New York’s State Government is Competing With Online Lenders on Pay-Per-Click and Misinforming Small Businesses

Move over online lenders, New York’s financial regulator is apparently shelling out big bucks to steer away New York’s online small business loan searchers to THEMSELVES. As someone who has historically kept tabs on Google’s search results for lending related keywords, this new result is one of the more interesting developments I’ve seen yet.

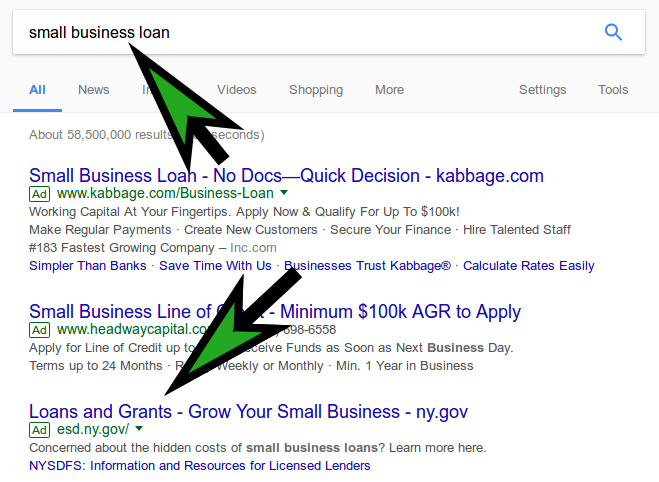

From a New York IP, querying Google with the keyword small business loan produced not only an ad for Kabbage and other online lenders, but also prominent paid placement from New York State with a sitelink extension to the New York Department of Financial Service’s page about licensed lending requirements.

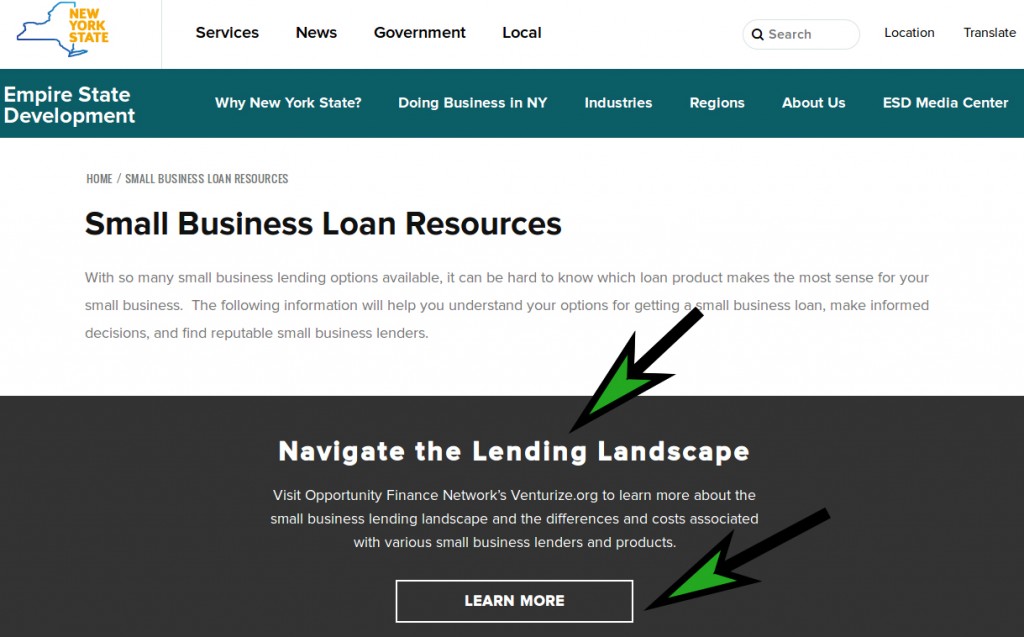

While there’s nothing that weird about marketing state-assisted development programs, the main Google ad link directs visitors to “Navigate the Lending Landscape” by clicking a “Learn More” button.

That takes you to Venturize.org, operated by Opportunity Finance Network, a Community Development Financial Institution (CDFI) that New York is apparently really doing the advertising for. And there’s a major problem with that.

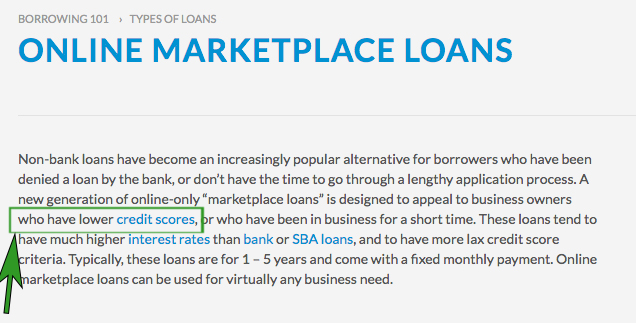

The information across that site is wildly incorrect. It explains online marketplace loans as “designed to appeal to business owners who have lower credit scores, or who have been in business for a short time.” That’s a pretty broad statement especially when many online marketplace lenders are in fact designed to appeal to business owners who have higher credit scores and have been in business for a long time.

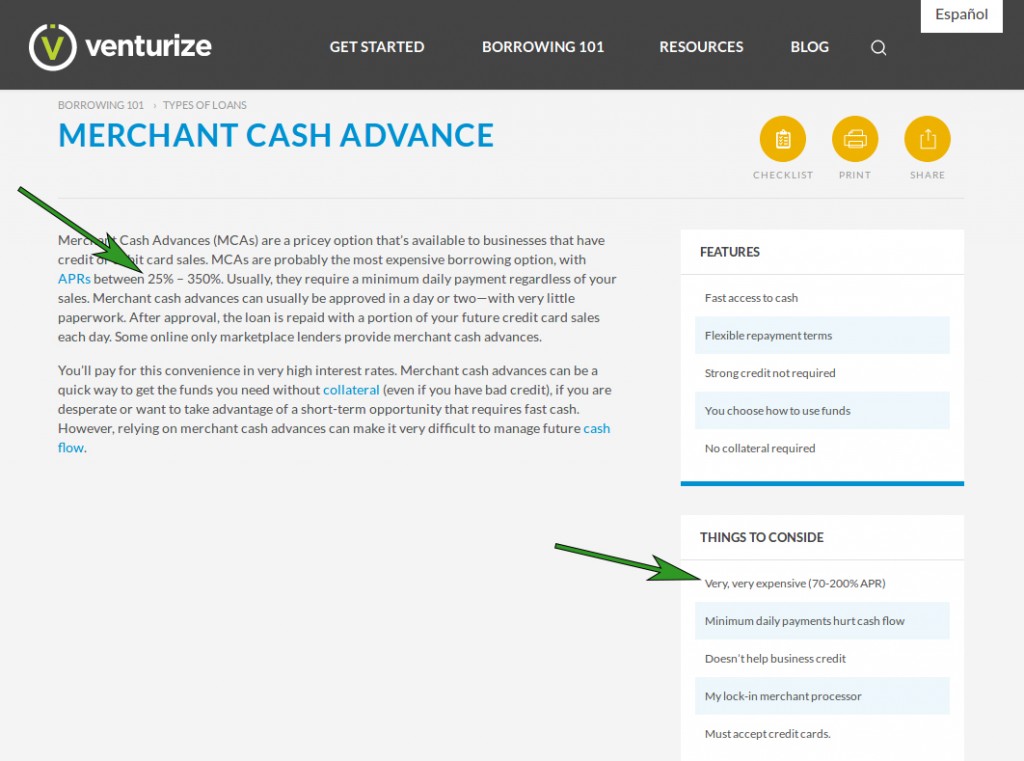

The description of merchant cash advances is even worse. Whoever wrote it has no understanding of them in the slightest. Good thing New York State is paying up to $100 a click with our tax dollars for premium keywords to teach businesses absolute nonsense! I quote what the website says below and my comments are in red next to them.

- “Usually, they require a minimum daily payment regardless of your sales.” – Um, no

- “After approval, the loan is repaid with a portion of your future credit card sales each day.” They’re not loans. This is mostly well settled in the New York Court system. Recently, see this and this

- “You’ll pay for this convenience in very high interest rates” – There are no interest rates

- “MCAs are probably the most expensive borrowing option, with APRs between 25% – 350%.” – Wrong. No APRs can be calculated on a purchase transaction

- “if you are desperate” – That’s a pretty unfair statement to say that a methodology is only for the desperate. New York State is insulting its small business constituency, private companies, and the jobs that have been maintained or created all at the same time

There are also typos and spelling errors throughout the page, as well as conflicting information. The very same page describes MCAs as having between 70% – 200% APR on one side and between 25% – 350% APR on the other side. You don’t need anymore proof that whoever wrote this stuff was just winging it on the fly to make it sound bad. These are the kinds of misleading figures that the CFPB sues financial institutions for and perhaps they should actually take a look at this.

It also says that businesses must accept credit cards. That’s not true either.

It’s strange that a CDFI would go to such great lengths to deliberately misinform small businesses, let alone have a state government foot the bill for them to do it.

Furthermore, as someone who recently used an online marketplace loan for my business, I’m personally offended that my state government would pay to market information that says it was designed to appeal to business owners who have lower credit scores. As my FICO score is over 800, the writer clearly does not understand the product, the market, or the appeal.

More troublesome of course, is that the NYDFS hopes to regulate these industries through language snuck in Governor Cuomo’s budget proposal. Given the above, what could possibly go wrong?

Last modified: March 10, 2017Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.