Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

More Small Businesses Seeking Merchant Cash Advances Than Factoring

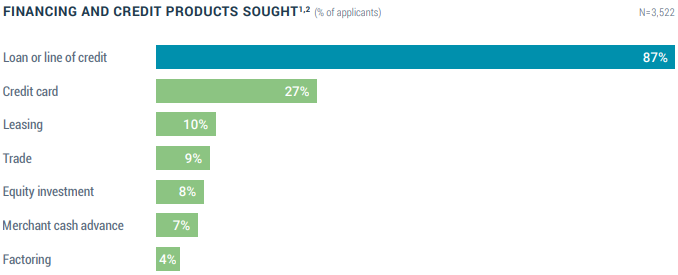

May 23, 2018 Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Auto and equipment loans had the highest approval rates among all financing options available to small businesses, at 82%. Merchant cash advances followed behind them at 79%. Lines of credit and business loans carried approval rates of 69% and 62% respectively. SBA loans came in at 54%.

When it comes to satisfaction, online lenders such as Lending Club, OnDeck, CAN Capital, and PayPal, have markedly improved over time, the report shows. The net satisfaction score of online lenders has increased from 19% in 2015 to 35% in 2017.

On transparency, online lenders rank at about the same level as large banks, though applicants were more likely to be dissatisfied with the interest rates of an online lender and the long and difficult application process with a large bank.

Missed Broker Fair? Get the Kit and Presentations

May 21, 2018

If you missed Broker Fair, you can still get your hands on some of the gear and the presentations. Simply email info@brokerfair.org and ask to be shipped a copy of the Broker Fair Kit. The accessories, which will only be provided while supplies last, include a USB drive with the day’s presentations, a Broker Fair bag, a Broker Fair shirt, a deBanked magazine, a Broker Fair handbook, and more.

Also, don’t wait too late to REGISTER for deBanked’s half-day event in San Diego on October 4th. deBanked Connect: San Diego will connect funders, brokers, and folks from the industry for networking and cocktails!

Broker Fair 2018 Story Continued

May 18, 2018A continuation of Broker Fair 2018 through photos:

We’ll publish the entire cache of them in the coming weeks.

JOIN US OCTOBER 4TH IN SAN DIEGO AT THE ANDAZ FOR A SPECIAL HALF-DAY INDUSTRY NETWORKING EVENT

Couldn’t find yourself in any of our photos? We’ll publish the full album in the following weeks.

The Broker Fair 2018 Story Through Photos

May 18, 2018Broker Fair 2018 was an amazing day of inspiration, education, and opportunities. We’ve posted some of our photo footage below:

JOIN US OCTOBER 4TH IN SAN DIEGO AT THE ANDAZ FOR A SPECIAL HALF-DAY INDUSTRY NETWORKING EVENT

Couldn’t find yourself in any of our photos? We’ll publish the full album in the following weeks.

Broker Fair 2018 Pre-Show Photos

May 17, 2018Photos from the Broker Fair 2018 May 13th Pre-show party at The William Vale in the Vale Garden Residence. Photos from the conference will be published separately. We hope you had fun.

Welcome to Broker Fair

May 13, 2018Update: Thanks to everyone who attended, participated, and sponsored!

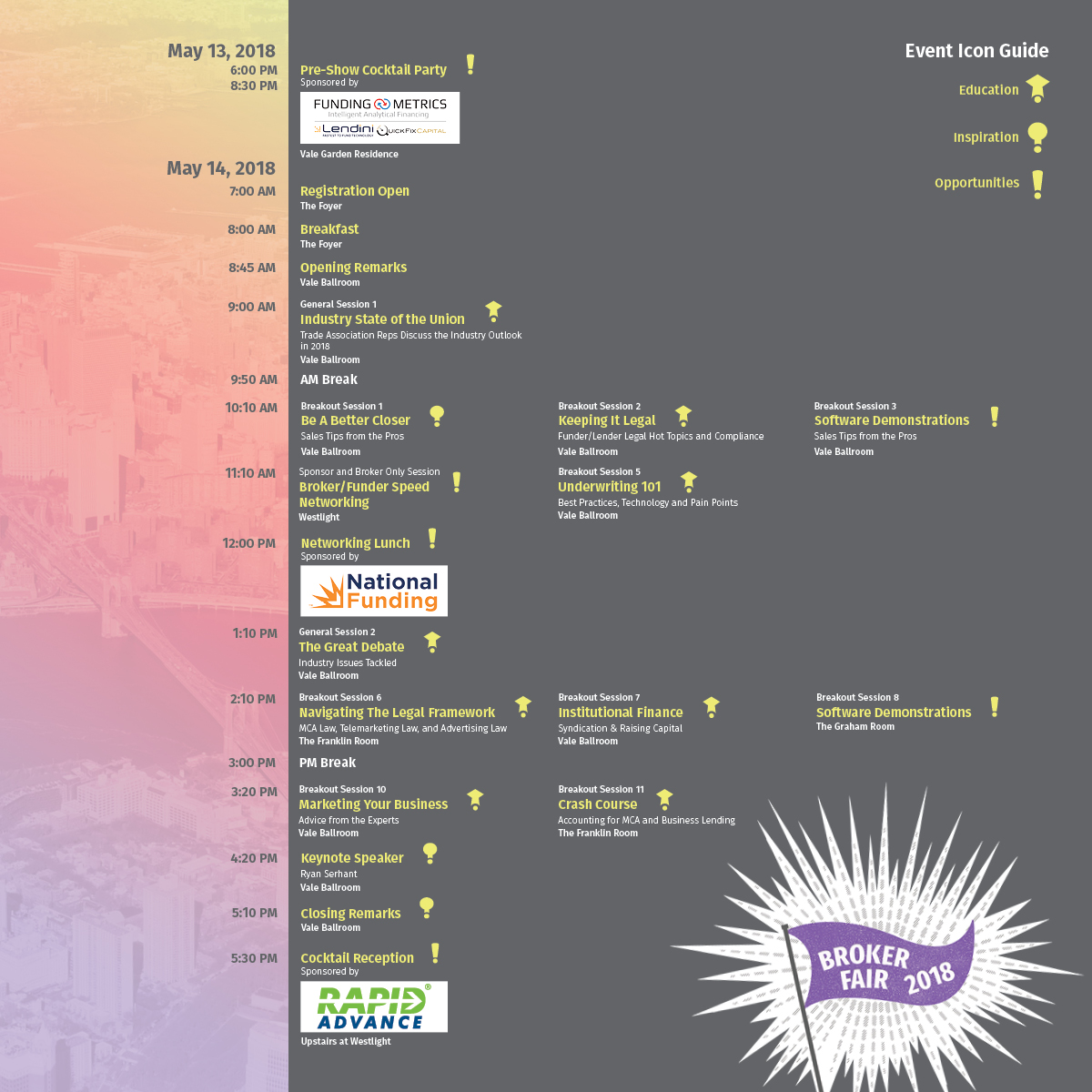

Registration on Monday starts at 7am where you will be able to pick up your badge. The continental breakfast will be available at 8am and the opening remarks begin at 8:45am.

Registration on Monday starts at 7am where you will be able to pick up your badge. The continental breakfast will be available at 8am and the opening remarks begin at 8:45am.

The lunch, sponsored by National Funding, begins at 12. There will be a kosher option available.

Later at the end of the day, the cocktail reception at Westlight, which is upstairs on the 22nd floor, will begin at 5:30pm. Westlight offers amazing outdoor views of the Manhattan skyline. That event is sponsored by RapidAdvance and all you need to enter is your Broker Fair badge.

The agenda will also be available on the backside of your badge.

Thank you also to our Gold Sponsors: National Business Capital, CFG Merchant Solutions, BFS Capital, and CanaCap

California Commercial Financing Disclosures Bill Still a Work in Progress

May 8, 2018 SB-1235, a bill that would require APR disclosures on all types of commercial financing products transacted in California (including some types of factoring, leasing, and merchant cash advance), survived the Judiciary Committee hearing on Tuesday. The bill was previously debated by the Senate Committee on Banking and Financial Institutions, where key provisions like a uniform APR disclosure came under fire.

SB-1235, a bill that would require APR disclosures on all types of commercial financing products transacted in California (including some types of factoring, leasing, and merchant cash advance), survived the Judiciary Committee hearing on Tuesday. The bill was previously debated by the Senate Committee on Banking and Financial Institutions, where key provisions like a uniform APR disclosure came under fire.

Since then, Senator Steve Glazer, the bill’s author, is now proposing an alternative Annualized Cost of Capital metric rather than an Annual Percentage Rate in an attempt to compromise with the opposition that says the metric will not work for non-lending products.

On Tuesday, two trade association representatives continued to press their case for a collaborative solution that would work best for all parties, especially small businesses.

Scott Riehl, VP, State Government Relations at the Equipment Leasing and Finance Association (ELFA) said that his association, whose members include Caterpillar and Hewlett Packard, was not on board with the bill as currently drafted. No one in the financial community has ever even heard of the term Annualized Cost of Capital, Riehl said.

Katherine Fisher, Partner at Hudson Cook, LLP, who was there on behalf of the Commercial Finance Coalition, testified that it would not be possible to calculate an annualized rate when the timeframe of products like factoring and merchant cash advances were indeterminate.

Judiciary Committee Chairwoman Hanna-Beth Jackson wrapped up the lively debate by saying that ultimately California “wants a robust small business community” after several of her committee members voiced concerns that the bill in its current form could potentially deter commercial finance companies from providing capital in their state.

The hearing concluded with only 3 aye votes, putting the bill “on call,” wherein no decision was formally reached.

Update: Before the close of the day, the committee secured a 4th aye vote, pushing the bill forward.

Online Lender Turns to Bachelorette Star to Promote Loans

April 26, 2018Will you accept this rose…err..loan?

Joelle “JoJo” Fletcher has come a long way since her 2016 season on The Bachelorette where she found love with Jordan Rodgers, the younger brother of Green Bay Packers quarterback Aaron Rodgers. The couple is still together and JoJo is now a spokesperson for Marcus, the online consumer lending arm of Goldman Sachs. In the TV advertisement, which you can click to watch below, she explains why Marcus is the way to go if you need financing for home improvement.

ABC seems to produce the best TV celebrities for online lenders. Three judges on Shark Tank, which is also an ABC show, have all been spokespeople for online lenders.

Barbara Corcoran – OnDeck

Lori Greiner – Kabbage

Kevin O’Leary – IOU Financial

While JoJo herself is no shark, The Bachelorette/Bachelor franchise is the number one reality program — among adults 18-49 living in homes with $100,000+ annual income, a demographic that Marcus is undoubtedly targeting.

Full disclosure: I watched the two seasons that JoJo was on in their entirety.