Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

‘We Cannot Have Opaque Black Boxes Running Our Economy,’ Says Director of US PIRG

June 9, 2016

During a marketplace lending event hosted by the FTC, one panelist said he was not impressed by the reliance that some consumer lenders have on proprietary algorithms and secret sauces to determine who gets approved for a loan. Ed Mierzwinski, Consumer Program Director for U.S. PIRG, a nonprofit consumer interest group, expressed that regulators should investigate these methodologies. “We cannot have opaque black boxes running our economy,” he said. “That may be something that excites the investors” but credit fairness has to come first, he added.

Meanwhile, Jessica Milano, a Deputy Assistant Secretary for the U.S. Treasury, explained that underwriting methodologies used by consumer marketplace lenders still produce results that are highly correlated with FICO. The Treasury published a much-talked-about report on marketplace lending just last month.

Peter Renton, who founded the LendAcademy blog and LendIt conference, countered Mierzwinski by explaining that alternative data sources are not so much about assessing credit-worthiness, but rather about verifying the identity of the applicant.

Milano and Renton both conceded that things were different on the business lending side of the industry.

This was an educational event, not an inquiry or hearing so nobody was officially being scrutinized. FTC Commissioner Edith Ramirez said in her introductory speech that “most observers agree that, given the advantages it offers both lenders and borrowers, marketplace lending is here to stay.”

You can watch a recap of the 3-hour event below. It starts at about 1 hour in to the recording.

Community Banks Worried That Marketplace Lenders Have Regulatory Advantage

June 8, 2016 Community banks have been slow to adopt services offered by marketplace lenders “out of fear of undue scrutiny by their prudential bank regulators,” wrote the Independent Community Bankers of America (ICBA) in a letter to the OCC last week. The banks would or could be more proactive in offering small loans in rapid fashion, if the regulators give “community banks the flexibility to lead the path,” they said.

Community banks have been slow to adopt services offered by marketplace lenders “out of fear of undue scrutiny by their prudential bank regulators,” wrote the Independent Community Bankers of America (ICBA) in a letter to the OCC last week. The banks would or could be more proactive in offering small loans in rapid fashion, if the regulators give “community banks the flexibility to lead the path,” they said.

One issue they raised was the consideration of a limited purpose federal bank charter, which, if implemented, would reduce the need for marketplace lenders to partner with chartered banks or eliminate the need for marketplace lenders to subject themselves to the maze of 50-state compliance. The ICBA, according to the letter, is all for this since it would subject marketplace lenders to federal oversight, but they fear it would not go far enough to truly level the playing field.

“For instance, if such a charter did not have authority to take deposits, the charter may be subject only to a compliance supervision and examination. ICBA believes that the recent problems that some of the online marketplace lenders have experienced with liquidity and earnings, as well as with compliance, makes it important that these lenders be subject to safety and soundness supervision and regulation.”

Their fear is that a limited charter would give marketplace lenders all the benefits but with less oversight than them, and that’s not fair. Not mentioned however is that marketplace lenders are for the most part regulated, albeit not in the exact same manner as banks. Another of the ICBA’s stated concerns is that marketplace lenders are exempt from safety and soundness oversight and thus their stability and liquidity is not being monitored.

“These companies have not experienced a serious economic downturn yet and already they have been subject to serious funding and capital issues,” they wrote.

While true, consumer deposits are not at risk since they don’t take them. And given the industry’s size at present, the potential danger to the economy should one or some fail, is relatively minor.

Midland Funding Gets Mentioned in John Oliver’s HBO Show

June 6, 2016The infamous Midland Funding you might know from the Madden v Midland case, was mentioned on John Oliver’s Last Week Tonight and not in the best context. Midland is a subsidiary of Encore Capital Group, the largest publicly traded debt buyer in the United States and the episode was about the not-always-peachy world of debt buying and debt collection.

Oliver referenced Midland just to provide background on an industry as a whole, not to imply that they were involved in anything negative.

More background was added by Jake Halpern, the author of Bad Paper: Chasing Debt from Wall Street to the Underworld, who explained that the sale of debt from one party to another is not always done using the most sophisticated means, with it often being simply a list of fields on an Excel spreadsheet.

Oliver, who took his research to the extreme, actually set up his own debt collection company in Mississippi and purchased $15 million worth of debt that was aged beyond the statutory collections period for the bargain price of $60,000. Rather than try to collect on the debt, which he mentioned would not have been illegal, he decided to forgive the debt entirely and set the record for TV’s largest monetary giveaway in the process.

Oliver was careful to remind viewers throughout that while there are a few bad seeds and horror stories, the industry itself is regulated and is not illegal. You can watch the episode below:

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

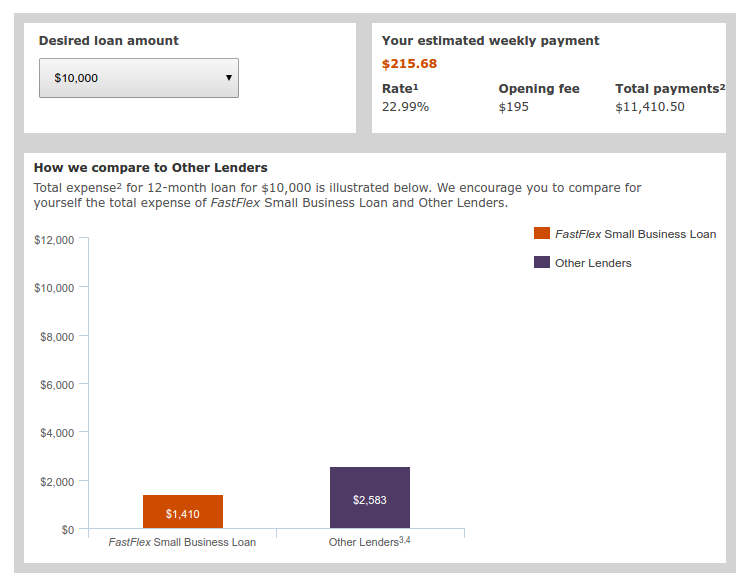

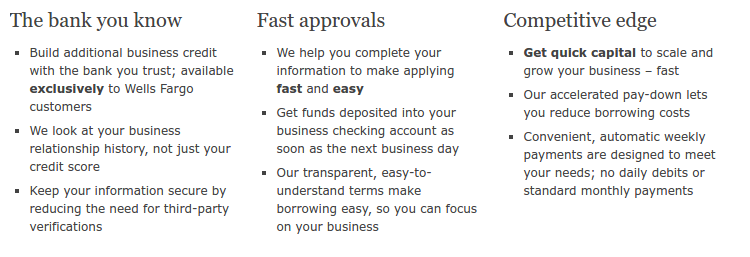

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

1,334 Page CFPB Loan Rule Proposal Warns Business Lenders

June 2, 2016 Congress isn’t responsible for lending lawmaking anymore it seems, the CFPB is. That’s a bit chilling considering the federal agency is also tasked with enforcing the laws it creates. A new 1,334 page law proposal published by Richard Cordray at the CFPB to assert control over payday loans, vehicle title loans, and certain high-cost installment loans also mentions business loans in it.

Congress isn’t responsible for lending lawmaking anymore it seems, the CFPB is. That’s a bit chilling considering the federal agency is also tasked with enforcing the laws it creates. A new 1,334 page law proposal published by Richard Cordray at the CFPB to assert control over payday loans, vehicle title loans, and certain high-cost installment loans also mentions business loans in it.

“The Bureau intends to exclude loans that are made primarily for a business, commercial, or agricultural purpose,” the proposal states. However, since the proposal is not a bill that would be brought before Congress for a vote, the weakly and seemingly intentionally phrased statement of “intends to exclude” is not the most reassuring language. Cordray concedes in an earlier paragraph though that Dodd-Frank only empowered the Bureau to prescribe rules over consumer finance, which was defined primarily as personal, family, or household purposes.

Already the proposal explains how a business lender might violate that threshold:

“A lender would violate this part if it extended a loan ostensibly for a business purpose and failed to comply with the requirements of this part if the loan in fact is primarily for personal, family, or household purposes. See the section-by-section analysis of proposed § 1041.19 for further discussion of evasion issues.”

That referenced further analysis basically says that if the lender is really just pretending a personal loan is a business loan, then they’re just trying to evade the rules and that won’t work.

If a consumer claims they’re going to use the money for a personal purpose but then decides to use it to finance a small business, well then it’s still a consumer loan, Cordray argues:

“Proposed § 1041.3(b) specifies that the proposed rule would apply only to loans that are extended to consumers primarily for personal, family, or household purposes. Loans that are made primarily for a business, commercial, or agricultural purpose would not be subject to this part. The Bureau recognizes that some covered loans may be used in part or in whole to finance small businesses, both with and without the knowledge of the lender. The Bureau also recognizes that the proposed rules will impact the ability of some small entities to access business credit themselves. In developing the proposed rule, the Bureau has considered alternatives and believes that none of those alternatives considered would achieve the statutory objectives while minimizing the cost of credit for small entities.”

Business lenders and even merchant cash advance companies should make sure they ask every applicant what the intended use of the funds are. If it’s for a personal purpose, the CFPB could try to exercise jurisdiction in the future.

Individual Investors Heart of Lending Club, CEO Says

June 1, 2016 Lending Club CEO Scott Sanborn sent out an email late Wednesday night to individual investors to remind them that they are “emphatically” the heart of their marketplace.

Lending Club CEO Scott Sanborn sent out an email late Wednesday night to individual investors to remind them that they are “emphatically” the heart of their marketplace.

“Our individual investor base is over 150,000 members strong,” the email says, but it was unclear if this is the amount of active investors or all investors that have participated since they launched in 2007.

Lending Club is doubling down on efforts to serve individual investors, Sanborn wrote, by staffing up on their investor services team and dedicating more engineering resources to improve the investment experience.

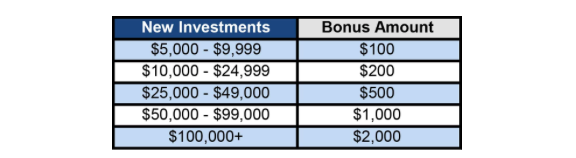

To prove this commitment, they’re offering investors that deposit new money and fully invest it by August 15th a matching bonus of 1% to 2% of the investment amount. The bonus can’t be withdrawn and they say you might have to pay taxes on it in the fine print.

Not mentioned in the email is the consideration of a Bankruptcy Remote Vehicle (BRV) to protect note investors from the underlying credit risk of Lending Club itself, something that many individual investors have been asking the company for. Lending Club rival Prosper instituted a BRV in 2012.

The question now is, will a potentially taxable small bonus that can’t be withdrawn be enticing enough to convince retail investors to double down on their commitment to Lending Club?

Discover Wants to Steal Lending Club Customers

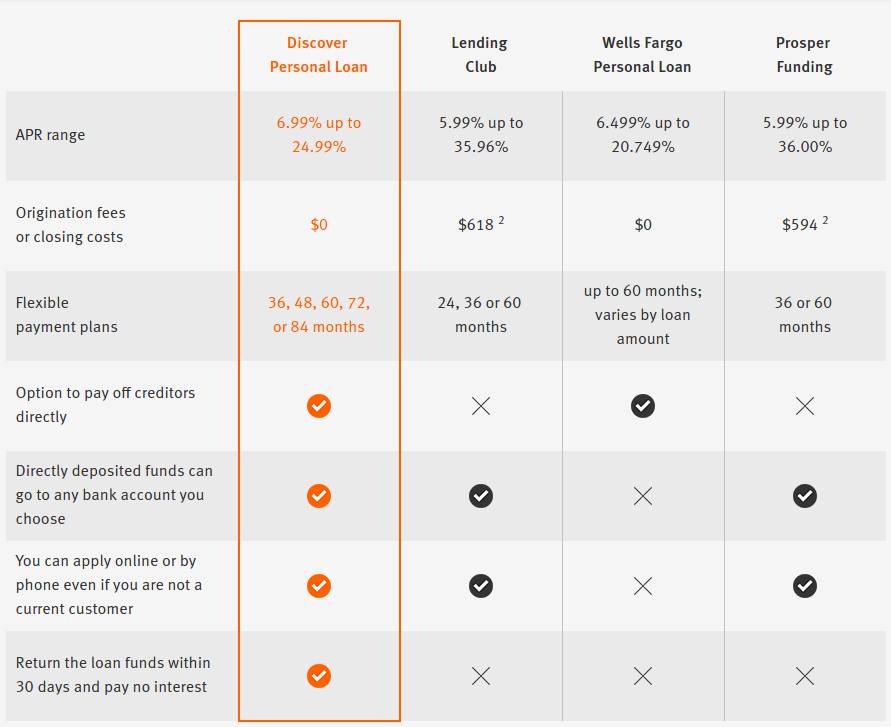

May 31, 2016Discover used to demonstrate to potential borrowers how their personal loans stacked up next to loans offered by Wells Fargo. But with Lending Club, another rival, showing weakness lately, the columns on their personal loan comparison page have been rearranged to put themselves directly next to Lending Club.

Prosper Marketplace, as shown above, has been part of this comparison chart for quite some time as well. Personal loans from Citi also used to be listed, but they were removed as a competitor last summer. Discover, according to this, seems to show that their loan program offers many advantages over Lending Club.

Both companies market heavily using direct mail and that probably won’t change any time soon. 96% of Discover personal loan borrowers have FICO scores above 660. Meanwhile Lending Club’s minimum required FICO score is technically 640. Both are going after the same type of borrower.

Discover only originated $3 billion in personal loans (which is separate from its credit card business) in 2015 while Lending Club originated $8.3 billion.

Lending Club has at least two weaknesses at the moment, one being that approved loans on the platform could go unfunded if there are too few investors, a problem they’re facing right now. The other is that their relationship with a bank to make their entire business model work is under fire. Discover on the other hand is already a bank and doesn’t have to worry.

Lending Club’s stock price jumped late last week on news that Citigroup might buy the loans that the company originates. The bind Lending Club finds itself in makes a potential Citi deal look like a rescue bailout. If the company cannot find buyers for its loans however, it could indeed be in jeopardy, an issue that has been raised by observers for some time.

It cannot be understated that in Discover’s 2015 earnings report, they championed the originate-to-hold approach. “We believe our brand, disciplined underwriting and ‘originate to hold’ model will continue to allow us to compete very effectively,” they wrote.

Madden v Midland Has Already Hurt Riskier Borrowers, Study Finds

May 28, 2016 If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

Since the Second Circuit’s decision only affected borrowers in New York, Vermont and Connecticut, researchers were able to monitor behavioral changes there against other states. They used data from three of the nation’s top marketplace lenders.

In the Second Circuit’s jurisdiction, approved borrowers showed a significant increase in annual incomes, years of employment and FICO scores compared to other districts. Specifically, growth was concentrated among borrowers with FICO scores over 700. Approvals for borrowers with scores below 644 “virtually disappeared” while literally zero loans were issued to borrowers with FICO scores below 625.

“Madden’s effect on loan volume grows as the borrower’s FICO score falls,” the data reveals.

But even though lenders became afraid of the usurious implications in these states, borrowers did not take the Madden decision as a signal to stop payment. “[We] are unable to find any evidence of strategic delinquencies,” researchers concluded after a series of tests.

We find, consistent with basic economic theory, that the sudden enforceability of usury laws had the greatest impact on higher-risk borrowers. In a market where consumer loans are generally increasing in volume, the Madden decision disproportionately affected loan volume for borrowers with the lowest FICO scores.

Read the full study titled, The Effects of Usury Laws on Higher-Risk Borrowers