Articles by deBanked Staff

Are Subprime Auto Loans Showing Cracks or Not?

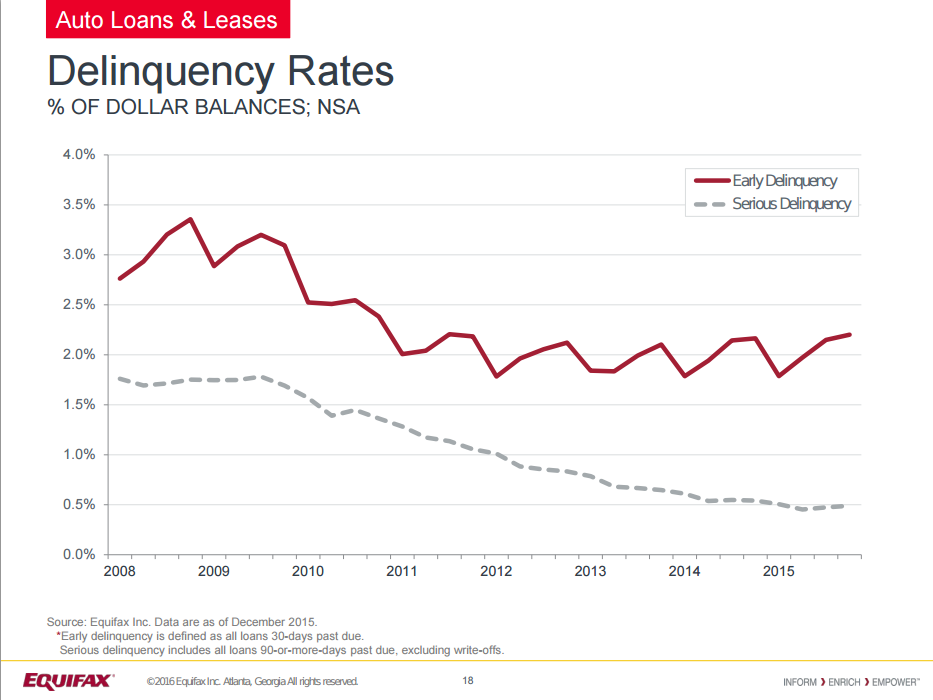

March 19, 2016 Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Fitch attributed this to weaker underwriting standards as well as sharp origination growth and increased competition.

The prime sector is mostly stable, they say. Further weakness is anticipated across all credit categories, though the outlook is stable.

But while Fitch spoke of weaker underwriting and nearly unprecedented delinquencies, consumer credit reporting agency Equifax spun a different picture just four days later when they announced the results of their own auto lending study.

“Lenders are making more informed lending decisions and the underwriting process has been strengthened as a result of new data and technology that is available to the marketplace,” said Amy Crews Cutts, chief economist at Equifax.

Indeed, the rates of both early delinquency and serious delinquency as a percentage of dollar balances are nowhere near recession levels, at least according to Equifax’s data set.

Both Fitch and Equifax agree there has been an increase in auto loan originations.

In a WSJ interview, hedge fund manager Ben Weinger said that demand for auto debt has led lenders to systematically loosen underwriting standards.

Equifax’s Cutts recently said however that “credit performance is still excellent, showing that lenders are prudently extending credit to well-underwritten borrowers.”

Who’s right?

Minority Small Business Owners Have More Income but Less Credit?

March 18, 2016 A third of minority small businesses are run by women and nearly 45 percent of all minority-owned businesses are from California, Florida and Texas.

A third of minority small businesses are run by women and nearly 45 percent of all minority-owned businesses are from California, Florida and Texas.

And most of them run restaurants and beauty services and their average credit score is nearly five points lower than the average for the general small-business population, even though they earn higher and are heel-to-heel in credit card delinquencies. 1.2 percent of minority small-business owners have at least one business credit card account that is severely delinquent (91-plus days) compared to 1.1 percent of the general small-business owner population. And the average consumer income for minority business owners is $92,489, more than the average income of the general small business owner of $92,338.

Credit-reporting company Experian in its new study on small businesses, however said that minority small business owners fall behind on managing credit — 15 points lower than the overall average for small-business owners, to be precise. The report does not explain why.

But “Gaining insight into the trends and behaviors of the small-business community is imperative given its importance to the growth and success of our overall economy,” said Pete Bolin, director of consulting and analytics for Experian, which also released tools and resources on credit management.

The market of lending to minority small business owners is well recognized. Apart from the SBA micro loans and community advantage loans that seek to bridge the gaps, the ‘Equal Credit Opportunity Act’ prevents lenders from discriminating against borrowers based on race and sex.

Bizfi Partners With West Coast Banking Group

March 17, 2016Bizfi will be the exclusive alternative finance solutions provider for small businesses that are members of the Western Independent Bankers, a trade association of community banks in the west coast.

Small businesses in the midwest and west coast in states including Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage.

“WIB member banks are the leading funders of America’s small businesses,” said Michael Delucchi, President and Chief Executive Officer of WIB and WIB Service Corporation. “With Bizfi as a WIB Premier Solutions Provider we are able to offer their expertise in alternative financing and superior technology to our member banks and deliver a complete solution for small business funding.”

Earlier this month, Bizfi partnered with The New York State Restaurant Association to provide business financing for its 2,000 small businesses in the restaurant space.

Funding Circle To Expand Bay Area Staff

March 17, 2016 P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

The company plans to hire 20 people in risk and compliance, product engineering and sales teams. Funding Circle’s marketplace connects borrowers, mostly small business merchants and investors. The company makes money in origination and servicing fees.

The San Francisco-based company was founded in 2010 in the United Kingdom and was launched in the US in 2013. It employs 550 people globally and has so far funded $2 billion to 15,000 businesses.

Earlier this month, Funding Circle announced that it hired former Executive Board Member of the European Central Bank (ECB), Jörg Asmussen, to join its board. This aligns with the company’s streak of boosting manpower. Last year, it hired top executives from Barclays and American Express to head its global risk and analytics team.

OnDeck, UK Trade Group Work on Fintech Policy

March 17, 2016 Don’t look now but OnDeck is getting knee-deep in fintech policy.

Don’t look now but OnDeck is getting knee-deep in fintech policy.

The online lender said that it will partner with UK’s Innovate Finance, a fintech trade group to launch a Transatlantic Policy Working Group to exchange intelligence and information on regulatory and policy issues governing fintech.

The group will work on universal fintech issues like the use of data, building a payments infrastructure for financial inclusion, open source APIs in banking and automated investment advice through robo advisors, when kicking off its first meeting at Google’s Washington DC office.

“The transatlantic policy working group represents a great opportunity to share key insights, best practices and knowledge between US and UK fintech stakeholders,” said Daniel Morgan, head of policy and regulation at Innovate Finance “It will help drive real change in the public policy arena when it comes to the development and growth of a vibrant fintech sector.”

Venture capital investment in fintech companies more than doubled last year compared to 2014, hitting an all time high of $14 billion, up 106 percent from $7 billion in 2014. The UK attracted a total of $623 million in fintech investment in 2014 and Innovate Finance committed to increasing that number to $8 billion by 2020 in venture and institutional investment.

Fed’s Steady Interest Rates: What Does This Mean for You?

March 16, 2016The Federal Reserve kept interest rates unchanged citing a global economic slowdown and market volatility in the US.

The central bank kept the benchmark federal funds rate at 0.25-0.5 percent and scaled back forecasts of higher interest rates noting that the economy is exposed to the “uncertain global economy.”

What does this mean for online lenders? Not much directly as marketplace lenders don’t use the prime rate as a benchmark. But by association, it could affect demand for loans, credit performance and capital supply as the Fed rates play with investors’ expectations of yield.

But a small increase in rates wouldn’t have affected the industry too adversely. “Given the cushion we’ve already built into our loan pricing, we don’t plan to increase rates if there’s a small shift in the base rate,” Sam Hodges, co-founder and managing director of Funding Circle told WSJ last year, ahead of the rate hike in December.

But policymakers expect the central bank to raise rates by 0.5 percent by the end of this year. Will that affect be of any consequence? Hard to tell.

Banks Admit They’re Scared of Startups

March 16, 2016If you cannot keep up with everything that is happening in fintech, you are not alone.

In the post financial crisis world, fintech startups perched themselves in the crevice between the big world of banks and the regulatory reform which controls their free reign. And since then, financial upstarts have only multiplied.

From P2P insurance, realty crowdfunding, marketplace loans and not to forget bitcoin, the capital infusion in fintech testifies for the market hype. In its report in November last year, CB Insights estimated that $24 billion has been invested in fintech startups and half that amount ($12.2 bn) was invested in 2015 alone.

It can be argued that some of these startups with multibillion dollar valuations are essentially smaller banks without the frills. Take SoFi for example, the San Francisco-based online lender is which worth $4 billion known for its touting we-are-not-a-bank image but provides most services from student loans, mortgage lending, personal loans to loan refinancing without the “bank branch.” The company also wants to start a hedge fund.

So, are the banks feeling left out? It depends on whom you ask, but a recent report from PwC surveying 544 CEOs, revealed that 23 percent believed their businesses were “at risk” by fintech innovation and 67 percent of the respondents said that they were under profit margin pressure.

“We thought we knew our customers, but FinTechs really know our customers,” the report quoted a senior bank official as saying. The report ranked consumer banking, payments and wealth management to be disrupted the most by these fintech startups.

The big bucks and the hype that follows it has made regulatory authorities sit up and take notice of the financial services upstarts and bring them under the supervisory purview. And while that may be legitimizing their foothold on the industry, the real questions around project revenues, possible exits and the companies’ wherewithal to handle a complex credit market remain unanswered.

Are we really at a tipping point of innovation or is it just new wine in old bottles?

FINRA Issues Best Practices for Robo Advisors

March 15, 2016 Robots will manage assets worth almost $500 billion by 2020.

Robots will manage assets worth almost $500 billion by 2020.

And since 2020 isn’t far, the Financial Industry Regulatory Authority (FINRA) has turned its attention towards the robo advisory industry and issued best practices for firms offering digital tools for wealth management.

Although companies are not legally bound to follow them, the regulator’s advisory guidelines outline regulatory principles in areas crucial to the business of digital investment advice.

Algorithms

FINRA suggested firms supervise and govern algorithms used in robo tools meticulously. “At the most basic level, firms should assess whether an algorithm is consistent with the firm’s investment and analytic approaches,” the report said.

Portfolios & Conflict of Interest

Manual approvals and supervision of portfolios proposed by tools is key. The report suggested that companies monitor the pre-packaged portfolios and assess its appropriateness for different investors. Herein, FINRA recommended customer profiling based on risk capacity and risk willingness.

Rebalancing

FINRA’s effective practices for automatic rebalancing recommended establishing customer intent on automatic rebalancing, disclosing to customers how the rebalancing works and apprising the customer of the potential cost and tax implications of the rebalancing.

Training

Robots are not fully infallible yet and the regulator endorsed training professionals on permitted use of digital tools, being fully aware of its assumptions and limitations and judging its suitability for a client accordingly.