Archive for 2020

Lawyers Chime in On What a Biden Administration Could Mean for Merchant Cash Advance

November 30, 2020 In the weeks following the election, the news cycle has been heavily focused on the presidential transition’s legal aspects.

In the weeks following the election, the news cycle has been heavily focused on the presidential transition’s legal aspects.

Instead of worrying about vote recounts, merchant cash advance (MCA) companies are considering what legal changes, if any, might come after Jan 20th. Will the Biden administration spell the beginning of new regulations on the world of business to business financing?

Lawyers say that while the industry is waiting on Georgia to decide the Senate’s fate, increased regulation at the federal is unlikely to occur.

“If the Republicans hold in Georgia, and we have a split legislative branch, that means gridlock, and gridlock is great for the industry,” Catherine Brennan, partner at Hudson Cook, said. “The more progressive wing of the Democratic Party would like to put merchant cash advance under the auspices of quasi-consumer [loans,] but they won’t be able to do that with the split legislative branch.”

Brennan has a wealth of experience as a commercial finance compliance and litigation lawyer and regularly contributes to the national conversation on alternative and fintech law topics. She said that even if Democrats control the Senate, moderates may still hold back progressives from making new regulatory laws.

“There’s some moderate Democrats who understand the need for this market, they understand the product, and their constituents, in particular, use the product,” Brennan said. “I don’t see anything at the federal level that should be viewed as an existential threat to the ongoing existence of the industry.”

What Brennan does see as more likely, is the gradual adoption of MCA under preexisting executive agencies like the CFPB and FTC. She pointed to the Dodd-Frank Act implementing consumer lending data collection as a possible avenue regulators might take by pushing for data collection in the MCA space.

What Brennan does see as more likely, is the gradual adoption of MCA under preexisting executive agencies like the CFPB and FTC. She pointed to the Dodd-Frank Act implementing consumer lending data collection as a possible avenue regulators might take by pushing for data collection in the MCA space.

Still, Brennan insists that MCA firms will be OK so long as they understand the FTC can already look into commercial finance practices and that it has gone after ISOs in the past. She sees that as the number one development from a regulatory standpoint because the FTC will ultimately review what took place in the financial service markets during the pandemic and decide if action is warranted. Still, if funders have been responsible and fair, they should be in a good place.

Brennan did say that the position might be up for grabs when it comes to the head of the CFPB. The previous leader, Richard Cordray, fought with the Trump administration against his re-appointment, believing his position surpassed the president’s authority to fill. Of course, it did not, and Cordray was removed, but there is nothing stopping the Democrats from re-appointing him, Brennan said, especially when other appointees may give up valuable Congressional seats.

James Huber, a partner at Global Legal Law Firm specializing in collections, believes that even if the Senate is somehow blue and passes regulation, that MCAs that are playing by the rules would benefit. The MCA business was born under the Obama administration during the last financial crisis, and if Biden beefs up the CFPB, it would only hurt payday lenders, Huber said.

“It certainly flourished under Obama, so one might think now that it’s got its foothold and it’s here you can almost guarantee that it’s going to continue to do really, really well when there’s stricter regulation,” Huber said. “Your typical deBanked cash advance technology company: I think they’re going to do well with their bread and butter product…”

Huber said that especially when we’re seeing businesses hurting for cash right now, b2b finance will thrive. Huber was worried about Biden’s talk about bankruptcy reform, however.

“Biden’s talked about bankruptcy reform, to make it easier for people to go through bankruptcy, and yield assets like their houses and their cars and things that,” Huber said. “That’s a concern; that would mean that you’re fraudulently applying for a loan, and that’ll be accepted. It slows down collection efforts; our main role in the MCA business is on [defaults].”

Katherine Fisher, a Hudson Cook partner who, alongside Brennan, has deep experience in MCA representation and compliance, agreed with her colleague that funders need to make sure they keep an eye open toward compliance when it comes to regulation.

“Firms that have not focused on the regulatory process need to start, and companies that have looked at it need to revisit it,” Fisher said. Funders should “expect to be comfortable if they are asked to describe how they comply and prepare to do so.”

But beyond that, she sees no doomsday event on the horizon; even if the Senate is no longer Republican-controlled, it would be up to the FTC and CFPB to set the tone. If the CFPB, for example, pushed for data collection under 1071 of the Dodd-Frank Act, it might signal a more attentive regulatory environment for MCA and factoring.

But beyond that, she sees no doomsday event on the horizon; even if the Senate is no longer Republican-controlled, it would be up to the FTC and CFPB to set the tone. If the CFPB, for example, pushed for data collection under 1071 of the Dodd-Frank Act, it might signal a more attentive regulatory environment for MCA and factoring.

Compared to 2008, when the last Democratic administration took office, MCA wasn’t on the radar, Fisher said. Now that it is on the map this time around, especially after MCA funders proved how vital they were to the SMB market during the pandemic, there will be more attention on B2B transactions.

But firms only need to think of this as a chance to make sure their practices are healthy, and most of the industry has already shown signs of doing so. Fisher pointed to the FTC’s small business finance forum last year, which included a panel of MCA representatives at the table.

“I don’t think it is a scary time. It’s an opportunity for MCA to improve their processes, make sure they are following the law,” Fisher said. “They don’t need to be afraid but need to batten down. Much of the industry has already done that, the MCA industry has been focused on adopting good practices.”

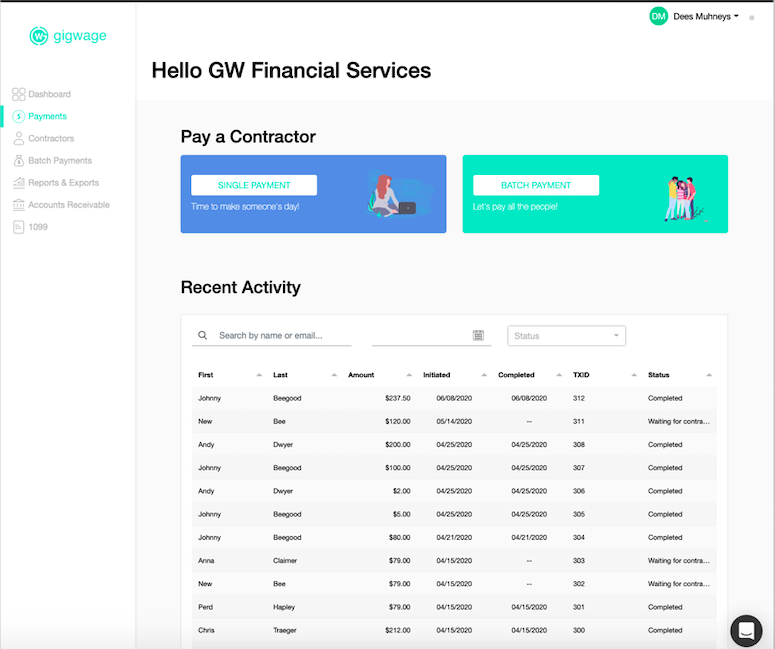

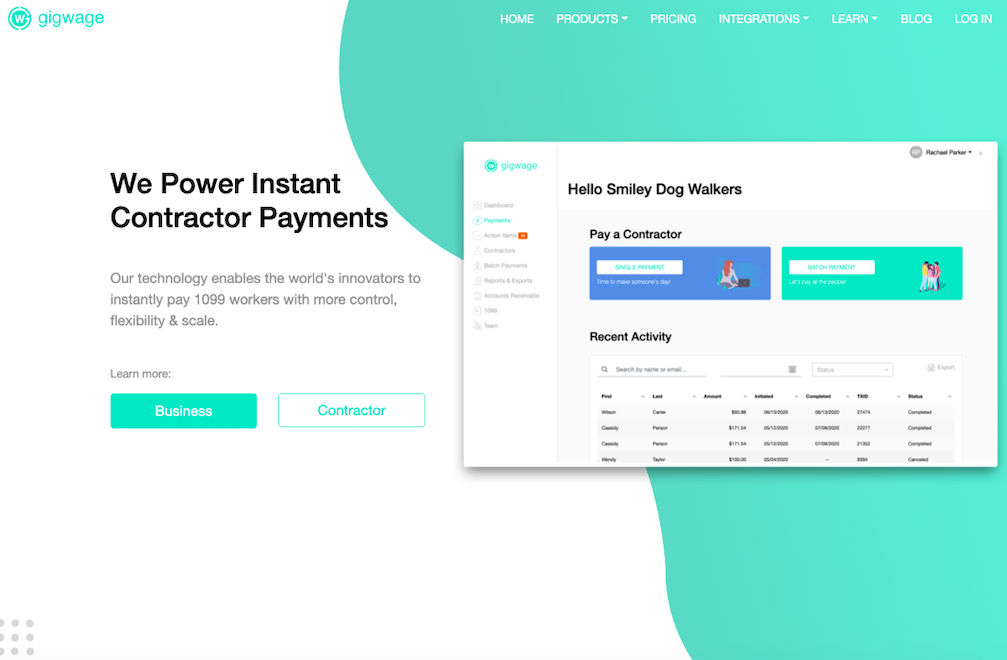

From Sales to Founder: Craig J. Lewis Talks Gig Wage’s $7.5 Million Funding Round

November 27, 2020 Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Lewis made $10 million in payroll tech sales before going on to lead a firm that has seen 30% month-to-month growth this year, during a pandemic no less.

“We help businesses pay independent contractors, but because we’re so tech-centric, it’s evolved beyond just payroll,” Lewis said. “What we ended up building was financial infrastructure for the modern workforce. We help businesses get money from their customers to their contractors as fast and as flexibly as possible.”

The way Gig Wage does this, Lewis said, is by offering an online platform for the hybridization of payroll, payments, and banking from a single login. Businesses can manage their payroll needs for 1099 workers, then shift to payment needs quickly, through direct to debit, all major cards, bank transfers, and accounts receivables.

“One of the only- the only platform in the world actually that has embedded banking into payroll and payments, which is what kind of allows for this speed and flexibility that we offer,” Lewis said. “We’re like B to B to C: We help the businesses with technology and operational excellence, and because independent contractors are separate from the workplace, we provide tools for them.”

Lewis has years of experience in the payroll space- starting as a salesman for ADP small business payroll products back in 2008. Realizing he had a passion for payroll tech and getting customers the best services possible, Lewis went on to learn anything he could about the industry. Selling $10 million in software while moving across the country, Lewis landed in Silicon Valley, where he studied what it took to start a company.

“I was just awed how they thought about technology and products and company building,” Lewis said. “And I vowed to bring that to the payroll industry.”

Lews joined a startup, learned the Silicon Valley way of creating a company through an African American tech acceleration program. In 2014, Lewis founded Gig Wage to do something disruptive in the payroll space.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

“With the maturation of Uber, Lyft, Postmates, Doordash, Grubhub, Upwork, all of these kinds of gig economy freelancer companies, we had great growth going into 2020,” Lewis said. “In Q1, we were set up to raise our series A, and then March happened, and the terms got pulled off the table.”

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

“The gig economy was right there waiting on the workforce to provide opportunities to earn, and we were positioned perfectly to help people compete for that talent and pay people in a modern way,” Lewis said. “The pandemic has been a huge growth accelerant for us, and we think those tailwinds will only continue.”

Those winds of success came during a time of protest. Amplified in the pandemic’s backdrop, the country was waking up to the unequal disenfranchisement black people faced. Only 1% of black founder entrepreneurs ever receive VC funding, and Lewis said he is proud to have raised a significant round, given that unfair stat.

“With so much controversy and negative energy around black people in general,” Lewis said. “I think putting this positive story out there and showing this black excellence, black tech, I think it’s super important, and it’s been something that I’ve embraced. We’ve been able to be a part of putting something extremely powerful and positive into the market.”

America is finally waking up to realize something Lewis said was obvious, that black people matter, even though it can be controversial to say so. He hopes his success can help others but affirms the funding round was no charity drive.

“This is a great opportunity for us to be clear about the fact that like hey, we’ve been working on this, we’ve built a good business and a good technology,” Lewis said. “This is a big business opportunity for our investors and us. It wasn’t charity, right: This isn’t like, oh he’s black, give him some money.”

The successful funding round shows confidence in the Gig Wage platform from Green Dot, which will allow Gig Wage to offer bank accounts and debit services to independent contractors. Green Dot is one of the only fintechs with a national banking license, Lewis said, and Gig Wage is joining the Banking-as-a-Service direction that the fintech industry is headed.

Beyond payroll, Lewis can’t wait to offer other financial products to businesses as the company grows.

“When you think about the gig economy, it’s important that people get paid fast and flexibly: You’ve got to have the cash to be able to do that,” Lewis said. “We see some unique opportunities to get involved in the lending space down the line as well as we continue to build out our technologies.”

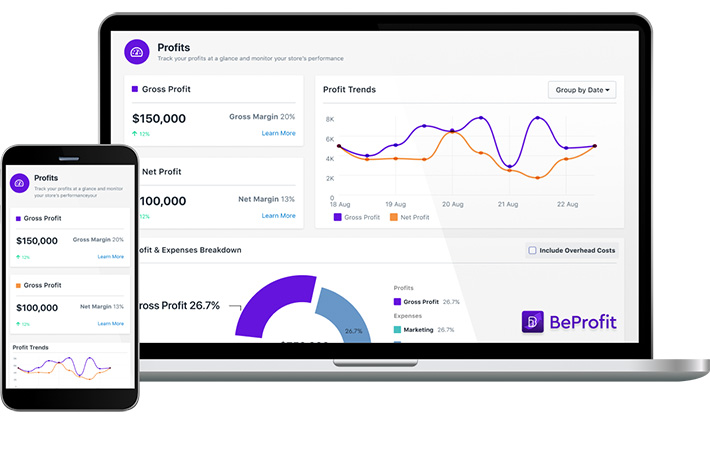

Become Releases a New Shopify App – Beprofit, to Expand Its Offerings to the E-Commerce Market

November 25, 2020 Tel Aviv, Israel – November 25, 2020 – Become, the leading online platform for small and medium businesses to find and optimize their funding solutions, announced today it has released a new Shopify app offering ‘BeProfit’.

Tel Aviv, Israel – November 25, 2020 – Become, the leading online platform for small and medium businesses to find and optimize their funding solutions, announced today it has released a new Shopify app offering ‘BeProfit’.

With the expansion of the ecommerce landscape in light of the coronavirus, Become noticed the need for a single intuitive dashboard that ecommerce sellers can use to track and manage their profit and expenses. With BeProfit, Shopify sellers across the globe can now trace their profits in real time and discover what areas of their business they can optimize to increase their bottom line.

“Creating BeProfit has been a big part of our ‘pivot strategy’ during COVID-19. Building a Shopify app is a totally new and exciting realm for Become,” said Eden Amirav, CEO and Co-founder of Become. “Although offbeat, BeProfit falls in line with our underlying mission – to create a better world of funding for businesses and essentially help business owners become more. Being more profitable is not only something all businesses aspire to achieve but it is also something that will make a business become more fundable down the line.”

With many e-commerce sellers struggling to calculate, map and understand their profits, BeProfit calculates and organizes everything for them in a process that takes a matter of minutes. The app enables sellers to know exactly how much they’re making and spending, and more importantly on what. The dashboard integrates with a number of external sources, such as shipping service providers, external marketing platforms, and payment processors. This results in both visual and dynamic financial reports that update in real-time.

Noam Sinansky, CEO and Co-founder of Spire Jewelry – one of BeProfit’s first users said it’s “the first app that really manages to put in order all the financial information of my store! The app helped me get rid of complicated excel files, it just displays the information in a convenient, simple, and accurate way.”

To learn more about BeProfit, visit apps.shopify.com/beprofit-profit-tracker

About Become

Become, is the leading online platform for SMBs to find and optimize their funding solutions. The company uses its proprietary technology to nurture each business throughout the funding cycle. Become is rapidly growing with near 200,000 loyal business owners registered through its platform. The company has built an ecosystem of more than 50 leading lenders and partners and has facilitated over $285 million in tailored business loans to date.

Become’s latest service is a Shopify App “BeProfit”, organizes complex data into an intuitive and interactive dashboard. Shopify sellers can easily track their profit and expenses to see which areas of their business needs improving in order to become more profitable.

Become is backed by Benson Oak Ventures, Magenta Venture, Viola Credit, RIO Ventures Holdings, Entrée Capital and iAngels. The company has offices in San Francisco and Tel Aviv. For more information, visit: become.co.

Media Contact

Amit Shalgi

shalgi@become.co

+972547331141

Smarter Loans Co-Founder: Study shows Fintech in Canada Seeing Accelerated Growth

November 24, 2020 There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

The findings show an accelerated shift to digital transactions, which Smarter loans co-founder Vlad Sherbatov attributed to a pandemic-acceleration of the tech-leaning trends that were already coming.

“One of the central insights from this year’s study is the overall increase of fintech adoption and lending,” Sherbatov said. “We’ve also noticed the fact that people are just much more likely to manage their finances online today than they were at this time 12 months ago or a year ago.”

Intending to gain insight into Canada’s fintech industry, Smarter Loans began sending questionnaires to their users starting in 2018.

“We survey some of the people that flow through our website that have used a fintech lending product in the past 12 months, we ask them questions about their experience,” Sherbatov said. “The purpose is to extract insights so that we can help push the industry forward and improve it.”

Even just two years ago the industry was a much smaller space but has ballooned since, and the Smarter Loans survey has become a one-of-a-kind focus on Canadian fintech markets. Featured with this year’s results is commentary from Canadian industry leaders like the Canadian Lenders Association, and deBanked’s own Sean Murray.

“It’s become a bit of a staple in the lending industry,” Sherbatov said. “Because it’s the only piece of research in Canada that is laser-focused on fintech lending.”

With three years of data to compare, Sherbatov said he could see a significant increase in online activity. Part of this is just due to where the world is heading, as Sherbatov described the younger generations just stepping into the financial world.

“This is something that’s been happening for years; this is a trend that has started a long, long time ago,” Sherbatov said. “For younger generations, the way that they approach financial products and companies is very different from someone in my generation or older. Online is the standard of doing business, on-the-go, and mobile is the standard of managing your financial affairs.”

Fintech in Canada, Sherbatov said, tends to lag behind the growth of the fintech industry in other countries but is on the rise due to the Coronavirus. The digital adoption trend was pushed forward, as some customers that had been reluctant to bank online were forced to do so by necessity. Now, these changes to the way business is transacted are here to stay, Sherbatov said.

Like the surge in eCommerce activity, people are going online to make financial transactions.

“You go to Amazon to buy laundry detergent, and you go online to open up a checking account to pay some bills,” Sherbatov said. “Everybody needs financial services, just like everybody else needs household items; it’s how we’re going about obtaining them. This has changed and has accelerated due to Covid.”

State of Fintech Lending in Canada Report Reveals Key Information for Lenders

November 23, 2020 Smarter Loans, Canada’s loan comparison giant, has published its 3rd annual State of Fintech Lending report.

Smarter Loans, Canada’s loan comparison giant, has published its 3rd annual State of Fintech Lending report.

“As Canadians stayed home longer, adoption of fintech products has accelerated dramatically,” the report says, accelerating trends that had already been developing for years. The data is based on survey results submitted by nearly 2,600 fintech lending customers.

While there are dozens of important takeaways, respondents indirectly signaled how valuable it is to be among the brands that are found first by borrowers.

That’s because loan applicants said that they researched fewer lenders than ever before (35% only researched 1 or 2 lenders before applying) and they spent less time researching lenders than ever before (31% said they spent less than 1 hour researching). Furthermore, 51% of respondents said that they only applied with a single provider.

This approach worked. Of those that got approved, 89% of respondents said that they were satisfied or very satisfied with their loan provider.

The trend should signal to lenders that borrowers may simply come to expect a satisfactory experience regardless of where they apply and that there is tremendous value in simply being the first 1-2 lenders that a prospective borrower considers.

And hint hint, it pays to be easily discoverable online. Fifty eight percent of respondents said they discovered their loan provider through online search.

Click here to view the full survey results in Smarter Loans’ official State of Fintech Lending.

ROK Financial Announces Direct SBA Loan Access

November 23, 2020![]() Over the past several months the state of the economy has been by no doubt uncertain. With unemployment hitting record highs and Coronavirus cases still on the rise, business owners all across the country have been faced with many difficult decisions regarding their livelihood.

Over the past several months the state of the economy has been by no doubt uncertain. With unemployment hitting record highs and Coronavirus cases still on the rise, business owners all across the country have been faced with many difficult decisions regarding their livelihood.

Finding business financing options during these uncertain times can be challenging and risky to not only business owners, but the banks and lenders they choose to work with.

ROK Financial truly understands the uncertainty a business owner feels during these current times. Having derived themselves from a company split back in August, the team is helping other business owners just like them navigate these unchartered waters.

“We have been working tirelessly with our lenders and partners over the past several months discussing different ways we can continue to better service our clients.” Says CRO, Patrick Manning of ROK Financial “The relationships we have built over the years allows us to become quite versatile with our product offering, in turn allowing us to better serve our business owners. That is why we are extremely excited to announce our exclusive partnership with Doug Hood, SBA Loan Consultant LLC. This unique partnership opens up direct SBA access to clients for SBA products $350,000 and above.”

Doug Hood has been facilitating SBA Loans for more than 35 years, resulting in more than $20 million in SBA Loans distributed to business owners annually. Hood said he connected with ROK via LinkedIn, “I’m on Linkedin way more than I should be, we connected at 10 or 11 o’clock at night, and we hit it off.” Says Hood. Excited at the fact that ROK offers short term financing that Doug himself would now be able to leverage in addition to his SBA Loan offerings for his clients was a win-win.

Doug now sits as the official SBA Loan Consultant under the ROK Financial umbrella for deals $350,000 and above. This unique relationship provides greater opportunities for business owners from purchasing existing businesses, refinancing existing debt, starting a business and much more.

“The worlds of Fintech and SBA have collided for the greater good” says Manning, “streamlining and modernizing a once antiquated process, which eliminates the frustration that comes along with long-term lending.”

—————

Megan Capobianco

press@rokfi.com www.rokfi.com

3500 Sunrise Highway

Building 100, Suite 201

Great River, NY 11739

833-337-6534

deBanked Meme Time – Happy Thanksgiving

November 21, 2020It’s Thankgiving time, which means…. more deBanked memes! This tradition started 8 years ago. Enjoy the holidays and be safe!

How Start-Up Founder Andrew Luong Went From House Flipper to Real Estate CEO

November 19, 2020 Andrew Luong said it all started seven years ago in San Francisco, just out of graduate school investing in real estate with his spare time on the weekends. Today, his startup Doorvest manages more than $20 million in real estate assets.

Andrew Luong said it all started seven years ago in San Francisco, just out of graduate school investing in real estate with his spare time on the weekends. Today, his startup Doorvest manages more than $20 million in real estate assets.

“I wanted to look for an avenue to put the money that I had earned from my day job to work,” Luong said. “The goal was to seek out some income security, build a long-term nest egg, hopefully, some passive income to support my life.”

That avenue turned out to be real estate. Luong thinks more people should have the option to invest in the estimated $3 trillion single-family renting market, now more than ever.

A second wave of infections is sweeping across the nation, and with shutdowns looming and business growth on hold, many face a familiar question:

What can I do to make more money?

Luong believes Doorvest has an answer. The firm offers what Luong calls a Democratized way to invest in real estate, entirely online.

Customers can invest up to $100,000 on the platform. Luong and his team of real estate flipping specialists buy, refurbish, and then rent properties, paying back the rent revenue to investors. Luong said Doorvest only gets paid when the properties are profitable, and the reported average annual return on investment is 18%.

The idea came about when Luong and co-founder Justin Kasad tried to find a better way to invest.

Like his peers back in San Francisco, Luong had tried his hand trading stocks. Many of his friends had Robinhood or high yield savings accounts, and were even trading cryptocurrency- but none of those options were what they were looking for. Real estate felt like that next step, but there was a large process to go from cash investment to payday:

“From identifying a mortgage to underwriting, looking through offers, ultimately an offer that sticks, then you’re figuring out how to find a mortgage financing, how to get homeowner insurance,” Luong said. “Then you’re closing on this thing, take the title, and you’re figuring out how to lease it out, how to manage your residents, and then ultimately, maintenance and bookkeeping.”

“From identifying a mortgage to underwriting, looking through offers, ultimately an offer that sticks, then you’re figuring out how to find a mortgage financing, how to get homeowner insurance,” Luong said. “Then you’re closing on this thing, take the title, and you’re figuring out how to lease it out, how to manage your residents, and then ultimately, maintenance and bookkeeping.”

With a long, dizzying list of steps, all with uncertain outcomes, it is no wonder a lot of people are put off by that risk, Luong said.

“When my good friend and co-founder Justin and I went through that long list of items, it dawned upon us that if we could deconstruct real estate investing and rebuild it in an online frictionless way, we could bring it to the masses,” Luong said. “We see real estate as a vehicle to funnel people toward financial security.”

The pair got a group of experienced real estate investors and partnered with mortgage providers and renovators to build a platform to handle all of the steps it takes to turn cash into rent income returns. Doorvest will run every step of the process, including property management, while updating investors at every step of the way.

The firm currently focuses on the Houston rental market, Luong’s long term bread-and-butter area, but plans on renting in other markets in the future.

The platform has been in the works for years, but finally launched last year and immediately had to deal with the pandemic, but Luong said Doorvest made it through so far with success.

“It was definitely an experience, back in mid-march Justin and I were like crap, I think we’re done,” Luong said. “Public equities markets were tanking; we’re a young company without a lot of cash. I think people saw the volatility of the public equities market. In that span of two weeks it went down 40% or so and I think that led a retreat towards perceived reliable asset classes.”

To some, investing in Doorvest was perceived as more reliable than a tanking stock market, and after initial fluctuation, the firm is on the up. In his experience, Luong said the real estate market would continue to push toward suburban areas outside of major city centers as the pandemic continues.

All the while, everything is moving digital. As the company evolves, Luong is excited to offer new products to customers, using real estate as a vehicle to build a banking platform or mortgage platform to service a growing smorgasbord of online real estate options.

“We as a company made a bet three to five years out: we believe that real estate will be transacted entirely online,” Luong said. “Historically, you’d show up at a house, walk around, etc. Due to COVID, people weren’t going out, weren’t shaking hands: The adoption of technology to look at a home entirely online just became a lot more natural. Because of that, we’ve had really strong customer demand and fundraising.”