Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Shark Tank, The Profit and Kitchen Nightmares

January 29, 2015 What do Shark Tank, The Profit and Kitchen Nightmares have in common? They’ve all featured merchants who’ve used merchant cash advances. Statistically it’d have to happen but there’s nothing more wild than watching Marcus Lemonis try to save a failing business I actually declined for funding.

What do Shark Tank, The Profit and Kitchen Nightmares have in common? They’ve all featured merchants who’ve used merchant cash advances. Statistically it’d have to happen but there’s nothing more wild than watching Marcus Lemonis try to save a failing business I actually declined for funding.

One deal I personally worked on has appeared on The Profit and there were a couple others that I’ve seen shopped around in the MCA space. Not sure if that restaurant on Kitchen Nightmares has used merchant cash advances? Just conduct a UCC search and find out!

No amount of underwriting could ever give you the perspective you get on TV. In between the lines of a business wanting help is usually a disaster or series of disasters that has the business on edge; All the employees are about to quit, the landlord wants them out, their vendors are mad at them, the owner’s an intolerable jerk, they don’t know how to market themselves, or the customer experience is horrible. It’s always something.

At least on Shark Tank the only thing scrutinized is the presentation of the product and the viability of it. On The Profit and Kitchen Nightmares, all the secrets are laid bare.

On the one hand it’s a glimpse into the struggles of running a small business, an experience I know firsthand from growing up working at two family owned restaurants. On the other hand, it’s a sobering reminder that there is so much risk in lending them money.

On The Profit, Lemonis hedges his risk by typically taking 50% (OR MORE!) equity in return. His famous pitch to these merchants who always come across as shocked is that, “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother.”

"I'm not a bank. I'm not a consultant. And I'm not the fairy godmother." –@MarcusLemonis #theprofit https://t.co/sIUH2Tj21p

— CNBC's The Profit (@TheProfitCNBC) November 18, 2014

Deals go bad

And even that approach carries risk. Early last year on the show, Lemonis wired $190,000 to Brooklyn-based business A. Stein Meat in return for 100% of their Brooklyn Burger Brand. The business used the cash to make payroll and reneged on the transfer of the burger brand, claiming they thought the money was a loan. They never made any payments back on it.

Lemonis filed suit against them in the United States District Court for the Eastern District of New York which opens by stating:

This is an action to enforce the straightforward, bargained-for agreement entered into by and between defendant Stein Meats and Lemonis, by which Stein Meats agreed to sell its “Brooklyn Burgers” brand of hamburgers to Lemonis. The agreement is unequivocal, and was witnessed by the millions of viewers who have watched Episode 2 of the second season of the CNBC reality television series “The Profit” that first aired on March 4, 2014.

However unequivocal it may have appeared, the case is still going. A peek at the court records show bitter and unrelenting litigation. At the time of filming, Stein Meats was only 2 weeks away from bankruptcy and was reportedly sold to its competitor, King Solomon. King Solomon is also named as a defendant.

The Brooklyn Burger brand is still in use as I enjoyed one of their tasty burgers at a Nets game last month.

Wait, don’t I know this deal?

In another episode of The Profit, the owner of a business I declined for a merchant cash advance is fingered as a bad guy. He was unrepentant, suggesting that the bridges burned, lives ruined, and debts defaulted on along the way were worth it to get the business to where it was now. I distinctly recall being shocked by their mountain of debt, which became the reason I declined it. Their debt problems were even highlighted on the show!

I had the luxury of examining their Balance Sheet since their request was sizable. Had the request been smaller, it wouldn’t have been required. Thankfully they were transparent about their debt. Of the thousands of applications I’ve underwritten in my day, I learned that it is incredibly hard for a small business to supply a financial statement, and of the ones I got, it was difficult to ascertain their accuracy. I’ve seen Balance Sheets that didn’t balance, numbers that were completely illogical, or statements that were missing major line items.

I see only two ways to approach something like this. It’s either a decline or it’s going to be expensive. I don’t care what my algorithms say their social media score indicates. If the business doesn’t keep good books then I have no idea what I’m exposing myself to.

The real world’s not so bad after all

I can’t help but notice that one of the best guys in the small business space takes a similar no-nonsense approach. You give Lemonis half of your business or he walks. Being on the show might boost sales but taking his money is not charity.

The only difference I’ve discovered between business financing deals made in real life and ones made on TV is that the ones on TV are more expensive. It’s the opposite of what you might expect.

If Lemonis thought his agreement witnessed by millions of people was unequivocal, then shouldn’t an online lender who has never met their client, nor visited their business, feel slightly less comfortable about their agreements?

I would think so.

Inc reports that Lemonis spends eight full days with each business but on twitter he claims it’s much more than that.

“@DominoTheGreat: how long do you film each show for? Few days, week? Does it vary from show? #asktheprofit #TheProfit” couple months

— Marcus Lemonis (@marcuslemonis) October 15, 2014

During filming, Lemonis can be seen going through the financial statements, interviewing employees, negotiating deals with vendors, trying out the products, and scrubbing toilets. With that experience and knowledge under his belt, he presents his cold hard deal, money for a massive equity stake. The terms are aggressive but he’s steadfast in his role as a businessman and not a fairy godmother.

Contrast that experience with a merchant cash advance company that has almost nothing to go off of by comparison; a few bank statements, a credit report, and maybe some online data points. With only this, they’re supposed to wire out $5,000, $50,000 or $150,000 to a business across the country and get no equity in return.

The two things that I’ve learned from these celebrity businessmen is that their underwriting is more personal and they manage to be even more expensive. They promise their expertise is what makes up the difference.

I’d love to say that every situation is different but it’s gotten to the point that we’re working on the exact same deals. If a merchant can get a better deal off TV than on it, I’d say things are pretty good right now.

deBanked Magazine

January 22, 2015The world of alternative finance is coming to print. Interested in subscribing to the industry magazine for FREE?

SIGN UP

SUBSCRIBE FREE

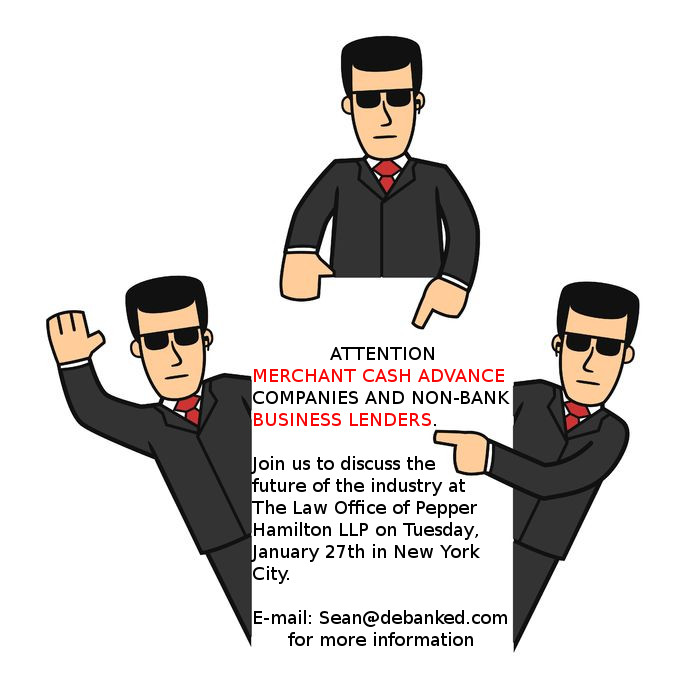

Discuss The Future of the Industry

January 20, 2015 The alternative business financing industry is made up of several thousand companies nationwide, but what holds it all together?

The alternative business financing industry is made up of several thousand companies nationwide, but what holds it all together?

With non-bank financing now in the mainstream, the general investing public and politicians are starting to ask questions. Can we answer them coherently?

January 2015: Rahm Emanuel pledges to lobby for state and federal regulations on business-to-business financing.

September 2014: Former head of the SBA recommends regulations for non-bank business lenders and merchant cash advance companies.

August 2014: NCRC recommends the Consumer Financial Protection Bureau regulate merchant cash advance companies.

May 2014: Merchant cash advance companies banned from factoring associations.

Let’s work together as an industry! The Law Office of Pepper Hamilton is hosting a lunch from 10am to 2pm on January 27th in their office in New York City.

If you’d like to attend, email me at sean@debanked.com.

ACH is the Annoying Little Thing We Can’t Live Without

January 19, 2015 A few months ago I paid an invoice via ACH. The vendor was used to getting paid by check and didn’t accept credit cards. When I mentioned the funds would be paid overnight, they got excited but were suspicious. Would there be a fee to receive the money like a Fed wire might? “Nonsense,” I told them.

A few months ago I paid an invoice via ACH. The vendor was used to getting paid by check and didn’t accept credit cards. When I mentioned the funds would be paid overnight, they got excited but were suspicious. Would there be a fee to receive the money like a Fed wire might? “Nonsense,” I told them.

When the banks opened the next morning, they didn’t see it. The funds had been withdrawn from my account and I double checked that the account and routing number matched their voided check. They took no comfort in that verification of course because they didn’t see the money on “their side.” That put the burden on me to convince them nothing had gone wrong or that I wasn’t lying. “It should be there,” I told them. “Who knows, depending on your bank it might not post until tomorrow.”

Let’s spend all day researching this payment

Putting the blame on the recipient’s bank or the ACH system as an imperfect fluid thing that comes with no guaranteed delivery schedule only heightened their levels of suspicion.

If you’ve been in this situation before particularly when funding a merchant who claims the funds are not there, there is only so much you can say or do to pacify them.

“Can you give me some kind of confirmation number?” they ask. Ahh, the mythical confirmation number.

So you call your bank, get some kind of number and pass it along to them which their bank does nothing with because they have no record of any incoming payment.

At the vendor’s behest, I went back and forth between my bank and their bank to try and locate these funds. The quest to find the missing deposit took up the first six hours of my day. Honestly I wasn’t worried about it. I was pretty sure it would show up eventually, but the vendor was freaking out.

With the work day almost over, the receiving bank finally logged a pending deposit in the vendor’s account.

It was good enough for them. They finally believed me. Phew.

You got the money, right?

How do I know my vendor actually got the money? Well because they told me they did…

Good enough perhaps, but a few years ago I helped a merchant get financing that claimed they did not receive their funds even though I was pretty sure they did. I went through the whole shebang, ACH system this, your bank that, confirmation number this, let me double check that, etc.

Three days later they claimed they still had not gotten it. It turns out they had but they knew without direct access to their bank account, we couldn’t confirm it, at least not in time to try and reverse the transaction successfully. Did we screw up somewhere? Was the routing number right? It’s a horrible feeling to believe you didn’t deliver what you promised you would to a merchant.

Three days later they claimed they still had not gotten it. It turns out they had but they knew without direct access to their bank account, we couldn’t confirm it, at least not in time to try and reverse the transaction successfully. Did we screw up somewhere? Was the routing number right? It’s a horrible feeling to believe you didn’t deliver what you promised you would to a merchant.

After more than a week we had figured out he not only received the cash, but had moved the money out of the account and bailed.

Once the money goes into the ACH system, you really don’t know anything. Some alternative lenders can confirm clients received deposits by requesting the client’s username and password to log into their bank account. This is a terribly flawed system.

Out there in the regular world I couldn’t have asked my vendor for the credentials to their online banking. Oh you didn’t get the ACH? Give me the password to your bank accounts, I’ll go have a good look.

You call this efficient?

In 2015 I can send money and have no idea if the other person got it. Somehow this is standard. It’s like e-mail in a way. I know I sent it but until they tell me they received it, who really knows.

There are obviously options to transfer money instantly but it comes at a great cost. And someone still has to tell me it got to the other side. I can’t confirm it myself.

In the age of the Internet, it’s amazing how inefficient payments are. We refer to modern payment processors as disruptive services, but it’s same problem with a different twist. Somebody pays you by credit card and the payment processor flags the sale, causing you to have to send documentation to their risk department to review. If rejected, the funds are held for six months and quite possibly your merchant account terminated. The customer won’t know all this though. All they knew is that their card was charged.

Intermediaries make transaction processing easy but they also make it really hard. The alternative lending industry spends entirely too much time managing payments.

The ACH debit was successful… or was it? Let’s wait 3 days to find out if it gets reversed before we really know for sure.

Did they get the money? Let me call them to confirm. Oh they didn’t pick up. I’ll write them an email asking them to confirm that they got my ACH.

They said they sent the money but I don’t see anything. Can you send me a confirmation number?

I sent you that email on thursday, you didn’t get it?

We’re used to a system where the only thing you can confirm is that something was sent and so we spend countless hours and money trying to figure out if they were received.

Meanwhile, in the future…err present day

One of the most remarkable features about the Bitcoin system is that I can confirm that the money I sent was received by the other person. Everyone else in the world can confirm it too. The dollar/bitcoin balance of all bitcoin addresses are public and anyone can create a near infinite number of bitcoin addresses.

One of the most remarkable features about the Bitcoin system is that I can confirm that the money I sent was received by the other person. Everyone else in the world can confirm it too. The dollar/bitcoin balance of all bitcoin addresses are public and anyone can create a near infinite number of bitcoin addresses.

I joked before that in order to truly see with my own eyes that a vendor did not receive my ACH was to request the credentials to their online banking and log in. But all they need to do is generate a one-time use bitcoin address for the transaction and when I send funds, both they and I will see it deposited there, instantly.

Money sent, they got it instantly, I see it there, end of story.

Recently, .01 BTC was sent to this bitcoin address of mine: 19kzD1RkC8MjazfCkCJkfx7369ULCyPsg1

Check it out here: http://bitref.com/19kzD1RkC8MjazfCkCJkfx7369ULCyPsg1

or here: https://blockchain.info/address/19kzD1RkC8MjazfCkCJkfx7369ULCyPsg1

If you needed to pay me, I would click a “generate address” button on my computer, you send bitcoins to it, and there will be no doubt that they were received because you can view the balance of it yourself. I can keep the funds in that address or move them to another one. Even if moved, the paper trail that they were there remains. There is no uncertainty or research required.

So who confirms the transactions? Not the Automated Clearing House thank God. Bitcoin miners and nodes do. You can read about my experience as a miner here.

At present, the standard bitcoin network transaction fee is .0001 BTC, the equivalent of 2 cents. Transactions are also irreversible! No chargebacks!

You can send me a thousand dollars or a million dollars instantly for the price of 2 cents and view the balance in my receiving address as proof that I got it. Thousands of people do this every day.

Bitcoin’s adoption has been slow, it’s history volatile, and its reputation murky, but I pray everyday that a decentralized technology like this will last in the mainstream. The bureaucracy, inefficiency, and lack of transparency in other forms of payments are a drag on commerce.

If you’ve ever spent longer than a minute trying to figure out if money made it from point A to point B, you need to start learning about the Bitcoin system. If you’ve ever spent more than 2 cents sending money, you need to start learning about the Bitcoin system. And if you’ve ever had a payment processor give you a hard time about a transaction, you need to start learning about the Bitcoin system.

You might be happy with ACHs for now but we were all happy with telegrams once. That’s about the level of sophistication the mainstream payments industry has now. I can’t wait until this era is over.

Mayor Rahm Emanuel Declares War on Merchant Cash Advance

January 16, 2015 FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

Mayor Rahm Emanuel will call on state and federal agencies to regulate business to business lenders. Emanuel said cash advance companies have accelerated their marketing efforts in recent months, resulting in small businesses taking loans they cannot afford.

The article states that business owners have turned to the City of Chicago for help in paying back loans with high rates of interest.

While the mention of APRs reaching into the ranges of triple digits is supposed to shock you, one business lender that charges such rates recently went public and had been backed by Google Ventures, Fortress Investment Group, Goldman Sachs, and Peter Thiel.

Less than 30 days ago we were celebrating these companies as the solution to a problem that has plagued small businesses for all time, access to capital.

While Emanuel is obviously famous for being the 23rd White House Chief of Staff and Obama’s right hand man for a period in his first term, he is not the first mayor to consider the role merchant cash advance companies and high interest business lenders have in cities across America.

All the way back in 2008, the U.S. Conference of Mayors (USCM) adopted a resolution titled, Protecting Main Street Small Business Owners from Predatory Lenders, from which some of the excerpts below are from:

WHEREAS, merchant cash advance companies have already lent approximately $2 billion at egregious rates and have been quoted in leading main stream media publications such as Forbes, Business Week, Dallas Morning News, and American Banker claiming that their new originations have increased 75% in the first half of 2008

WHEREAS, as with payday lenders and predatory lenders in the home mortgage community, Mayors need to take a leadership role to scrutinize predatory merchant cash advance companies, educate small business owners of the dangers posed by these firms, and increase awareness and promotion of alternative, more affordable funding sources to support this vital segment of our economy

BE IT FURTHER RESOLVED, that to protect the general health and viability of their small business communities, cities should investigate whether they can effectively regulate or ban merchant cash advances.

3 months after this resolution was passed, Lehman Brother’s collapsed and the economic crisis was in full swing.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

Who do they think rolled up their sleeves and kept local economies alive when things were at their worst?

While non-bank funding can obviously be expensive, countless business owners have praised merchant cash advances in particular as a solution that came through when none other were available.

Emanuel will learn that companies such as Square and PayPal are part of the crowd that provides merchant cash advances. This is not a shadow industry. Non-bank business-to-business financing is already becoming less expensive nationwide.

According to Fox, the Commissioner of the Chicago Department of Business Affairs and Consumer Protection said the goal is to offer small business owners loans at affordable rates with full disclosure.

Merchant cash advance companies would undoubtedly feel the same way. The dilemma is that advocates of affordable rates tend to really mean single digit rates. When single digit rates are not possible given the risk, they seem to argue that no financing should be given at all, leaving the business to fail or miss out on an opportunity. That’s the exact type of flawed thinking alternative financing companies address…

Ironically, a report from the Federal Reserve Bank of Cleveland last week concludes that small business job creation is lagging with a possible culprit being a lack of access to credit.

Coming out of the most recent recession, however, job creation by small businesses has lagged, and the new business formation rate continues to fall. While it is not clear that these trends are driven by weaker borrowing or limited access to loans, it is evident that businesses need adequate credit to succeed and grow. As such, policy makers should not lose sight of the trends related to small business credit, even with the recent positive reports showing improvements.

And of course in a supposed exposé on merchant cash advances that aired on Chicago Public Radio in November, clips of an interview I did with them were aired to fit the narrative of merchant cash advance as predatory. When asked by the interviewer what a small business owner should do if they didn’t understand a contract, I advised that they hire an attorney or an accountant, and if they couldn’t afford those then to find somebody they felt qualified to offer an opinion. “They should always get a 2nd set of eyes to review a contract if they don’t understand,” I said.

My advice did not air, nor did my explanation that there were two separate types of products that they were confusing as one, one being loans and the other being purchases of future receivables. I suppose it didn’t fit the characterization they were going for.

As quoted in Fox, Financial Advisor Kent Travis advised business owners to “read the documents, don’t sign anything on the spot, make sure you read it thoroughly and if you have trouble understanding it seek the advice of an advisor, CPA, an attorney or a financial planner.”

I couldn’t have said it better myself because I already did.

And in an interview I had with former Congressman Barney Frank, a chief architect of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Frank voiced his opposition to regulations on business-to-business lending in early 2014.

There’s one thing the Fox story does mention that’s hard to argue with and that’s the need for greater transparency. I am all in favor of that.

—————–

For those that haven’t already signed up, this is a reminder that the Law Office of Pepper Hamilton LP is hosting a lunch at their office in New York on January 27th to specifically discuss the merchant cash advance industry’s future.

Interested in discussing legal issues, best practices, and the path forward for alternative business financing? Are you an ISO or funder interested in sharing your thoughts? Send me an email to let me you know if you’d like to attend. sean@debanked.com.

—-

Watch the Fox news report about merchant cash advances:

Merchant Cash Advance Accounting Pitfalls

January 13, 2015This is question #5 in an interview between deBanked’s Sean Murray and accountants Yoel Wagschal, CPA and Christina Joy Tharp.

- 1. Merchant Cash Advance How to Guide Intro

- 2. Do I Need a Special MCA Accountant?

- 3. and 4. Recording Merchant Cash Advance Transactions on the Books

- 6. Revenue recognition for Merchant Cash Advance

- 7. Q&A – Real questions that MCA companies or syndicators have

Q: Are there any pitfalls for ISOs or funders in the industry with how they run their books? Big no-nos, etc?

A: Here are some of the most common pitfalls we have seen:

- Don’t think of this as a loan – that’s a huge pitfall that we have experienced firsthand (get rid of that word!)

- Don’t have your CFO be one of your syndicators. This inevitably creates multiple conflict of interest issues.

- The biggest no-no – don’t rely solely on spreadsheets! You need a good accounting system that will cross reference and reconcile your accounts. It needs to track and present your cash activity and it should ultimately provide you with your crucial reports. Basically, it needs to accomplish all of the trifecta in question #1.

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

Recording Merchant Cash Advance Transactions

January 13, 2015This is question #3 and #4 in an interview between deBanked’s Sean Murray and accountants Yoel Wagschal, CPA and Christina Joy Tharp.

- 1. Merchant Cash Advance How to Guide Intro

- 2. Do I Need a Special MCA Accountant?

- 5. Merchant Cash Advance Accounting Pitfalls

- 6. Revenue recognition for Merchant Cash Advance

- 7. Q&A – Real questions that MCA companies or syndicators have

Q: ISOs and funders are often asked by their clients or their accountants how to record selling their future sales on their taxes. Should merchants just record it as a loan?

A: No, No, No, and absolutely NO. “Loan” is a dangerous word. MCA’s do not handle loans because if these cash advances were loans then you could not charge such a high percentages. These percentages on “loans” would be against usury laws. Never, ever, use the word “loan”. Take it off of your websites. Take it off your business letters. Remove “loan” from your vocabulary entirely. The funder is buying and the merchant is selling “future sales”.

Q: How should a funder record buying future sales from a GAAP perspective? From an IRS tax perspective?

A:The IRS does not have any special provisions for the MCA industry so follow GAAP. If you have a departure from GAAP for tax purposes, it is the same as in any other industry.

Here is the typical debit and credit entry for most every normal sale:

The company pays for product XYZ with 1,000 USD:

| Account | Debit | Credit |

| Inventory/Purchases | 1,000 | |

| Cash | 1,000 |

The company sells product XYZ and collects 1,500 USD:

| Account | Debit | Credit |

| Cash | 1,500 | |

| Sales | 1,500 |

Very simple. Here you have a profit of 500 USD and this is what you see in your bank account. If the 500 USD is not in the bank it could be for various reasons which is why you need to reconcile.

Of course, there is much more to the merchant cash advance business than these simple transactions but we want to stay focused on this for a little while.

Now remember the business model of the supermarket? Every day the supermarket does thousands of orders and each order has dozens of items. We have to do the accounting for all of those transactions in order to reconcile the proper balances with the inventory. If done manually, we would need an entire staff of accounting clerks just to do those transaction entries.

That’s why everyone in the retail industry understands that they need a good point of sale (POS) system in order to record the information. What do you think the accountant does? The accountant prints out a report at the end of the day/week/month and from that report the accountant creates one entry in the general ledger showing the summary of the day.

I.E.: The summary tells the accountant that registers have rung up the total of 300,000 USD in sales of which 280,000 USD was paid in cash and 20,000 USD was paid on credit.

| Account | Debit | Credit |

| Cash | 280,000 | |

| A/R | 20,000 | |

| Sales | 300,000 |

The idea is that you can sell as many items as you want in a single period but that your accountant should not have more than one transaction to post to the general ledger.

When you want to micro manage you look at the point of sale system. How do you know that the POS system is correct? What is the end goal? Where does the buck stop? Yes, the buck stops in your bank!

If the POS summary is being put in the general ledger, and the general ledger is matching up with the money in your bank – BINGO! If it doesn’t match – TROUBLE!

With this simple transaction in mind we see that the MCA industry has two big challenges:

1) Finding the right management software

2) Finding an accountant who really understands how to reflect these numbers in the general ledger

Unlike in a regular retail business (where you sell a product for money) the product that you are selling here actually is underlying money. It is not a loan, but a purchase of future sales. As this is the case, your bank account becomes the point of sale system. However, a bank typically doesn’t have point of sale capabilities when it comes to reporting and accounting.

To successfully track every cent of your transactions a good cash advance company must have excellent management software. The software must provide a mirror image of the transactions in your bank accounts.

The only way you can do that is if you have one bank account designated to handle only transactions that are reflected in the management software. If you decide to pay a phone bill from this “software transaction only” account, it will be just like a supermarket owner that takes a 100 bill from a cash register in order to pay the store’s phone bill.

Once you establish the “software transactions only” account, (and you have an accountant who can record the summaries into the general ledger while understanding how the general ledger ties into the bank account) then and only then will you be in good shape.

The understanding of the cash advance accounting journal entries can be very confusing if you don’t understand the small steps that make up the big picture. Research reveals sparse results. As that is the case, I will only illustrate a basic example (with no fees).

Please keep in mind that each MCA has different ways of doing some things. This example will cover the basic standards but for modifications and special needs, you will need to find an accountant that understands the eccentricities of your own company’s business model.

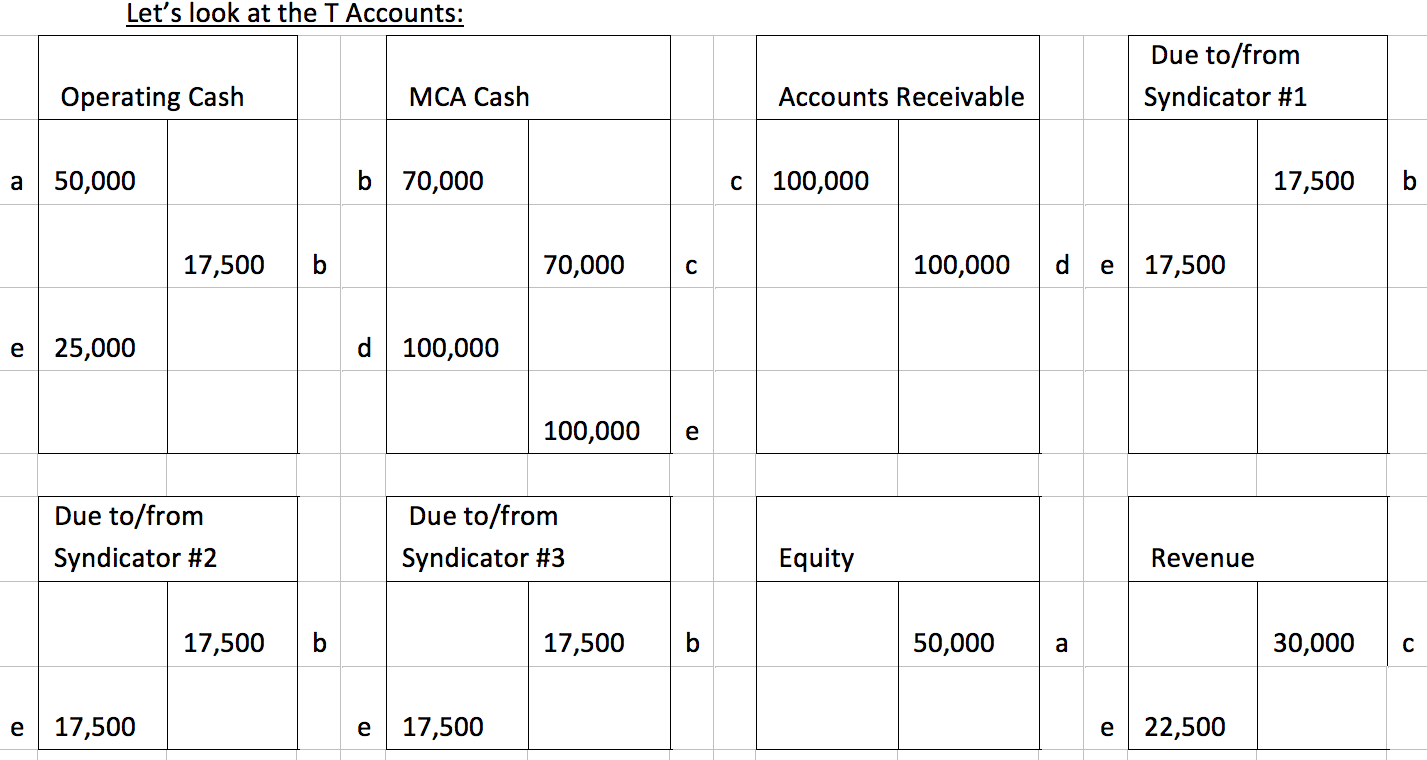

Our MCA model starts with the formation of a small fictional cash advance business. We will start this MCA business with 50,000 USD seed money and we make contact with three investors who we will refer to as syndicators. Yes, I know that some of you reading this call these investors or syndicators by different names, which is part of the confusion out there. To avoid further expatiation, we will use only the term “syndicator” in this article.

On day one “ABC merchant” wants to sell 100,000 USD of their future sales to our MCA business for the discounted rate of 70,000 USD. We reach out to the aforementioned syndicators. They agree to contribute 25% each.

Future sales will be scheduled in terms of 1,000 USD per day for the next 100 days

We are going to have 30,000 USD in profit and it is going to be split among 4 people, each receiving 7,500 USD.

Now we will give it some familiar terms:

Funding amount = 70,000

Payback amount = 100,000

Daily ACH = 1,000

| Account | Debit | Credit |

| Operating Cash | 50,000 | |

| Equity | 50,000 |

| Account | Debit | Credit |

| MCA Cash | 70,000 | |

| Due to/from Syndicator #1 | 17,500 | |

| Due to/from Syndicator #2 | 17,500 | |

| Due to/from Syndicator #3 | 17,500 | |

| Operating Cash | 17,500 |

| Account | Debit | Credit |

| Accounts receivable | 100,000 | |

| MCA Cash | 70,000 | |

| Revenue | 30,000 |

| Account | Debit | Credit |

| MCA Cash | 1,000 | |

| Accounts Receivable | 1,000 |

Although the next step depends on when a MCA company repays its syndicator investments, we will assume the syndicators are all paid at once to allow for a simple transaction example. There is a credit to cash and debits to the syndicator accounts for the principal and the revenue account or an offset account for their share of the profit. The share that I have to split with syndicators wasn’t really my own revenue in the first place.

Multiply this transaction for the number of days (in our example, 100 days). The net effect on this particular transaction will look similar to this:

| Account | Debit | Credit |

| Due to/from Syndicator 1 | 17,500 | |

| Due to/from Syndicator 2 | 17,500 | |

| Due to/from Syndicator 3 | 17,500 | |

| Revenue | 22,500 | |

| Operating Cash | 25,000 | |

| MCA Cash | 100,000 |

| Cash | 57,500 |

| Total Assets | 57,500 |

| Equity | 57,500 |

| Revenue | 7,500 |

After you examine all of the transactions, you’ll see that the chips fall in the right places. We started out with 50,000 USD and received profit from our 25% participated in a merchant funding deal. That deal ended with total revenue of 7,500 USD. It’s all there!

If you truly understand these transactions and you have the proper system in place, then this process should be very easy to follow (even if each of these transactions happens a million times a day).

However, if you don’t understand then you should be very careful because only proper accounting measures can save you from losing tens of thousands or even hundreds of thousands of dollars without ever knowing it. Unfortunately, I have seen it happen with my own eyes. Just like the grocery store example above, the sale of money to MCAs is just like the sale of tomatoes is to grocery stores. If left unaccounted for, those tomatoes could go missing without the store owner even noticing. Don’t let that be you with your money!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.