Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Get $10 Worth of Bitcoin FREE

November 28, 2017 Ok, so this is a shameless affiliate marketing offer. If you buy $100 worth of Bitcoin from Coinbase using this link, you’ll not only get an extra $10 worth of Bitcoin free, but I’ll get $10 worth of free Bitcoins as well.

Ok, so this is a shameless affiliate marketing offer. If you buy $100 worth of Bitcoin from Coinbase using this link, you’ll not only get an extra $10 worth of Bitcoin free, but I’ll get $10 worth of free Bitcoins as well.

While it’s awesome that a single Bitcoin is worth $10,000 these days, I personally fell in love with the utility of the currency 3 years ago. I mined it, bought it, sold it, became a node on the network, donated it, spent it, accepted it as payment, went to meetups dedicated to it, and read books on it. The ironic part about it all is that few, if any, people cared about my coverage of it. Now that’s it up nearly 900% YTD, readers have been asking about it.

Before you get get caught up in the hype aspect, maybe take a minute to read through some of my very old blog posts about Bitcoin and decide for yourself if the currency makes sense.

- 12/3/14 – My Satoshi Monday – My trip to the Bitcoin Center

- 12/8/14 – How to Use Bitcoin – I bought a computer monitor on Overstock with Bitcoin

- 12/18/14 – Confessions of a Bitcoin Miner – My tale of mining Bitcoins

- 3/10/15 – deBanked Inks Deal With Lenders Marketing in Bitcoin – deBanked priced an advertising deal in Bitcoins

- 4/20/15 – Rand Paul Speaks at Bitcoin Event – A forward thinking Senator latched on to Bitcoin years ago

ISO Roadmap For 2018

November 26, 2017ISOs, as you finish out a wild year of funding, we’ve put together a roadmap to prepare you for a very successful 2018!

1. Educate yourself. Litigation in the MCA industry skyrocketed in 2017. That means as a salesperson you’re  more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

2. Source your own leads. Sneaking deals out the backdoor or being on the receiving end of ill-gotten leads may yield a couple bucks but it may ultimately come at the expense of your reputation and career. It could also be against the law. The surefire way to become a legitimate top performer in the industry is to generate your own deals. How else do you expect to build a book of business that’s truly yours and relationships with clients that are built on trust and integrity? Need help getting started? Check out this list of lead sources!

3. Participate in industry events. In 2018, it will pay to truly  know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

4. Keep up on the news. Keep up on  developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

5. Choose your partners wisely. In the same way that it’s probably not a good idea to send your deal off to a random funder that cold called you, using old-fashioned methods like Google to discover who’s who can be onerous. That’s why we’ve segmented our sponsor directory by business type so that you can narrow down the right partner to fit your needs fast. While it’s true that these companies pay to advertise here, it’s an excellent starting point. So check out our list of sponsors!

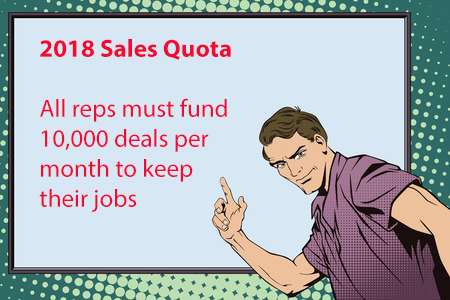

Take a Break From Funding This Thanksgiving

November 21, 2017This Thanksgiving…

Step back from the daily grind

Those merchants eager for your cold calls can wait

There’s no need to start worrying about next year just yet

It’s Thanksgiving

So hug an underwriter

Kiss a broker

Think about your favorite merchant

And pay no attention to the algorithms automating your job

Give thanks

Because nobody wants to hear you recap your holiday like this

Or this

Or this

Enjoy the Holiday!

You should also check out our 2016 Thanksgiving Day post and 2012 Thanksgiving Day post.

Good Riddance F and G Notes on Lending Club

November 9, 2017 When Lending Club announced they were discontinuing F and G grade notes on their platform for investors, I wasn’t surprised. Investors in general have been reporting disappointing returns, even dipping into negative territory some months. My own portfolio there is on track to generate a loss for 2017, which seems even worse when I consider that those funds could’ve returned nearly 15% in an S&P 500 index fund or more than 600% in bitcoin. Granted, only a small portion of my investable assets were tied up in Lending Club so it’s not all bad.

When Lending Club announced they were discontinuing F and G grade notes on their platform for investors, I wasn’t surprised. Investors in general have been reporting disappointing returns, even dipping into negative territory some months. My own portfolio there is on track to generate a loss for 2017, which seems even worse when I consider that those funds could’ve returned nearly 15% in an S&P 500 index fund or more than 600% in bitcoin. Granted, only a small portion of my investable assets were tied up in Lending Club so it’s not all bad.

Out of the 3,262 notes I purchased on Lending Club, only 99 were F-grade and 53 were G-grade. They didn’t do so well in retrospect, echoing Lending Club’s findings.

27 of my G notes have already been charged off. 17 have been paid off, with the rest still outstanding. A charge-off rate over 50% is not so good on its own, but the data is worse because the interest earned on the performing ones was not enough to offset the charge-offs. Even if all of the remaining notes perform, it is no longer possible to earn a positive return on G notes. The amount I loaned exceeds the total dollars returned. The end result of a category that investors heralded as high-risk, high-return is a big fat loss.

31 of my 99 F notes have already been charged off. Only 26 remain outstanding, 4 of which are delinquent. The rest have been paid off. At this time, the amount I loaned exceeds the total dollars returned. It is still mathematically possible to break even if the remaining loans do not default, but we’ll see. Suffice to say, these were a bad investment.

I have been winding down my portfolio since May 2016. RIP F and G notes.

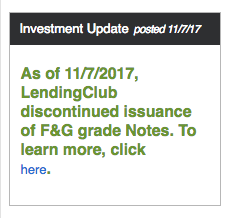

Lending Club is Discontinuing F and G Grade Notes

November 7, 2017 Per Lending Club’s website, the company is discontinuing issuance of F & G grade notes.

Per Lending Club’s website, the company is discontinuing issuance of F & G grade notes.

According to an announcement published by the company:

We are consistently assessing the value our product delivers to our investors, and have noticed an increase in prepayment and delinquency rate in F and G grade Notes. We feel it is in the best interest of our investors to remove F and G grade Notes while we test new capabilities and refinements to the underwriting and pricing criteria and determine how to best offer a better experience for both borrowers and investors in the F and G segment.

Peers invested in previously-issued F & G grade notes will still receive their payments until maturity.

Performance played a role in their decision.

Every quarter, we review product performance. During our third quarter 2017 forward-looking analysis, we saw increases in delinquency and prepayment rates in F and G grade loans. This update allows us the opportunity to re-assess how we can best deliver value to our investors through the platform.

More information about this change can be found here.

Lending Club also published their Q3 earnings Tuesday afternoon. The company loaned $2.44B for the quarter and hit a record $154 million in revenue. The company still eeked out a $6.7 million loss, but that’s down from $19 million over the same period last year.

Dependence on retail investors or “peers” declined again. Only 10% of loan funding was sourced from the self-managed individuals category in Q3 or $249 million of the $2.44 billion funded.

Lending Club funded 9% of their own originations in the quarter or $217 million.

Catching Up With LendingPoint

November 6, 2017 At Money2020, we sat down with Chief Executive Officer Tom Burnside and Chief Strategy Officer Juan Tavares, both of LendingPoint, an online consumer lender we examined in the July/August magazine issue. Not mentioned in that story is Tavares’ background at Avanzame Latin America, a merchant cash advance company based in the Dominican Republic. Burnside, however, originally started on the consumer side at First Data, before working for 13 years at CAN Capital, until he left and launched LendingPoint.

At Money2020, we sat down with Chief Executive Officer Tom Burnside and Chief Strategy Officer Juan Tavares, both of LendingPoint, an online consumer lender we examined in the July/August magazine issue. Not mentioned in that story is Tavares’ background at Avanzame Latin America, a merchant cash advance company based in the Dominican Republic. Burnside, however, originally started on the consumer side at First Data, before working for 13 years at CAN Capital, until he left and launched LendingPoint.

The lender focuses on near prime consumers and has even trademarked the word “NEARPRIME.” Their algorithm, which processes data from dozens of APIs in 5 seconds, handles the heavy lifting, the secret sauce of which they could not disclose. “You could use 3,000 attributes but maybe actually 57 attributes could become your core,” Tavares says. Their “credit-first” mentality has allowed the company to build a healthy performing portfolio. And “credit-first” doesn’t necessarily mean FICO scores, Burnside says, it’s about “predictives” to price accordingly for the risk you take. “How you run [the variables] together, that’s the magic,” they say together.

An interesting initiative that they’re now just ramping up, Tavares says, is partnerships with hospitals that allow patients to determine their deductible expenses and obtain credit on the spot to pay for it. Fitting into their “point of need” strategy, Tavares say “We’re at the intersection between credit and payments.”

Burnside says that LendingPoint was on par to finish with $28 million in funded loans for the month of October. “Demand is not the problem,” Tavares interjects. “We’re tempering growth to make sure that we grow wisely.”

And the market to expand that growth is big despite the numerous tech companies competing in the lending space. Burnside reports the company receiving $2.5 billion worth of loan applications in September alone. 60% of their applications come in through mobile devices. Peak application hours are lunch time and late at night, sometimes as late as 1 or 2 in the morning, they say. The entire loan application process can be done on mobile without them ever having to talk to anyone. Tavares qualifies that by saying that doesn’t mean that they take shortcuts.

As to whether an IPO could be in the works, Burnside deflects and says, “we’re busy building something special right now. We’ll see what happens.”

“What I will tell you is, is that investor confidence is up,” Tavares says.

FundKite Event at the Jets/Bills Game Had a Big Turnout

November 3, 2017About 100 people attended the FundKite event at the Jets/Bills Thursday night game in The Meadowlands including several dozen ISOs. In addition to premium seating and sideline access through the 50 Club, a select group got to stand on the field during the national anthem. Below is a handful of snaps I took at the game:

LendUp May Have a Leg-up

November 1, 2017

deBanked recently sat down with LendUp CEO Sasha Orloff and COO Vijesh Iyer at an auspicious time. The company, an online lender that provides consumers with alternatives to payday loans and credit cards, is uniquely positioned in the wake of the CFPB’s 1600+ page Payday loan rule that was issued in early October.

And that’s not exactly an accident. Orloff says the company was founded (5 years ago) with the expectation that the CFPB would issue an eventual rule. “At the time, we had no idea what it was going to be but I could imagine that if they were going to write a federal rule that it would completely change the industry,” he said.

Orloff’s journey, as he tells it, began by reading Banker to the Poor, which inspired him to move to rural Honduras nearly 15 years ago to help the Grameen Foundation, a non-profit that focuses on providing loans and education to the poorest of communities. He was only 21 at the time. After a three-year tour, he moved on to roles at The World Bank, Citi, and finally starting in 2012, LendUp.

When LendUp was being envisioned, he explains, the smart phone was making it possible for consumers to access financial services outside of what was in their neighborhood and bank technology was the last thing that was going to become modernized.

“The CFPB rule was going to make it harder for banks to work with underserved consumers,” he says. “So we said let’s start a financial services company that focuses exclusively on the people that have the least amount of options and let’s start reinventing [these] products one at a time.”

And with that, they consulted academics, educators, government officials, and people from the industry. “How do you give somebody credit in an emergency fashion that can change it from a trap into an opportunity? And so we did that and it turned out the rule looked really similar to what we did,” he explains.

“I think there’s a lot of things they got right [about the CFPB rule],” he says in regards to how to eliminate debt traps. LendUp, for example, doesn’t allow customers to roll over their loans, they have to pay off their loans in full before they can consider borrowing again. Rollovers were a big sticking point for the CFPB when they published their rule last month. Their official announcement on the matter had stated that “many borrowers end up repeatedly rolling over or refinancing their [payday] loans, each time racking up expensive new charges. More than four out of five payday loans are re-borrowed within a month, usually right when the loan is due or shortly thereafter. And nearly one-in-four initial payday loans are re-borrowed nine times or more, with the borrower paying far more in fees than they received in credit.”

One piece of the payday alternative puzzle is in the underwriting. COO Vijesh Iyer, an alumni of both Capital One and PayPal, says “we basically use a variety of data sources, both the traditional bureaus and as what we call the non-traditional bureaus.” For the credit card product, LendUp will pull credit from a traditional bureau. “For the small dollar loan product we use non-traditional CRAs,” he says. Their team of data scientists tries to extract the most significant signals out of all of the data sources they have at their disposal. “That’s really valuable when you’re dealing with a subprime customer where the reason why someone could be underserved or subprime is very different. We all have different life stories and we’re really trying to figure out the differences which we get from multiple signals, multiple data sources.”

“The easiest person to convince that we’re a better product is an existing payday user,” Orloff says. “because it’s slightly cheaper at the beginning, it gets much cheaper over time. It has a lot more flexibility. It gives people for the first time the opportunity to report to the credit bureaus. It teaches you better financial behavior. You can do it on a mobile phone. You can get alerts and reminders…”

Meanwhile, payday borrowers always have to pay the same amount, Orloff contends. The loan terms don’t improve, he says. One notable advantage a LendUp borrower might experience is that when they first run into trouble with making a LendUp loan payment, they can get a few extra days leeway at no extra charge, which usually comes as a welcome surprise.

Granted, a LendUp loan’s APR can still look pretty steep. A calculator on their website offers an example of one that is 458.86% APR. Orloff says a part of understanding that is understanding what a consumer’s options are and what the costs to process the applications are. A 220% APR might only equate to something like $30 total in fees depending on what the loan terms are, he explains. Their borrowers don’t get paid in APR though he says, they get paid in dollars. “They care about what’s the total cost of credit in terms of dollars.”

“Our customers pay more than that on overdraft fees,” Iyer adds. “Every time they have a slight overdraft, even if it’s for a dollar, even if it’s 10 cents. Even if it’s two dollars. No one ever tries to evaluate what the APR for that is. But that is their fee and this is also a fee.”

But more than anything else, it’s about whether the borrower’s and lender’s interests are aligned, Iyers contends. Right now, LendUp believes they’re doing the right thing at the right time.

—

This interview was conducted at Money2020 in Las Vegas