Business Lending

Enova Surpasses $1 Billion in SMB Loans in a Single Quarter For First Time

October 23, 2024Enova’s small business loan arm had a huge 3rd quarter.

“Notably, for the first time in our history, we originated over $1 billion in small business loans, up 33% year-over-year and 14% sequentially,” said Enova CEO David Fisher during the company’s earning call. “The main drivers of this growth are consumer spending and confidence from small business owners in this current economy.”

Additionally, he said:

As discussed on our first quarter call, we identified opportunities within our SMB business that we believe would support continued strong growth with improved unit economics. We continue to see the benefits of this strategy in the third quarter as small business originations growth was strong, small business revenue yield continued to move higher sequentially and the small business quarterly net charge-off ratio remained on the low end of our expected range. Expectations for our future credit performance remained stable as the consolidated consumer and small business fair-value premiums were all largely unchanged from last quarter.

TikTok is Now Offering Business Financing

October 7, 2024 Add TikTok to the list of tech platforms offering business loans. TikTok Shop Capital is now “offering sellers access to fast and flexible business financing,” the company states on its website. Unsurprisingly, one of TikTok Shop’s partners is Parafin but the company also lists Storfund and Kanmon as funding partners. Storfund announced its deal with TikTok earlier today and said that its program would be called Daily Advance.

Add TikTok to the list of tech platforms offering business loans. TikTok Shop Capital is now “offering sellers access to fast and flexible business financing,” the company states on its website. Unsurprisingly, one of TikTok Shop’s partners is Parafin but the company also lists Storfund and Kanmon as funding partners. Storfund announced its deal with TikTok earlier today and said that its program would be called Daily Advance.

“TikTok is not a lender or loan broker,” the company website states. “TikTok partners with third-party lenders and financing providers to offer TikTok Shop sellers business financing options.”

The process works different depending on which solution a customer uses. For example, Storfund repayments are automatically debited from TikTok Shop payouts, Parafin repayments are automatically debited from the business bank account associated with TikTok Shop payouts, and Kanmon requires repayment via auto-pay deductions from the business bank account provided during the application process.

The Parafin option does not appear to be a standard merchant cash advance. TikTok says it would actually be a Parafin commercial flex loan issued by Celtic Bank. There is no credit check required for it.

TikTok’s foray into business financing is invite-only. “If a seller has an available pre-qualified and/or pre-approved offer, it will appear within Seller Center under the Finances tab,” the website says.

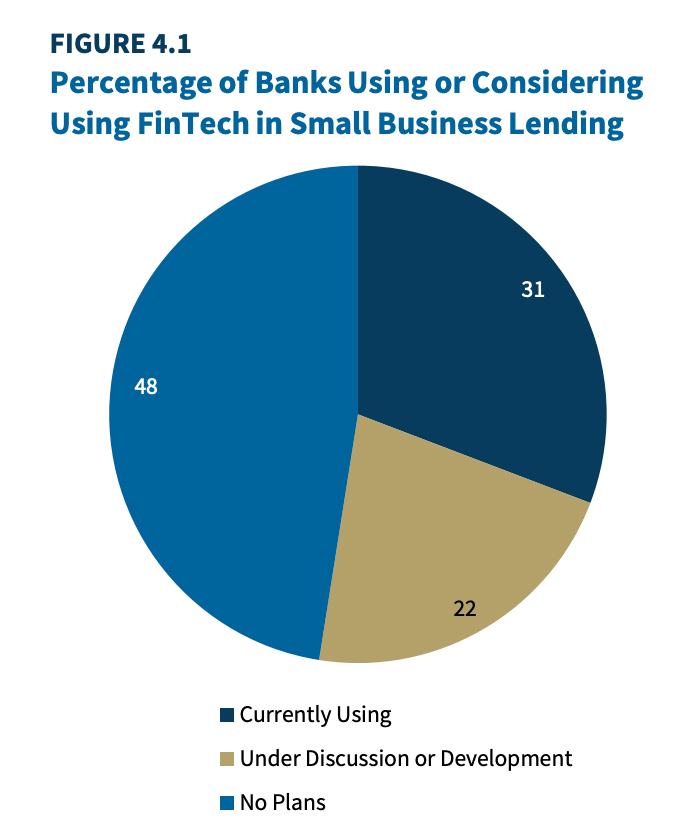

Only 10% of Banks Have a Credit-Scoring System That Can partially or Fully Automate Small Business Lending

October 3, 2024If you thought that fintech had already largely come in and revolutionized the lending process at banks, you’d be wrong. According to the FDIC’s latest annual small business lending report, only 10% of banks have a credit-scoring system that can partially or fully automate the underwriting of some non-credit-card lending. Further, only 3% of banks use a credit-scoring system to auto-approve loans and less than 1% will auto-approve a loan of $250,000.

When it comes to fintech, “banks most commonly use fintech to help with regulatory compliance and for steps taken after loan approval,” the report says, “such as closing, performance and servicing, and portfolio analytics.”

Still, that doesn’t mean they’re terribly slow. In fact, thirty percent of banks can approve a small and simple business loan within one business day and 75% of of banks can approve one within five business days, though approvals usually happen within ten days on average.

And just because a bank’s business loan operation isn’t fully automated doesn’t necessarily mean they’re at a disadvantage competitively because banks actually tend to view the personal relationship with their small business loan customers as one of their core advantages.

“Banks use and high value branch locations and on-site visits as ways to generate and maintain small business lending relationships,” the report says. “About four in five banks define their geographic market for small business lending based on their branch footprint and, on average, their market extends 40 miles from their branch locations.”

“Very few banks allow borrowers to complete a loan application entirely through an online portal,” it adds. And that’s by design apparently. Of the banks surveyed for the report, almost half of them said they had NO PLANS to use or CONSIDER fintech in small business lending.

There’s a lot more insight in the full report that you can view here.

Photos From B2B Finance Expo and More

September 30, 2024

Photos from B2B Finance Expo can be FOUND HERE. The order of them arranges at random. We’re still adding a few to the gallery. If you want a higher res version of a photo or to inquire if there are any of you that may not be here, email events@debanked.com. Video interviews from the red carpet or from the trade show floor will start being added over the next couple days and should take up to 2 weeks to get them all up. There is a ton of video content!

Congratulations to Cesar Valero (pictured at right), Business Development Exec of Spartan Capital on his victory at the event’s official poker tournament! Story on this to follow! Second place went to Erica Bell, Business Development Exec at Tax Guard. The final table of the match was HIGH PRESSURE so if you want to know how they got so good at the game, make sure to give them a buzz.

Congratulations to Cesar Valero (pictured at right), Business Development Exec of Spartan Capital on his victory at the event’s official poker tournament! Story on this to follow! Second place went to Erica Bell, Business Development Exec at Tax Guard. The final table of the match was HIGH PRESSURE so if you want to know how they got so good at the game, make sure to give them a buzz.B2B Finance Expo was a two-day event in Las Vegas that brought folks together from across the fintech and commercial finance industries.

Special thanks goes out to Greg Smith and Steve McLaughlin of FT Partners for their incredible insights on Day 1. Proceeds from the event will benefit the Small Business Finance Association (SBFA). A thank you to all the sponsors and attendees.

Applicant Didn’t Complete their Business Loan Application? They Might’ve Gotten Stuck

September 26, 2024 “Early discovery showed us in the market that over 85% of [small business] loan application packets were straight up abandoned,” said Jay Long, COO and co-founder of Parlay.

“Early discovery showed us in the market that over 85% of [small business] loan application packets were straight up abandoned,” said Jay Long, COO and co-founder of Parlay.

In an era where fintechs have sought to increase the speed and accuracy of the underwriting process, Parlay, an AI-native SaaS company, noticed that one major lingering challenge for small business lenders starts well before today’s tech stacks even come into play. For example, an applicant might not be sure what they’re supposed to be submitting to the lender in the first place and thus the process may never even make it to the fintech underwriting stage. This bottleneck comes at a cost for both a lender who fails to move a loan application forward and for a borrower who gets stuck and isn’t able to get what they wanted.

“A lot of small businesses when you request a bunch of stuff in an email or you just say ‘give me these things,’ they may not have the financial background, that financial education to know how to answer those questions,” said Alexandra McLeod, CEO and co-founder of Parlay. “And so what we’ve done is we’ve built a series of really intuitive, user-friendly, plain-English workflows that are easy and rapid to get through but also systematic.”

Parlay’s Loan Intelligence System (LIS) was drawn from interviews with hundreds of small businesses and also by observing how they did with existing workflows.

“We’re asking them yes-no questions, and based on how they answer, then the questions arrange themselves in a specific way,” said McLeod. “But also, we have tool tips in the platform, so if somebody doesn’t know what a term is or if they need help building something—like a debt schedule is something they have to provide, and people don’t know how to generate those, then we have these builders in the workflows to help them with that.”

At present, Parlay is focused on SBA 7(a) loans with their most common customer being a community bank or credit union. The company’s focus on the intake process has also enabled their technology to do even more, and that is to nurture applicants that are not eligible for approval to eventually become eligible through personalized actionable recommendations.

According to Parlay, their LIS easily integrates with existing Loan Origination Systems and it improves profitability without increasing overall business risk.

For McLeod, who has a prior background with financial inclusion initiatives and startups, she’s seen firsthand that there are financial institutions eager to provide capital to the underserved but that the economics to do it with legacy systems at scale have just made it too cost prohibitive. “The other side of the problem is the small business needs more hand holding,” said McLeod, “and the lender can’t provide it. And so this is a perfect application of technology where you can offer a scalable alternative where you can handhold the small business, you can provide a lot more insight to the lender as to the needs of those small businesses and you can generate that outcome of more booked loans because more people can actually get through the process.”

Notably, Parlay is a recent graduate of the Center for Accelerating Financial Equity (CAFE) Fintech Accelerator Program, which supports fintechs advancing health & wellness of underserved populations. CAFE is headquartered in the Fintech Innovation Hub building on University of Delaware’s STAR Campus, a building deBanked covered in 2022.

Business Finance Companies on Inc 5000 List in 2024

August 13, 2024Here’s where small business finance companies rank on the Inc 5000 list for 2024:

| Company Name | Ranking | Growth |

| Clara Capital | 158 | 2,295% |

| 4 Pillar Funding | 251 | 1,620% |

| Fundible | 254 | 1,611% |

| Byzfunder | 303 | 1,404% |

| Valiant Business Lending | 337 | 1,286% |

| CapFront | 541 | 792% |

| SellersFi | 974 | 523% |

| SBG Funding | 1,158 | 443% |

| Splash Advance | 1,238 | 418% |

| Channel | 1,330 | 389% |

| iAdvance Now | 1,421 | 362% |

| Flexibility Capital | 1,513 | 342% |

| eCapital | 1,968 | 265% |

| Kapitus | 2,025 | 258% |

| Merchant Industry | 2,057 | 254% |

| ApplePie Capital | 2,265 | 230% |

| Backd | 2,282 | 228% |

| Capital Source Group | 2,306 | 226% |

| Direct Funding Now | 2,323 | 225% |

| Expansion Capital Group | 2,829 | 179% |

| Fora Financial | 3,560 | 134% |

| Percent | 4,047 | 111% |

| Smarter Equipment Finance | 4,566 | 89% |

| Gateway Commercial Finance | 4,598 | 88% |

Did we forget you?! Let us know at info@debanked.com and we’ll add you.

Square Funds $1.14B in Q3

November 5, 2022 Square Loans, a subsidiary of Block, originated 126,000 loans for a total of $1.14B in Q3. The company has a positive outlook on the state of its lending business, saying that “Square Loans achieved strong revenue and gross profit growth during the third quarter of 2022.” Overall, originations grew by more than 10% over the previous quarter.

Square Loans, a subsidiary of Block, originated 126,000 loans for a total of $1.14B in Q3. The company has a positive outlook on the state of its lending business, saying that “Square Loans achieved strong revenue and gross profit growth during the third quarter of 2022.” Overall, originations grew by more than 10% over the previous quarter.

Square Loans is one of several lenders thriving during this period of economic uncertainty. Rivals Enova and Shopify Capital also recently reported strong business loan results.

National Funding is Venturing into Automated Lending

November 3, 2022 National Funding did more than just survive the pandemic. Already in 2022 the company upsized its credit facility, invested in Finova Capital, closed on a $125M ABS, and now more recently is going full force into automated lending.

National Funding did more than just survive the pandemic. Already in 2022 the company upsized its credit facility, invested in Finova Capital, closed on a $125M ABS, and now more recently is going full force into automated lending.

The new initiative that aims to build off of National Funding’s 20 years of experience will be led by Rob Rosenblatt, a seasoned fintech veteran that previously worked for American Express, Chase, Citi, Kabbage, and Behalf.

National Funding will still do business as it has previously but Rosenblatt said that his separate division, formally organized as Business Loan Center, LLC, will differ in that it will be fully digital to the point that borrowers won’t have to engage with a human being if they don’t want to when accessing capital. The self-serve automated experience that takes a customer from application to approval in a matter of minutes is admittedly not a new concept in that of itself, Rosenblatt concedes, but he believes National Funding is equipped to do it better than the rest.

“…what we hope to do that’s unique is, first of all, leverage all of the learnings that National Funding has because they’ve been in business for over 20 years,” Rosenblatt said. “Number two is create a superior technological experience which will help with speed and user experience because we’re brand new, so we won’t in any way be beholden to systems of the past. Third is really be aggressive in our use of alternative data.”

Rosenblatt also emphasized that they will create a “world class user experience” and he expressed his belief that there is more than ample room for a new player to enter this market.

“Dave Gilbert, the founder of National Funding, and Joe Gaudio, who’s the president and COO, they became in the course of our conversations very firmly convinced that there’s a huge opportunity to better serve large swaths of the small business universe that maybe today aren’t quite being served fully by the suite of products that are out there,” Rosenblatt said.