Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate

How Banks Are Coming Back to SME Lending (Summary)

March 6, 2017

The banks are no longer sitting on the sidelines of small business lending. At LendIt on Monday, a panel featuring representatives from two of the biggest banks in the country, reminded young upstarts that they intended to be the primary capital sources for small businesses.

Unlike JPMorgan Chase, which partnered with OnDeck, Bank of America (BoA) decided to build the technology to deliver loans easily and quickly on their own. BoA SVP Nadeem Tufail said that reputational risk had held them back from partnering with a platform back when they were considering it years ago. “We couldn’t make that leap,” he explained, citing factors like cost, which they saw as simply being too high on some platforms to feel comfortable with.

But that doesn’t mean that the opportunity has passed them by. “A Bank of America customer can get funded in 48 hours,” Tufail proclaimed, while adding that a business that doesn’t bank with them can get a loan from them in about 7 days. The bank is also now doing fully automated approvals on a very small scale with a sliver of their best clientele to test the concept.

Meanwhile, Julie Chen Kimmerling, Senior Manager at Chase, made it a point to say that they were also really worried about things like reputational risk but that they found OnDeck to be a perfect fit. The maturity of their management team and platform really impressed them, she said. Still, Chase governs how the loans are underwritten and keeps the customers on their balance sheet. So they haven’t exactly handed the keys over to OnDeck but obviously trust their brand to be affiliated.

BoA recognized that some of their customers were telling them that they shouldn’t have to submit all these documents when the bank should already have access to their financial histories, particularly their cash flow. Tufail said that this was one of the most important factors in their underwriting. “Does the business have cash flow?” he said. “Does the business have liquidity?” The bank should already be able to evaluate these metrics.

“We certainly have an advantage with transactional level data,” Chase’s Kimmerling said of banks doing loan underwriting. And Chase is no amateur in this market. Kimmerling said that her bank had provided $24 billion of credit to US small businesses last year alone, a figure prominently displayed in their last earnings report.

To boot, both banks retain brick & mortar presences around the country, an advantage for small business customers, who they say are pretty likely to visit a branch.

The banks it seems are coming back. Lendio CEO Brock Blake moderated the panel.

Quotes and paraphrases were derived from the panel. The summary is my own analysis of it.

With Clock Ticking, Members of the Commercial Finance Coalition Journeyed to the New York State Capitol

March 5, 2017 With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

“It could destroy the industry if the worst comes to fruition,” declared Robert Cook, a partner at Hudson Cook LLP, who was speaking in reference to the proposal. The industry not only employs thousands of people in New York State but also provides much-needed capital to small businesses there. The CFC says that their members injected more than $50 million into New York businesses just last year alone.

Several law firms who have written about the proposal have used words like could, may and likely to explain what will happen, in part because it seems as though no one’s really sure. CFC members worry that the proper research hasn’t been done, especially when there hasn’t been any engagement with them. “They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director.

As the clock ticked down, the CFC’s two-day effort in the capitol building played out like a scene from a movie.

Are you aware of Part EE of the TED Bill?

This is what we do…

No, nobody from the Department of Financial Services has even talked to us

No, we’re not kidding

And on it went…

Gans says the CFC is looking for additional companies in the small business financing industry to support their efforts. He’ll be at the LendIt Conference. “I would be happy to meet with anyone interested in joining the CFC and helping us fight this misguided policy that is also attending,” he said. He can be contacted at dgans@polariswdc.com.

The budget deadline in New York State is March 31st.

Letter From the Editor – Jan/Feb 2017

March 4, 2017When deBanked first launched online in 2010, I thought it was too late, that perhaps all the exciting changes in alternative finance had already taken place and that aside from a few obsessed geeks, there wasn’t that big of an audience to write for. It certainly felt a bit out-of-style, especially since I had been working in the industry for more than four years by that point. The only publication that was dedicated to the scene at the time had already come in to the public eye and vanished. Many alternative financial companies had met the same fate, thanks to the financial crisis.

In a way, deBanked started off as a post-apocalyptic diary, an accounting of the industry’s survivors and their roles in the new world order. Primitive, my reporting may have been then, but interest quickly grew. By mid-2011, I was already forced to change web hosts to keep the website from slowing down. In my day job as a commercial finance broker, I continued to talk to small business owners all the over the country about a common theme, that banks just weren’t lending. And maybe they never would again, some predicted anyway. Or maybe the way loans were made in general would just never be the same.

Looking back among my old 2011 stories, I discovered that I had written a personalized review of Square’s payment technology and had given it high marks. Back then however, I saw Square as a payments toy. It was innovative and sexy, but unrelated to lending. Fast-forward to 2016 and Square’s capabilities have expanded. I should know, they funded my business exactly five years after my review. In this issue, I’ll walk you through what it was like to play the role of borrower, and put marketplace lending up to the ultimate test. Thanks to Square Capital, my journey has come full circle or more appropriately, full square.

This issue is the first of 2017. For alternative finance, it fortuitously feels like the beginning, not the end. If our descendants far in the future stumble upon these stories, I pray they will enjoy our accounts of the transformation, when entrepreneurs dared to look at the world in front of them and boldly decided to change it. It was the early 21st century, historians will say, when mankind dared to de-bank and change everything we knew about finance. In the here and now, you are a part of it all…

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

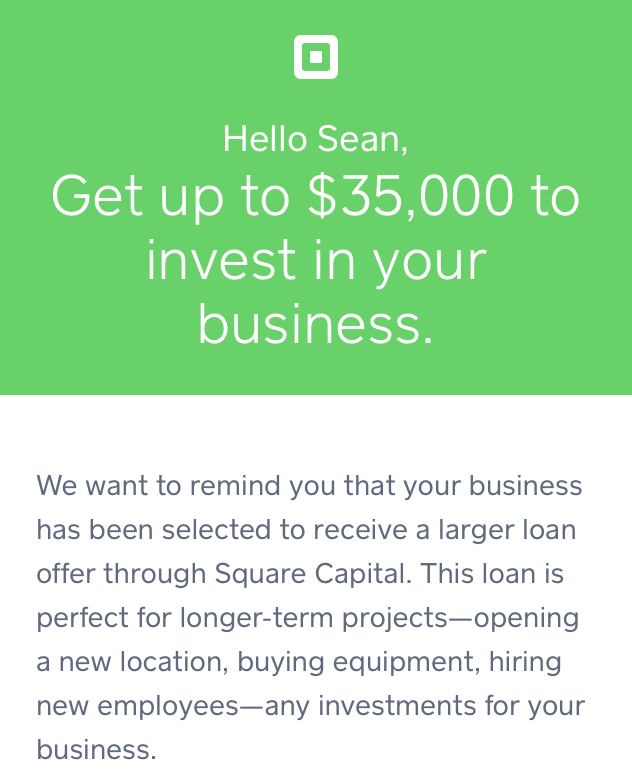

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

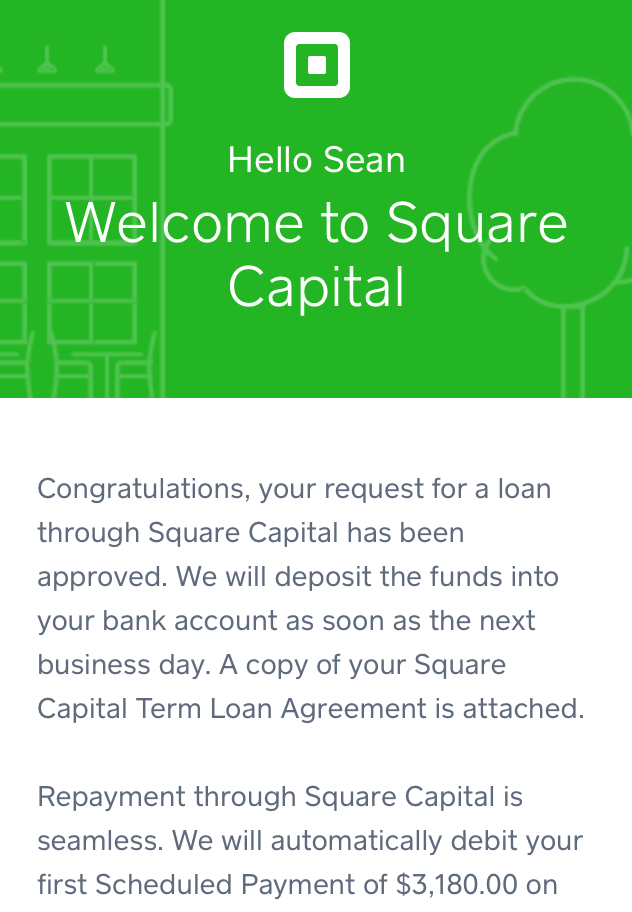

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

See You At LendIt

March 3, 2017Monday kicks off the LendIt conference at the Javits Center in NYC. Given that it’s the biggest event of the year for the industry, I certainly hope to meet as much of you there as possible.

If you still haven’t registered, make sure you at least take advantage of a 15% discount by using promo code: Debanked17USA. My schedule is pretty booked up, fueled in part by the excellent session topics this year which I want to catch a bunch of. That being the case, I am potentially available to get together even on Sunday or Wednesday (since I live in Manhattan) or any other day outside of the conference.

I hope you enjoy LendIt. You should check out their story of how they came to be HERE.

Letter From The Editor – Mar/Apr 2017

March 1, 2017Out of the many lenders and marketplaces that reported their 2016 earnings in the last month, several didn’t look so good. If algorithms and branchless-finance was supposed to make lending so much more efficient, why is it that so many online lenders are struggling to make a pro t?

As it would turn out, banks were not as doomed or as outdated as the technologists characterized them to be. Their cost of capital and brand name recognition (for most of them anyway) is proving very tough to compete with. In this issue we explore the latest trend, the drift back towards banking. That doesn’t mean that we are returning to a purely bank-dominated lending universe, however. On the contrary, it’s mainly the prime borrower market that banks are working to service better. There’s an entire segment out there for which bank financing is not the answer, at least not yet, and there’s plenty of exciting events taking place.

For small business owners, some still want a relationship with the person helping them obtain capital, they just want it in a different way. In the last few months, we spoke with several professionals who attest to having a text-based relationship with their clients, as in they communicate back and forth through their phones over text.

When I first heard about this, I assumed it had to be a one-off. “Wait, your applicants text you for updates with the underwriting process?” I asked a sales representative who seemed stunned that I would think that was odd. After a quick poll of other salespeople at a conference, the truth became clear to me. If you don’t attempt to have a text relationship with your clients, you might be at a disadvantage. In this issue, we explore why that might be.

And on that note, RU ready 4 this issue? Cuz I g2g so ttyl. Thx. ![]()

–Sean Murray

Prosper, A Marketplace for the World’s Richest Banks and Billionaires?

February 28, 2017

Credit Suisse, Deutsche Bank, Goldman Sachs, Morgan Stanley, and funds tied to some of the world’s richest billionaires (including George Soros) all make up the “consortium of institutional investors” and “syndicate of lenders” involved in Prosper’s recently announced landmark deal. The terms allow for the investors to purchase up to $5 billion of loans on the platform while the lenders will provide warehouse financing up to $1 billion. It’s safe to say that this is not your father’s peer-to-peer lender.

The WSJ reported too that investors will receive warrants to buy equity in Prosper that’s tied to the amount of loans they buy, all the way up to 35% of the company if they buy the full $5 billion.

Prosper used to call itself a “peer-to-peer lending marketplace” but these days it’s adopted a slightly different label, “consumer lending marketplace.”

Back in July, I half-jokingly scoffed at the phrase marketplace lending as the industry had begun to call itself, seeing that it was morphing into just Wall Street lending after Goldman Sachs announced it would actually be launching an online consumer lending arm to compete against Lending Club and Prosper.

The deal is obviously great for Prosper, whose future seemed kind of up in the air, but it’s hard to get excited about the world’s biggest banks and richest funds now being the consortium behind an online lender who pioneered peer-to-peer lending, if things like peer-to-peer lending excited you.

To be fair, peers/retail investors can still invest on the platform too so I guess there’s that.