Business Lending

Is Online Lending Really Just Offline Lending?

October 19, 2015 Two weeks ago the Wall Street Journal postulated that online lending’s biggest beneficiary was the U.S. Postal Service. “In July alone, Lending Club mailed 33.9 million personal-loan offers,” it said. “The average monthly volume of personal-loan offers sent through the mail has more than doubled in two years to 156 million in the year through July from 73 million in the same period in 2013,” it added.

Two weeks ago the Wall Street Journal postulated that online lending’s biggest beneficiary was the U.S. Postal Service. “In July alone, Lending Club mailed 33.9 million personal-loan offers,” it said. “The average monthly volume of personal-loan offers sent through the mail has more than doubled in two years to 156 million in the year through July from 73 million in the same period in 2013,” it added.

These figures have some people concerned that there is no network effect for these lending platforms. Last month, Timothy Puls, an equity analyst for Morningstar, said that the value of a company like Lending Club doesn’t grow just because more users are on the platform. That means a continuous stream of marketing is essential since they’ll always need to find new borrowers to sustain the business.

To illustrate how sensitive lenders are to this, OnDeck CEO Noah Breslow spoke to the increasing competitiveness of direct mail in their 2nd quarter earnings call and argued their strategy was to “break through the clutter” and “better communicate our value proposition.” Analysts on the call were concerned by that, which prompted a question by Christopher Brendler of Stifel, Nicolaus & Company during the Q&A session.

Question by: Christopher Brendler of Stifel, Nicolaus & Company

You mentioned in the direct channel about a response rate, talking about a response rate to direct mail. Can you talk about the response rate that you are seeing in that channel? It seems like from an outsider’s perspective we’ve gotten more competitive and it sounds like you’ve had a little bit of a struggle there. We just want to see if there is any color you could add on what the competitive environment is having on the direct channel.Answer by: Noah Breslow of OnDeck

I think what we are seeing really is just an intensified set of activities and you can’t really isolate it down to any single or couple of competitors but it’s sort of both in the offline direct mail channel, we are seeing increased mail volumes over where they were six months ago. And then in the online channel we are seeing increased bidding and so forth for Google Adwords and the like.

Nothing to worry about when it comes to that mail stuff though right? Google Adwords, facebook, instagram, and snapchat are where the real action comes from for online lenders, you might think.

According to Marlette Funding CEO Jeffrey Meiler, that’s not the case. In the WSJ, he admits that 90% of the billion dollars in online loans they’ve originated have come from offline channels.

And maybe that’s because the term online lender might be a red herring. Online lenders don’t only exist in cyberspace, they have offices in the real world just like banks do. And sure, they have websites, but then again so do banks. When you start to boil it down, online lenders look a lot like every other business in existence today. And while it may not be typical for a small business owner to walk into the office of an online lender to get funding, several lenders have said this happens. And for the brokers that arrange business loans, it’s pretty common for them to visit the actual businesses and meet with the owner(s). Not a very online experience…

It may be fashionable to say what separates banks from online lenders is that you have to walk into a bank to apply for a loan, but that’s often just not the case. Most banks offer loans through the form of credit cards both online and through direct mail and they’ve been doing this for decades. The only difference is now they’re competing with other lenders that don’t have local branches for the customer to walk into it, the online lenders. And maybe that’s what the difference is, being branchless could be what defines an online lender.

For now though, a heck of a lot of online lending seems to be originated offline.

World Business Lenders Makes Credit Prediction, Employs Different Model

October 19, 2015World Business Lenders (WBL) Managing Director Alex Gemici thinks the next credit correction will take place within three years, he told a crowd at Lend360 last week in Atlanta. When he and his fellow panelists were asked what keeps them up at night, Gemici said, “irrational exuberance.” He clarified that by saying that there was an incredible amount of capital pouring in right now and insinuated that it’s not all being deployed intelligently. He also pointed to the country’s economic history and said we’re naturally due for a shift in the credit cycle.

From Left to Right: Bob Coleman of the Coleman Report, Jason Rockman of CAN Capital, Craig Coleman of ForwardLine, Alex Gemici of World Business Lenders, David Gilbert of National Funding and Jeremiah Neal of Biz2credit

Part of WBL’s hedge (if you could call it that) against a future industry shakeout, is that their loans are actually collateralized, though they didn’t start out that way. When they launched in 2011, they initially offered unsecured loans and eventually evolved towards collateralizing them with all different types of assets. They have shifted even further in that direction and today the only collateral they accept is real estate. That makes WBL’s model quite traditional by comparison to competing products like merchant cash advances and OnDeck loans. Gemici says however, that they believe in technology and data mining to make better underwriting decisions, just like today’s unsecured fintech lenders.

But while they use technology, their process isn’t fully automated and that’s because Gemici believes algorithms aren’t advanced enough yet to make decisions on their own. You can’t ask Siri whether she’d approve a business loan yet, Gemici joked.

Will business loans backed by real-estate give them a long-term edge over unsecured lenders? Only time will tell. One thing many people agree on however is that there will most certainly be a shakeout when the next economic downturn hits.

Chairman of House Financial Services Committee Requests Information from CFPB on Fair Lending Enforcement Actions, Requests Interview with Director of Fair Lending Office

October 18, 2015 Earlier this month, the Chairman of the House Financial Services Committee, Rep. Jeb Hensarling (R., Texas), sent a letter to the CFPB requesting information related to the Bureau’s recent investigations in to alleged fair lending law violations by auto lenders. This information may be helpful in understanding how the Bureau conducts fair lending focused exams and investigations. The Bureau recently announced plans to conduct its first small business lending focused exams within the next year.

Earlier this month, the Chairman of the House Financial Services Committee, Rep. Jeb Hensarling (R., Texas), sent a letter to the CFPB requesting information related to the Bureau’s recent investigations in to alleged fair lending law violations by auto lenders. This information may be helpful in understanding how the Bureau conducts fair lending focused exams and investigations. The Bureau recently announced plans to conduct its first small business lending focused exams within the next year.

Chairman Hensarling’s letter was co-signed by Rep. Sean Duffy (R., Wis.) and requests emails and other records that document how the Bureau built its recent cases against Ally Financial, American Honda Finance Corp and Fifth Third Bancorp. In each of these cases the CFPB alleged that the companies pricing policies resulted in minorities being charged more than white borrowers. In the three actions, the lenders did not admit or deny wrongdoing.

Chairman Hensarling’s letter also asks if the Bureau will make the director of the CFPB’s Office of Fair Lending and Equal Opportunity, Patrice Ficklin, available for a transcribed interview. An interview may provide lawmakers additional insight in to the Bureau’s efforts to address allegedly discriminatory pricing policies.

Ms. Ficklin recently spoke at the ABA’s Consumer Financial Services Institute where she explained that she expects the Bureau’s upcoming small business lending focused exams to provide the CFPB with useful information about small business loan underwriting criteria. Ms. Ficklin said that this information will assist the Bureau as it begins its work on the small business lending data collection regulations required by Section 1071 of Dodd-Frank.

Chairman Hensarling’s letter requested a response on Ms. Ficklin’s availability by Oct. 13 and the other requested documents by Oct. 20.

Kabbage, Fora Financial and Square Have a Roaring Wednesday

October 15, 2015 Wednesday, October 14th was packed with exciting industry news. Right after Congressman David Scott blessed online lenders, Kabbage announced a Series E round investment led by Reverence Capital Partners for $135 million. The Wall Street Journal said the deal valued the company at over $1 billion, a figure that elevates Kabbage to unicorn status.

Wednesday, October 14th was packed with exciting industry news. Right after Congressman David Scott blessed online lenders, Kabbage announced a Series E round investment led by Reverence Capital Partners for $135 million. The Wall Street Journal said the deal valued the company at over $1 billion, a figure that elevates Kabbage to unicorn status.

At the same time, Fora Financial announced that a Palladium Equity Partners affiliate had made a significant investment in the company. In the official release, Palladium principal Justin Green said, “we believe Fora Financial has developed a highly attractive credit offering and technology platform that have made it a valued provider of financing to thousands of small businesses seeking capital.”

Palladium once held a stake in Wise Foods, the potato chip snack company, and currently counts PROMÉRICA Bank, a full-service commercial bank in its active portfolio. They have more than $2 billion in assets under management.

And then there’s Square, the payment processor and merchant cash advance company who publicly filed their S-1 for an IPO. Their registration form uses the term merchant cash advance 16 times so there is no doubt it’s a significant part of their business. “Square Capital provides merchant cash advances to prequalified sellers,” the document states. “We make it easy for sellers to use our service by proactively reaching out to them with an offer of an advance based on their payment processing history. The terms are straightforward, sellers get their funds quickly (often the next business day), and in return, they agree to make payments equal to a percentage of the payment volume we process for them up to a fixed amount.”

As of June 30th, Square had already racked up a net loss for the year of nearly $78 million. In 2014, the company lost $154 million. While the losses stem mainly from their payment processing operations, they had outstanding merchant cash advance receivables of $32 million as of mid-year which illustrates how much exposure they have with that product.

The three announcements ironically coincided with comments made by SoFi CEO Mike Cagney about the industry’s lack of ambition. “The problem with fintech is that it’s not ambitious enough in terms of its objectives. It’s not really transforming anything,” he’s quoted as saying in the San Francisco Business Times. Cagney went on to categorize Lending Club as just an electronic interface bolted onto a bank to originate loans for them. While his comments hold weight given that his lending company recently just raised $1 billion in a Series E round led by Softbank, it may be fair to say however that Wednesday proved there was anything but a lack of ambition in the space right now.

God Bless The Online Lenders

October 14, 2015 “God bless the online lenders,” said Democratic congressman David Scott while addressing an enormous crowd at Lend360 in Atlanta on Wednesday. Scott kicked off the morning’s events by offering a plan of action for online lenders. “Your industry is faced with some enormous challenges,” he said.

“God bless the online lenders,” said Democratic congressman David Scott while addressing an enormous crowd at Lend360 in Atlanta on Wednesday. Scott kicked off the morning’s events by offering a plan of action for online lenders. “Your industry is faced with some enormous challenges,” he said.

Among those challenges is the aftermath of Operation Choke Point and the Consumer Financial Protection Bureau. On Choke Point, Scott said that the government saw themselves as coming to the rescue after the Four Oaks Bank fraud case. A theme of his speech was that the onus is on the online lenders to make sure the Department of Justice and other regulators don’t overreact to problems.

“You’ve got to raise the issue because when you do nothing, something bad happens to you,” Scott rallied the crowd. He pointed out that a large percentage of the population is unbanked or underbanked and that we’ve got to make sure that people and small businesses have access to loans.

Attorney Tom Sullivan immediately followed Scott and introduced the Coalition for Responsible Business Finance (CRBF), an advocacy and education platform for those that provide alternative capital for small businesses. CRBF was created to educate state and federal policymakers, media, and communities on how technology and innovation are providing small businesses access to capital that is necessary for growth.

“Federal regulators and congress are interested in what you’re doing,” said Sullivan. “That could be a good thing or a bad thing.”

On a panel later in the day, Sullivan told attendees that a best practices framework can be used as a template for a law or guidance for regulators and that such a framework should be specific and not overgeneralize. Take the theoretical and apply it to an actual lending transaction, he said.

The general consensus at the conference was that an intelligent proactive approach with policymakers was the best course of action for the industry going forward. Congressman Scott communicated that while the federal government might have good intentions, it definitely helps if there’s a strong voice available to tell their side of an issue.

God bless America and God bless the online lenders.

Palladium Equity Partners Announces Investment in Fora Financial, a Provider of Working Capital Financing to Small- and Medium-Sized Businesses

October 14, 2015 Palladium Equity Partners, LLC (along with its affiliates, “Palladium”), a private investment firm with over $2.0 billion in assets under management, today announced that one of its affiliates has made a significant investment in partnership with the co-founders and management of Fora Financial LLC (together with its affiliates, “Fora Financial” or the “Company”), a technology-enabled provider of financing to small- and medium-sized businesses nationwide.

Palladium Equity Partners, LLC (along with its affiliates, “Palladium”), a private investment firm with over $2.0 billion in assets under management, today announced that one of its affiliates has made a significant investment in partnership with the co-founders and management of Fora Financial LLC (together with its affiliates, “Fora Financial” or the “Company”), a technology-enabled provider of financing to small- and medium-sized businesses nationwide.

Founded in 2008, Fora Financial offers loans and merchant cash advances of between $5,000 and $500,000 to small businesses throughout the country. Since inception, the Company has provided total funding of nearly $400 million to more than 8,000 businesses. It has experienced rapid growth and recently was ranked among the fastest-growing companies in America in the Inc. 5000 list. Fora Financial recently expanded its New York City offices to accommodate its growing roster of over 100 employees as it bolsters key capabilities in analytics and technology and aims to continue to execute on its strategy of delivering capital in a timely and cost effective way.

Fora Financial will continue to be led by its two founders, CEO Jared Feldman and President Dan Smith.

“We believe Fora Financial has developed a highly attractive credit offering and technology platform that have made it a valued provider of financing to thousands of small businesses seeking capital,” said Justin Green, a Principal of Palladium. “My partners and I look forward to supporting Jared, Dan and the Fora Financial management team to continue the strong growth trajectory of the Company, including through new partnerships, expanded product offerings and increased lending capabilities.”

Feldman said, “We are excited to partner with Palladium, a firm with extensive financial services expertise and many years of experience supporting founder-owned businesses.”

Smith added, “With this partnership in place, we are well-capitalized to continue offering the small business community the custom, innovative funding solutions that have enabled us to build this Company into a market leader.”

Terms of the investment were not disclosed. Fora Financial was advised by Raymond James & Associates.

About Fora Financial

Fora Financial offers flexible, working capital solutions to small businesses in need of financing to sustain or grow their enterprise. The Manhattan-based company places a high value on trust and transparency and provides businesses with quick, customized financial solutions utilizing its state-of-the-art technology platforms. Founded in June 2008, Fora Financial has more than 100 employees who have provided nearly $400 million to over 8,000 customers. For additional information, please visit www.forafinancial.com, call (855) 515-2413 or follow Fora Financial on Facebook at facebook.com/Fora.Financial.

About Palladium Equity Partners, LLC

Palladium is a middle market private equity firm with over $2.0 billion in assets under management. The firm seeks to acquire and grow companies in partnership with founders and experienced management teams by providing capital, strategic guidance and operational oversight. Since its founding in 1997, Palladium has invested over $1.5 billion of capital in more than 25 platform investments and over 50 add-on acquisitions. The firm focuses primarily on buyout equity investments in the range of $50 million to $150 million. The principals of the firm have significant experience in financial services, business services, food, healthcare, industrial and media businesses, with a special focus on companies they believe will benefit from the growth in the U.S. Hispanic population. Palladium is based in New York City. For more information, visit www.palladiumequity.com.

For media inquiries, please contact:

Todd Fogarty or Peter Hill of Kekst and Company

212-521-4800

todd-fogarty@kekst.com or peter-hill@kekst.com

Coalition for Responsible Business Finance Submitted RFI on Behalf of Both Funders and Small Businesses

October 1, 2015 If you haven’t heard of the Coalition for Responsible Business Finance (not to be confused with the Responsible Business Lending Coalition), I recommend paying attention to it.

If you haven’t heard of the Coalition for Responsible Business Finance (not to be confused with the Responsible Business Lending Coalition), I recommend paying attention to it.

“The CRBF is a group of businesses and service providers that advocate for the value of alternative financing opportunities for small businesses,” they said in their response to the Treasury RFI. “We created the coalition to help educate Congress, Treasury, and other federal departments and agencies on how technology and innovation are providing small businesses access to capital that is necessary for growth.” Simply put, this coalition allows lenders, funders, and small businesses to have a unified voice to educate policymakers.

And yes, merchant cash advance companies are welcome, though representation is very diverse.

“Small business owners value choice and speed when looking at alternative finance and lending options,” the CRBF says in their response. “Any federal approach needs to balance new regulatory requirements with the impact on the alternative finance and lending sector and on the sector’s small business customers.”

The overall message in the submission is that regulators need not feel shy about opening a dialogue with those most likely to be affected by any change in policy.

For those reasons, CRBF recommends that Treasury create an alternative finance and lending interagency working group that will meet on a quarterly basis. We suggest that twice a year the working group meet as a group comprised solely of governmental personnel, with officials from SEC, SBA, FTC, Federal Reserve, OCC, and other relevant agencies. And, we suggest that twice a year the working group meet with business leaders from across the alternative finance and business lending spectrum including representatives from lead generators, aggregators, merchant cash advance professionals, peer-to-peer lenders, risk analytics services, direct lenders, marketplace lenders, and others. Meeting with different groups of businesses throughout the life span of an interagency working group will allow Treasury to keep up with a rapidly evolving business sector and will help ensure that any federal approach is sensitive to its impact on the sector and on its small business customers.

CRBF is committed to educate federal authorities on how alternative lending and finance benefits small business and the economy. We would certainly help Treasury establish any working group that serves the same purpose.

As I am currently an advisory board member of this coalition, I encourage you to consider the organization’s mission and purpose by visiting the website at http://www.responsiblefinance.com. If you’d like to learn more or consider support for it, email me at sean@debanked.com.

Why OnDeck and CAN Capital Nailed Their Treasury RFI Responses

October 1, 2015 A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

Both CAN Capital and OnDeck accomplished that in their comprehensive responses to the Treasury RFI.

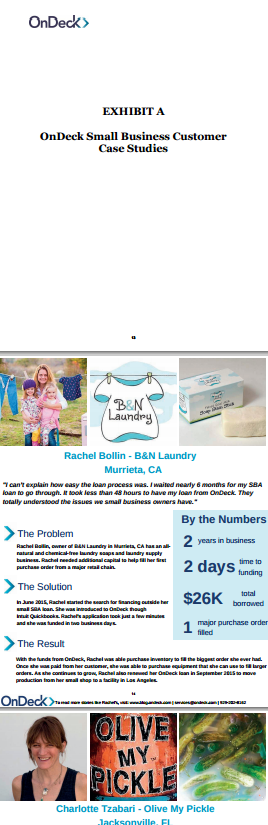

OnDeck went a step further and even attached case studies that included photographs of actual small business owners they’ve helped. They also put to bed the notion that their business model is unregulated:

At the federal level, we are regulated by the SEC and subject to US securities laws. We further satisfy applicable lending requirements under, among others, the Fair Credit Reporting Act, the Servicemembers Civil Relief Act, the Equal Credit Opportunity Act, and sanctions programs administered by the Office of Foreign Assets Control (OFAC).

They also clue us in to the size of the potential market they’re in. “It is estimated that there is $80-$120 billion in unmet demand for small business lines of credit,” they wrote.

Notably, they support the logic that a short term high APR loan can make more financial sense than a long term low APR loan. “With respect to loan cost, by matching a loan’s term with the estimated investment payback (or ROI) period, a small business can minimize total overall interest expense. For example, a loan used to purchase inventory can have a payback term that corresponds to the expected sale of the inventory — in this way, a borrower may pay less in total interest expense on a higher-rate, short-term loan than on a lower-rate, long-term loan (which may take weeks or months to procure).”

Meanwhile, CAN Capital explained just how time consuming the process can be for small business owners. “On average, a small business owner might spend over 30 hours applying for credit from a traditional lender and wait weeks or longer for the underwriting process to run its course and the funds to be disbursed, assuming the loan request is approve,” they wrote.

CAN’s response at time reads like an S-1 registration form (could there be a reason for that?). “Our approach to assessing the risk of small businesses and their ability to pay has been very effective, as manifested by our lifetime weighted average net write off rate of 7.2% over 17 years and more than $5.3 billion in funding transactions,” they say. “For returning customers that access capital through our platform more than once, we see an increase in their gross sales of approximately 7% on average between their first and last funding transaction.”

And if you don’t want your data sources to be questioned, the easy thing to do is cite governmental studies which both companies did often. “Traditional lenders are not serving the capital needs of small businesses. This is especially true when small businesses need $100,000 or less, which accounts for 90% of small business loans,” CAN wrote while citing a report published by the SBA’s Office of Advocacy.