Loans

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

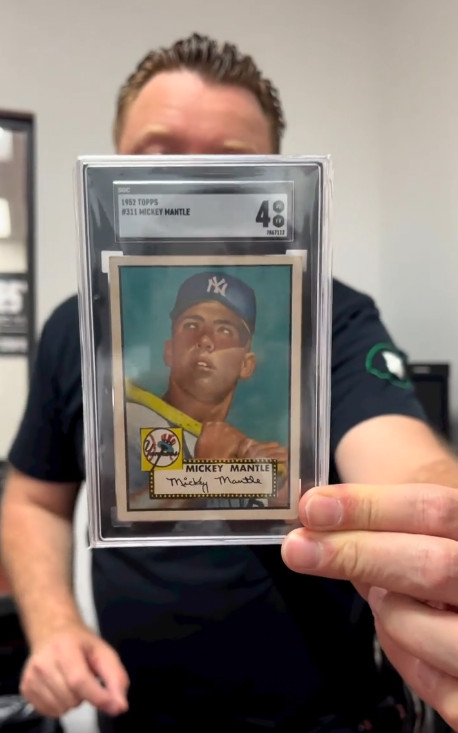

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

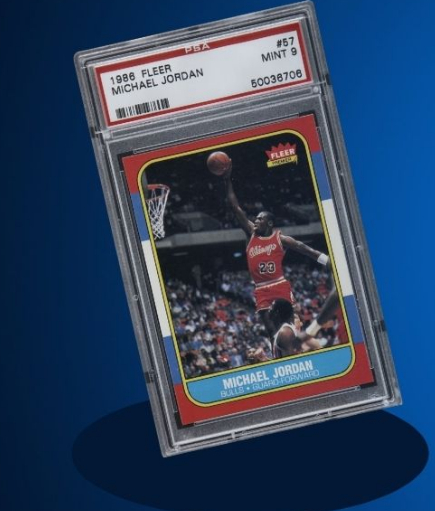

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

Prosper Marketplace Originated $891.9M in Loans in Q2, Records $42.6M Profit

August 23, 2022 Despite some uncertainty in the lending markets, Prosper Marketplace had a fairly good quarter. The company originated $891.6M in loans in Q2, nearly double the volume over the same period last year. Profitability too was there, coming in at $42.6M, up from a loss of $5.8M in Q2 2021.

Despite some uncertainty in the lending markets, Prosper Marketplace had a fairly good quarter. The company originated $891.6M in loans in Q2, nearly double the volume over the same period last year. Profitability too was there, coming in at $42.6M, up from a loss of $5.8M in Q2 2021.

Notably, Prosper did acknowledge that the fair value of its loans were being affected by an increase in capital markets volatility and benchmark interest rates but neither were enough to hurt the company.

Prosper is a holdout of the peer-to-peer lending era in that it still has a “note channel” for investors. Ninety-one percent of all loans funded in the second quarter, however, were done through the Whole Loan Channel, up from 87% during the same period last year.

Prosper is in the business of originating consumer loans with 3-5 year terms and interest rates ranging from 5.31% to 31.82%.

Need a “Lenda?”

July 13, 2022LendingTree helped Linda get a “lenda.” Former SNL star Molly Shannon, playing Linda, explains to waitress, Brenda, how hassle-free finding a personal loan through LendingTree was for her. The newly released commercial uses assonance to get viewers to understand how easy it is to get the best possible loan. In the commercial, Brenda is under the impression that LendingTree is only for “big spendas” but learns that they will find her a lender despite the circumstances.

Another “Linda lenda” commercial is featured on LendingTree’s home page where Linda tells her niece how they assisted her on a home loan as well. The objective is get viewers to understand how getting a loan can be just as effortless for them as it was for Linda.

New Owner of Loan.eth Says its Worth Millions

June 8, 2022 Less than two months after spotlighting a new domain name market linked to the Ethereum blockchain, the name loan.eth was sold on a secondary market for the equivalent of $45,000. It’s not a website domain like one would expect with a .com or a .net, but rather a crypto wallet address shortener that can double as a screen name and authentication service on web 3.0. That’s just the tip of the iceberg of the utility that a .eth domain can offer.

Less than two months after spotlighting a new domain name market linked to the Ethereum blockchain, the name loan.eth was sold on a secondary market for the equivalent of $45,000. It’s not a website domain like one would expect with a .com or a .net, but rather a crypto wallet address shortener that can double as a screen name and authentication service on web 3.0. That’s just the tip of the iceberg of the utility that a .eth domain can offer.

Although most people may not be familiar with .eth domain names, the new owner of loan.eth, who goes by @BloomCapital_ on twitter, is so confident that such names will be adopted in the future, that he believes the value of this one will be many times what he paid for it.

“Just so it has to be said, Loan.eth won’t be sold for less than $10M,” Bloom wrote. Bloom said he considers loan to be the top .eth name that he has.

Prosper Marketplace Receives Full Forgiveness of Its SBA Loan

May 18, 2022Three months after the SBA told a Sioux Falls small business lender that it wasn’t eligible for PPP loan forgiveness because it was involved in lending, the same agency approved full forgiveness for one of the nation’s largest consumer lending businesses, Prosper Marketplace.

“On March 21, 2022, we were notified by the SBA that all principal and interest under our PPP loan, totaling $8.6 million, was forgiven through a full forgiveness payment made on March 15, 2022 by the SBA to the lender of our PPP loan,” Prosper reported in its Q1 earnings. The company also announced that it had facilitated $560.6M in Borrower Loan originations in the first three months of this year so far.

Technically, Prosper is a “credit marketplace.” All loans originated through the marketplace are made by WebBank. Prosper facilitated $1.9B in loan originations last year alone.

Prosper was among the lenders that actually turned a profit in 2020, $18.5M to be precise, on $1.5B in loans facilitated.

Developed and Developing Credit Markets, How Many People Are Actually Underserved or Unserved?

April 7, 2022 TransUnion recently conducted a global study, “Empowering Credit Inclusion: A Deeper Perspective on Credit Underserved and Unserved Consumers.” Both developed and developing credit markets were observed including the United States, Canada, Colombia, Hong Kong, India, and South Africa. The study further focused on the journey of credit disadvantaged consumers and how they migrate from being underserved to credit served, and the ability to gain access to additional credit opportunities. New-to-credit consumers – individuals who have opened their first product within the past two years – were not considered.

TransUnion recently conducted a global study, “Empowering Credit Inclusion: A Deeper Perspective on Credit Underserved and Unserved Consumers.” Both developed and developing credit markets were observed including the United States, Canada, Colombia, Hong Kong, India, and South Africa. The study further focused on the journey of credit disadvantaged consumers and how they migrate from being underserved to credit served, and the ability to gain access to additional credit opportunities. New-to-credit consumers – individuals who have opened their first product within the past two years – were not considered.

Among the US market, about 45 million consumers have been categorized as unserved or underserved. Approximately 8.1 million are unserved or invisible to the credit bureau while 37 million are underserved, resulting in 14% of the adult population.

In developed countries versus emerging economies there is a large contrast between what percent of the population is still credit unserved. In Canada about 7% of the adult population is unserved while Colombia’s percentage reaches 44% and India is at 63%.

Nidhi Verma, Vice President, International Research and Consulting at TransUnion stated, “…I think a lot of it has to do with, it’s not a saturated market quite yet, in terms of the presence and the availability of credit access, and consumers actually having to rely on credit or understanding the importance of private credit in their daily lives. And that’s generally the essence of a developing credit economy.”

According to the study credit migration decreased post-pandemic amongst all regions. Two cohorts of consumers were analyzed, each over a two-year time period. The first during the pre-pandemic period from March 2018 to March 2020 and the second through June 2019 to June 2021.

Around one in four consumers identified in the underserved population were becoming credit served pre-pandemic. Due to the pandemic there was a drastic halt and a cut back in lending. The migration rate of transitioning from being underserved to served from a credit perspective went down from 24% to about 22% not only in the US but within other global markets as well.

Unserved consumers are faced with a “chicken and egg conundrum” of how to get their first credit card without a credit score or credit history. Although many lenders are hesitant to extend credit to these consumers, alternative data is an option.

“Especially in the current environment, where most lenders, financial services are seeking to grow their portfolio,” said Verma, “there’s certainly a huge opportunity of acquiring these new customers that have no scores or credit history, and leveraging incorporating alternative assets, such as your rental information, such as your deposit account information, incorporating that in the underwriting strategies, so we find fewer consumers to be credit invisible.”

This is applicable for both a growth for lenders and consumers to potentially find an upward mobility with the ability to get better access to credit, financial products, and services.

“Having access to credit, without overextending, can help consumers with a financial situation in daily life and alternative data, which would be just basically one of the gateways to enable that credit score for consumers,” Verma noted.

According to Verma, TransUnion is making efforts to help those who are credit invisible be seen. “We’ve continued to invest and enable alternative data assets, solutions in each of the markets to make sure that those can be incorporated for lenders to make lending decisions in lending criteria.”

Alternative data provides an opportunity for more consumers to become visible with credit history and in the credit market. This will also ensure to underserved consumers that there are more alternative products with lower cost of credit, a key finding that lenders could leverage in their day-to-day pricing and underwriting strategies.

BNPL Survey says 25% of Customers are “Financially Vulnerable”

April 3, 2022 The Financial Health Network, an organization that attempts to quantify the nation’s financial health, recently released the results of their first truly nationally representative survey titled Buy Now, Pay Later: Implications for Financial Health. The survey seeks to understand who uses Buy Now Pay Later (BNPL) and their experiences with the service, and touched on what kind of financial habits are coming about for those BNPL use.

The Financial Health Network, an organization that attempts to quantify the nation’s financial health, recently released the results of their first truly nationally representative survey titled Buy Now, Pay Later: Implications for Financial Health. The survey seeks to understand who uses Buy Now Pay Later (BNPL) and their experiences with the service, and touched on what kind of financial habits are coming about for those BNPL use.

“Buy Now Pay Later could be a mixed bag for consumers–on the one hand it provides a convenient and low-cost way for consumers to finance purchases, but there are customers who are using BNPL to make purchases they would not otherwise make,” said Meghan Greene, director of research at Financial Health Network.

According to the release, the data found that roughly one in four users of BNPL are financially vulnerable. Out of this group, a quarter of BNPL users reported struggling to make payments. With this, the survey later mentions that 92% of users reported no difficulty making payments, and 99% stated that they understood the terms and conditions of the product.

“It’s still too early to know the full impact of BNPL on the financial health of consumers, but we do see potential warning signs in the number of consumers,” Greene said. “Particularly those who are already financially vulnerable, who report struggling to make repayments.”

Out of those surveyed, 47% said they would not have made a purchase or spent more than they otherwise would have spent had BNPL not been available. With this being said, it seems that BNPL executives are getting exactly what their product is marketed to retailers to do.

There are many types of plans using the BNPL label ranging from plans which divide payments into four installments with no interest charge (“pay in four”) to longer-term installment loans. Companies like Ikea, Walmart, Urban Outfitters, and thousands of other global businesses have gotten into offering these financial products.

Other interesting finding from the survey are below-

–Short-term BNPL users reported owing an average balance of $330.

–10% of households report having used BNPL in the 12 months prior to November 2021, a significant deviation from other published estimates. Of these, 70% report using a short-term, no-interest BNPL plan.

–Younger and less financially healthy households are more likely to use BNPL. Financially Vulnerable households, as measured using the Financial Health Network’s innovative FinHealth Score(R), are nearly four times more likely to use BNPL than Financially Healthy households (18% vs. 5%). In fact, almost one-quarter (24%) of BNPL users are Financially Vulnerable.

–Despite the recent emergence of BNPL in the United States, almost half (46%) of users had used BNPL three or more times in the previous 12 months, as of November 2021.

–Total U.S. consumer spending on interest and fees from BNPL in 2021 is estimated at less than $1 billion, a small fraction of the estimated $95 billion spent on revolving credit card balances.

–Over 20% of BNPL users do not have or do not use credit cards (roughly the same as non-users).

–More than 40% report having subprime credit scores.

–One in three users of BNPL report that they would not have made the purchase if BNPL were not available. Among Financially Vulnerable BNPL users, over 60% said they would not have made the purchase without BNPL.

Could Siri, Alexa, and Video be the New Frontier for Lenders?

January 25, 2022 The annual fintech study published by Smarter Loans revealed that 25% of respondents had used either Alexa, Siri, or another voice search to find information about financial services.

The annual fintech study published by Smarter Loans revealed that 25% of respondents had used either Alexa, Siri, or another voice search to find information about financial services.

Voice devices, it appears, are not only getting better at answering regular questions, but users are also getting more comfortable even asking them in the first place.

“Alexa, what is deBanked?” for example, returns an accurate reply despite our not having made any efforts to opt-in to the device’s knowledge base. Alexa just knows.

So why bother performing an old-fashioned Google search? Turns out, it’s becoming less common to do. Only 57% of respondents said they discovered the lender they applied with through online search. 13% said they discovered them through social media. 8% came from a friend’s recommendation. 15% found them through a well-regarded “Loan & Financial Directory” (Smarter Loans, who authored the study).

Once on a lender website, users had questions. 27% read online articles and reports, 37% read reviews, 16% called the company, and 9% consulted a friend or family member.

60% of respondents said informative videos about a company or its products would increase their confidence in that company. That could be key since 66% of respondents said that they researched more than 3 lenders before applying for a loan.

All of the respondents resided in Canada. 92% of respondents also said that they were satisfied or very satisfied with their loan provider.