Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

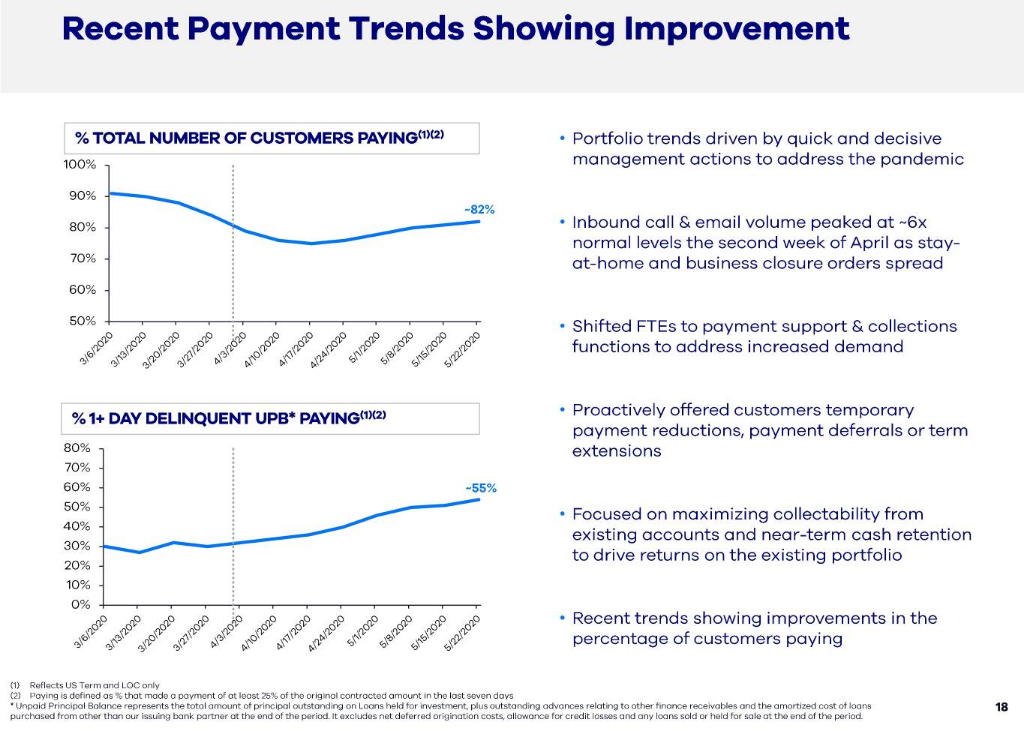

OnDeck Status Update

May 28, 2020

OnDeck submitted an unprompted mid-quarter update with the SEC early this morning on its status. Unlike previous submissions, the company prepared a visual of its debt situation. The bad news is that there is a good amount of negotiating with creditors left to be done. The good news was that there was an uptick in borrower payments. The attached graphics were pulled straight from their filing.

The company also said that it believes it is “well-positioned to benefit from economic recovery & market dislocation.” It based that belief on the below stated bulletpoints:

- Small business lending is a large market and will be critical in leading the economic recovery.

- OnDeck has deep experience from a 14-year operating history to increase originations with a targeted approach and reshape the portfolio.

- OnDeck is a scaled platform with demonstrated historical profitability and an established brand, unlike many competitors.

- Consistent with the last crisis, banks are likely to retrench further and only selectively serve SMBs.

- Expected consolidation of SMB lending industry will ultimately lead to improved unit economics and growth opportunities.

The full presentation, which is mostly a recap of the company’s Q1 earnings data, can be accessed here.

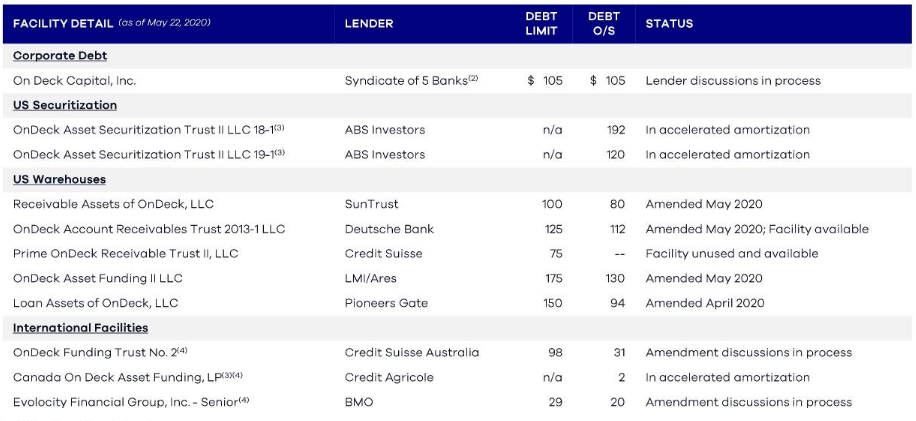

OnDeck Hits Payout Event Trigger on $105M Credit Facility

May 22, 2020Earlier today, OnDeck filed a status update to shareholders with the SEC. The company’s portfolio performance triggered an Asset Performance Payout Event (Level 1 they say) with a credit agreement that at present has an outstanding balance of $105 million.

The event triggers monthly principal repayments which, if not cured or amended, would commence with a $13 million payment on June 17, 2020. Subsequent principal payments are based on a percentage of the currently outstanding balance of $105 million until the Corporate Facility matures in January 2021. The Company is in active discussions with the Corporate Facility lender group to evaluate potential options with regard to this facility.

OnDeck was able to further modify agreements on two credit facilities (ODAF II and ODART) to which they had previously secured only interim relief of a few days.

Shares of OnDeck have hovered between 60 cents and 70 cents in the past week.

Broker Fair, Not a Webinar… A Virtual Reality Conference

May 21, 2020 Coming June 11th, Broker Fair in Virtual Reality. Much different from a webinar, Broker Fair Virtual will actually be a virtual world with a lobby, exhibit hall, networking lounge, and auditorium. Attendees will be able to interact with each other as well as visit and interact with sponsors at their virtual booths.

Coming June 11th, Broker Fair in Virtual Reality. Much different from a webinar, Broker Fair Virtual will actually be a virtual world with a lobby, exhibit hall, networking lounge, and auditorium. Attendees will be able to interact with each other as well as visit and interact with sponsors at their virtual booths.

There will be live video sessions too of course (see the agenda here), but if you’re there for the networking, get ready for a totally unique experience!

Broker Fair 2020 Virtual isn’t replacing the In-person event. That’s been rescheduled to 3/22/21 at the same location, Convene at Brookfield Place in New York City. All attendees registered for the in-person event are able to attend this virtual event on June 11th for free. If you never registered for that, you can still buy tickets that grant access to both at: https://brokerfair.org/register/

See you at Broker Fair!

Hidden Tax Liabilities: Assessing Small Business Borrower Risk Before, During, and After The Pandemic

May 19, 2020How lenders assess the risk of small business borrowers is changing and one important factor that no one will be able to ignore is tax liabilities. Hansen Rada, CEO of Tax Guard, told deBanked that outstanding tax liabilities are not always readily apparent in the form of a lien. Tax Guard can fill in the blanks on what lenders normally wouldn’t be able to see.

I asked Rada what tax liabilities even meant for a small business, especially in today’s environment.

“Tax liability is not the disease,” Rada said. “It’s a symptom of the disease. The disease is cash flow.”

In this 17 minute Q&A, I asked Rada many questions that underwriters all over the country are probably thinking about right now. Watch it below:

The Latest With OnDeck

May 18, 2020A Week after OnDeck reported Q1 earnings, the company experienced its first early amortization event brought on by the COVID-19 crisis.

The news was publicized in a May 11th filing with the SEC:

On May 7th, an early amortization event occurred with respect to the Series 2019-1 notes issued by OnDeck Asset Securitization Trust II LLC, or ODAST II as a result of an asset amount deficiency in that Series. Beginning on the next payment date under the ODAST II Agreement, all remaining collections held by ODAST II, after payment of accrued interest and certain expenses, will be applied to repay the principal balance of the Series 2018-1 notes and the Series 2019-1 notes on a pro rata basis.

The company also revealed that it had amended a debt facility “so that no borrowing base deficiency shall occur during the period from April 27, 2020 to July 16,2020.”

The company also revealed that it had amended a debt facility “so that no borrowing base deficiency shall occur during the period from April 27, 2020 to July 16,2020.”

On May 15th, OnDeck notified shareholders of additional events and maneuvers through a new filing published after the closing bell. The filing stated that:

On May 12th, a similar event happened with the 2018-1 notes as had happened with the 2019-1 notes.

On May 14th, OnDeck modified the terms of a debt facility so that “from March 11, 2020 to August 31, 2020, receivables granted temporary relief in response to the COVID-19 pandemic will generally not be considered delinquent […] so long as such receivable is paying in accordance with its modified terms.”

Also on May 14th, OnDeck obtained a temporary waiver on another debt facility. “Under the waiver, the lenders temporarily waived the occurrence and existence of reported borrowing base deficiencies and any failure to cure such deficiency amount, in each case, until the close of business on May 19, 2020.” OnDeck accepted the waiver with the understanding it would enter into a broader amendment to remain in compliance with performance and other criteria in light of increased delinquency and other portfolio dynamics that result from COVID-impacted loans. “If such an amendment is not entered into or if the borrowing base deficiency is not otherwise cured, the borrowing base deficiency would constitute an event of default under the ODAF II Facility at close of business on May 19, 2020.”

The 19th is tomorrow.

A similar waiver was obtained for another debt facility. The company has until May 20th to enter into a broader amendment to remain in compliance on that one.

The company is in a fight for its survival. In late April, OnDeck “suspended nearly all new term loan and line of credit originations and previously ceased all equipment finance lending.” The company reported that it is “focused on liquidity and capital preservation and expects there will be a significant portfolio contraction, reflecting an 80% or more reduction in the second quarter origination volume.”

The stock closed at 64 cents on Friday and a market cap of only $37.3M. Shares had traded over $4 earlier in the year.

On May 7th, shareholders voted overwhelmingly in favor of keeping CEO Noah Breslow on the company’s board of directors.

Forgiven Debts: The Hidden Tax Time Bomb That Could Kick Small Businesses While They’re Down

May 12, 2020 Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

Small businesses that stay out of bankruptcy but have some portion or all of their debts forgiven (excluding PPP debt) are in for a rude awakening come tax time next year. In a variety of circumstances, cancelled debt can be classified as taxable income for the debtor per the IRS. This, according to a new tax study titled Did The IRS Forget Non-PPP Debt? authored by Grassi & Co, a leading accounting and business firm based in New York, that was produced in collaboration with deBanked.

At face value, it would appear that taxpayers who have non-PPP debt canceled, forgiven or discharged during the COVID-19 crisis and do not meet any of the specific exclusions mentioned in the report, would be subject to tax on the cancelled debt as income.

This tax treatment, which pre-existed COVID-19, could be devastating in this era where the prevalence of debt forgiveness is likely to reach unprecedented levels.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

In many cases this year, debt cancellation will be the direct result of government mandated shutdowns that were of no fault of the businesses themselves. Should they refrain from filing for bankruptcy and successfully negotiate a cancellation of some debt, it seems quite disastrous that the same government that shut them down might deliver a second blow by taxing the acts that enabled the businesses to survive.

One must also consider that a lender may just cancel some or all of a portion of a debt without any direct action of the debtor, with the end result being the same, a potential tax bill to the business on the cancelled portion.

It’s important to understand the various exclusions to the IRS guidelines that govern cancelled debt. The full report can be ACCESSED HERE.

$100 Million in PPP Fees

May 12, 2020 $100 million. That’s the gross revenue floor that Ready Capital reported yesterday will be earned from its PPP loan origination efforts. PPP lenders earn between 1% to 5% of the loan amount in the form of a fee from the SBA and Ready Capital was the 15th largest PPP lender by dollars in the first round alone.

$100 million. That’s the gross revenue floor that Ready Capital reported yesterday will be earned from its PPP loan origination efforts. PPP lenders earn between 1% to 5% of the loan amount in the form of a fee from the SBA and Ready Capital was the 15th largest PPP lender by dollars in the first round alone.

The SBA pays 5% for loans under $350,000, 3% for loans between $350,000 and $2 million, and only 1% on loans over $2 million. With the majority of Ready Capital’s loans being for less than $350,000, the pure volume of loans originated (40,000+), translates into significantly larger fee income against a lender who may have originated the same dollar amount but with a much larger average loan size. JPMorgan’s average PPP loan size in Round 1, for example, was $515,000 (an average of a 3% fee) versus Ready Capital’s $73,000 (an average of a 5% fee).

Ready Capital clarified that on a net basis of those fees, they will take home substantially less, since the economics of those fees were in many cases split with referral agents and other partners that contributed in the process. Without committing to a firm figure, they estimated that their net revenue on PPP originations is actually going to be in the neighborhood of 35%-50% of the gross ($35 million to $50 million).

That is so far. Ready approved $3 billion in loans and has so far only funded $2.1 billion of them. The company said it expects that a large percentage that remain will still be funded and they will earn additional fee income respectively from those.

The company also addressed funding delays that had been reported across social media. “While there have been some challenges outside our control that have caused some delays in the distribution of funds, we have facilitated the funding of 2.1 billion through last Friday and are actively working through the remaining population to disperse funds as quickly as possible.”

Ready’s exposure on the loans themselves may be limited. The company said “we do not expect to carry much of the production on the balance sheet at all. So a very small portion will remain on the balance sheet. The majority of it will now be sold off balance sheet.”

Interview With Polling Expert Scott Rasmussen

May 7, 2020On Tuesday, I interviewed nationally recognized public opinion pollster Scott Rasmussen, who is the publisher of ScottRasmussen.com and is the editor-at-large for Ballotpedia, about the trajectory of the presidential race and how the current environment is affecting how people think.

Mr. Rasmussen will be a guest speaker at Broker Fair 2020 Virtual on June 11, 2020. You can watch the video interview below.