Articles by deBanked Staff

Finn & Co, Inc. To Manage Two New Equity/Debt Funds

December 14, 2017Below is a letter that was circulated by Finn & Co, Inc.

Finn & Co, Inc. is pleased to report the formation of two new equity/debt private equity funds to be managed by our firm. The first of these two funds is a US$100M equity fund which will seek investments in the MLM Industry (multi-level-marketing). This fund will be seeking and entertaining opportunities in North and South America as well as Europe. It is the intention of the fund to have heavy concentrations of ownership in relatively few investments and in addition to the contribution of the invest cash, it is the intention of the fund to offer geographical business partnerships with Asian ‘like-type’ MLM entities. The second fund is a US$200M debt/equity fund engaged in lending to the MCA Industry (merchant cash advance). This fund will offer senior debt, sub-debt and equity investments to the MCA industry here in America and in specific areas of Asia. The management of these funds will embrace additional industry experienced individuals and hopes to ‘fill a void’ of available capital for these traditionally difficult ‘to bank’ business endeavors.

Finn & Co. Merchant Banking Activities at this time.

Please review the following activities of our firm in the areas of consulting, merger and acquisition assignments and current capital fundraising activities. Finn & Co. has recently completed valuations for operating companies engaged within the Direct Sales/MLM industries and that of aerospace and defense. In addition, we are currently engaged with multiple capital raising assignments for companies within the following industries: Nutrition Products, Merchant Credit Advance (MCA), Medical services, Tobacco, Fish Farming, Oil Refinery, Lodging, Technology, Consumer Water Bottlers and the financing of Credit Card Receivables. Finn & Co., Inc. has active M&A assignments detailed later in this communication. We welcome your inquiries for valuation assignments, merger and acquisition advisory services, and capital fundraising needs.

Merger and Acquisition Assignments:

(1) Binocular Manufacturers: The Purchaser is a manufacturer of ‘high end’ binoculars, ground, airborne and maritime Electro-Optic/Infrared cameras sold primarily to the military and law enforcement communities. This acquirer is engaged in the design, development and sale of advanced optical devices to expand its domestic and international sales and is seeking manufacturers of related devices targeting the commercial, law enforcement and military markets. Asian and European-based manufacturers of binoculars and vehicle cameras are of a particular interest to this acquirer. In addition, the buyer is interested in the purchase of optics companies with strong R&D personnel — specializing in the development of binoculars, rifle scopes, and any and all related advanced EO/IR technology. This acquirer will entertain joint-ventures in place or in lieu of outright purchase or merger.

(2) Fish Processing Companies: The acquirer is an international integrated fishing enterprise engaged in catching, processing, and value-added functions in the worldwide fishing industry. This company desires to acquire a value-added fish processing company located in the USA. The desired company will be profitable at the time of purchase, selling into the retail market, restaurants, and the cruise ship sector of the marketplace.

(3) Health Care:

- (A) Seeking Acquisition Targets operating in business process outsourcing, employment, staffing, billing, surgery centers, and ancillary services to health care industry. The target platform company should have an EBITDA of between US$5M and US$20M.

- (B) Home Health & Hospice: Seeking a home health and hospice platform acquisition in any Geographical area, if the acquisition target enjoys US$3.0M in EBITDA or more AND Management team is willing to remain with the company post the acquisition is completed.

- (C) Large, publicly traded NYSE ‘for profit’ hospital ownership and management company seeking additional ‘hospital’ acquisitions and/or management contracts. While any ‘locale’ will be entertained, the States west of the Mississippi River are preferred.

(4) Multi-Level-Marketing Industry/Direct Sales: We continue to seek North American, Latin American and Asian-based operating MLM/direct selling companies for various buyers and investors. We have multiple buyers of nutritional products, cosmetics, personal and health care companies, lingerie sellers, fashion jewelry and other consumable products. The targeted acquisition or investment opportunity can range in annual sales size from US$25M to as large as multi-hundred million dollar sales companies located in the USA. We have interest in direct sales/MLM companies with annual revenues of US$10M or greater located outside the continental boundaries of the USA. These American and non-American buyers are either currently operating MLM entities or are the investment arm of non-USA based MLM operating companies, all of which have a long and “in-depth” operating knowledge of the industry and are anxious to expand their businesses into the USA, Canada, Latin America and/or Asia. The buyers or investors are prepared to purchase 100% of any entity or are prepared to partner with a seller that wishes to maintain some equity ownership and a management role. Our buyers will require at least 51% equity ownership.

(5) Nutritional Products

- (A) Manufacturers (third party): We are seeking third party nutritional products manufacturers of tablets, capsules, powders, gels, and liquids. There is a particular interest to acquire a liquids manufacturer at this time. The targeted companies should possess the appropriate industry certifications and conform to recent government-imposed manufacturing processing requirements. The targeted companies will have annual sales of US$15M or larger.

- (B) Branded Nutritional Products: Sold via retail chains, direct through mail order or online. The more ‘direct’ the sale method of delivery, the stronger the interest from our buyer.

(6) Food

- (A) Hispanic Food Suppliers: Our client is an acquirer of North American-based manufacturing and distribution companies offering Hispanic foods and related items to the wholesale or retail marketplace. The candidate will have a known brand name and an obvious presence in the Hispanic community and a recognized name or product to the Hispanic food buyer.

- (B) Restaurant Chains: A currently operating restaurant team is seeking restaurant chains with annual sales of US$50M or more and EBITDA of US$5M or more. The target chain could be an independent restaurant concept, a franchisor, or a franchisee. Minority Recaps/and or Growth Equity will also be considered.

- (C) Branded Food companies: We represent a financial buyer of ‘branded’ food companies. The targeted candidate will have annual sales sufficient to generate an EBIT of US$10M or greater. The food offering can be across a wide spectrum of food offerings and will be considered a national brand.

(7) Aerospace/Defense:

- (A) We have multiple buyers seeking aerospace and defense operating companies that will range in annual sales size from US$20M to US$250M. The ideal candidate will currently be a supplier of materials and/or parts to the aerospace after-market, manufacturer of such parts and supplies, a provider to the aerospace/defense industry and/or engaged in a business relationship within the industry that allows it to participate in any of the ongoing support and/or replacement vendor positions in this after-market sector.

- (B) In addition to our above targets, we represent a US$200M sales company, privately-owned, seeking an aerospace manufacturer. Tight tolerance machining and/ or the manufacturing of aerospace/defense parts are the two areas of interest. Turnarounds and under-performing companies will be considered. The preferred size target is an entity generating revenue of US$25M to US$250M.

- (C) We represent a buyer of “Type Certificates” of established aircraft. These airplane types are currently in operation but not in production and range from piston propeller, turbo propeller and/or jet engine type aircraft.

- (D) Security Companies: We are seeking businesses that offer services to the military or law enforcement markets associated with intelligence gathering, manufacturers of security equipment, service companies that are engaged in the guarding and maintaining of premises, sea-going security in the area of anti-piracy and other related services.

- (E) Hand Gun, Rifle and Shotgun Manufacturers: We are seeking USA and/or Western European hand-held weapons manufacturers. There is a particular interest on the part of the buyer in a manufacturer that is currently supplying its weapons to the military and/or law enforcement communities.

The financing of ‘gun’ or related companies in today’s banking marketplace is most challenging. Finn & Co. is in a position to offer short and long term credits as well as growth capital to gun industry-related operating, profitable companies. If you or your clients are in need of working capital or acquisition capital, we would be most pleased to work with you.

- (F) A&D, Medical Products or Photonics Industries: Our Client is seeking a USA-based manufacturing operation in the highly regulated aforementioned industries. Acquisition opportunities with annual sales/revenues of up to US$100M and EBIT of US$10M are the size range of our client’s investment interest.

(8) Oil and Gas

- (A) Service and Support Companies: We are seeking North American-based oil and gas industry service and support companies. The targeted prospect might offer a service for ‘on-shore’ or ‘off-shore’ drillers, maintenance of wells, work-over and stimulation of wells, transportation and security management. The targeted company could be solely domestic or international in its operations. Our clients have a decided interest in targeted acquisitions that represent what would be defined as the larger participants in the industry, in short ‘the bigger the better’.

- (B) Large Oil and Gas proven properties seeking a sale or requiring large capital investment. These properties will be domestic locales with proven oil and/or gas reserves that can be currently producing or not. The buyer/investor will entertain the outright purchase of the property or a joint venture with the current owners.

(9) Trailer Manufacturers and Distributors: We are seeking manufacturers and/or distributors of ‘open and closed’ commercial trailers that would traditionally be pulled by a pickup or SUV and used in a wide variety of activities, both for commercial and private family purposes. Our client has a present interest in acquiring additional closed box trailer manufacturers or large distributors.

(10) Water Treatment Companies: Manufacturers of water treatment equipment, new technologies for the purification of water, and companies offering deliveries of commercial water supplies. All water related opportunities entertained.

(11) Consumer Products, Consumer Durables, Retail or Retail Services: We have a buyer of companies in the aforementioned sectors (logistics, e-commerce, etc.). The minimum required EBITDA is US$3M.

(12) Risk-based Consulting Services: Our client is a platform entity engaged as a provider of risk-based consulting services including – Internal Audit, IT Audit, Information Security, Corporate Governance and Regulatory Compliance. Our client would like to grow their business with the acquisition of similar type functioning companies both domestic and international.

Family Related Operating Companies:

Tethys Corporation: a holding company that has as its investment criteria the acquisition and/or investment in the aerospace/defense/medical or medical service industries. Tethys will also entertain ‘control’ investments in security companies and/or service companies servicing the military, diplomatic or international work-place.

Blue Steel Ventures, www.bluesteelventures.com. This ‘alternative’ wholesale funder of the Merchant Cash Advance (MCA) industry is a provider of senior debt, sub-debt and equity investments to established operators of merchant cash advance providers. Blue Steel Ventures will entertain loans and investments of US$2M to US$30M or more subject to the specifics of the MCA applicant.

Board Assignments:

Members of the Finn & Co organization currently sit on Boards of Directors or finance committees of various commercial and non-profit companies and/or organizations. We particularly wish to expand our assignments of Directors and Members of the Board of commercial companies here in the USA. We are prepared to entertain appointments to private or public corporations, located anywhere in the USA. Any inquiries or suggestions that you might wish to offer would be warmly received.

We would be most pleased to hear from you concerning your interest and needs for any of our consulting services, capital raising or M&A activities listed in this communication. We look forward to hearing from you.

Sincerely yours,

Kenneth R. Finn

Chairman

Finn & Company, Inc.

Kenneth R. Finn

Finn & Co., Inc.

Merchant Bankers

5776-D Lindero Canyon Road, #382

Westlake Village, CA 91362

(818) 219-3097(818) 219-3097

krfinn2001@yahoo.com

Wyoming Location

4350 Fallen Leaf Lane

Jackson, WY 83001

(307) 203-2556(307) 203-2556

krfinn2001@yahoo.com

Judge Okays Leave to Add Additional Defendants in Kalamata Capital / Biz2Credit Lawsuit

December 12, 2017A three-year-old lawsuit pending in the New York Supreme Court has experienced a flurry of motion practice, according to the docket. The latest order issued by the Honorable Kelly O’Neill Levy granted Kalamata Capital leave to amend the complaint to include both Direct Lending Investments, LLC and Direct Lending Income Fund LP as defendants.

A key claim in this case is the allegation of tortious interference. A previous legal brief on the matter can be read here.

The case can be found in the New York Supreme Court under index number 653749/2014.

Yellowstone Capital Surpasses $2 Billion in Originations

December 8, 2017Jersey City-based Yellowstone Capital has surpassed $2 billion in originated deals. The milestone was announced Thursday evening at the company’s year-end holiday soirée.

The company was founded in 2009.

Yellowstone Capital Funds $100 Million Over Last 60 Days

December 1, 2017An email circulated by Jersey City-based Yellowstone Capital yesterday, confirmed that the company had originated $50 million in deals for the month of November. The figured tied the record set in the previous month, bringing the 60-day total to $100 million.

Two sales representatives ended up in a tie for top performer of the month, each originating $4.65 million. Juan Monegro, whom deBanked interviewed almost two years ago, was right behind them at $4.55 million.

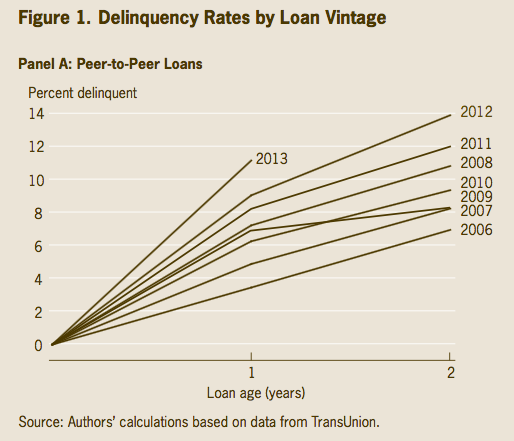

Cleveland Fed Retracts Their Report on P2P Lending

November 18, 2017Here’s something you don’t see every day. A paper published by the Federal Reserve Bank of Cleveland about peer-to-peer lending was so dubious, that it has been taken down.

Since working paper no. 17-18 and related commentary on peer-to-peer lending were posted on our website on November 9, the authors have received several questions about the composition of the underlying data set they used in their analysis. In light of the comments received, the authors are currently revising their paper to further clarify the data sample they used in the study. Their revised paper will be posted as soon as it is completed.

– Federal Reserve Bank of Cleveland after analysts poked major holes in their findings

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

“This chart shows that the lowest delinquencies from P2P loans occurred in 2006. Really?” Renton wrote on his blog. “I am sorry but this is just plain wrong and I challenge the authors to show me the actual data this is based upon. In 2006, the only consumer P2P lending (or any significant online lending) platform in existence in this country was Prosper and their 2006 vintage was terrible.”

Nat Hoopes, executive director of the Marketplace Lending Association (MLA), was even more vocal. In an op-ed he wrote for American Banker, Hoopes says, “In our view, this paper — ‘The Taste of Peer-to-Peer Loans’ — and its accompanying materials show that a lack of precision and understanding of subject matter can result in significant inaccuracies. The report’s authors presented findings that seemed to reflect issues with the P-to-P industry, but they actually relied on data from a much broader category of loans. The result was a misleading and brutally critical report about the P-to-P industry that was actually based in part on data from more traditional loans.”

Online lenders had reason to fret over the report as the Cleveland Fed did more than just publish charts. “P2P loans resemble predatory loans in terms of the segment of the consumer market they serve and their impact on consumers’ finances,” the Fed concluded. “Given that P2P lenders are not regulated or supervised for antipredatory laws, lawmakers and regulators may need to revisit their position on online-lending marketplaces.”

The worst offense, according to MLA’s Hoopes, was that the data the Cleveland Fed relied on was not even p2p lending data. A senior VP at Transunion had reportedly admitted that the data used comprised of both traditional loans and online loans that had been requested by the Fed a long time ago to use for a different study.

Oops.

Check Out The Preliminary Agenda of Broker Fair 2018

November 15, 2017The preliminary agenda of Broker Fair 2018 was published to the event’s website on Tuesday evening. While subject to revisions between now and May 14th, Broker Fair is already shaping up to be the hallmark event for the MCA and small business lending industry. Fifteen sponsors have already signed on including National Funding, RapidAdvance, and Funding Metrics as Platinum-level and CFG Merchant Solutions as Gold-level.

Broker Fair 2018 will be the largest gathering of merchant cash advance and business loan brokers in the country. Until now, there’s never been anything like it.

To register, sign up online or contact Sarah@brokerfair.org

We hope to see you in Brooklyn at The William Vale in May!

Update 4-26-18:/strong> Most recent version of the agenda below

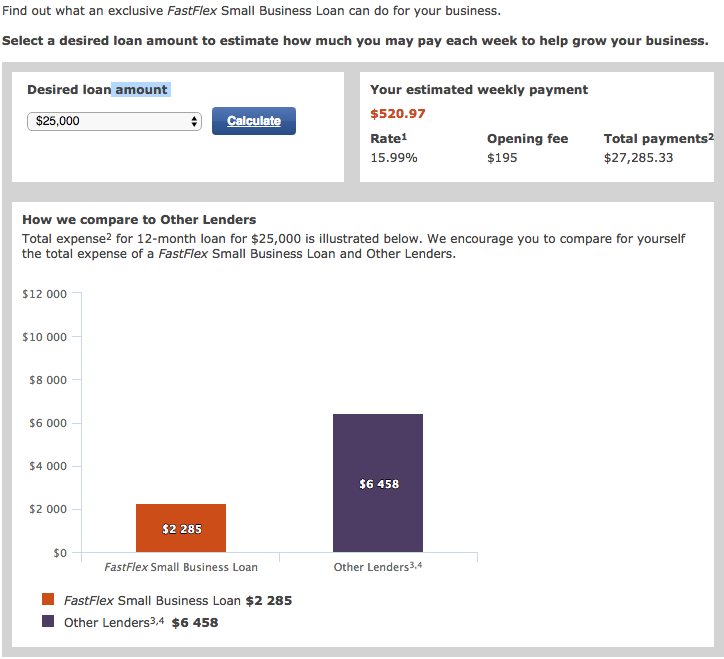

Don’t Forget About FastFlex

November 13, 2017 The OnDeck-Chase partnership isn’t the only game in town when it comes to fast weekly payment bank loans. Wells Fargo announced their own program, called FastFlex, in 2016 as part of a goal to lend $100 Billion to small businesses over five years.

The OnDeck-Chase partnership isn’t the only game in town when it comes to fast weekly payment bank loans. Wells Fargo announced their own program, called FastFlex, in 2016 as part of a goal to lend $100 Billion to small businesses over five years.

deBanked was shown an anonymized bank statement snippet recently of a merchant that was purportedly being debited daily by Wells Fargo. So we reached out to Wells to ask if there might be a daily payment loan product that had not yet been announced.

“[F]or Wells Fargo’s FastFlex Small Business Loan, we only offer the weekly payment option, in which required payments are made on a weekly basis automatically deducted from the customer’s business-deposit account,” they responded. “None of our Small Business loan products have daily payments.”

While the mystery remains unsolved, Wells already compares its FastFlex product to OnDeck, Kabbage, and CAN Capital on their website. Loan amounts ranging from $10,000 to $35,000 come with 1-year terms, weekly repayment, and interest rates starting at 13.99%. Their loan calculator approximates a 1.09 total cost factor on a $25,000 loan.

Their underwriting criteria comprises of cash flow history, existing credit obligations, credit experience, payment history, and relationship status with Wells Fargo. Merchants are funded the day after accepting the terms.

Users on a handful of message boards have reported that cash flow history weighs heavily in the approval.

MCA Funder Asks Court to Set Aside Default Judgment in Usury Case

November 10, 2017If it wasn’t for the Usury Law Blog, an MCA company may never have known about the default judgment entered against it in Florida for usury, according to documents filed in the case.

On Wednesday, the funding company filed a motion to set aside the default judgment and reopen the case on the basis that the in-house attorney handling the case for them left the company in September. The company had no way of receiving case notices after he left, they say, because the attorney had used a non-company email address as the email of record with the Court.

The funding company’s new attorney only became aware of the case when the Usury Law Blog published an analysis of it, they say.

The Court has initially denied their motion without prejudice on the basis that procedure requires that they certify that they have conferred, or describe a reasonable effort to confer, with the parties affected in good faith effort to resolve the dispute. Presumably, the funder can refile the motion once the defect has been cured.