Regulation

California’s Business Loan & MCA Disclosure Law Is Nearing Finality

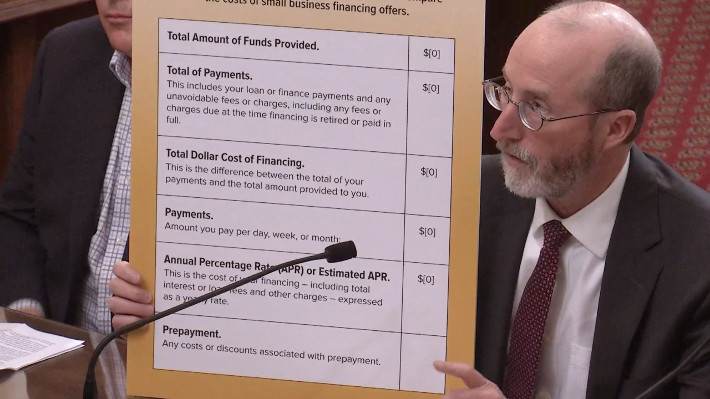

April 13, 2021 Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

The 52-page document is the result of years of negotiations between various parties that all have a stake in its implementation. Among the finer details are the characteristics of the fonts permitted in the disclosures, what column a certain disclosure can be placed in, and the aspect ratio of the columns themselves.

But that’s the easy part. Here’s the hard part, according to a brief published in Manatt’s newsletter yesterday.

“The modified regulations continue to require use of the annual percentage rate (APR) metric, rather than annualized cost of capital (ACC), to disclose the total cost of financing as an annualized rate. This appears to be a final decision, which will make it difficult if not impossible for many commercial finance companies to comply given the significant challenges of calculating APR on products with substantial variance in the amounts and timing of payments or remittances.”

Manatt highlights other issues, including that all the necessary disclosures be provided “whenever a payment amount, rate, or price is quoted based on information provided by the proposed recipient of financing…”

This requirement, the firm says, is not even required under Federal Regulation Z for consumer loans.

“Many companies will not be able to comply with this requirement absent radical changes to their California application and underwriting procedures, as it is common today for companies to have preliminary discussions with applicants about potentially available financing terms before full underwriting has been completed.”

Manatt’s newsletter on the issue can be found here.

Any interested person may submit written comments regarding SB 1235’s modifications by written communication addressed as follows:

Commissioner of Financial Protection and Innovation

Attn: Sandra Sandoval, Regulations Coordinator

300 South Spring Street, 15th Floor

Los Angeles, CA 90013

Written comments may also be sent by electronic mail to regulations@dfpi.ca.gov with a copy to jesse.mattson@dfpi.ca.gov and charles.carriere@dfpi.ca.gov.

The last day to submit comments is April 26, 2021

Implementation of New York’s Commercial Financing Disclosure Law Delayed

April 6, 2021The implementation of New York’s commercial financing disclosure law has been pushed back. Originally scheduled to go into effect in June of 2021, an amending bill changed the date to January 1, 2022.

The only other material change of note is that the exemption from the law for transactions greater than $500,000 has been increased to $2.5 million.

NY Court Says MCA Agreement is a Factoring Agreement, Not a Loan

March 22, 2021 A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

In Principis Capital LLC v Team Van Eyk, Inc. et al, Principis sued the defendants over a breach of contract. Defendants “did not deny the facts underlying the motion or the the amount due,” the judge said, “but asserted instead that the Agreement is not an agreement for the purchase of future receivables; but is instead, a criminally usurious loan, and is therefore void as a matter of public policy.”

This defense actually led to victory for the plaintiff.

The Appellate Division, First Department, in Champion Auto Sales, LLC v Pearl Beta Funding, LLC (159 AD3d 507, 507 [1st Dept], lv denied 31 NY3d 910 [2018]) has considered this issue, involving a merchant agreement substantially similar to the agreement in this matter, and has held that the type of agreement involved in this case is a factoring agreement rather than a usurious loan. This court is bound to follow Champion and, therefore finds that the Agreement is a factoring agreement and not, as defendants assert, a usurious loan. There are, therefore, no genuine triable issues of fact, and plaintiff is entitled to summary judgment on its complaint.

Case closed.

Steve Denis, SBFA on Why Maryland MCA Bill Failed

March 22, 2021 “In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

“In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

Denis was referring to the nearly unanimous canning of Maryland’s MCA “Prohibition” bill last week. The bill failed to get enough support to leave the committee, blocked by a 19 to 3 vote against bringing the law out to the House floor. Denis, a proponent of the MCA and alt financing industry for years, said it was due to legislators understanding the need for capital “out there during the pandemic” and how harmful an APR cap could be for both business owners and the broker industry.

The law was originally proposed last year before covid shutdowns, but that also failed to make it to the floor. It now appears to be an annual event.

“Our goal as an organization is to make sure that small businesses have access to all different types of financial products and that we believe that small businesses are in the best position to make good decisions for their businesses,” Denis said. “The bill in Maryland narrowly targeted MCA products, and as you know and a lot of folks in the industry know, that sometimes MCA is in the best interest of the business, there’s a lot of benefits to an MCA.”

Denis punctuated his statement with the mantra- we were not out of the woods yet. An APR disclosure bill was just introduced in the Connecticut State Senate last month, modeled off the New York APR bill set to go into effect this year. Denis was hopeful the legislators could learn from speaking to industry interests and change their course like in Maryland.

“We are engaged, I think we’re in a good spot. With any of these bills, Maryland, Connecticut, I caution you know we’re not out of the woods yet,” Denis said. “We still want to work really closely with policymakers. We’re for meaningful disclosure, we think there needs to be some guardrails on our industry, but I think that the most important thing we can do is continue to educate folks in states.”

Maryland’s Latest Merchant Cash Advance Prohibition Bill Failed to Advance

March 18, 2021 Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

“I don’t want to snatch defeat from the jaws of victory,” he maintained.

There were several amendments up for consideration, including the inclusion or removal of a 24% APR rate cap on MCA transactions. The subject of APR dominated the light Q&A that took place, but one delegate voiced concern that creating restrictions on capital providers to businesses that might not be able to obtain funding elsewhere would probably be counterproductive. And when a roll call of votes was taken to determine if the Bill should advance to the Floor, he voted no, as did nineteen of his colleagues. Only three voted yes, so the bill did not advance, ending its prospects for the 2021 legislative session. However, it could be reintroduced again in 2022.

Committee Vice-Chair Kathleen Dumais (D) said that she thought the bill “was not ready” despite Delegate Howard “having worked hard on it.” This was Howard’s second try in two years to move it forward. His first attempt, introduced on February 7, 2020, was called the Merchant Cash Advance Prohibition Bill. The more recent one dropped the “prohibition” label but used language that would have effectively prohibited them in the state of Maryland.

CFPB, SEC Chair Appointments Begin Senate Hearing

March 2, 2021CFPB Chair Nominee Rohit Chopra (“Chopra like Oprah” he explained) and SEC Chair nominee Gary Gensler faced questions from Senators in the first confirmation hearings on Tuesday.

The pair were fielded questions over a video call. The confirmation hearings are mostly ceremonial; with a partisan house and senate, it is unlikely either appointment will be blocked.

Senators used their time to make question-statements featuring popular political talking points. Topics ranged from student loan finance reform, Bitcoin and crypto regulation, environmental reform through business regulation, and retail stock trading protections.

The appointees answered in the uniform tone of life-long public servicemen that have mastered the art of not directly answering questions. Each demonstrates their respective regulator points of view through action. By Reading each appointee’s resume, it becomes clear why they were chosen for Biden’s regulatory offices.

Chopra became a secretary at the CFPB when the organization was minted in 2008, and he focused on regulating student loans. The CFPB under Chopra will likely focus on extending CFPB regulatory controls over lending, payday lending, student debt, and possibly even fintech lending.

Gensler was the Commodity Futures Trading Commission’s chair, and he helped scale up securities regulation following the housing crisis, his work creating the Dodd-Frank act. The SEC will likely ramp up regulatory action over crypto-currency and address concerns with retail investing and public security sales.

“Technologies change, and markets change, but we should always evaluate new approaches to markets,” Gensler said in response to questions about stock trading and gamification.

Steve Daines, a Republican from Montana, asked Chopra his opinion whether the CFPB should be led by a multiple-member commission to avoid politicization over the leadership. Chopra said it wasn’t up to him.

“It’s the job of Congress to decide the agency structure. In my view, regardless if it’s a single director, there needs to be accountability, responsiveness,” Chopra said. “Where I sit at the FTC, this agency has missed some of the worst engagements when it comes to big tech privacy, while the CFTC under Gary did take action and was transparent.”

When the Trump administration attempted to appoint a new CFPB director, the Obama chair claimed it was illegal for the president to seat a new chair. In June last year, the Supreme Court said that was unconstitutional, and like most other executive offices, the president has the power to appoint leaders.

Chopra did say that regulating student loan debt was something under the purview of the CFPB. He was asked if CFPB had the authority to address the $1.7 trillion in student loan debt.

“Yes, my understanding is that the existing law and regulations, those financial services are covered.” He said.

Senator John Kennedy, a Louisianan democrat who tuned republican after 2007, asked Gary Gensler about the great recession and his time creating regulation at the US Treasury in the aftermath.

“Why didn’t anybody go to jail?” Kennedy said.

“Well, I wonder the answer to that question too; I was pursuing civil cases. It is largely up to the Department of Justice,” Gensler tried to answer. “These cases are hard to try and hard to find intent.”

Bill Hagarty, a Republican from Tennessee, asked Gensler about using business regulatory offices for social reforms, using the local proverb “You don’t shoot where the rabbit was.”

Andrew Smith Recalls Era as FTC Director

February 27, 2021Andrew Smith, who became Director of the FTC’s Bureau of Consumer Protection (BCP) in 2018, ended his time with the agency on January 29, 2021. In a LinkedIn post recapping his tenure there, he said:

Despite a month-long government shutdown and a once-in-a-century pandemic, BCP brought more than 200 enforcement actions against companies great and small, including many household names, obtaining strong injunctions and billions of dollars in civil penalties and consumer redress.

BCP also had several firsts, including the first cases holding technology platforms liable in connection with user-generated content; the first small business financing cases; the first cases against VoIP service providers and finance companies for assisting and facilitating fraud; the first cases involving fake reviews, fake rankings and consumer review gag provisions; the first fair lending case at the FTC in more than a decade; the first paperless redress program; and the first CBD cases.

The FTC has been going through some changes with the introduction of a new administration. FTC Commissioner Rohit Chopra, for example, will be the next head of the CFPB, pending his confirmation.

CFPB’s Reach May Extend to PPP Lending

February 16, 2021 The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The foray into non-consumer finance was instead driven by PPP lending.

“Consistent with its authority to ensure compliance with the Equal Credit Opportunity Act (ECOA), the Bureau conducted [Prioritized Assessments] to assess potential fair lending risks attendant to the institutions’ participation in the [PPP] program,” the report said.

Accordingly, the CFPB determined that small business lenders that restricted or limited eligibility such as banks who only permitted applications from existing customers, for example, “may have a disproportionate negative impact on a prohibited basis and run a risk of violating the ECOA and Regulation B.”

The CFPB conceded that it had not actually investigated if violations occurred and noted that the majority of institutions had argued that such limitations were either in place to comply with Know Your Customer legal requirements, to prevent fraud, or both.

The CFPB did not say that it had supervisory authority over non-banks that participated in PPP, but it did signal that its purview was larger than just consumers when it came to the institutions it supervised.

The report can be viewed here.

The CFPB is expected to have more proactive involvement in small business finance under its new incoming director, Rohit Chopra. Chopra’s nomination was formally submitted on February 13th. Dave Uejio, the Bureau’s Chief Strategy Officer, has been serving as Acting Director since President Biden took office.