Archive for 2020

Yellowstone Capital Moves to Dismiss FTC Lawsuit

October 3, 2020 Newly revealed in court documents filed on Friday is that the recent FTC lawsuit against Yellowstone Capital culminated after a 2-year inquiry. What may have been a surprise to the Yellowstone defendants is how the FTC brought its case or that it ultimately even decided to bring one at all. A motion to dismiss has been filed.

Newly revealed in court documents filed on Friday is that the recent FTC lawsuit against Yellowstone Capital culminated after a 2-year inquiry. What may have been a surprise to the Yellowstone defendants is how the FTC brought its case or that it ultimately even decided to bring one at all. A motion to dismiss has been filed.

Specifically, counsel for Yellowstone references in its papers that in the preceding years, Yellowstone had already complied with FTC discovery requests that amounted to the production of “24,000 pages of documents, more than 1,400 audio recordings, and responses to numerous interrogatories and follow-up inquiries.”

Following that, the FTC filed suit on August 3, 2020, alleging Misrepresentations Regarding Collateral and Personal Guarantees, Misrepresentations Regarding Financing Amount, and Unfair Unauthorized Withdrawals. In it, it relies heavily on alleged materials dating as far back as five years ago to make its case.

This is fatal to the FTC’s suit, the defendants contend, because the FTC laid out its claims under a very specific statute of the FTC Act, Section 13(b), which can only be brought in federal court if they believe a defendant “is violating, or is about to violate” this area of the law. Past conduct, they say, even if it were true, is not applicable. No acts in 2020 or even from 2019 are alleged with any particularity, nor is it said that any might be happening or will happen.

Some of the purported web pages, ads, or contracts that the FTC refers to no longer exist, have long since been replaced, were taken out of context, or could not even be identified as to where or whom they even originated from, defendants say.

Some of the purported web pages, ads, or contracts that the FTC refers to no longer exist, have long since been replaced, were taken out of context, or could not even be identified as to where or whom they even originated from, defendants say.

Defendants make further arguments for dismissal, one of which takes issue with alleged quotes or comments made by anonymous merchant customers. “The Complaint does not indicate, for instance, if these unidentified customers had breached their MCA agreements or otherwise incurred additional fees beyond the Purchased Amount that were due and owing to Yellowstone under their respective agreements.”

Deprived of all context and specifics, the complaint is loaded with elements that look bad but fall well short of the necessary legal burden, defendants essentially argue.

“The FTC has overextended itself in this litigation,” defendants say in their papers.

They further raise concern that it arises from a possible personal agenda rather than a legally-founded one. Reference is made to an NBC interview in which FTC Commissioner Rohit Chopra told the interviewer that “We’ve started suing some [merchant cash advance companies] and I’m looking for a systemic solution that makes sure they can all be wiped out before they do more damage.”

Chopra had also issued an official statement regarding Yellowstone in which he expounded almost entirely on legal questions that were not even raised in the lawsuit itself but create the impression that they are.

Yellowstone has asked for a stay of discovery pending the outcome of the motion to dismiss.

You can read Yellowstone’s full motion to dismiss here.

The FTC’s interest in this area of finance has been known for some time.

Jackie Reses is Leaving Square Capital

October 2, 2020 Square Capital’s lead executive, Jacqueline Reses, is leaving the company. Square announced on October 2, that her resignation would be effective as of October 31. Reses is largely responsible for developing Square’s robust lending business, one that effectively made the company one of the largest non-bank small business lenders in the country.

Square Capital’s lead executive, Jacqueline Reses, is leaving the company. Square announced on October 2, that her resignation would be effective as of October 31. Reses is largely responsible for developing Square’s robust lending business, one that effectively made the company one of the largest non-bank small business lenders in the country.

It’s time to hang up my boots and say goodbye to my good friends at @Square. To the people I’ve worked with: everything I love about Square is related to you. It is my privilege and honor to have been along for the ride with you.

— Jackie Reses (@jackiereses) October 2, 2020

I shared my thoughts with Squares today because the place is so special! I thought I would share. pic.twitter.com/tXAE0dZhK9

— Jackie Reses (@jackiereses) October 2, 2020

CredoLab Lands $7M Funding, Bringing the “Gini” to US, Elsewhere

October 2, 2020

Chief Product Officer Michele Tucci said the platform uses 50,000 data points of mobile phone activity to predict a prospective borrower’s debt capabilities. CredoLab serves the 1.7 billion “credit-invisible” customers across the globe that may have some credit history, but not enough for a score, let alone a prime score.

“We do this in real-time: in less than a second a lender anywhere in the world, receives a credit score from Credolab,” Tucci said. “We don’t know the identity of the user; it’s only known to the bank or the lender, not to Credolab.”

CredoLab anonymously collects thousands of mobile data points, uses that data to create behavioral models, and then derives a credit score. The data can be anything- from the type of apps a user downloads, to the number of calendar events created- even the amount of texts the user sends. Is the user a gambler, a gamer, does the user use a work email during the week, and how many calendar events they schedule- all go into the predictive model.

“Some of these micro behavioral patterns could be the type of files being downloaded. Is it mostly music, or is it PDFs- or the percentage of photos taken in the week prior to the loan application that are selfies,” Tucci said. “So these are all indications that we collect and find a correlation we compare and analyze about 1.3 million micro behavioral patterns.”

Tucci said the CredoLab platform offers unmatched speed and predictability for customers’ future credit habits. He said Credolab helps lenders save money because they can better predict how their borrowers will act. Borrowers benefit by the program: Tucci argued that if lenders can better expect how they will be repaid, they tend to lend more.

The team built the platform for the world’s risk managers, whom Tucci knows constantly worry about the health of their transactions.

“Our CEO and founder Peter Bartek has more than 20 years of experience managing risk,” Tucci said. “So he feels the pain of the CROs out there, and our solution is built to address the very specific needs of chief risk officers.”

To explain the CredoLab platform’s accuracy, Tucci used a data metric called the Gini coefficient, a number between 0 and 1 that identifies to which category a request belongs. In this case, the GINI is used to classify borrowers as creditworthy or unworthy based on their mobile data.

“Zero is like flipping a coin; you have a 50/50 chance of getting the decision right. Basically no predictability,” Tucci said. “A GINI of one is like my wife; she’s always right. You know exactly what outcome to expect every single time.”

CredoLab’s platform has a predictive power of 0.6. Tucci cited World Bank economist David Mckenzie, who found for each decimal increase in GINI, there is a 1% cost savings from a risk point of view.

Software That Automatically Fights For Bank Refunds Adds “PRO Index”

October 1, 2020 Harvest fills a unique role in the fintech world. The platform is an automatic banking advocation software that fights on behalf of users for the best deals possible.

Harvest fills a unique role in the fintech world. The platform is an automatic banking advocation software that fights on behalf of users for the best deals possible.

Connect your bank information and the Harvest AI will fight late fees and overdraft fees. Customers are only charged a portion of funds returned, and if the program does not succeed at getting money back, it doesn’t cost the user a cent.

Automatically arguing for better deals, the platform last year saved customers a collective $2 million, and manages $500 million in debt to date.

The brainchild of CEO and founder Nami Baral, Harvest released a new “PRO Index” that builds a credit profile for each customer to pair with information from FICO scores. Harvest created the index to help lenders get better information and for customers to track their financial health. Baral hopes the data will help lenders find a reason to continue credit flowing to those who have hit hard times but still can make their payments.

“In the post-COVID recessionary environment, the creditworthiness of customers continues to plummet,” Baral said. “[Harvest] saw that traditional credit scores do not provide enough of a picture about a customer’s actual worthiness and potential.”

This announcement is not just a press release, but a continuation of the founding premise of Harvest: to help the average American overcome debt and build financial health.

Baral, a Nepali native, came to America during the last financial crisis on a scholarship to study ovarian cancer at Harvard medical school. Expecting the country to be a utopic economic powerhouse, Baral instead saw lost jobs, defaulting mortgages, and debt.

“In many ways, America is one of the most wonderful places in the world,” Baral said. “But at the time it was a complete departure from what I’d hoped the US to be, because what I saw was, people were losing their jobs, losing their homes in the financial crisis.”

She decided to work toward fixing the problems she saw, pivoting to study finance. Graduating with an applied math and economics degree, Baral then trained in investment banking. She worked on an auto-advocation software for a digital advertisement startup that was eventually bought by Twitter.

She decided to work toward fixing the problems she saw, pivoting to study finance. Graduating with an applied math and economics degree, Baral then trained in investment banking. She worked on an auto-advocation software for a digital advertisement startup that was eventually bought by Twitter.

She had seen a company’s growth from IPO to merger and stayed at Twitter for four years. When she left, she began market research, talking to everyday Americans about what they needed to improve their finances.

“In those conversations with people from all over the US, Alaska, Oklahoma, San Francisco, New York everywhere,” Baral said, “I realized that the issues plaguing Americans in the last financial crisis had not gone away.”

Baral said these issues had intensified over this past decade. Incomes were volatile and stagnating, student loans had risen, and the people Baral talked too were getting more and more into debt.

“So I thought what the average American needs today is not another savings product, not yet another investment product,” Baral said. “But something that can help them reduce the debt that they have in their lives. That’s the genesis of Harvest.”

With the addition of the PRO Index, Baral is excited to offer another way Americans can maintain their financial health. She said that during the pandemic, every day could be a challenge for the average American, but the new platform can act as a barometer and compass.

“A lot can change between the time you extend a loan to the customer versus when they have to pay,” Baral said. “We call that Ability-to-pay as-a-service, and that’s where the PRO Index is used, determining: ‘is this customer still healthy? is my overall portfolio still healthy?'”

If the customer is no longer healthy, the info gathered to form the PRO Index, like transactional cash flow data, can supply lenders with information on improving their health. Baral says the platform encourages lenders to keep customers and shows borrowers how to improve their credit standing.

Capify Announces $10 Million Equity Round As Well As Continued Support From Goldman Sachs Merchant Banking Division

September 30, 2020

Access To Business Loans Especially During COVID-19 Pandemic

(Manchester, England and Sydney, Australia) – Capify (http://www.capify.co.uk, http://www.capify.com.au ), a leading fintech small business lending platform, today announced it has closed a $10 million equity round as well as continued support from Goldman Sachs Merchant Banking Division through its existing credit facilities.

“The fact that we were able to raise $10 million for an online small business lender in the midst of a global pandemic from sophisticated investors with industry experience speaks to Capify’s business model, the unprecedented opportunity ahead of us and its management team,” said David Goldin, Founder and CEO of Capify.

Continued, Mr. Goldin, “We believe demand by small businesses seeking access to unsecured capital will be at unprecedented levels because most businesses have already accessed the government backed business loan programs in the UK and Australia market but will still need additional capital – as do the many businesses that didn’t qualify for the Government guaranteed programs and are seeking much needed working capital to grow.”

In addition, Capify is actively seeking partnerships with companies with large small business customer bases to provide much needed financing to their small business customers, thus allowing them access to capital to purchase goods / services which have proven financially difficult during this challenging time. Furthermore, we are looking for opportunities where we can assist our industry peers who don’t have access to capital during this time by providing capital to their customer base.

Capify’s 12 year presence in the UK and Australia market is more relevant than ever as small businesses demand for access to capital to navigate through COVID-19 is at an all time high. According to John Rozenbroek, COO / CFO of Capify, “It is crucial at this time that small businesses are aware of alternative funding solutions to support cash flow or invest in their future. Capify is one of the few online small business lending platforms in the marketplace that can actively provide non-government backed business loans at scale to small businesses seeking working capital to grow their business. ”

About Capify

Capify is an online lender that provides flexible financing solutions to small businesses in the UK and Australia seeking working capital to sustain or grow their business. The fintech company has been operating in the UK and Australia market for over 12 years.

For more details about Capify, visit

Capify UK: http://www.capify.co.uk

Capify Australia: http://www.capify.com.au

Capify UK Media Contact:

Ian Wood, Marketing Director

iwood@capify.co.uk

+44 0161 393 9536

Capify Australia Media Contact:

Nandita Graham, Senior Marketing Manager

ngraham@capify.com.au

+61 433 511 653

Capify CEO David Goldin on New $10 Million Equity Round

September 30, 2020 Capify, a leading international small business lending platform, announced a $10 million equity round this week from a new investment group with vast experience in the alternative lending industry.

Capify, a leading international small business lending platform, announced a $10 million equity round this week from a new investment group with vast experience in the alternative lending industry.

“[investors were] diligent seeing Capify, the management team, and the opportunity,” Goldin said. “They thought it was a very good investment, particularly how Capify’s portfolio performed during the pandemic.”

Goldin said the capital is a great “restart of the engine” after the cautious approach the company took to lending at the height of the pandemic. The money is not an equity round from current investors, but rather new capital joining the team.

The funding will be directed toward ramping lending back up and extending business partnerships with firms that serve small businesses, as well as direct and indirect lenders.

“So, hindsight is actually better than 2020 vision; no one in our lifetime has experienced the pandemic,” Goldin said. “No one knew what to expect from a risk profile, so we took the conservative approach.”

That approach was to shut down new loans and focus on servicing its current customers. It was a difficult time for the alternative lending industry veteran, but now Goldin said he sees a great demand for capital.

“This was one of the toughest challenges that I’ve experienced ever as an entrepreneur,” Goldin said. “The result really speaks to Capify as a company. People are willing to make that investment, believing in opportunity ahead and not the current times or the past during the pandemic.”

Goldin said that Capify has always been known for its well-performing portfolio, one of the reasons that in 2019 the firm received a $95 million credit facility from Goldman Sachs’ Merchant Banking Division.

Goldin began working in the fintech industry before the word fintech was even coined; in the early 2000s, he started one of the first MCA companies. Amerimerchant started selling loans and MCAs internationally in the UK and Australia in 2008, then rebranded to Capify in 2015. After leaving the US market in 2017 gained Goldman’s attention last year.

“So now that we have the firepower, we believe there’ll be opportunities in these markets as demand picks up for small business lending,” Goldin said.

Another Attorney Charged Criminally in 1 Global Capital Saga

September 29, 2020 Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Ledbetter was criminally charged on Tuesday by the US Attorney’s office in South Florida for his alleged role in the 1 Global Capital Securities fraud case. Ledbetter was formally accused of Conspiracy to Commit Wire Fraud and Securities Fraud. He was simultaneously hit with civil charges by the Securities and Exchange Commission.

Both agencies say that Ledbetter reaped nearly $3 million in referral fees from 1 Global Capital in exchange for raising nearly $100 million from investors, mostly retirees, all while making knowingly false statements and misrepresentations about the investments. For instance, they say that he knew the investments were securities but claimed they weren’t anyway. Similar circumstances brought down Florida attorney Jan Douglas Atlas last year. Ledbetter had been compensating Atlas on the side as part of the alleged scheme.

Ledbetter is the 4th individual to be criminally charged in connection with the 1 Global Capital case. The other three: Atlas, Alan G. Heide, and Steven Schwartz, have all already pled guilty.

Following Nine Lawsuits, OnDeck Discloses Supplementary Details Behind Planned Enova Merger

September 28, 2020

After OnDeck announced its planned merger with Enova, it was sued nine different times (See here and here) by shareholders that accused the company’s Board of Directors that they had failed to disclose material information about the deal.

OnDeck formally responded on Monday, September 28th, wherein they disclosed that plaintiffs in all of those actions had agreed to dismiss their claims in light of the release of this supplemental information:

The Company and Enova believe that the claims asserted in the Actions are without merit and that no supplemental disclosures are required under applicable law. However, in an effort to put the claims that were or could have been asserted to rest, to avoid nuisance, minimize costs and avoid potential transaction delays, and without admitting any liability or wrongdoing, the Company has determined to voluntarily supplement the Proxy Statement/Prospectus as described in this Current Report on Form 8-K to address claims asserted in the Actions, and the plaintiffs in the Actions have agreed to voluntarily dismiss the Actions in light of, among other things, this supplemental disclosure. Nothing in this Current Report on Form 8-K shall be deemed an admission of the legal necessity or materiality of any of the disclosures set forth herein. To the contrary, the Company and the other defendants specifically deny all allegations in the Actions that any additional disclosure was or is required and expressly maintain that, to the extent applicable, they have complied with their respective legal obligations.

OnDeck first re-explained its background situation leading up to the Enova deal:

Starting in April 2020, OnDeck management commenced a review of potential financing options to secure additional liquidity and potentially replace the Corporate Line Facility and began contacting potential sources of alternative financing, including mezzanine debt. OnDeck contacted, or was contacted by, more than ten potential sources of mezzanine or alternative financing, and received pricing indications from four sources. The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component. The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points. Based on the initial term sheets proposed, OnDeck engaged in negotiations with each of the four potential sources of alternative financing. As these negotiations progressed and COVID-19’s impact on the macro economy and OnDeck’s loan portfolio intensified, two of the four potential sources of alternative financing ceased to actively participate in negotiations. Discussions with the final two potential sources of alternative financing remained ongoing through the time that OnDeck and Enova entered into the merger agreement. Throughout the Process, OnDeck management reported the status of such negotiations on a frequent and ongoing basis to the OnDeck Board for its deliberation in the context of OnDeck’s standalone plan, and the OnDeck Board considered the significant uncertainty of being able to reach agreement on alternative financing in its decision to enter into the merger agreement.

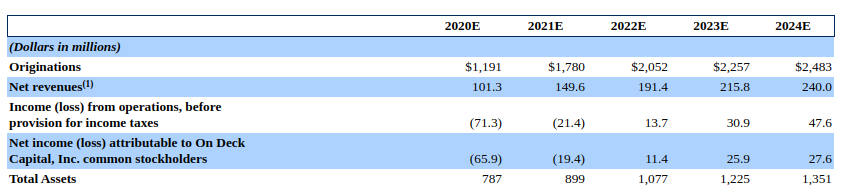

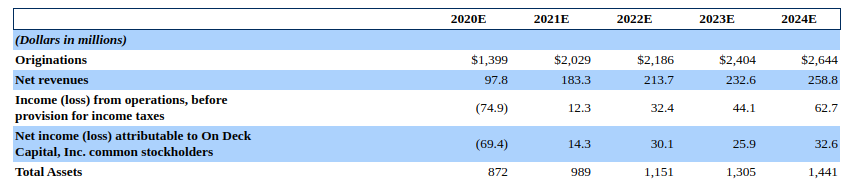

Of particular contention in the deal were OnDeck’s financial projections, prepared to estimate OnDeck’s trajectory as an independent entity. Shareholders complained that there were two sets of books and that they only got to see one. The other set, dubbed Scenario 1, had been used to shop OnDeck around to other suitors. OnDeck published both sets in their supplemental materials on Monday.

The difference is stark. Originally disclosed to shareholders was a projected cumulative net loss of $20.4 million through the end of 2024. The other set of projections, Scenario 1, state a cumulative net income of $33.5 million over the same time period, a difference of over $50 million.

The original predicted a 2021 net loss of $19.4 million while Scenario 1 predicted a net income of $14.3 million.

One reason offered for selecting the less optimistic of the two is that OnDeck’s management determined that loan originations were trending below both sets of projections as of July 12th. OnDeck announced the Enova deal about two weeks later.

Shareholders will cast their votes on the merger on October 7th. OnDeck’s Board “unanimously recommends” that they vote in favor of the proposed merger with Enova.