowing the seeds for a future crisis?”

The response…

Frank: “What activity? The law gives the regulators the power to regulate. When people tell you that activity has been moved to the shadow banking system, ask them what activity because I don’t know exactly what they’re talking about.”

One has to wonder what the awareness level was then when the Dodd Frank lawmakers drafted up Section 1071 to expand the Equal Credit Opportunity Act.

Meanwhile, Frank told me personally last year in a walking one-on-one in NYC that he supported transparency in business loan transactions, such that the borrower should be easily able to identify the terms. The premise behind consumer loan protections was that consumers were less sophisticated, he said. He also that he was not in favor of a federal cap on business loan interest rates.