|

Related Headlines

| 10/19/2021 | Intuit Introduces Money by Quickbooks |

| 09/13/2021 | Intuit to acquire Mailchimp |

| 02/22/2021 | LoanMe,Liberty Tax to take on Enova, Intuit |

| 11/25/2020 | DOJ approves Credit Karma/Intuit deal |

| 08/25/2020 | Intuit revenue up 13% |

Related Videos

Intuit and Prosper Marketplace - Ep. 75 |

Stories

Intuit Originates $452M in Business Loans in FY Q3 2024, Has Excellent Portfolio Performance

May 27, 2024Intuit generated $452M in business loans in its recent fiscal quarter ending April 30th. That was down slightly from the $469M in the quarter before it. Apparently the performance of its business loan portfolio has been excellent. Not only did the company say that “past due amounts were not material” but it also said that the allowance for losses on these loans was also immaterial. Similar to the prior quarter, this segment of Intuit’s business did not even come up once during the earnings call.

Intuit’s business loan originations are roughly on pace with Shopify Capital’s, at somewhere in the neighborhood of $2B a year. Both companies benefit from a sticky core product that their customers use. In the case of Intuit it’s the Quickbooks bookkeeping software.

Intuit’s CEO, Sasan Goodarzi, opened the quarterly earnings announcement by saying that AI is changing the world. “The era of AI is one of the most significant technology shifts in our lifetime and our strategy to be the global AI-driven expert platform is delivering significant benefits to our customers and strong results across the company,” Goodarzi said. “I’m proud of our innovation and performance, and because of our momentum, we are raising Intuit’s revenue, operating income, and earnings per share guidance for the fiscal year.”

Intuit Experiences Big Business Loan Surge

February 26, 2024Intuit experienced a significant surge in small business lending activity, according to the company’s most recent earnings report, originating $469M in FY Q2 2024 (which ended Jan 31, 2024) which was up from $279M in FY Q1 2024. That’s a jump of nearly 70%! Intuit makes these loans via Quickbooks Capital through a partnership with WebBank. The increase warranted no mention during the earnings call.

The positive sentiment echoes that of its rivals, including Square Loans and Enova who both just reported their biggest quarters ever for originations.

Intuit’s SMB Loans Relatively Flat Year-over-Year

December 18, 2023Intuit originated $279M worth of term loans to small business for the fiscal quarter ending October 31. This is down from the $314M originated over the same time period last year.

“As of October 31, 2023 and July 31, 2023, the allowances for loan losses on term loans to small businesses were not material,” the company wrote in its earnings report.

Further, Intuit said that “In August 2023, we entered into a forward flow arrangement with an institutional investor. Pursuant to this arrangement, we have a commitment to sell to the institutional investor a minimum of $250 million in participation interests in unsecured term loans purchased or made to small businesses over the next 18 months, subject to certain eligibility criteria.”

Intuit did not raise its term loan program on its earnings call nor did analysts ask about it.

Here’s how Intuit’s flat SMB loan originations stacks up against some of its direct competitors:

Square Loans – Steady

PayPal – Significant pullback

Shopify Capital – Significant increase

Intuit Originated $933M in Small Business Loans in FY 2022

April 5, 2023Intuit, the software company often associated with Quickbooks, originated an astounding $933M in small business loans in its fiscal year 2022. That’s up substantially from the $232M it originated in FY 2021.

It’s important to note that the company’s fiscal year 2022 ended on July 31, 2022 which means more data exists beyond that time. From Aug 1, 2022 – October 31, 2022, the company originated $314M in business loans. In the quarter that followed (Nov 1, 2022 – Jan 31, 2023), Intuit renamed the easily identifiable line item from “originations and purchases of term loans to small businesses” to “originations and purchases of loans” which may bear some significance given that it indicates a steep increase to $701M for that quarter, a record for Intuit by far. If that was entirely business loans then it would place Intuit amongst the largest small business lenders in the country.

Intuit Originated $232M in Small Business Loans in Fiscal Year 2021

August 30, 2021Intuit, the producer of QuickBooks and owner of Credit Karma, originated $232M in small business loans for the fiscal year of 2021 that ended on July 31. That was slightly below fiscal year 2020’s $243M and down significantly from 2019’s $316M. Cumulatively, however, the company has originated approximately $928M since it started lending at the end of 2017.

QuickBooks Capital requires that applicants have their bank accounts connected to the QuickBooks software and revenue of at least $50,000 over the past 12 months. APRs can range anywhere from 9.99% APR to 34% APR.

Intuit completed its acquisition of Credit Karma at the end of last year. Credit Karma generated a quarterly record revenue of $405 million.

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

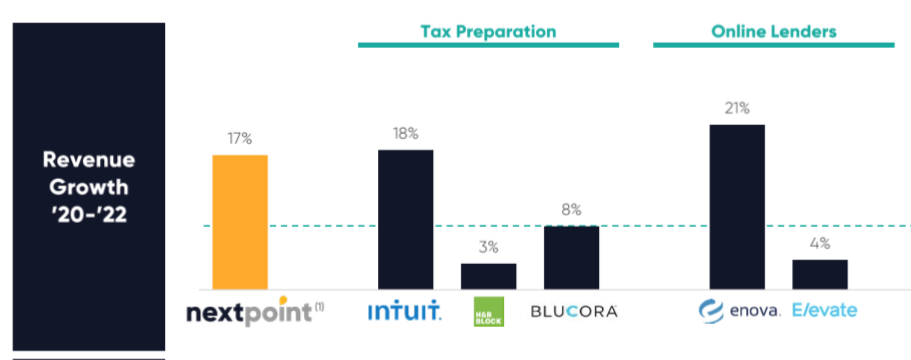

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.

Square, Stripe, Intuit, Shopify, Talked SMB Lending at LendIt Fintech 2020

October 8, 2020 The LendIt Fintech digital conference last week was a sign of the times. This year, millions of average businesses and consumers have had to go virtual: they had no choice. 2020 has been a year of struggle and survival, and a time of great fintech adoption.

The LendIt Fintech digital conference last week was a sign of the times. This year, millions of average businesses and consumers have had to go virtual: they had no choice. 2020 has been a year of struggle and survival, and a time of great fintech adoption.

Some firms have been more successful than others. Going full digital, LendIt introduced virtual networking at the conference- the first day alone saw 2,171 meetings. Zoom meetings and virtual greetings took the place of handshakes and elevator pitches that would regularly accompany the convention.

On day three, LendIt hosted a panel of SMB lending leaders from Stripe, Shopify, Square, and Quickbooks Capital. Bryan Lee, Senior Director of Financial Services for Salesforce, served as moderator and he focused the discussion on “How the leading fintech brands are adapting.”

THE PIVOT

Lee began the talk by asking Eddie Serrill, Business Lead from Stripe Capital, about how the industry has pivoted.

Serrill talked about how Stripe was powering online interactions and saw an influx of traditionally offline businesses switching over to their platforms. Stripe also saw an increased demand for online purchases and payment.

“We’ve been trying to find that right balance between supporting users that have been doing incredibly well,” Serrill said. “While trying to support our users who are seeing a bit of a setback.”

Stripe introduced a lending product in September of last year and now SMBs can borrow from Stripe and pay back by diverting a percentage of their sales, much like the other panelists’ companies offer.

Jessica Jiang, Head of Capital Markets at Square Capital, talked about how her firm adjusted. Square reacted to fill the niche of their underserved customers by introducing a main street lending fund, serving industries hard hit by the pandemic, Jiang said. Small buinesess that relied on in-person action like coffee shops and retail community businesses were given preferential lending options.

Product Lead at Shopify, Richard Shaw, said that this year his firm learned to be prepared for anything. Everything that Shopify was potentially going to do or planning on implementing in the coming years suddenly became a here-and-now necessity.

“We tore up our existing plans,” Shaw said. “It was like the commerce world of 2030 turned up in 2020. You need to do ten years of work, but you need to do it today.”

Shopify, the Canadian e-commerce giant has doubled in value this year. The firm launched Shopify Capital in the US and Canada in 2016 and has originated $1.2 billion in funding to small businesses since that time.

Luke Voiles, the VP of Intuits QuickBooks Capital, talked about how his team handled pandemic conservatively.

“Five years of digital shift has happened instantaneously due to COVID,” Voiles said. “Intuit is pretty recession-resistant in the sense that you have to do taxes, you have to do your accounting, and the shift to digital helps a lot.”

Business lending was different, Voiles said, as soon as his team saw COVID coming, they battened down the hatches, slowed lending, and pivoted to facilitating PPP.

PPP

Voiles said the craziest thing he has seen in his career was what Quickbooks did to deploy PPP aid.

Within about two weeks, almost 500 people from across Intuit came together to shift all the data they carried on customers to aid applications.

“We were uniquely positioned to help solve and deploy that capital,” Voiles said. “We have a payroll business where 1.4 billion business use us, we have a tax business where we have Schedule C tax filings, and we have a lending business. We were able to pivot and put the pieces together quickly.”

QuickBooks Capital deployed $1.2 billion to 31,000 business in a process that Voiles said was 90% automated. Now customers are awaiting other rounds of government aid.

Square’s Jiang said the initial shutdown weeks in March and April saw hundreds of Square team members working on PPP facilitation through the night and weekends. As the funds dried up those first two weeks, it was clear to Jiang the program was favoring larger firms and higher loan amounts, leaving out small businesses.

“That’s typical of investment bankers, but not very typical of tech,” Jiang said. “PPP is a perfect example of how small businesses are continuing to be underserved by banks.”

THE SHAKEOUT AND THE FUTURE

2020 has been a major shock to the lending marketplace. Voiles from Quickbooks said the amount of work it took to make it through the first wave was a significant shakeout.

“You’ve seen what’s happening with Kabbage and OnDeck and other transactions with people getting sold; there is a shakeout happening in the space,” Voiles said. “The bigger players will make it through and will continue to help small businesses get access to capital that they need.”

When asked about the future roadmap of QuickBooks Capital, Voiles said it wasn’t just about automating banking. Using Intuit’s resources to build an automated system is only half of the picture- the firm believes in an expert-driven platform. After the automated process, customers will be able to talk to an expert to review the data, and “check their work.” Voiles said Quickbooks wants to offer a service that is equivalent to the replacement of a CFO.

“These small businesses that have less than ten employees, they can’t afford to hire a pro,” Voiles said. “They need automated support to show them the dashboard and picture of what their business is.”

Pointing to Stripe’s online infrastructure, Serrill exemplified what successful lenders will offer next year: a platform that combines many needs of SMBs in one place.

“I think it’s really about linking all of this data, making it super intuitive and anticipating the need for their users, so they don’t need a team of business school grads to manage their finances,” Serrill said. “So they can get back to building the core of their business, not figuring out whether they have enough cash flow tomorrow.”

Jiang said the future of small business would be written in data, contactless payments, and digital banking. She sees consolidation in the Fintech space and has a positive outlook on bank-fintech partnerships.

The FDIC granted Square a conditional approval for the issuance of an Industrial Loan Company ILC in March this year. Jiang outlined plans on launching an online SMB lending and banking service next year called Square Financial Services if the conditional charter remains in place.

For Shopify’s future, Shaw was excited to look forward to the launching of Shopify balance- a cash flow management system, and Shopify installment payments. He reiterated that the success of Shopify’s lending division was due in part because making loans was not the entire business.

“Shopify Capital is one piece of a wider ecosystem,” Shaw said. “All these things together are more powerful than individual parts.”

Intuit Agrees to Buy Credit Karma For $7.1 Billion

February 26, 2020 This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

This week the news broke that a deal had been reached between Credit Karma and Intuit that will see the latter purchase Credit Karma for $7.1 billion, paid for with cash and stock. After rumors of the deal leaked over the weekend, the agreement was confirmed on Monday by chief executives from both companies.

Under the deal, Credit Karma will continue to operate as a stand-alone business and its CEO, Kenneth Lin, will stay on and run the company. Beyond that, some believe that the merger will see Intuit rise as a go-to platform for financial services. Owning TurboTax as well as Mint, tools for filing taxes and budgeting, respectively, the addition of Credit Karma, which allows customers to view their credit score for free, would advance Intuit’s product suite as well as bolster the data it already has on users.

“There hasn’t been that much innovation in the financial services world in the past two decades,” Credit Karma Founder and CEO Kenneth Lin said. “The combination of the two companies will really be able to move consumers forward.”

Credit Karma claims to have 100 million customers, with half of all American millennials being included within that number. It also states that it has over 2,600 data points on each customer, including their social security number as well as loan history. The company makes its money by selling customer information to third parties who advertise new credit cards and loans on the Credit Karma site. Credit Karma also receives a couple of hundred dollars for each card and loan that is acquired through ads on its site. Being one of the few tech startups that actually turn a profit, Credit Karma claimed to have received $1 billion in revenue in 2019.

Speaking on the deal, Intuit’s CEO, Sasan Goodarzi, said that “This is very core to what we’ve declared around helping our customers make ends meet and make smart money decisions.”

Lucky Or Prepared?... luck is what happens when preparation meets opportunity. -seneca production month in and month out is typically peak and valley for ordinary per... |

Best Application For Tracking Deals... intuit quickbooks, and obviously excel, , feel free to reach out if you need bookkeeping / accounting help, , dassi cole, better accounting solutions, 347-416-3928... |

See Post... intuit (owner of quickbooks) so it was great to help with the accounting side. you can integrate it with achworks as well. i send out the nacha files directly to the bank so i can notified of miss payments much quicker than using a 3rd party like achworks, , is this difficult to d... |

See Post... intuit (owner of quickbooks) so it was great to help with the accounting side. you can integrate it with achworks as well. i send out the nacha files directly to the bank so i can notified of miss payments much quicker than using a 3rd party like achworks... |