Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

SBFA Braved Snow Storm for Spring Fly-In

March 23, 2018 The Small Business Finance Association (SBFA) had their Washington DC Spring fly-in earlier this week. SBFA members met with Karen Kerrigan, the President and CEO of the Small Business & Entrepreneurship Council, on Tuesday afternoon, and Congressman Josh Gottheimer (D-NJ) in the evening.

The Small Business Finance Association (SBFA) had their Washington DC Spring fly-in earlier this week. SBFA members met with Karen Kerrigan, the President and CEO of the Small Business & Entrepreneurship Council, on Tuesday afternoon, and Congressman Josh Gottheimer (D-NJ) in the evening.

Despite the blizzard, a handful of members continued to meet with members of Congress on the Hill on Wednesday.

Founded ten years ago, The SBFA is a non-profit advocacy organization dedicated to ensuring Main Street small businesses have access to the capital they need to grow and strengthen the economy.

It’s Settled, Merchant Cash Advance Not Usurious

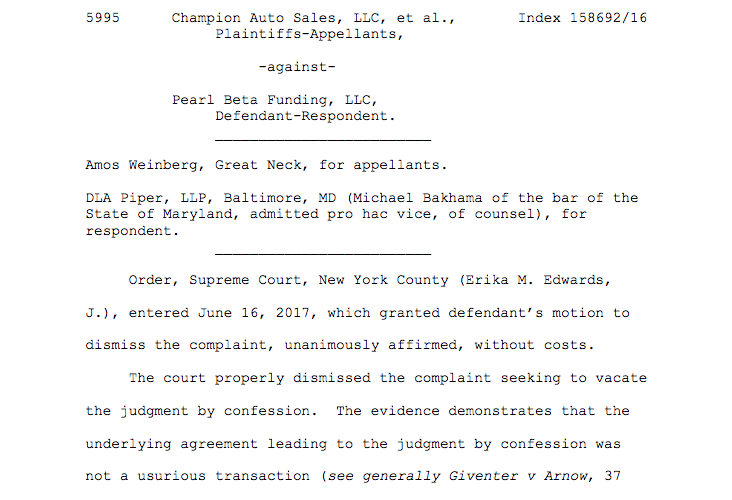

March 15, 2018 It’s not a usurious transaction. That’s how trial courts across New York State have been ruling on merchant cash advances for years, but now, thanks to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, the matter has been settled in a key jurisdiction.

It’s not a usurious transaction. That’s how trial courts across New York State have been ruling on merchant cash advances for years, but now, thanks to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, the matter has been settled in a key jurisdiction.

On Thursday, March 15th, The Appellate Division of The First Department published their unanimous decision that the underlying Purchase And Sale of Future Receivables agreement between the parties was not usurious.

In October 2016, the plaintiffs sued defendant Pearl in the New York Supreme Court alleging that the Confession of Judgment filed against them should be vacated because the underlying agreement was criminally usurious. As support, plaintiffs argued that the interest rate of the transaction was 43%, far above New York State’s legal limit of 25%.

The defendant denied it and moved to dismiss, wherein the judge concurred that the documentary evidence utterly refuted plaintiffs’ allegations.

With the case over, plaintiffs appealed the decision. Their major loss is spelled out below:

The decision is an interesting chapter in the story of Amos Weinberg, the attorney who represented the plaintiffs in this case. Prior to the appeal, he managed to file more than 100 lawsuits against merchant cash advance companies for usury. He has had very little success on the merits. Last May, deBanked reported that a judge in another lawsuit had admonished Weinberg for misleading the court over the actual wording of what a contract said.

Now he’s responsible for one of the biggest legal decisions in merchant cash advance history. And not in his favor.

The matter arose out of Index # 158692/2016 in the New York Supreme Court.

9 Real Industry Stories To Get You Fired Up

March 7, 2018 Whether you’re working from home as an independent agent or you’re the owner of a young alternative funding startup, here are nine deBanked stories that are guaranteed to inspire. For those of you that haven’t been in the industry very long, you’ll definitely want to read some of the older ones!

Whether you’re working from home as an independent agent or you’re the owner of a young alternative funding startup, here are nine deBanked stories that are guaranteed to inspire. For those of you that haven’t been in the industry very long, you’ll definitely want to read some of the older ones!

Nest Planner: The Story Of A Startup MCA Broker | 3/4/18

Hard Work, Big Success – The True Story of an MCA Broker | 12/15/17

A True Rapid Advance For Mark Cerminaro | 12/16/16

Can an ISO “Excel” in 2016? | 8/26/16

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True? | 4/28/16

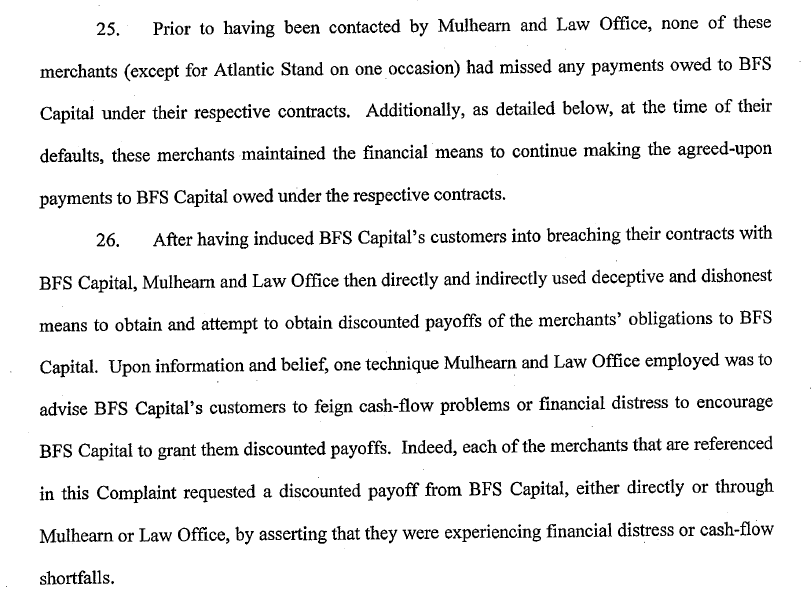

The Dual Aura of Fora – How Two College Friends Built Fora Financial and Became the “Marketplace” of Marketplace Lending | 2/16/16

The Closer – Meet the Yellowstone Capital Rep That Originated $47 Million in Deals Last Year | 2/10/16

Meet the Source: How Jared Weitz and United Capital Source became one of the industry’s fastest growing shops | 10/23/15

From Lowes to Loans: Meet William Ramos | 4/12/15

Ready to network with your industry peers in person? Register For Broker Fair! coming on May 14 in Brooklyn, NY.

I Got Funded, Again

March 1, 2018 One year after I received a 12-month loan from Square on fixed monthly ACH, I logged onto my dashboard to renew. I was pre-approved to do it all over again, the screen indicated, but the monthly ACH payment option had disappeared. In its place, Square offered to withhold a fixed percentage of my credit card sales going forward until the balance was paid in full.

One year after I received a 12-month loan from Square on fixed monthly ACH, I logged onto my dashboard to renew. I was pre-approved to do it all over again, the screen indicated, but the monthly ACH payment option had disappeared. In its place, Square offered to withhold a fixed percentage of my credit card sales going forward until the balance was paid in full.

Known as a “split,” diverting a percentage of the card payment proceeds to a financial company is straight out of the merchant cash advance playbook. Square, however, structures their transactions as loans. That means that regardless of how my sales ebb and flow, I must pay off my balance in full in 18 months.

I was okay with that. I had to be. It was that time of year when working capital is very important, the holidays. Not to mention, deBanked was in the process of moving, again. If you recall in December of 2016, we moved to a slightly larger office in the same building on Wall Street. In December of 2017, however, we moved from Manhattan to Brooklyn, a process that was a little more involved.

But this loan had no monthly payment, just a 15.75% split. Others may refer to this as the holdback, withhold, or specified percentage. Square’s application process this time around was slightly more rigorous than a year ago, a few more buttons, a couple more disclosures, and even a notice that a review could take between 1-3 days. I was still approved the same day, however, and had funds the next. There were no hidden fees or closing costs.

Six days after being funded, I ran a charge, Square took their split, and I netted the different minus the interchange fees. I noticed, but in a way I didn’t. I didn’t have to worry about how much the monthly payment would be and when. The loan was being repaid all by itself. That was how I processed it psychologically anyway, as I imagine many other small business owners have as well.

And the feeling of relief from impending monthly payments is not entirely mental. Seven weeks later, I was already 17% paid off. That’s real progress, especially with a 65-week window remaining to pay off in full.

Had the same transaction been structured as a merchant cash advance, the timeframe would’ve been unlimited. But hey, I guess sometimes you can’t have it all. It was a 1.10 factor rate, decent by industry standards, certainly not the most expensive, but not the least expensive either. It was fast, it was helpful, and best of all, it was free from the burden of fixed monthly payments.

I got funded again and loved it. What are you still waiting for?

Editors Note: deBanked did not collaborate with Square in the writing of this editorial. Square did not even contact us after I published my first experience with their product one year ago. It is unclear if they are even aware that I wrote anything at all. Square is not an advertiser nor have they sponsored any of our events. I did not attempt to interview them for this write-up or tip them off that I would be writing anything. To my knowledge, we did not receive any special benefit or pricing. deBanked chose Square for funding in part to avoid the conflict of writing a review about a paying advertiser or sponsor.

BFS Capital Secures $175M Revolving Line

February 20, 2018

BFS Capital has secured a new $175 million revolving credit facility from funds managed by Ares Management, L.P. (NYSE:ARES), according to a company announcement. Stephens Inc. acted as financial advisor to the transaction.

ARES is one of the largest global alternative asset managers with $106.4 billion under management. They previously announced a $100 million line for LendingPoint, an online consumer lender.

BFS Capital also recently announced that 2017 was their biggest year yet. They generated more than $300 million in originations for the year.

BFS Capital plans to use the new facility to accelerate the growth of its lending business.

“The market continues to appreciate our small business customer focus,” said BFS Capital CEO Michael Marrache in a prepared statement. “Our strategic partners, such as ISOs, also commend us for our data and underwriting expertise—based on 15 years of financings across multiple economic cycles—which enables us to better anticipate the future performance of our financings.”

Law Firm Sued for Tortious Interference With Loans and MCAs

January 31, 2018Rhode Island Superior Court has a tortious interference case on its hands. Small Business Term Loans, Inc., and BFS West, Inc. v Christopher M. Mulhearn, and Law Office of Christopher M. Mulhearn, Inc. is yet another front in the debt settlement war enveloping the alternative finance industry.

Here, the plaintiffs (known to many as BFS Capital), allege that Mulhearn and his law office attempt to persuade BFS Capital’s customers to breach their obligations to BFS Capital while routinely making misleading representations to their customers, including by promising to save them money by settling their obligations to BFS Capital for a discounted amount when they have no legitimate basis for being able to make such promises.

At least seven customers are alleged to have breached their agreements as a result of the defendants’ actions.

The defendants have not yet responded to the complaint. The suit is registered in Providence/Bristol County Superior Court of Rhode Island under case # PC-2018-0094.

Other such companies that have found themselves on the receiving end of a tortious interference lawsuit include MCA Helpline, Protection Legal Group, and Creditors Relief.

deBanked Connect – Miami (Recap)

January 30, 2018Thank you to everyone who attended our cocktail networking event in South Beach last week. It was a great opportunity for funders, lenders, brokers and others in the industry to connect with each other (many for the first time ever). Thank you again to Everest Business Funding, National Funding, Knight Capital Funding, NISO, Grand Capital Funding, and Venture Credit Solutions for sponsoring.

Below is a sample of our photos from the evening. If you attach any of your own on social media, please use #debankedconnect so that we can find them.

READY FOR AN EVEN BIGGER & MORE COMPREHENSIVE DEBANKED INDUSTRY EVENT?

BROKER FAIR IS COMING MAY 14, 2018

TO BROOKLYN, NY

JOIN FUNDERS, LENDERS AND BROKERS FOR THE INAUGURAL CONFERENCE

LEARN MORE HERE

CHECK OUT THE BIG NAMES SPONSORING BROKER FAIR 2018

Attorney Suing Dozens of MCA Companies Disqualified as Counsel

January 29, 2018Rayminh Ngo, an attorney with Higbee & Associates that has appeared in no less than 80 lawsuits against merchant cash advance companies in New York State, hit a fatal roadblock in one case, court records reveal. That’s because Ngo and Higbee aren’t qualified to practice law in the State of New York. This disturbing matter was brought to light and evaluated by the Honorable Jerome C Murphy, a judge in Nassau County, late last month.

Platinum Rapid Funding Group, the plaintiff against a party that Ngo was representing, argued that the defendant’s attorney was in violation of Judiciary law §470, specifically that Ngo and the law firm did not have an office in New York State and consequently could not represent a client in New York.

Ngo denied the assertion and argued that he did in fact have offices there. But the evidence was not on his side. The two addresses he provided turned up empty, according to process servers who visited both locations. And the lease agreements submitted as exhibits were not valid for the time period in question.

“In the end, this Court finds that there is no evidence on this record that Ngo and Higbee had physical addresses in New York,” the order on the matter read. Ngo and Higbee were therefore disqualified as counsel of record. They have filed a notice of appeal in response.

That he has appeared in dozens of other lawsuits in the State was not addressed in the order, but it may be worth noting to his opponents both past and present that pursuant to this Court, they cannot practice in New York.

You can view the decision here.

The decision arose in Platinum Rapid Funding Group, Ltd. v. H D W of Raleigh, Inc. d/b/a Pure Med Spa, a/k/a Pure Cosmetic and Surgical Center and Holly Donielle Wybel a/k/a Holly D. Wybel, Index # 605890/2017 in New York Supreme Court.