Articles by deBanked Staff

FTC Forum on Small Business Financing & Merchant Cash Advances

May 7, 2019At the FTC Forum on Small Business Financing & Merchant Cash Advances this morning, FTC regulators asked questions of a panel of industry representatives about controversial topics, including the use of COJs. Below are some closely paraphrased responses.

On Confessions of Judgment (COJs)

Scott Crocket, Founder & CEO, Everest Business Funding

The role of COJs is a conversation worth having. What’s the right balance?

We choose only to use them for deals of $100,000 or more. And COJs apply for only 3% of our business. So if there was a ban on COJs, it wouldn’t really affect us. It might just limit the amount we would fund.

The Bloomberg stories are not representative of what we do. We don’t file a COJ when a business is slowing down, but only when we suspect fraud.

Jared Weitz, CEO, United Capital Source

90% to 95% of our deals do not include COJs. And for those where we do use COJs, we give merchants a document that has a description of what it is so that they’re comfortable with it. We tell them that they have to be comfortable with it before they take it.

Jesse Carlson, Senior Vice President & General Counsel, Kapitus

After we saw the extent of the use of confessions of judgement by certain individuals/companies, as a trade association, we at the Small Business Finance Association (SBFA) decided to include in our code of conduct a ban on the use of confessions of judgement if you’re a member of the SBFA.

Part of the reason why we do include COJs is because we’re very careful with our underwriting.

On True-ups

Jesse Carlson

We have 5 to 10 employees who speak with merchants when they are having unforeseen financial challenges and we’ll adjust their ACH repayment. Some companies treat the percentage of the company’s sales as an absolute. We’ll offer them modifications.

Scott Crocket

We remind merchants that the true-up is available.

Ami Kassar, Founder & CEO, Multifunding LLC

Many funders are not as forgiving as these funders say they are.

Kate Fisher, Partner, Hudson Cook

Some MCA funders reached out to merchants affected by the hurricane in Texas and the forest fires in California to adjust their payments.

Jared Weitz

Other funders stopped requesting payments altogether from merchants who were affected by these natural disasters.

Brokers / Aggressive Marketing

Jared Weitz

A broker of an MCA deal has to give the commission back if the merchant fails within 90 days.

Jesse Carlson

We work with about 100 brokers/ISOs at a given time and we do background checks on them.

Scott Crocket

We do background checks on brokers and we monitor their behavior. We don’t hesitate to cut off a relationship with an ISO. We do spot checks, but we don’t monitor every ISO every day.

The Federal Trade Commission hosted a forum on small business financing including loans and merchant cash advances to examine trends and consumer protection issues in this marketplace.

The forum began at 8:30am and concluded at 1pm. Among some familiar names that spoke are:

- Jared Weitz, CEO, United Capital Source

- Scott Crockett, Founder & CEO, Everest Business Funding

- Christian Spradley, Head of Policy & Senior General Associate Counsel, OnDeck

- Kate Fisher, Partner, Hudson Cook

- Ami Kassar, Founder & CEO, Multifunding LLC

- Jesse Carlson, Senior Vice President & General Counsel, Kapitus

- Sam Taussig, Head of Global Policy, Kabbage

- Lewis Goodwin, Banking Lead, Square Capital

Square Originated $508M in Business Loans in Q1

May 1, 2019Square Capital, Square’s business lending arm, originated 70,000 small business loans for a total of $508 million last quarter, according to their recent earnings report.

As a payments company first, Square processed $22.6 billion in gross payment volume in Q1 and generated a net loss of $38 million on $959 million in revenue.

Shopify Capital Issued $87.8M in Merchant Cash Advances in Q1

April 30, 2019Shopify’s small business funding division, Shopify Capital, issued $87.8 million in merchant cash advances in the first quarter of 2019, according to the company’s earnings report. The figure is a 45% increase over the same period last year. Overall, the company has funded more than $535 million in MCAs since inception.

Shopify is primarily an e-commerce platform, but they are quickly becoming a competitor to both Square and PayPal, both of whom also offer funding solutions.

Has PayPal Eclipsed OnDeck in Small Business Loans?

April 26, 2019

It’s been said that Kabbage is on pace to surpass OnDeck in small business loan originations, but PayPal has already done it.

When PayPal announced a working capital program in the Fall of 2013, few were predicting that the initiative would propel them to the top of the small business lending charts. Just two years later, however, the payment processing giant had already loaned more than $1 billion to small businesses.

Today, that number is over $10 billion, according to a comment made by PayPal CEO Dan Schulman on the company’s Q1 earnings call.

That figure would suggest that they had loaned approximately $9 billion from Fall 2015 to the end of Q1 2019. OnDeck, by comparison, loaned $7.5 billion since Fall 2015 through Q4 2018. Several other data sources, including previous statements from PayPal that they had surpassed more than a billion dollars in quarterly small business funding in 2018 (already more than OnDeck), indicate that PayPal has become #1 on the deBanked small business funding leaderboard.

PayPal’s growth was helped in part by its acquisition of Swift Capital in 2017.

Two of the top four are payment processors:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| PayPal | $4,000,000,000* | $750,000,000* | ||||

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate

< 5% Annual Returns On Small Business Loans?

April 25, 2019 If you were to invest in small business loans with 4-year terms, what kind of return would you hope to get?

If you were to invest in small business loans with 4-year terms, what kind of return would you hope to get?

Retail investors that put their money in a mix of high-risk and low-risk loans on Funding Circle’s UK platform should expect to achieve a return of 4.5% to 6.5% a year (after defaults and 1% servicing fee), the company recently announced. That’s down from their previous projections. Meanwhile, their conservative loans could achieve returns of 4.3% to 4.7% a year.

A Marcus By Goldman Sachs savings account in the UK by comparison earns 1.50%

Funding Circle explained in a blog post that the returns could actually be higher or lower than projected.

To-date, investor interest has continued to grow with peers on the platform investing £1.5 billion in 2018 and £419 million in the 1st quarter of 2019.

More Than Half of Small Businesses Seek Less Than $100,000 in Financing

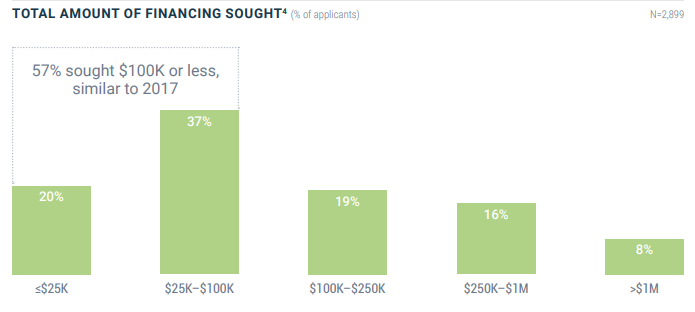

April 22, 2019 Small businesses need capital in small doses. That’s a takeaway of the latest study published by the Federal Reserve that revealed 57% of employer firms (with less than 500 employees) that applied for financing in 2018, sought $100,000 or less. 20% sought less than $25,000.

Small businesses need capital in small doses. That’s a takeaway of the latest study published by the Federal Reserve that revealed 57% of employer firms (with less than 500 employees) that applied for financing in 2018, sought $100,000 or less. 20% sought less than $25,000.

56% of all financing applicants said they applied in order to expand their business or pursue a new opportunity while 44% said the funds would be used to meet operating expenses.

47% of employer firms that applied for credit received all of the financing they sought. 19% said they received less than half of what they needed and 22% said they didn’t get anything at all.

Unsurprisingly, those that received nothing were categorized as high credit risk. The Federal Reserve defined that category as having a FICO score less than 620 or a business credit score between 1 and 49.

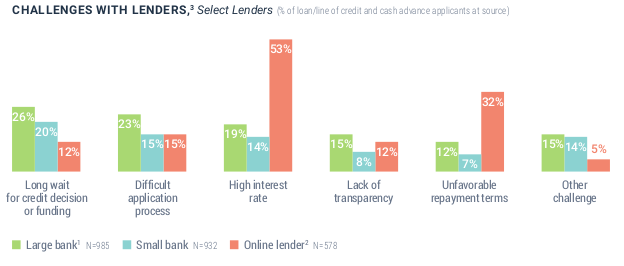

Small Businesses Rank Online Lenders More Transparent Than Big Banks

April 16, 2019When it comes to business loans, small businesses say online lenders are more transparent than big banks.

Specifically, 15% of respondents to a Federal Reserve survey reported challenges with transparency experienced at big banks versus only 12% with online lenders. Small businesses also ranked big banks worse on credit decision wait times, application process difficulty, and other unspecified challenges.

The Federal Reserve survey examined small businesses with less than 500 employees.

Small banks fared the best on transparency, payment terms, and interest rates.

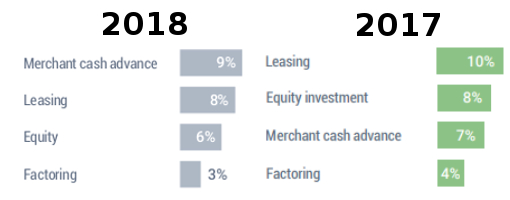

Merchant Cash Advances Surpass Leasing As Goto Financing Option for Small Businesses

April 16, 2019

More small business applied for merchant cash advances in 2018 than they did leasing, factoring, or equity investments. That’s according to a recent Federal Reserve study of small businesses with less than 500 employees.

Nine percent of applicants applied for merchant cash advances in 2018 while only 3% applied for factoring. Leasing dropped year-over-year from 10% in 2017 to 8% in 2018.

On average, merchant cash advances were approved 85% of the time compared to business lines of credit (73%), business loans (67%), and SBA loans (52%). Six percent of all small businesses surveyed said they used merchant cash advances on a regular basis, versus 9% for leasing and 3% for factoring.

Unsurprisingly, small businesses overwhelmingly still sought loans or lines of credit. Of those surveyed that applied for any type of financing in 2018, 85% applied for a loan or line of credit and 28% applied for a credit card.

You can download the Federal Reserve’s complete report here.