Big Banks Less Transparent Than Online Lenders Federal Reserve Study Finds

The results are in. Dissatisfied small business borrowers are more likely to encounter transparency problems with big banks, not online lenders.

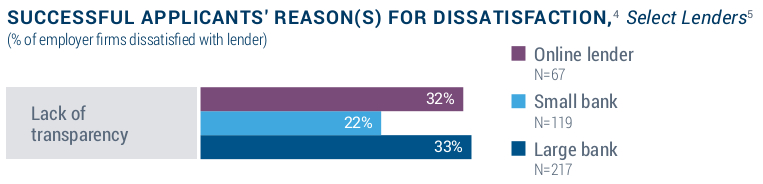

The margin of difference on this measure may have been razor thin, but the anti-online lender rhetoric isn’t matching up with borrower feedback. The 2015 Small Business Credit Survey, a comprehensive report released by the Federal Reserve, found that 33% of borrowers that were dissatisfied with a small business loan from a big bank, cited a lack of transparency as a reason. 32% of borrowers that were dissatisfied with an online lender cited a lack transparency. While both statistics show room for improvement, the results shatter the myth that online lenders are uniquely lacking in transparency.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

Small banks were less likely than online lenders and big banks to experience dissatisfaction over transparency.

Online lenders were defined by the Fed as “alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.” Respondents could select multiple options for dissatisfaction, ensuring that a separate issue didn’t merely trump transparency.

Big banks also scored worse on difficulty of the application process. 51% of dissatisfied borrowers that got a loan from a big bank cited difficulty. Only 21% of dissatisfied borrowers that got a loan from an online lender cited difficulty.

A more difficult, lengthier, and more regulated process at big banks has apparently not led to more transparency with borrowers. The findings echo B. Doyle Mitchell Jr.’s testimony presented during a House Committee hearing last fall. Mitchell, who was speaking on behalf of the Independent Community Bankers of America, said that adding more pages to loan agreements do not make them any more clear to borrowers. “In fact it is even more cumbersome for them now,” he said.

The Federal Reserve’s own study has proven to be consistent with that assessment.

Last modified: March 4, 2016Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.