deBanked Inks Deal with Lenders Marketing in Bitcoin

March 10, 2015 deBanked has inked an advertising deal with Lenders Marketing, a company that provides trigger leads to the business financing industry. The deal is significant because it was priced in Bitcoin, not dollars.

deBanked has inked an advertising deal with Lenders Marketing, a company that provides trigger leads to the business financing industry. The deal is significant because it was priced in Bitcoin, not dollars.

“Bitcoin’s value against the dollar is volatile,” said deBanked’s Sean Murray. “But 1 BTC today is still equal to 1 BTC tomorrow.”

deBanked does convert a portion of its Bitcoin revenue into dollars, but holds the rest. “I think it’s important to practice what you preach,” Murray added. “What better way is there to debank than by using Bitcoin as a currency?”

Lenders Marketing and deBanked used Coinbase to transact, the country’s first regulated Bitcoin exchange.

deBanked’s March/April print magazine issue will be distributed in the mail at the end of this month. Anyone can subscribe to receive it for FREE.

Lender’s Marketing monitors business credit databases, credit card processing companies, financial institutions, government and public filings and merges them with their own database to provide a real-time reflection of current business loan needs.

In the upcoming magazine issue, you will literally be able to smell the leads. You’ll have to hold a copy in your hand to find out what that means.

Does Your Own Hunger Affect Lead Quality?

March 7, 2015 5 years ago in this very month, I funded 29 MCA deals for a total purchased amount of $608,000. 23 of those deals were renewals. It wasn’t my best month and it was also a different era. They were all split-processing accounts, not ACH. New deals could take six weeks to set up depending on the payment hardware. There was also no such thing as stacking then. The deals I was funding were from a good mix of warm leads, usually people who had filled out a form for financing somewhere online.

5 years ago in this very month, I funded 29 MCA deals for a total purchased amount of $608,000. 23 of those deals were renewals. It wasn’t my best month and it was also a different era. They were all split-processing accounts, not ACH. New deals could take six weeks to set up depending on the payment hardware. There was also no such thing as stacking then. The deals I was funding were from a good mix of warm leads, usually people who had filled out a form for financing somewhere online.

I didn’t always get warm leads. When I first started in sales in 2008, every rep got three or four actual leads a day. These were the golden geese, the Glengarry leads. The challenge was that they were sold to at least five ISOs at once so it was a race to get the merchant on the phone and establish a rapport with them first.

Caller number five was usually dead in the water. The least likable or least experienced of the remaining four would be cut by the merchant right away. That brought it down to 2 or 3 that the prospect would at least entertain.

None of these merchants had actually applied for a cash advance, but rather they had expressed an interest in business financing on a generic website and claimed that they accepted more than $5,000 in merchant account sales a month. Yet competing against four other companies to offer an expensive solution the merchant had never heard of was as good as the leads could possibly get. And if I started the day at 9 AM, then odds were I’d have made all 3 calls by 9:30.

I didn’t get paid a base salary so I couldn’t fake my way through the rest of the day. The remaining 9 hours were UCC lists and follow up calls with leads from previous days. I can’t imagine calling a UCC now in the age where stacking exists. The only option back then was to satisfy their outstanding advance in full with the proceeds of the new one.

Hi, my name is Sean Murray with ____________ and I’m calling about the advance you have with _____________. I know that company’s products can be awfully expensive and I was wondering if you were open to the opportunity of a lower holdback percentage, lower dollar for dollar cost of capital, and some additional money in your pocket.

I was notorious for cutting points off my upfront commission to get deals done. Sometimes I’d make nothing on the upfront commission but at least I’d get a new merchant account out of it and a backend cash residual. My residuals grew really fast.

Fast forward to 2011, I didn’t want to call UCCs anymore. I wanted the warmest leads possible. I was losing my edge on how to even approach UCCs because I had become so adjusted to higher quality material. I felt I had earned my way past them or that UCCs no longer offered the same value they once did.

So it was enlightening when I watched a junior account rep fresh out of college bring in more than 20 applications in his first week just from UCCs. Few funded, but I was impressed by his ability to engage prospects and bring in paperwork on leads I considered to now be crap.

He was hungry. He was new. He also realized that if he couldn’t bring in applications, that he’d be fired pretty quickly. He didn’t have the luxury of telling management that the leads sucked and to give him something else. This was all he would be given.

Watching him brought me back to my first few months as an underwriter in 2006 when there were very few MCA ISOs in existence. One day when deal flow was very slow, I was given a binder full of names and phone numbers of business owners who had applied for a mortgage in the past few years. The boss told me to “underwrite these files.” I learned immediately that all I was doing was cold calling random businesses. As a brand new hire, I was scared that if I didn’t “underwrite” them that I would be fired. So I started calling them with an offer to buy their future credit card receivables (the Merchant Cash Advance term was not widely adopted yet).

I got in applications and statements, I underwrote them, and then if approved, converted their merchant processing accounts and funded them. I didn’t get a commission because I was a salaried underwriter. All I hoped was that enough would fund (and not default) that I would be able to keep my job.

Eventually I was on a team where it was the responsibility of the underwriters to pitch the merchant on the product, gather the docs, close them on terms, underwrite the file, and fund it. The ISOs would just send us a lead and make 8-10 points if we somehow turned it into a funded deal. A few ISOs were sending us pure garbage, random names and phone numbers (literally a first name with no last name and a phone # of a non-lead) and passing them off as leads to see if our underwriting team could turn them into deals that they’d get paid on. Some were shocked when they heard we funded them. Others were mad that we weren’t funding enough.

As the company grew and the industry expanded, It eventually became normal to receive an application, 4 months merchant statements, 4 months bank statements, lease, voided check and a driver’s license and communicate with an ISO who did almost all of the legwork. All I had to do was underwrite the deal. When someone would submit much less, I got frustrated that I even had to look at it. My job was to underwrite files, not make half promises to ISOs based off of very little information. With so many completed files being submitted every day, I began to look at incomplete files differently. The fear that I would lose my job wasn’t there because I was already approving millions per month.

Fear was a huge motivator for me, especially in sales where I had no base pay. You either turned shit into gold or you lost.

It’s amusing to see how opinions vary today around the industry. Some ISOs still swear by UCCs, some stopped bothering with them years ago. Some say mailers are great. Others say they have tried them and they were terrible. Press 1s are the worst or Press 1s get deals funded. Web leads bring in too many annoying startups or web leads are the only type of leads that work.

What sucks and what doesn’t is undoubtedly affected by your attitude. If you’re used to the Glengarrys, then how patient will you be for what veterans consider to be junk?

In the upcoming March/April magazine issue that will be mailed out at the end of this month, I interviewed a 25-year old sales rep who had much more on the line than the fear of just losing his job. He became very successful after just a few years of cold calling.

For anyone out there who has bought leads only to bash them afterwards, was it really because they were bad? Or was it because you weren’t hungry enough?

It makes all the difference.

Revenue Recognition for the MCA Industry

March 1, 2015This is question #6 in a 6-part interview series about Merchant Cash Advance Accounting between deBanked’s Sean Murray and Yoel Wagschal, CPA and Christina Joy Tharp.

- 1. Merchant Cash Advance How to Guide Intro

- 2. Do I Need a Special MCA Accountant?

- 3. and 4. Recording Merchant Cash Advance Transactions on the Books

- 5. Merchant Cash Advance Accounting Pitfalls

- 7. Q&A – Real questions that MCA companies or syndicators have

Q: How should funders record revenue?

A:

The accounting of MCA companies must not show their transactions in a way that cash advances can be seen as loans. As we all know, a lot of people in the law enforcement community wish to compare MCAs to lending companies. They would like to conclude that MCAs are lending money at a higher interest rate than is currently allowed by law.

The accounting of MCA companies must not show their transactions in a way that cash advances can be seen as loans. As we all know, a lot of people in the law enforcement community wish to compare MCAs to lending companies. They would like to conclude that MCAs are lending money at a higher interest rate than is currently allowed by law.

When our firm speaks to clients in the MCA industry who continually use the loan method of accounting, it makes our firm very nervous for them. We see that MCA companies are unwittingly affirming what those law enforcement communities want to allege.

By keeping your accounting books on an established lending method of accounting, you are setting up your company for lawsuits while simultaneously setting up the industry for scrutiny. There is one thing we all must agree on: MCA companies must strive against accounting procedures that will ultimately classify them as loan sharks. If an MCA company is unsure as to how to set up their accounting so as to reflect MCA standards, please contact a knowledgeable CPA who can guide you appropriately.

In general, revenue is recognized when a specific critical event has occurred and when the amount of revenue is measurable. Every American business recognizes revenue and gains when goods and services, merchandise, or other assets are exchanged for cash (or claims to cash). However, there are a number of issues with the old US GAAP way of revenue recognition, especially for MCA companies.

A lot of companies are struggling in their attempt to establish the right path for their specific industry. What happens is that certain companies in the same industry conclude differently than other companies and this leads to inconsistencies in reporting. This is why the accounting standard setters now feel a need for new revenue recognition standards. As most accountants are aware, the new standards will be put into practice over the next two years.

Unfortunately, although the new standards reach a wide variety of industries they have not specifically addressed the MCA industry. The MCA industry has its own challenges in accounting for revenue, specifically the ‘right’ way to account for purchasing future sales. Whenever the topic comes up it soon turns into a hot debate regarding how and when to recognize revenue.

Going into all of the nuances would be too complex and truly each side of the argument may have merit. The real issue is when revenue should be recognized. One option is to recognize revenue at the time of funding. The other option is to recognize revenue on an ongoing basis (pro-rate when funds are being collected).

Here we will go back to our initial example and show the difference between the two options. All we need to change is journal entry C and journal entry D.

Here are the original entries, which show immediate revenue recognition:

| Accounts | Debit | Credit |

| Accounts Receivable | $100,000 | |

| MCA Cash | $70,000 | |

| Revenue | $30,000 |

| Accounts | Debit | Credit |

| MCA Cash | $1,000 | |

| Accounts Receivable | $1,000 |

Here we use the deferred method, which show ongoing revenue recognition:

| Accounts | Debit | Credit |

| Accounts Receivable | $100,000 | |

| MCA Cash | $70,000 | Deferred Revenue | $30,000 |

| Accounts | Debit | Credit |

| MCA Cash | $1,000 | |

| Accounts Receivable | $1,000 | |

| Deferred Revenue | $300 | |

| Revenue | $300 |

There are two other methods, both of which are completely incorrect and both of which our accounting firm has seen in use. The first incorrect method is when revenue is only recognized at the end – when the contract is completely paid off. This method could get your organization into real trouble. For instance, what if the contract is renewed? In those terms, a contract could renew over and over and the MCA company would never recognize the revenue. This could lead to the IRS charging you (even criminally) for tax evasion.

The second incorrect method is the loan method. This method calculates each payment’s interest and principal (similar to a conventional loan). As we outlined above, using the loan method of accounting only sets your MCA company up for scrutiny and legal action. Your own books could be used as evidence to show that your company is violating usury laws.

In conclusion, if it looks like a duck, quacks like a duck, and swims like a duck – it’s a duck! Be sure your accounting books do not paint the portrait of a loan company. Simply calling yourself a MCA company is not enough – you must be a MCA company through and through.

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

Advice to New Loan Brokers, ISOs, and Funders

February 24, 2015 Some words of wisdom to avoid having a bad experience in this industry:

Some words of wisdom to avoid having a bad experience in this industry:

1. If you can’t afford a lawyer, don’t be a funder. This is a litigious business and despite the myth that commercial financing is unregulated, there are plenty of ancillary laws to adhere to. States, FTC, OCC, IRS, etc.

2. Have a lawyer review your contracts (merchant agreements, ISO agreements, syndication agreements, etc.) If you can’t afford one or don’t want to take the time to do it, this business might not be for you.

3. Don’t send your deal to someone with a free email address (yahoo, gmail, hotmail, etc.).

4. Don’t send your deal to some random company just because they posted something on a forum, LinkedIn, or somewhere else. Check them out on Google, ask other forum members to vouch for them. Be extremely smart and overly diligent about it.

5. This is not a get rich quick business or industry. You can lose money funding and syndicating. You can technically also lose money brokering on commission clawbacks for deals that go bad right away.

6. Leads are expensive. Do not launch an ISO with only 2 grand in the bank.

7. Learn to generate your own leads and you will save yourself a lot of stress down the road.

8. A wise man once told me it is better to build a book of business and a long lasting passive income than to grind it out for a quick buck month after month. What’s your strategy?

9. You will lose deals, commissions, arguments, and occasionally your mind. Accept your losses when they happen and focus on the next deal.

10. Use appropriate language. A company that buys future revenues is not a lender and their financial transactions are not loans. Loans have noticeable things like interest rates and fixed terms. Make sure you know which one you’re talking about at any given time.

More Red for OnDeck (ONDK)

February 24, 2015 Back in the red?

Back in the red?

It looked like the tide had finally turned. After 8 years and just in time for their IPO, OnDeck had pulled off their first quarterly profit, a meager amount of $354,000. But it was a start right? After their debut on the NYSE, the price swung heavily from a high of $28.98 to a low of $14.52. It closed at $19.37 right before the report was released.

OnDeck reported a $4.3 million loss for the 4th quarter and an $18.7 million loss for the year. Despite this, their margins are definitely improving.

The company issued $369 million in loans last quarter, bringing the 2014 total to $1.2 billion. Sales and marketing expenses doubled in 2014 over the prior year with CEO Noah Breslow and CFO Howard Katzenberg acknowledging on the call they’ve made a big go at TV and radio advertising.

Competition? What competition?

Noticeably, the average APR of loans originated in the fourth quarter was 51.2%, down from over 60% in Q4 of 2013.

One analyst asked if competitive pressures were leading to the reduction in interest rates but Breslow said that wasn’t the case. If anything their closing rate or “booking rate” has been improving and rates coming down is an initiative they’ve taken up on their own. Merchants are actually shopping less according to them.

“Overall this market is still characterized by extreme fragmentation,” Breslow said. “The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.”

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

So was it just a weird quarter? Under Guidance for First Quarter 2015 and Full Year 2015 in their quarterly report, they suggest another long year of losses ahead.

To infinity and beyond!

The economic and regulatory environments couldn’t be any more favorable to a company that now has almost a decade worth of data under its belt. But unfettered growth still seems to be the number one priority on the agenda. Breslow and Katzenberg spoke optimistically about their recent entry in the Canadian market and the potential to set up shop in other countries. As for the OnDeck Marketplace… surprisingly they claimed its only real purpose is to diversify their funding sources. They are not aiming to become a marketplace but rather they view the OnDeck Marketplace as just one of many vehicles to sell off loans.

So when does the profit part come in? None of the analysts on the line asked about profit. They mostly all offered their congratulations on a “great quarter”. Coincidentally they were almost all from companies that originally underwrote their stock offering.

Six months ago I wrote that OnDeck’s lack of profits has been intentional. In An Insider’s Perspective, I wrote, “What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market.” Nothing has changed.

As long as they have cash in the bank, they’re going to keep pursuing growth. They had $220 million in cash and cash equivalents as of December 31st. So for now that means continuing to turn up the marketing heat to increase volume domestically while planting seeds in other markets like Canada.

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

Those rates are too high low

OnDeck’s price jumped in afterhours trading. The market is chalking up the results as a positive. It’s just another losing quarter in a long line of losing quarters for OnDeck and they’ve promised more of the same in the year ahead. Nothing to see here folks, business as usual.

OnDeck may have made it easier for small businesses to get a loan, but they have yet to prove since 2006 if their methodology can actually make money. That should be a wake up call to critics that complain their interest rates are too high.

It is quite possible that their interest rates are actually too low. At an average of 51.2% APR, that’s a heck of a theory to consider.

But it looks like it’s true.

OnDeck 4th Quarter Earnings Call

February 21, 2015 OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

This is a surprisingly crucial moment for OnDeck who has recorded losses every quarter since inception except for the one just prior to the IPO. Since then the company has been confused as a Lending Club for businesses. The companies differ in that OnDeck’s core business is lending and Lending Club’s is servicing fees.

Critics have called out OnDeck’s high interest rates which top out at 99% APR.

In just a couple months, OnDeck has bounced from a high of $28.98 per share to a low of $14.52. It closed Friday at $18.37.

It’s Okay For a Business to Act Like a Business

February 10, 2015 A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

McCarthy wrote that achieving a transformation, “will depend in part on facilitating greater transparency, accountability, and fairness across our sector, and reining in predatory actors.” He cuts right to the chase by attacking lenders all while ignoring the reality that businesses are regularly preying on financial companies too, especially in the technology age.

It’s an epidemic. There is actually an entire industry association that is dedicated to preventing repeat merchant fraud. Respecting that small business is the backbone of this country though, it probably wouldn’t be appropriate to draft a Lenders’ Bill of Rights, whereby merchants promise not to deceive, lie, or commit fraud against them. Instead the industry deals with it quietly, investing in new risk infrastructure and ultimately passing the costs on to the good borrowers.

Merchants aren’t inherently bad, but neither are the companies that provide them with financial services. Let’s agree that the world is good but that bad actors exist.

McCarthy’s argument for a Small Business Borrowers’ Bill of Rights is premised on the assumption that in every commercial financing transaction, one side is painfully unaware and uneducated about what’s going on around them despite being an owner, president, or CEO of a company.

I think a dose of self-deprecating reflection is healthy and 2014 definitely brought out many discussions about how to increase transparency and better serve small business. But there’s a line between self-improvement and self-loathing that nobody should lose sight of.

It’s okay to make a profit

It’s okay to make a profit

Imagine that the CEO of a widget retailer grossing $2 million a year is looking for a new widget wholesaler to buy product from. The CEO sits down with a prospective wholesaler and asks for a quote. The wholesaler says they have deals with domestic widget manufacturers and Chinese exporters and based upon these relationships and the circumstances they can sell them in bulk at a price of $2 per widget. Unbeknownst to the retailer, the wholesaler quoted a competing retailer a price of only $1.80 per widget earlier that day. But this is business and if the wholesaler can charge more to this company, he will.

Unsure if he should accept the terms, the retailer pulls out a Widget Retailers’ Bill of Rights and demands the wholesaler charge not a penny more than what would adequately compensate the wholesaler for his work in the name of fairness. He also demands to be presented with unbiased facts on costs, benefits, and risks of every widget manufacturer, so that they can compare products on an apples-to-apples basis without pressure. And if they don’t do this, they will get Washington involved.

If you think this is supposed to be silly, it’s not. It’s McCarthy’s worldview applied. What’s missing from this scenario is that the wholesaler has a widget cost basis of about $1 and is selling them for $1.80 to $2.00, a nice margin. The retailer will sell these widgets for $10 a piece in their stores for an even better margin.

Maybe it’s the consumer that ends up getting screwed on price but even that seems unlikely since widgets are selling off the shelves at lightning speed. So what would be fair and adequate compensation for every party involved? What if the manufacturers are producing widgets for 7 cents each? Is there another layer of possible unfairness here?

Everybody has some kind of incentive and that’s how a marketplace works. If the price is too high, customers won’t buy, they’ll negotiate the price down or they’ll shop elsewhere.

In McCarthy’s Bill of Rights, he rejects the very notion of self-interest. “Some lenders charge higher interest rates just because they can,” he writes. This is how capitalism works. Find your customers price point and sell for a profit. Don’t forget we’re talking about commercial transactions only here!

You ever wonder why they’re called deals?

I’m reminded of someone from the peer-to-peer lending world that once asked me why folks refer to merchant cash advances as deals. They’re not loans, they’re not units, they’re deals!

And true to their deal making roots, terms on them are almost always negotiable. Two companies come together to make a deal… get it? Traditional merchant cash advances are also not loans. They’re literally contracts negotiated by businesses to sell future revenues at a discount in return for upfront cash flow. The concept couldn’t be any more commercial.

And over on the lending side, McCarthy might have you believe that the average small business CEO is unsophisticated shark bait in this unfair world so I pulled up the stats on the industry’s most famous small business lender. According to the S-1 filing, 90% of OnDeck Capital’s borrowers gross between $150,000 and $3.2 million a year in revenue and have been in business for an average of 7.5 years. These are bright companies.

Curiously there’s a group of financiers that are unabashedly capitalist. They will charge whatever they can get away with, take half a business if they want and even call their customers shark bait to their faces. Hopefully they clean up their act before Washington steps in! Thankfully the regulators have not yet put an end to ABC’s Shark Tank though I’m sure McCarthy will propose they do so.

That means you too Marcus Lemonis… Rumor has it you do things to make money all while applying high pressure sales tactics on TV to get people to agree and without telling the business owners the unbiased facts about every other financing option in the entire marketplace.

If it’s okay on TV, it has to be okay in real life.

Business on a deeper level

Business on a deeper level

I didn’t mean to take a stab at Brayden McCarthy personally but his message reflected a culmination of emotions that some people feel in this industry when they’re struggling to keep up. They can’t believe that a client would take something more expensive when they had an offer for something less expensive. Almost 7 years ago I competed against another salesman for a client to whom we both made almost the exact same offer; Same advance amount, same holdback %, same closing fees, but a different receivable purchase amount. The ONLY difference was that the other guy’s price was $2,000 more expensive. Everything else was the exact same and he knew it. And you know what happened? He went with the more expensive offer…

I remember confronting that salesman about it a few days later after I had let my anger cool down. A lot of thoughts had gone through my mind, that perhaps the other guy had lied, coerced him, or conducted some kind of shady trick. Why else could this have happened?! It seemed completely illogical. Of course it was none of those things. The other salesman developed a strong rapport with the customer and they spent most of their time talking about football on the phone.

“He freaking loved me,” the salesman said.

“That can’t be it,” I thought. Still hurt and determined to get the truth, I sent the lost prospect a very long email complete with mathematical formulas (I even used exponents, square roots, and fancy squigglies for good measure) to show how much he would’ve been better off with my offer. He responded almost immediately. “You see, this is exactly why I didn’t go with you,” he wrote.

While I was busy trying to open the customer’s eyes to the magic of the Black-Scholes model, the other salesman was talking to him about whether or not Eli Manning was really franchise quarterback material.

Still a very inexperienced salesman at the time, I had learned a new truth. Business went deeper than just prices, market efficiencies, and a desire to make money, it was also about relationships. Treating one side like an uneducated idiot has become a cornerstone of regulations to protect consumers, and perhaps even rightfully so but imagine the widget retailer grossing $2 million a year walks into a business negotiation and is immediately told that he is too dumb and too unaware to not only understand how to assess a deal but to foresee the consequences of his own decisions if he makes a deal.

Transparency is good, relationships are greater. There’s no need to codify sour emotions into an awkward Bill of Rights. Let two businesses make a deal. It doesn’t have to be the smartest, the fairest, or the best, just something both ultimately agree to. I can’t imagine it any other way.

The Industry’s Bad Paper

February 8, 2015 Sometimes deals go bad. But what happens next?

Sometimes deals go bad. But what happens next?

I just finished reading, Bad Paper: Chasing Debt From Wall Street to the Underworld on a recommendation from a friend. In it, author Jake Halpern walks readers through the shadowy world of consumer debt collection. It was eye-opening to say the least.

Halpern’s research uncovered that consumer debts with seemingly no original paperwork is sold, resold, and resold again to companies that the debtor never heard of and would not recognize. A debt’s record amounted to some fields on a spreadsheet where the information is not always correct and might even have been collected already by someone else.

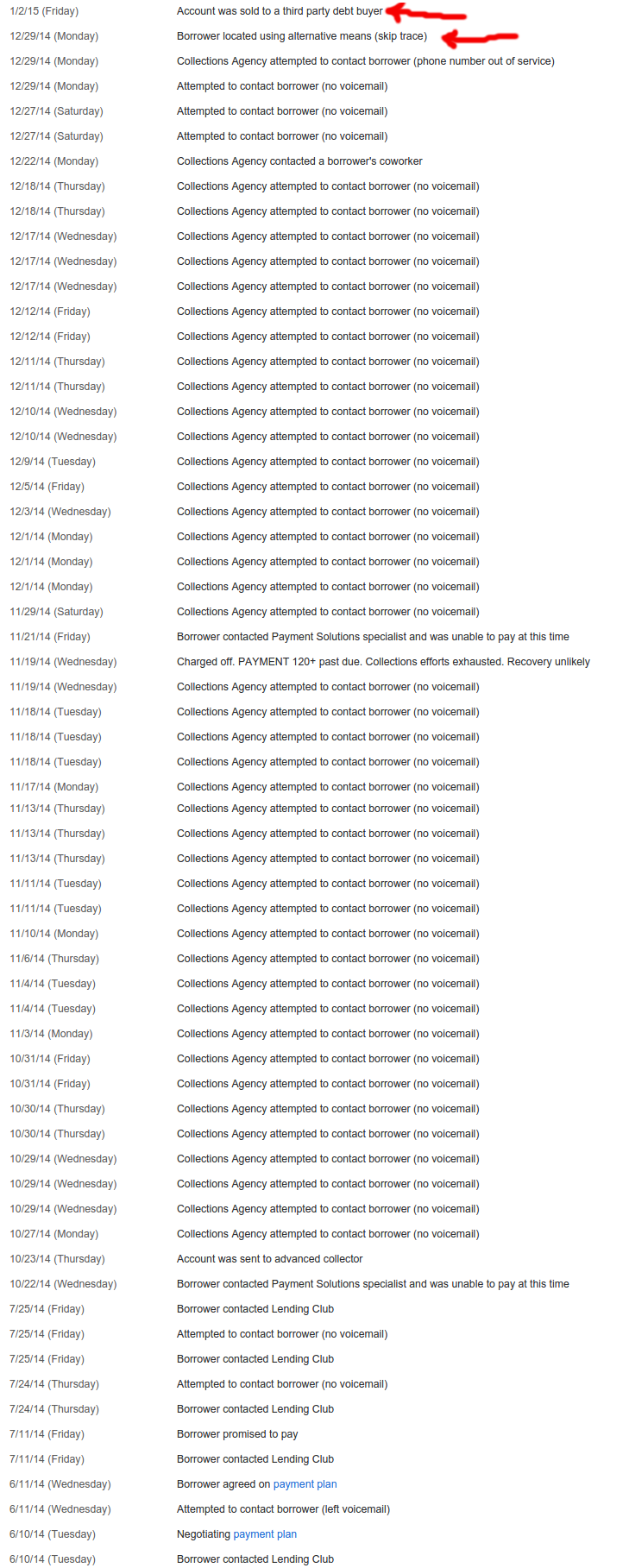

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

I’ve found that a lot of my defaulted loans thus far have gone bad in the first few months, a pattern that looked more like fraud than borrower hardship. It actually prompted me to call Lending Club and speak to a representative about it, who explained that they’re doing all they can to prevent fraud.

They were pretty relentless on this particular file, a nurse that was making $60,000 a year sounded like a winner. They had virtually no debt but the loan was supposedly used to consolidate outstanding debt into one monthly payment at the rate of 9.67%. The story didn’t exactly add up but since I don’t actually get to talk to the borrowers or look at their paperwork, I’m essentially just playing a numbers game.

That debt has been sold off and I as a note holder do not appear to be entitled to any money on the sale of it, not even pennies on the dollar. Bummer.

Because of platforms like Lending Club, I wasn’t the only one to lose out. 277 other retail investors who I don’t know and have never met participated in it with me. We’re all playing the numbers and we lost on this one.

With 1907 notes acquired on the platform so far, I’m not emotionally invested in any of them. How can I be? I have no idea who the borrowers are. I don’t even know their names! All I can do is diversify and make decisions based off of statistical analysis. If the borrower stops paying, go after them hard whoever they are!

Meanwhile in commercial transaction land

When it comes to merchant cash advance and business lending, the collection rules are different but so are the relationships. Even with strong advancements in automation, phone interviews remain an integral part of the underwriting process. A risk analyst typically calls the business owner, their landlord, and even several of their suppliers. Large dollar amount deals may even be presented to an entire risk committee for approval.

Suffice to say, pesky things like signed contracts do not usually prove elusive when a collector in this world gets their hands on it. Many commercial funding providers even record phone calls with the business owners where they get an additional verbal confirmation to the terms and conditions of the arrangement.

The collections process usually begins with the sales person or sales office that negotiated the terms with the business. Back when was I was an account rep, my commissions were paid in two pieces, upfront and a residual. That meant almost half my pay on a deal was tied to its performance. If a deal started to fall apart or defaulted, I had a personal stake in restoring the business to good standing.

The Fair Debt Collection Practices Act does not cover commercial transactions. And in the case of traditional merchant cash advances, there is likely no debt at all in a default, but rather a possible case of stolen receivables.

In the event where a deal I brokered was suspected of diverting receivables, I’d be the first one to know about it and the first person tasked with fixing it. That meant calls to the business, their home phones, their cell phones, and when necessary their landlord. If none worked, then their suppliers. The first goal was to determine if the business was still operating and in the vast majority of cases where defaults happened, they were.

Hardship was sometimes cited as a reason for breaching the agreement but not always. With a chunk of my paycheck on the line, I had to talk them back into good standing and unlike debt collectors, I didn’t have the ability to renegotiate the terms, lower a payment or cut them slack. It was back to the way it was or nothing.

It escalates

Some returned to good standing and others played hardball. The deal’s original underwriter might then involve themselves and if they failed, then on it went to the internal funder’s portfolio management/collections team.

This is why the situation here on out is different: Imagine a doctor sells you the accounts receivable of all his patients for a discounted price. The doctor gets cash upfront and the buyer will hopefully collect the full value of the accounts receivable to earn a profit.

Now imagine the doctor accepts your cash upfront and then also collects the accounts receivable from the patients and shuts you out. In traditional merchant cash advances, collectors aren’t going after debt, but rather acquired property that is rightfully theirs. The business has shut them out of receivables they purchased.

If internal collection efforts fail, they can attempt to freeze various receivables the business might have. Merchant processing proceeds are usually the first stop. If the business accepts credit cards, the merchant processor can be instructed to freeze all or a percentage of the revenues without a court order. This is easier said than done but it does work and there are even a few third party collection firms that specialize in this.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

Some business owners are shocked to learn that a deal they made over the phone with people they never met will actually track them down and sue them. Unlike consumer debts which might only be a few hundred dollars, commercial transactions are typically tens of thousands or hundreds of thousands of dollars. They will definitely pursue it.

On the largest default I ever presided over as an underwriter, the business owner said something to the effect of, “I stole your money. Let’s see how good you are at getting it back.” He said this just 24 hours after we had wired him the money. Ouch!

That happened more than six years ago but it was something I’ll never forget. A quick Google search today reveals that guy is still alive and kicking as he was recently interviewed about his success in amassing a restaurant empire in Florida.

Over the next couple years, I would hear variations of that “I stole your money” line from other businesses, typically on deals larger than $75,000. These were strategic defaults designed to strong-arm the funding company into a settlement or an attempt to simply walk off with the funds altogether. In other words, fraud.

All this does is raise the cost for the next business that conducts themselves honestly. It’s a damn shame.

Merchants prey on Wall Street

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

One experience I had was with the owner of a steakhouse in NYC that flew up from his residence in Brazil to try and close me (as the underwriter) on purchasing roughly $400,000 of his future credit card sales. What he didn’t know is that the night before I checked out the place anonymously by having dinner there with my wife. When the bill came, the server told me they no longer accepted credit cards. The next morning, the owner who spoke only in Portuguese arrived in tow with a translator and a lawyer. They traveled directly from JFK to our office, to which I informed them of the decline. They had stopped accepting credit cards a day too early for their scam on us to work and the restaurant closed two months later.

In another case, a souvenir shop in NYC asked if I would come by to pick up his application and statements in person since we were locally-based. After spending a half hour with the guy at his shop, I returned back to the office only to find out that he gave me doctored bank statements.

And then there’s the owner of a florist that made a career off of robbing merchant cash advance companies. The store, which is close to my hometown, had obtained more than 20 merchant cash advances by late 2008 and defaulted on all of them, netting the business close to $1 million. They hoped to make me victim number 21 but we figured it out in the 11th hour before the funds went out. The business is still there today though I’m unsure if it’s still the same owner.

In 2015, fake documentation is an epidemic. Underwriters in the industry cannot rely on faxed or emailed statements alone. They should be verified through APIs or through direct contact with banks. Many funding providers go a step further and actually request the usernames and passwords to business bank accounts just to be absolutely sure that what they’re seeing is what they’re getting.

But as tech-savvy millenials become the face of American small business, the ante is being upped on fraud. One underwriter told me they saw something even more worrisome, a fake bank website.

The scam is this: Knowing the underwriter is going to request the username and password of the business bank account to verify the statements, the applicant has designed a functional replica of a bank website on a web domain they own, one that looks like the bank name. The unsuspecting underwriter logs in to it and verifies the account data. There’s only one problem, it’s all fake.

While this appears to be an isolated event, it just goes to show that the war on bad paper is entering another phase.

Bad paper

While fraud is a substantial cause of the bad paper in the merchant cash advance and business lending industries, hardship does have its place. It is perhaps fortunate that in the commercial space, the paper isn’t sold off into some convoluted world of debt collection. More than likely the business will be dealing with the actual funding provider the entire way through the collections process, not a debt buyer ten levels down the chain. That’s good and bad for them.

It’s good because the owner will able to discuss matters related to the default with the party directly familiar with the original contract.

It’s bad because any chance that the contract and proof of the agreement will somehow get lost in the shuffle is pretty much nil.

Jake Halpern discovered that debtors can win lawsuits by simply challenging the debt buyer to produce evidence the debt is owed. That might work in the consumer world where debt changes hands ten times. On the commercial side, bad paper is an enduring companion. It may be business-to-business but somehow it’s more personal.

Contrast that with the Lending Club nurse who I know only as Member XXXXXXX. His/her debt is in the wind. I have no idea who they are, nor anything about the 277 other people that invested with me.

Halpern spent 256 pages tracing the path of a debt, the companies that bought it, sold it, stole it, and sued for it. It’s amazing how complex it is.

If he were to do a book on bad paper in merchant cash advance, it would go like this:

The business defaulted, the funding provider tried to collect and then sued. The End.