Archive for 2020

Merchant Indicted For Sending Fake Bank Statements to Online Lenders

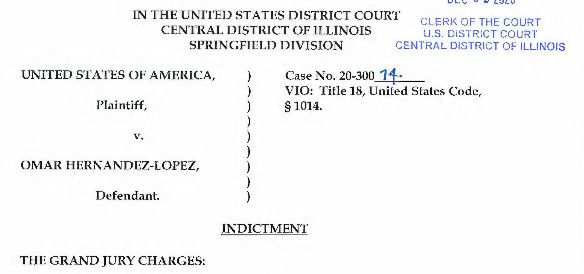

December 7, 2020 On December 17, 2018, the owner of a mexican restaurant in Springfield, Illinois, is alleged to have submitted altered bank statements to National Funding, Inc as part of a loan application to obtain $35,000. What he got in return was an indictment by a federal grand jury.

On December 17, 2018, the owner of a mexican restaurant in Springfield, Illinois, is alleged to have submitted altered bank statements to National Funding, Inc as part of a loan application to obtain $35,000. What he got in return was an indictment by a federal grand jury.

On Dec 2, 2020, the US District Court for the Central District of Illinois unveiled a seven-count indictment against Omar Hernandez-Lopez. Hernandez-Lopez is the owner of El Tapatio De Jalisco Inc DBA La Fiesta Grande.

Prosecutors say Hernandez-Lopez sent doctored PNC bank statements to two lenders, National Funding and Loan Depot in multiple instances. The actual charge is that the defendant knowingly made a false statement for the purpose of influencing the action of a lender in connection with a loan application.

Apparently, no falsehood is too small. For example, in one count the defendant is alleged to have changed a monthly ending bank statement balance of negative $72.91 to positive $131.90, a difference of $204.81. He is also said to have obscured the amount incurred in overdraft fees.

The penalty if found guilty on any one count? Up to 30 years in prison.

Prosecutors cite Title 18, United States Code,§ 1014.

Defendant is innocent until proven guilty. A copy of the indictment can be viewed here.

Aspiria Co-Founder On Successful Funding in Mexican SME Space: Still Lots of Room to Grow

December 5, 2020 After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

After 38 years, Guillermo Hernandez has seen the boom and busts of the Mexican financial markets, weathering seven recessions in all, he said. But until 2020, he had never led a company through a pandemic.

Aspria, Hernandez’s online lending firm, had planned on completing a Series A from international investor Oikocredit, but the deal went into the icebox as the cases came.

“In the beginning of the year, things were doing very well in Mexico, the whole economy was booming,” Hernandez said. “Out of nowhere, we got hit by the pandemic. And the transaction that we were supposed to be closing in March 2020, our investor said, ‘you guys are fantastic, but there are too many unknowns.'”

But due to Aspiria’s resilience and the fact that they went into 2020 with a rock-solid business, Hernandez said Oikocredit decided to complete the investment deal. Aspiria was growing and profitable, and though it was unclear if the markets were going to fall apart, Hernandez said he and his team put the nose to the grindstone and worked through it.

Oikocredit is a worldwide cooperative that provides loans and investments to promote financial inclusion while empowering people by improving livelihoods. That vision is what Aspiria aims to accomplish as an SME lender, Hernandez said, helping businesses access funds to grow.

The Mexican financial space has ample room for growth, and Hernandez said Aspiria is one of the first alternative business lending firms to capture the market.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

Hernandez said the banking world in Mexico is twenty years or more behind the US, and he founded Aspiria to bring some change to the financing space.

“The whole financial services industry, I mean it’s light-years behind the US,” Hernandez said. “I saw that the way that people would do the underwriting, the way that people provided financing for small businesses was just so outdated; it was more of an old school market here. I decided there was this huge opportunity for the market.”

For example, Mexico has a third of the US population, but only 30 banks to the 7,000-10,000 the US has. That population is also a younger demographic than up north. In Mexico, the average age is 27 (It’s 38 in the US); Hernandez said: the Average Mexican is trying to establish themselves and reach the middle class, young, educated, and ready to start a business.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

Hernandez has been working in finance all his life, starting in Mexico as a banker and consultant for new financial companies before leaving to get his MBA on an HSBC scholarship in Manchester, England. He worked for a time in financial services there before joining a payment startup in the US, where he found his love of startup tech culture.

“It was my first exposure to technology, and I was completely amazed. I fell in love with it,” Hernandez said. “At that moment, I was actually thinking about changing careers. I was completely fed up with financial services because it’s boring sometimes. I thought it was not sexy anymore.”

Co-founding Aspiria, Hernandez went on to become the major funder in the space. He said there is so much demand for capital in a standard year that his firm can see 100% year-over-year growth. Even in a pandemic, his firm received a confident investment that will go directly toward building the shop, scaling up funding, hiring, and aiming toward a firm that will one day put it on par with the rest of North America’s leading alternative finance firms.

Oikocredit Expands Its Commitment to Mexican SMEs With Investment in Aspiria

December 4, 2020 Aspiria (www.aspiria.mx), a digital lender targeting underbanked small and medium enterprises (SMEs) in Mexico, has completed an important Series A funding round with participation from social impact investor and worldwide cooperative, Oikocredit.

Aspiria (www.aspiria.mx), a digital lender targeting underbanked small and medium enterprises (SMEs) in Mexico, has completed an important Series A funding round with participation from social impact investor and worldwide cooperative, Oikocredit.

The Series A closing also saw follow-on investments from Aspiria’s current shareholders. The proceeds from the capital round will strengthen Aspiria’s financial capability to support Mexican SMEs.

With its investment in Aspiria, Oikocredit continues its commitment to support SMEs in Latin America, as Oikocredit sees SMEs as playing an important role in areas such as job creation.

Aspiria began operations in 2015 and has lent thousands of loans throughout Mexico. The institution has leveraged digital technologies, data analytics and high-quality service to support the financial needs of Mexican SMEs.

Guillermo Hernandez, CEO and cofounder of Aspiria, commented: “At Aspiria we are very excited to have Oikocredit onboard. SMEs have faced big challenges due to the pandemic and are in need of great financial services. Oikocredit’s investment is an acknowledgement of the tremendous potential of the Mexican SME sector. We look forward to continuing to serve a multitude of SMEs and helping create thousands of jobs in the country”.

Rodrigo Villalta, Equity Officer at Oikocredit, said: “At Oikocredit, we are proud to become shareholders of an institution whose mission is to provide financial support to SMEs that have been typically excluded from the formal financial system”.

“Mexican SMEs are key contributors to employment generation and economic development. We are happy that we can contribute towards building stronger social impact in the country by supporting access to the formal financial system for Mexican SMEs.”

About Aspiria

Aspiria works to increase access to capital to small businesses. Through our platform and the use of statistical credit origination models, we make it fast and simple for the small business owners who have been shunned by the traditional banking system, to obtain financing to continue growing their business.

For more information see: www.aspiria.mx

About Oikocredit

Social impact investor and worldwide cooperative Oikocredit has 45 years of experience funding organisations active in financial inclusion, agriculture and renewable energy.

Oikocredit’s loans, equity investments and capacity building aim to enable people on low incomes in Africa, Asia and Latin America to improve their living standards sustainably. Oikocredit finances close to 689 partners, with total outstanding capital of € 856 million (September 2020).

For more information see: http://www.oikocredit.coop

Note for editors

For more information or to request an interview, please contact Leyda Mar Blanco, Marketing Manager, Aspiria, press@aspiria.mx

Libertad 1966, Col Americana, Americana, 44160 Guadalajara, Jal., Mexico

Why The PPP and EIDL Data Got Dumped

December 3, 2020 The SBA’s time has run out: on Tuesday night, the organization released the loan data for all Paycheck Protection Program (PPP) recipients. The name, address, and how much each recipient received was posted in a series of excel spreadsheets in compliance with a D.C. District Court order, decided November 24.

The SBA’s time has run out: on Tuesday night, the organization released the loan data for all Paycheck Protection Program (PPP) recipients. The name, address, and how much each recipient received was posted in a series of excel spreadsheets in compliance with a D.C. District Court order, decided November 24.

The results do not inspire confidence. Despite knowing this data would be scrutinized by the public, records show that nearly $10 million went to businesses for which the business name field was not entered correctly. Some of these were blank while others contained phone numbers or random dates.

Is it fraud? Maybe, maybe not. It certainly suggests, however, that the official books on $525 billion in individual PPP loans aren’t exactly up to snuff.

The legal struggle to release the data began with filing a Freedom of Information Act (FOIA) in May by a coalition of news companies, including the New York Times, representatives for the Wall Street Journal, ProPublica, and 11 other newsrooms. They hoped to uncover where billions of CARES Act loans went but received privacy concern pushback from the SBA.

In June, the SBA released limited info on the top bracket of loans, from $150,000 upward. United States District Court Judge James Boasberg ruled that there was no reason not to release the information after the SBA refused to open the files up on the bottom 4 million loans at the beginning of November. The SBA pushed for a stay of the order, which was shot down by Boasberg, and finally, the SBA released the data.

As of early November, the agency had processed and approved more than 5.2 million individual PPP loans, along with an additional $192 billion in EIDL loans. PPP funds had the unique distinction of being forgivable so long as they were used for expenses like payroll.

A PPP & EIDL search tool is available on the Small Business Forum where anyone can query the released data.

EIDL Loans Searchable

December 3, 2020The Small Business Forum has added additional functionality to its PPP loan querying tool. The tool now enables users to query every single EIDL borrower as well.

SBA Dumps Detailed Data on Every Single PPP Borrower

December 2, 2020 The SBA has dumped all of it.

The SBA has dumped all of it.

A court order recently forced the SBA to reveal precise details of every single PPP and EIDL borrower regardless of loan size and regardless of privacy concerns.

The SBA dumped all the data late on Tuesday night through a series of downloadable .csv files.

However, small-business-forum.net has made a web-friendly search tool for the PPP loans (not the EIDL), which contains 5 million records. The loan amounts are precise. This latest cache of data is different from the previous reveal in that the loan amounts are exact. There is no approximating here.

The mass disclosure was viewed as controversial because PPP loan amounts were directly correlated with monthly payroll figures so one could potentially deduce the salary of a self-employed business owner with no employees by knowing just their PPP loan amount.

In any case, all of the data has been made public. The easiest way to search the database is at https://www.small-business-forum.net/pppchecker.php

Enova Appoints James J. Lee to Chief Accounting Officer

November 30, 2020Enova International announced the appointment of James J Lee to the position of Chief Accounting Officer. The new role went into effect on November 23rd.

Lee was previously the Controller of Life & Health of Kemper Corporation.

Black Olive Capital Announces Launch

November 30, 2020An Inventory and Purchase Order Lending Platform Targeting $500K to $10MM Opportunities

Bethesda, Maryland / November 30, 2020 – Black Olive Capital LLC (“Black Olive”) announced today the launch of its intelligent inventory and purchase order lending platform. Black Olive’s mission is to provide fast and easy inventory and purchase order financing to underserved small-to-medium sized businesses (SMBs) to help them unlock capital to grow and create jobs. Its financing solutions work for businesses nationwide, and in most industries.

Bethesda, Maryland / November 30, 2020 – Black Olive Capital LLC (“Black Olive”) announced today the launch of its intelligent inventory and purchase order lending platform. Black Olive’s mission is to provide fast and easy inventory and purchase order financing to underserved small-to-medium sized businesses (SMBs) to help them unlock capital to grow and create jobs. Its financing solutions work for businesses nationwide, and in most industries.

By utilizing Black Olive’s intelligent inventory lending platform, SMBs can dramatically increase their liquidity, and ability to scale their businesses with credit facilities that can grow and become more flexible.

Black Olive will address the SMB niche that has been underserved for years. SMBs that need $500,000 to $10 million of liquidity based on inventory or purchase orders are often overlooked by traditional and alternative financing because the large, fixed costs of traditional underwriting make economies of larger deal sizes important—creating a barrier for smaller opportunities. Black Olive’s platform uses more efficient proprietary processes and technology to lower fixed costs and barriers and target $500,000 to $10 million opportunities.

Black Olive’s platform streamlines the application and approval process for SMB owners. SMBs will be able to utilize Black Olive’s lending platform to obtain financing in a fast, efficient and transparent way.

Carlos D. Gomez, who has significant experience in inventory, purchase order and asset-backed lending, will serve as co-founder and president of Black Olive. Mr. Gomez said, “Black Olive’s proprietary platform unlocks capital tied up in inventory and maximizes loan sizes. Through Black Olive’s purchase order financing program, we can help SMBs acquire the inventory needed to fulfill customer orders. Our proprietary processes and technology are available to most industries, ranging from e-commerce to retail to industrial.”

Black Olive’s platform was also specifically built to partner with accounts receivable (AR) factoring lenders, e-commerce lenders, asset backed lending (ABL) lenders, and traditional.

About Black Olive Capital LLC

Provide fast and easy inventory and purchase order financing to small-to-medium sized businesses in the United States seeking $500,000 to $10 million to grow and create jobs.

For more information about Black Olive go to www.blackolivecapital.com or contact Black Olive at info@blackolivecapital.com to learn more about its financing solutions.

Related Links

www.blackolivecapital.com

https://www.linkedin.com/in/carlos-d-gomez-627b90158/