Kevin Travers was a Reporter at deBanked.

Articles by Kevin Travers

Shopify Capital Q1 SMB Funding Soars

April 28, 2021 Shopify Capital posted monster figures on Wednesday, originating $308.6 million total in MCA and loans. Across the US, Canada, and the UK, Shopify saw a 90% increase from Q1 last year.

Shopify Capital posted monster figures on Wednesday, originating $308.6 million total in MCA and loans. Across the US, Canada, and the UK, Shopify saw a 90% increase from Q1 last year.

In total, Shopify Capital originated $794 million in 2020, and with a blistering first quarter, it may be on track to originate over a billion dollars this year.

“Shopify’s momentum continued into 2021 as digital commerce tailwinds remained strong and merchants took advantage of the range of capabilities offered by our platform,” Shopify CFO Amy Shapero said in an earnings statement. “We are focused on building a commerce operating system that will help shape the future of retail. Our merchant-first business model positions us to capture the massive opportunity presented by the growth of digital commerce, benefiting both our merchants and Shopify.”

Overall, total revenue for Q1 was $988.6 million, a 110% increase year over year. Nearly a third of the posted revenue was small business lending and MCA funding.

Loan Fraudsters Resorting to AI Generated Faces

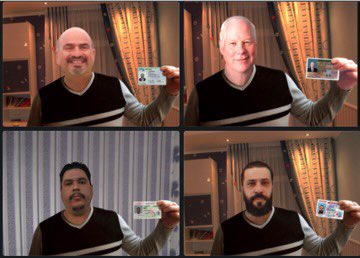

April 27, 2021 According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

“Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?” Blake wrote in a tweet. “Here are four ‘applicants’ seeking a loan.”

Four pictures showing computer-generated “business owners” all have the same sweater, but different heads. People are using AI tech to create randomized, just barely discernible pics of borrowers holding IDs beside them to beat new compliance measures.

It’s like a techno arms race between an automated scanning system that looks for fakes versus an automated fake ID and person generator that tries to make passable fakes.

After a year of PPP and EIDL success stories and fraud concerns, funders are still beating back scam artists. During a recent U.S. Senate hearing, SBA Inspector General Mike Ware said his office had secured $2.1 billion in fraudulently claimed PPP and EIDL loans.

In related news, the SBA announced the $28.6 billion Restaurant Revitalization Fund applications would open on Monday, May 3. Fraudsters start your fake restaurant owner generators.

Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?

Here are 4 different “applicants” seeking a #ppploan. pic.twitter.com/kdbLmNGlvt

— Brock Blake (@BrockBlake) April 26, 2021

Move Over PPP, There’s a New Gov Grant in Town

April 23, 2021 We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

The $1.9 trillion American Rescue plan signed last month set aside $28.6 billion toward the Restaurant Revitalization Fund. Just like PPP, the fund will dole out refundable grants up to $10 million to the most hard-hit food-related businesses.

Since PPP funds tend to run out quickly, the SBA apportioned $500 million just for merchants with less than $50,000 gross receipts in 2019. $4 billion will be set aside for the $50k- $500k bracket and $4 billion toward the $500k- $1 million bracket.

During the first 21 days of the program, the SBA will also focus efforts on disadvantaged businesses controlled by veterans, women, or those that suffer bias due to race or ethnic prejudice.

Just as in the PPP program, eligible businesses will have to devote the grant toward business expenses. That means payroll, loan financing, utilities, supplier, and equipment costs. Only companies that have survived the pandemic thus far with a physical location are eligible. The stipulations forbid a recipient to use funds to open a new venue.

Recipients will have to spend the money before the SBA end date, possibly December 2021 or later, or they will have to return the funds. The program is not live yet, but rumor has it will be opening in late April.

420: SAFE Banking Cannabis Finance Bill Passes House

April 20, 2021 De-banked cannabis firms are a step closer to being danked.

De-banked cannabis firms are a step closer to being danked.

The house of Representatives voted to pass the SAFE Banking Act in a partisan vote 321-101. The bill protects legitimate cannabis businesses from federal sanctions and regulations that bar banks from funding cannabis firms.

The law will pass to the Senate, where it failed to get support last year (and the year before) when it was lumped into a trillion-dollar stimulus plan that the GOP blocked over the summer.

But now, as a standalone bill, supports believe it has a chance to succeed, enabling cannabis firms to delve into institutional coffers and directing federal regulators to create guidelines to supervise weed banking.

“We are grateful to the bill sponsors who have been working with us for the last eight years to make this sensible legislation become law,” said Aaron Smith, CEO of the National Cannabis Industry Association. “The SAFE Banking Act is vital for improving public safety and transparency and will improve the lives of the more than 300,000 people who work in the state-legal cannabis industry.”

Time may be running out for alternative finance to fund cannabis firms before more traditional finance gets in. Advocates believe the bill should go through the Senate Banking Committee and pass before the end of the year.

The American Bankers Association has lobbied aggressively for the bill.

“Banks find themselves in a difficult situation due to the conflict between state and federal law, with local communities encouraging them to bank cannabis businesses and federal law prohibiting it,” the group wrote in a letter to lawmakers on Monday. “Congress must act to resolve this conflict.”

President of Fora Financial on New Credit Facility

April 19, 2021 Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

“Covid was really a kick in the pants,” Gutman said. “How we were doing at the time, our strategic plans were out the door, our growth plan shuttered.”

Flash forward to April 2021, Fora announced a new $100 million credit facility: Not just back on track but finally ready to pursue the plans from a year ago.

“The first months were rough; after the pandemic started, we lost our securitization facility,” Gutman said. “But we kept going, originating aggressively. By around June or July, we started to feel competitive again and rebounded; we started bringing people back– hiring back staff that was furloughed.”

Gutman said the firm was able to change the winds, and by December they were not far off from where they were in 2019. Now set up finally for the aggressive growth plan they had laid out before Covid, Gutman said that though the pandemic threw everything to the wind, Fora still had the capital to back up a good book of business when everything else failed.

Can’t Wait For An Inheritance? Someone Will Fund You

April 19, 2021 Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

For some, the aftermath of losing a loved one can turn into a long drawn out legal process and delay the transfer of rightfully owed inheritance in the process. Probate funders fix the problem, paying cash upfront, purchasing the future receivable of a will. The small industry is remarkably similar to the merchant cash advance world and uses the same terminology. “Inheritance Cash Advances are not loans,” one website says, “with an Inheritance Cash Advance, we send immediate cash to heirs in exchange for an assignment of a fixed dollar amount of their eventual inheritance.”

David Horton, a University of California-Davis law professor who delved into 1,119 probate agreements in the San Francisco area as part of a UPenn Study, said of the product “in almost all cases, with rare exceptions, the lender not only gets their advance back but also gets a huge markup.”

Interestingly, this type of funding is most popular in California, where some of the most complicated estate laws in the country make inheriting a hassle. But a less than flattering industry profile in Consumer Reports says that such companies “earn millions offering cash advances to heirs, with effective interest rates as high as 490 percent.”

And yet, industry advocates say that they are providing a needed service. “We are proud of the service we provide and the highest ethical way we conduct our business at IFC,” said Doug Lloyd, CEO of Inheritance Funding Company to Consumer Reports. “It is easy to understand why banks and other financial institutions are not in this business.”

His company has already advanced more than $200 million to customers. The following video is featured on their website:

Selling Finance Door-to-Door During Covid

April 9, 2021 This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

“We just went back into lockdown. The whole province, everything just shut down,” CEO Patrick Labreche said. “We were getting 20 to 30 new cases a day, and then it jumped to like 200 a day.”

Meanwhile, 110 miles down south at deBanked, de Blasio announced NYC public beaches would be opening up by Memorial Day. Because of the wide range of government shutdowns this past year, Labreche said it is hard to admit to some that his business is booming.

“I was having a conversation with a guy who does payment processing, he makes residuals on his customers, and so his book of business was not making any money right now; he’s hurting,” Labreche said. “So it’s kind of hard to tell a guy like that that we’re flourishing, and maybe you should come work with us.”

Labreche said that the processor was actually going to work with Canadian Financial. Success this past year came from leveraging the interpersonal skills that make an excellent door-to-door salesperson thrive, Labreche said.

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

With a team of salespeople connected through weekly department meetings and messaging groups to keep the energy up, the deals kept rolling in throughout covid. Labreche said his firm is set apart from a good portion of Canadian alt finance: they offer a smorgasbord of financial products directly to the borrower instead of using lead generators.

While most fintechs think all business owners want a one-button final product, Labreche attests to the opposite- his firm sends out salespeople to make sure businesses know they have a rep to rely on.

“I have nothing bad to say about aggregators; that’s their business model, not ours,” Labreche said. “Our business model is going into a business that didn’t even know that the solution was available. When you’re looking online, you’re looking for a solution that you already know is available.”

Labreche favors traditional finance. His firm offers MCAs and other alternative forms of funding but said those are mostly band-aid solutions and he regularly sees MCA deals taking advantage of merchants. For example, Labreche said he walked into an ESCO gas station last month, and through talking to the owner, discovered an opportunity. The owner had taken an MCA from a big Canadian firm but was confused about the cost of capital- he thought he was paying 17%, but Labreche read a recent statement and discovered the rate was really 50%.

“Right there and then he was like, ‘oh my God, that’s crazy I didn’t know,’ he was misled, and it’s like that across the board. So I ended up getting him a quarter-million dollars at four and a half percent on a term loan,” Labreche said. “Nobody’s ever walked into his business or called him, offering him traditional money. We feel like there’s a huge underserved, undereducated market.”

This week, walk-ins have become less of a possibility, with a lockdown banning all non-essential travel. Still, business development manager Julian Hulan looked forward to when things would open back up. He had masked up and gone out on sales calls throughout the year when the government wasn’t in shutdown mode. Recently he traveled to 20 car dealerships to offer financing in a two-day period and said he found merchants excited to see him in person instead of over email.

“They were like ‘oh, I can actually sit down and talk to this guy?’ and that’s when they eat it up,” Hulan said. “They know because they’ve already made that connection face to face, they can call me directly. We don’t do this whole 1-800 Number. You’re going to call me directly and if I don’t answer, you leave me a voicemail, I call you back, it’s that personal relationship between me and that client.”

Industry Ponders: Broker Blacklisting, or Certification?

April 5, 2021 It’s a concept that’s been thrown around the industry for years- swapped like business cards at meetups, conventions, and chatrooms. Shouldn’t there be a broker certification, database, or even blacklist for known bad actors?

It’s a concept that’s been thrown around the industry for years- swapped like business cards at meetups, conventions, and chatrooms. Shouldn’t there be a broker certification, database, or even blacklist for known bad actors?

As deBanked petitioned the question, the industry responded with its naturally diverse responses. The problem: bad actors can keep getting away with shenanigans. The solution? Well, no one size fits all approach could work in the alternative finance industry, but a certification source may do the trick.

CEO of FundFi, Efraim “Brian” G. Kandinov, recently brought up the idea of a “Datamerch for Brokers.” Like a DNC list, Kandinov said there has got to be a way to sort out the known bad actors, scam artists, and even the brokers that play the funding houses by training merchants.

“I think opposed to a blacklist: a list that notes bait and switches, where the merchant was coached by the broker,” Kandinov said. “This way can go around a lawsuit or any fear of that, and the funder is free to choose once reading others’ notes.”

Kandinov said that most of his “problem files” show signs of brokers coaching merchants to start protesting deals after the clawback period ends. Get paid, pass the smell test during a 30-60 day waiting period, and then tell the merchant to jump ship on the deal or argue to lower the payments.

“If they were not [suddenly going out of business], they were calling in like a schedule to lower their payments. No way it can be that uniform unless they were being coached. The broker comes off as the good guy that he played the funding houses,” Kandinov said. “I think harsh means are necessary to expel these guys from the industry.”

Other funding side members of the industry have voiced their support for some type of broker record database. Kristen Ferrara, Director of Underwriting at The LCF Group based in New York, said that LCF pays a high expense to select ISOs. A vetting platform could be a great resource.

“I think it would be a good resource for funders,” Ferrara said. “We turn down about 50% of the ISOs who try to sign up with us. This resource could save funders millions of dollars in deals going bad from ISOs over-promising or committing fraud.”

“I think it would be a good resource for funders,” Ferrara said. “We turn down about 50% of the ISOs who try to sign up with us. This resource could save funders millions of dollars in deals going bad from ISOs over-promising or committing fraud.”

On the other side of the country in San Diego, CEO David Leibowitz from Mulligan Funding said he is all for a way to help funders vet brokers. Mulligan is lucky to work with a trusted brokers network and drops a client like a broken elevator at the first sign of fraud or unethical behavior, he said.

“We are extremely careful about which brokers we do business with. If we see any kind of practice that we think is unethical, we’ll cut a broker loose in a heartbeat,” Leibowitz said. “Is there value in the sort of thing you’re talking about? I think there probably is because I think it makes vetting brokers for [funders] a lot easier, and it also allows brokers to differentiate themselves against their competition by their ethics.”

Leibowitz is a proponent of ethics as an indicator of value and said a certification could help members of the public tell the difference between good and bad funders and let funders spot good ISOs and bad ISOs.

A worry for some is that whatever company, organization, or site that hosts a broker ledger could face lawsuits for liability, could accept payments to make bad reviews go away, list competitors to hurt them, or be outright ignored by an industry always hungry for deals.

But industry lawyers seem to agree that a broker certification or blacklist would ultimately benefit the industry if provided from the right source. Patrick Siegfried, the Deputy General Counsel at Rapid Finance, said that whatever agency would be rating brokers would need its own trusted reputation.

“To have a legitimate background or rating system, it needs to be done by an independent third-party that has its own credentials,” Siegfried said. “I think that’s a big reason you don’t see many third-party or private rating systems.”

Siegfried said one option that ensures a true third-party point of view is a government agency taking care of a broker tracking system. Another option would be an industry coalition, but then it’s a question of cost- Who is paying to staff and maintain a complaint system?

Siegfried said one option that ensures a true third-party point of view is a government agency taking care of a broker tracking system. Another option would be an industry coalition, but then it’s a question of cost- Who is paying to staff and maintain a complaint system?

“At the end of the day, having a good industry regulator is a benefit for the industry,” Siegfried said. “It will allow a third-party, government entity to vet brokers in terms of licensing and then maintenance, looking into valid complaints.”

As conversations across the country point toward a licensing regime, Siegfried said it’s a sign the industry is maturing and that one day there will be a government agency to lodge complaints with and to actually vet brokers in the space.

Steve Denis from the Small Business Finance Association (SBFA) proposed a solution to the issue. He said that in the works right now is an SBFA-sponsored certification program.

“We started just looking at brokers and thinking about how to certify them,” Denis said. “We think that it’s the time, from the feedback we’ve gotten from regulators, that we launch a true industry-wide certification.”

In the coming months, brokers may be able to apply for certification when the program rolls out. Instead of a ‘blacklist,’ Denis said brokers could set themselves apart as trusted providers by going through a basic background test or industry knowledge checks.

“If you’re a broker and you can’t get certified, then there’s probably some issues,” He said. “So our hope is if you carry a certification, that’s sort of a message that you are a good broker.”

When it comes to government regulation, Denis said he is still cautious. While he 100% expects certification programs to crop up for state licenses, he thinks no government agency can achieve what an industry coalition can do.