Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

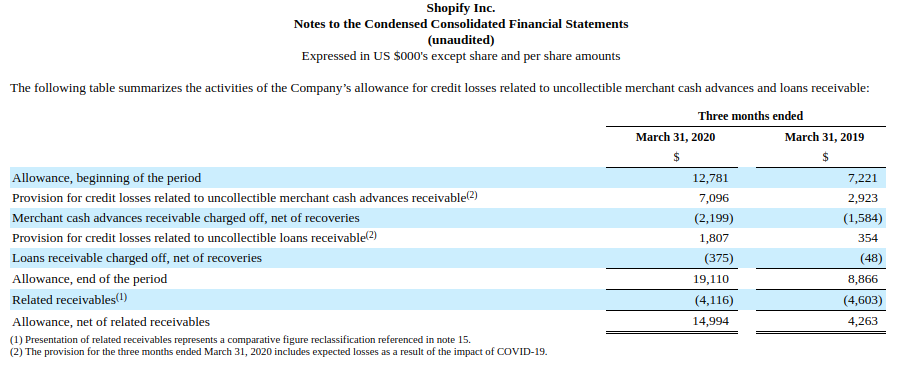

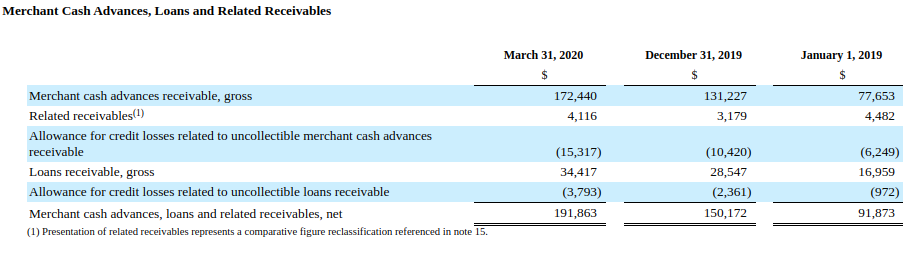

Shopify Shows Strength in Q1 Results, Issues $162.4M in MCAs and Loans

May 6, 2020eCommerce platform Shopify, 2nd only to Amazon in retail eCommerce sales, issued $162.4M in merchant cash advances and business loans in Q1, up from $115.9M in the previous quarter. The statistic pushed them past the $1 billion threshold of funds cumulatively issued since inception.

The company’s provision and allowance for loan losses ticked up from significantly from the same period the prior year but Shopify at that time was originating 50% less volume.

The company reported a GAAP net loss of $31.4M on $470M in revenue. Shopify also has approximately $2.36B in cash and cash equivalents on its balance sheet.

The company reported an increase of monthly recurring revenue, thanks to an increase in the number of merchants joining the platform, strong app growth, and Shopify Plus fee revenue growth.

Shares of Shopify (NYSE: Shop) jumped by more than 5% after the announcement.

Round Two of PPP Is Targeting Much Smaller Businesses

May 4, 2020 $79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

$79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

Though the pause button for big lenders was only in effect for eight hours that day, it was recognition that the playing field had not been level in the first round. JPMorgan Chase, the largest lender in round 1, for example, had an average PPP loan size of $515,304 in that round.

It’s a competitive process for limited dollars. 5,400 direct PPP lenders have already participated in the second round. More than 80% of those have less than $1 billion in assets. Senator Marco Rubio, a champion of PPP, called the latest figures released by the SBA as “all good news.”

Square Capital, meanwhile, has taken small to the extreme. Their average PPP loan approval as of April 29th was just $16,000, according to stats published by Square Capital head Jackie Reses on twitter. But only 2,711 of the 38,000+ approved had received the funds so far.

Still, that average is significantly smaller than the average loan size of $73,000 approved by Ready Capital in Round 1, a non-bank lender that got widespread attention for approving more PPP loans than any other lender in the country. Those record-breaking numbers, however, led to delays in borrowers receiving their funds to the point where as of April 30th, the responsibility of funding those loans had reportedly transferred to Customers Bank.

OnDeck has also played a role in the PPP, though only as an agent despite being approved by the SBA to lend. That news, which was revealed last week in the company’s quarterly earnings call, is likely due to the company’s current predicament brought on by government-mandated shutdowns.

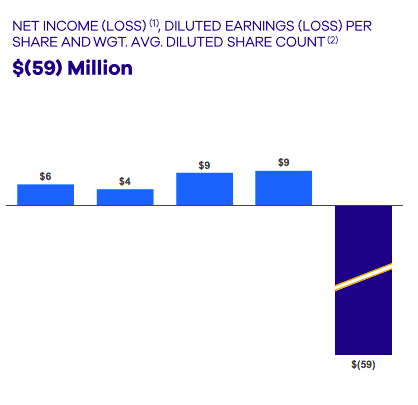

OnDeck Reports Q1 Net Loss of $59M, Suspends Non-PPP Lending Activities

April 30, 2020O nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

The company has also suspended its pursuit of a bank charter. The company has instituted a 15% pay reduction for its full-time employees, a 60% pay reduction for part-time employees, and furloughed additional employees that will receive benefits but no salary. OnDeck CEO Noah Breslow and members of the Board took a 30% pay reduction.

The company said that PPP funding has not really reached real small businesses like the ones they serve and as such only a handful of their customers have received PPP funds. While OnDeck is approved to operate as a PPP lender themselves, they have been acting as an agent of them in the interim and will dedicated their resources almost entirely to this endeavor. The company anticipates that originations of its own products could contract by 80% or more in Q2.

The company has not tripped any covenants or triggers with its own lenders as of yet but is currently in discussions with them on a path forward in this environment.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

Noah Breslow, chief executive officer, is quoted in the announcement:

“In the span of several weeks, the spread of COVID-19 led to government-mandated lockdowns for small businesses both in the US and globally, placing our customers under unprecedented economic stress.After a successful and rapid transition to remote work, we effected immediate changes to our business to preserve liquidity, support our customer base, manage our loan portfolio and reduce costs. With an uncertain timetable for the reopening of the economy, and the effectiveness of government stimulus for small businesses unclear, we will be reducing debt balances in the second quarter and focusing on managing our portfolio, delivering government stimulus to our customer base and ensuring the company has the runway to scale operations again when the economy reopens.”

The company fully utilized its initial $50 million share repurchase authorization in the first quarter of 2020. On February 10, 2020, the Board authorized the company to repurchase up to an additional $50 million of common shares, and the company has approximately $23 million of remaining capacity under that authorization. The company suspended share repurchases late February but maintains authorization to resume purchases at its sole discretion.

For 2020, OnDeck expects:

- Portfolio contraction reflecting an 80% or more reduction in second quarter origination volume

- Increased delinquency and charge-offs stemming from COVID-related economic deterioration

- Reduced Net Interest Margin reflecting a lower portfolio yield

- Reduced operating expenses, on pace to cut second quarter expenses by approximately 25%.

The company had been on a modestly positive trajectory as of year-end 2019.

The company’s stock had a somewhat minor rally on Wednesday, closing at $1.61. That’s still substantially down from where it stood on February 20th at $4.22. It hit a low of 66 cents on March 18th. The share price dropped by nearly 19% after earnings were released on Thursday morning.

This story will be updated as the information becomes available.

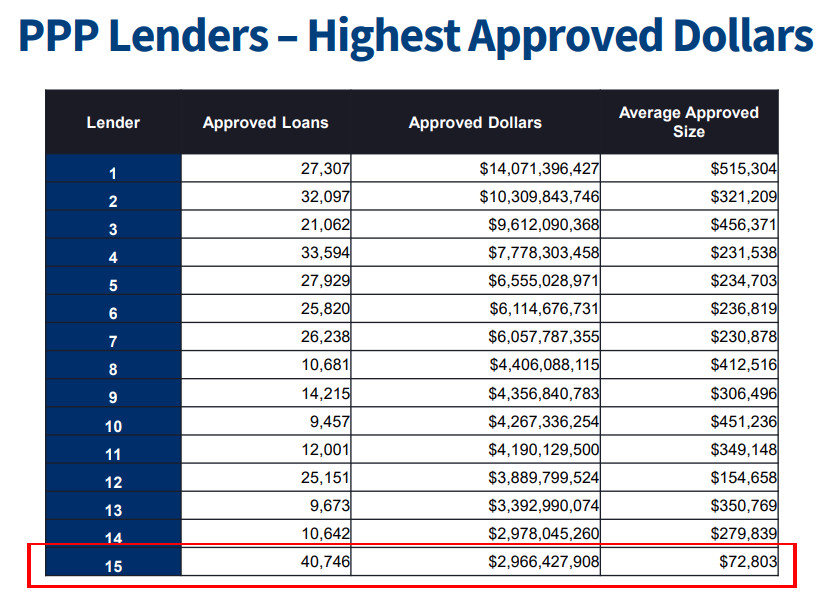

Ready Capital Was The Biggest PPP Lender By Volume in Round 1 of PPP Funding

April 22, 2020 Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

“As a leading non-bank, SBA lender, there’s 14 of us, we’re number two in terms of originations last year,” Capasse said on Fox Business, “we focused broadly, we don’t have deposit relationships, so we open our doors broadly to in particular the smaller mom and pop, the local deli, the pizzeria, the nail salon, so just in terms of the numbers, round one of the PPP, we approved 40,000 loans which is number one in the US, it was about $3 billion in total approvals. And our average balance was only $73,000 versus $230,000 for the average in round one.”

Among Ready Capital’s channels for acquiring PPP loan applications is Lendio, who reported consistent figures (a rough average of $80,000 per PPP loan facilitated), and high volume. Lendio has said on social media that they have been working with several partners, Ready Capital among them.

Ready Capital’s Capasse reasoned that their speed could probably be attributed to an affiliated fintech lender. “We are maybe more efficient than some of the banks because we have an affiliated fintech lender which is able to create online portals and processes to work in a more efficient manner and that enabled us to not only process these loans more efficiently but also to provide broad access to the program, to the smaller business owners.”

The company acquired Knight Capital, a small business finance provider, late last year.

Small Business Group Advocates For Community Anchor Loan Program (CAP) In Wake Of PPP Wind Down and Possible Refresh

April 17, 2020 At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

Congress is considering another round of additional PPP funding but Americans may be worrying that such funds will once again go into the hands of some of America’s largest chains. (44.5% of the $349B PPP funds went toward loans over $1 million)

Outspoken successful businessman Mark Cuban has proposed a solution, a lottery system next time around to improve the chances that smaller businesses get their share of the pie. While the public debates the merits of such an approach, one organization (the SBFA) is calling for something much more direct, a targeted fix via a Community Anchor Loan Program (CAP) that would appropriate $10 billion for businesses that were PPP-eligible for loans under $75,000 but did not receive funds.

Deployment of this capital under CAP can and should be administered by non-bank alternative lenders with proven success with this particular small business market, they say.

The proposal also calls for 25% of the funds to specifically be allocated for minority, women, and veteran-owned and agricultural businesses.

In a letter the SBFA submitted to Congress earlier this week, the organization said:

“Women and minority-owned businesses are historically smaller and employ fewer people and, in some communities, are under-banked without the established relationships required to secure a PPP loan. Small farms and agricultural businesses are important to communities and often have trouble qualifying for traditional financing.”

The Small Business Finance Association is a non-profit advocacy organization whose mission “is to take a leadership role in ensuring that small businesses have access to the capital they need to grow and thrive.”

That’s All Folks? – The PPP Money Is Already Gone

April 15, 2020

Update 4/16/20: The SBA has put up an official statement on its website that says “The SBA is currently unable to accept new applications for the Paycheck Protection Program based on available appropriations funding. Similarly, we are unable to enroll new PPP lenders at this time.”

A number of fintech companies have just joined the Paycheck Protection Program, but they’re a tad late to the PPParty. On Twitter, Senator Marco Rubio, one of the co-sponsors of the CARES ACT that developed this program, confirmed the rumors that the well had run dry. “Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.”

Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.

Now 700000 small business applications are in limbo & no new loans will be made until the game of chicken in Congress ends & additional $ approved.

Inexcusable

— Marco Rubio (@marcorubio) April 15, 2020

Here’s the math

Congress approved $349 billion to guarantee #PPP

At 2pm today had over $300 billion in approved #PPPloans

Need $10 billion to cover fees & processing

When we reach $339 billion limit PPP will stop until they end with the ridiculous games & approve more funds

— Marco Rubio (@marcorubio) April 15, 2020

The SBA has often made reference to total funds “approved” when calculating its numbers rather than loaned out, so if you’re a business that has already been approved, then presumably funds have already been allocated for your business and you will still receive them. But if your application is pending, well it’s possible that funding may require additional congressional authorization. That however, as noted by Rubio’s remarks, will require some political compromise.

Update: 4/16 8 AM: Senator Rubio said on Fox Business that the PPP program was now frozen after having reached its limit and has stopped.

We’ll update this as more information becomes available.

Should I Apply to Become a PPP Lender?

April 10, 2020 One question being posed in the small business finance community is whether or not you should apply to become a PPP lender. Unless you are a very large well-capitalized company with a deep legal and compliance bench, you probably shouldn’t.

One question being posed in the small business finance community is whether or not you should apply to become a PPP lender. Unless you are a very large well-capitalized company with a deep legal and compliance bench, you probably shouldn’t.

Here’s why:

- You must supply the capital. While a federal mechanism is being put in place to offload the PPP loans you fund, you need the balance sheet to fund the loans in the first place. Also, consider that community banks have historically expressed frustration with the guaranty process and that’s when times and loan volumes were operating at normal levels. You must be prepared for hiccups to take place that delay or even possibly prevent offloading of some or all of these loans.

- You only earn a 5% processing fee on loans under $350,000. For larger loans, it’s a smaller percentage. You can’t even charge the applicant any fees at all so your compensation is entirely dependent on the SBA to pay you. Consider that your underwriting costs may offset some or all of that fee, leaving very little room for profit.

- You must have 2019 audited financial statements available for inspection by the SBA.

And you must have either of the following:

1.

- You must already have been applying Bank Secrecy Act-level compliance prior to this crisis.

- You must have been originating at least $50 million in business loans or other commercial financial receivables per year for each of the last 3 years consistently.

OR

2.

- You must already be a service provider to a bank.

- You must already have a contract to support the bank’s lending activities.

It’s a tough bar to meet for a small and mid-sized small business financing provider, but the program isn’t really set up to become a major profit center for lending companies, it’s supposed to be a support center for SMBs to keep workers employed. Initially, many banks were hesitant to get involved because PPP participation was going to generate LOSSES for them. It still might.

So what’s the incentive to be a non-bank PPP lender? It’s a moral pursuit on the front-end rather than a financially-driven one. On the back-end, it’s a tool for lead generation, public relations, and elevating goodwill value. If such lenders are able to execute successfully, it could further develop trust for fintech with legislators, regulators, and the general public. On the other hand, however, if they perform poorly, it could reflect negatively on fintech as a whole.

So if you find yourself on the PPP lending bench, you’re not missing out financially. You can still become an agent/broker should an approved SBA lender accept you. Such a role presents limited upside financial potential, so if it’s riches you seek, the PPP doesn’t provide them.

Lastly, becoming a PPP lender certainly won’t save a dying lending company. Making loans at 1% interest to distressed and closed businesses isn’t going to somehow save a company with an already damaged loan portfolio. It’s just going to put it out of business faster.

Should you apply to become a PPP lender? That’s up to you. Good luck!

Sorry, You’re Not Eligible For PPP Money

April 8, 2020 The rush to submit your PPP application may be for naught if you own an ineligible business. The SBA prohibits loan guarantees to “businesses primarily engaged in lending, investments, or to an otherwise eligible business engaged in financing or factoring.” If there’s any confusion as to what that includes, the SBA lists 7 specific ineligible business types under this definition in the statutory code. They include:

The rush to submit your PPP application may be for naught if you own an ineligible business. The SBA prohibits loan guarantees to “businesses primarily engaged in lending, investments, or to an otherwise eligible business engaged in financing or factoring.” If there’s any confusion as to what that includes, the SBA lists 7 specific ineligible business types under this definition in the statutory code. They include:

- Banks

- Life Insurance Companies (but not independent agents);

- Finance Companies

- Factoring Companies

- Investment Companies

- Bail Bond Companies

- Other businesses whose stock in trade is money

The PPP’s interim final rule refers to this statute as a rule for ineligibility as it applies to the PPP.

The statute does list a handful of businesses engaged in lending that may traditionally qualify for an exception. They are as follows:

- A pawn shop that provides financing is eligible if more than 50% of its revenue for the previous year was from the sale of merchandise rather than from interest on loans.

- A business that provides financing in the regular course of its business (such as a business that finances credit sales) is eligible, provided less than 50% of its revenue is from financing its sales.

- A mortgage servicing company that disburses loans and sells them within 14 calendar days of loan closing is eligible. Mortgage companies primarily engaged in the business of servicing loans are eligible. Mortgage companies that make loans and hold them in their portfolio are not eligible.

- A check cashing business is eligible if it receives more than 50% of its revenue from the service of cashing checks.

- A business engaged in providing the services of a financial advisor on a fee basis is eligible provided they do not use loan proceeds to invest in their own

deBanked is not a law firm. Consult a CPA or an attorney to provide better guidance on your company’s eligibility.