Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

CAN Capital To Bring its Executive Functions Back to Kennesaw

September 18, 2018 For CAN Capital, the power is coming back to Kennesaw, GA.

For CAN Capital, the power is coming back to Kennesaw, GA.

Gary Johnson, CAN’s Executive Chairman, said “Today, CAN Capital announced it will be moving its finance and executive functions from New York to Kennesaw. The board believes this move will position CAN for increased efficiency and faster decision making as it continues to meet the growing needs of small businesses. As a result, CEO Parris Sanz and CFO Tom Davidson currently based in NY, will be transitioning out of their roles. CAN Capital recently crossed the $7 Billion milestone of providing access to capital to small businesses which includes almost $300 million over the past year. The company also secured a commitment from Varadero Capital for up to $287 million to augment its expansion initiatives and capital.”

A spokesperson from CAN confirmed that Sanz and Davidson did not want to move to the Atlanta-area headquarters for personal reasons and that the board is conducting a new search for a CEO. Sanz has been with the company since 2004, rising to the CEO position in November 2016.

Founded in 1998, CAN Capital is among the oldest alternative lending companies.

The Google Battle for Lending & SMB Finance Keywords Revisited

August 29, 2018When it comes to Google’s organic search for major keywords, companies like Nerdwallet and Fundera still dominate. A few players, however, have gained or lost significant ground since last year.

The Small Business Administration relinquished its place on the first page for words like “business loan” and “business line of credit” while PayPal and Credit Karma have begun to make major appearances as their activity in these markets increases.

Take a look:

| Keywords | Fundera | Fundera | PayPal | PayPal | Credit Karma | Credit Karma | Kabbage | Kabbage | OnDeck | OnDeck |

| Date | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 |

| business loan | 1 | 1 | 2 | 3 | 4 | 5 | ||||

| merchant cash advance | 3 | 2 | 2 | 4 | ||||||

| working capital | 8 | 9 | ||||||||

| commercial loan | 3 | 1 | 5 | |||||||

| small business loans | 2 | 1 | 3 | 5 | 4 | |||||

| business line of credit | 2 | 2 | 5 | 3 | 3 | |||||

| fast business loan | 4 | 5 | 1 | 4 | ||||||

| business loan with bad credit | 7 | 5 |

| Keywords | Lending Club | Lending Club | Nerdwallet | Nerdwallet | National Funding | National Funding | Traditional Banks | Traditional Banks | SBA.gov | SBA.gov |

| Date | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 |

| business loan | 9 | 6 | 3 | 7,8 | 5 | 4,7 | 6 | |||

| merchant cash advance | 4 | 1 | 8 | 9 | ||||||

| working capital | 4 | |||||||||

| commercial loan | 2,7 | 3,8,9,10 | ||||||||

| small business loans | 9 | 3 | 7,8 | 5 | 7 | 1 | 2 | |||

| business line of credit | 11 | 1,4 | 1 | 6,7,8,9,10 | 4,6,7,9,10 | 5 | ||||

| fast business loan | 2 | 3 | 5,6 | 8 | ||||||

| business loan with bad credit | 1,4 | 1 | 2 | 2 | 3 |

As mentioned in previous posts, this is not a scientific analysis. Keywords are measured using a wiped browser on my own computer.

The value of a Page-1 ranking too, is not as valuable as it once was, due to the heavy placement of paid ads above the search results. Ads, however, are not a factor for the keyword “merchant cash advance” since Google banned all advertising for that search term last Fall. Originally it was theorized that the ban was accidental, but ten months later it is still in place.

No such ban exists on Bing.

Read my previous analyses on the industry’s search war over the years:

September 2017 The Google Battle for Lending and SMB Finance Keywords

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

Merchant Cash Advance Company Wins in Bankruptcy Court After Judge Rules It’s an Ordinary Part of Business

August 21, 2018 Last week, a bankruptcy judge in the Northern District of Illinois ruled that a merchant had used so many merchant cash advances that it had become a normal part of their business.

Last week, a bankruptcy judge in the Northern District of Illinois ruled that a merchant had used so many merchant cash advances that it had become a normal part of their business.

At issue was Network Salon Services, a business founded in 2004 that was brought back from the brink of insolvency in January 2013 by a merchant cash advance. That advance, coupled with dozens of advances from more than 14 MCA companies over the following 3 and a half years would keep Network Salon on life support until it finally failed for good.

At the end, Network Salon had just $200 to its name and nearly $4 million in outstanding future receivables due to MCA companies.

After the Chapter 7 proceedings commenced, the bankruptcy trustee came knocking on the doors of several MCA companies to give back the funds it believed had been fraudulently transferred and obtained through criminally usurious means.

One of those companies, NY-based LG Funding, pushed back hard, and on August 15th the judge ruled in LG’s favor. In a carefully considered decision, The Honorable Jacqueline Cox said that an exception applied to LG Funding. Unlike a normal creditor where certain property obtained leading up to a bankruptcy becomes returnable to the trustee, Network Salon relied on MCAs in its normal course of business for years and thus the transfers of funds to LG Funding was the ordinary course of business not subject to return.

So ordinary was it in fact that Network Salon used MCAs to make payments on other MCAs, going so far that at one point one of its bank accounts showed no deposit activity for a month except for deposits from MCA companies and online lenders.

Ultimately it didn’t matter if LG Funding was actually debiting the deposits made by rival companies rather than the actual proceeds of sales, Judge Cox opined, because this deviation from the contract was not fraudulent and both parties benefited from it.

The usury arguments, as usual, failed, because New York courts (The state governing LG Funding’s contracts) have already determined that MCA transactions are not loans and therefore can’t be usurious.

“The Trustee has failed to meet her burden to establish by a preponderance of the evidence that the transfers were preferential or constructively fraudulent and therefore subject to avoidance,” The judge ordered. “LG Funding has succeeded in establishing that the transfers were made in the ordinary course of business, defeating the Trustee’s 547(b) preference claim. The constructive fraudulent conveyance claim fails because Network Salon received reasonably equivalent value in the transactions in issue. Judgment will be entered in favor of Defendant LG Funding on all counts.”

This post is an oversimplified explanation. Download the 24-page decision HERE for the full facts and details.

The 2018 Top Small Business Funders By Revenue

August 16, 2018The below chart ranks several companies in the non-bank small business financing space by revenue over the last 5 years. The data is primarily drawn from reports submitted to the Inc. 5000 list, public earnings statements, or published media reports. It is not comprehensive. Companies for which no data is publicly available are excluded. Want to add your figures? Email Sean@debanked.com

| Company | 2017 | 2016 | 2015 | 2014 | 2013 |

| Square | $2,214,253,000 | $1,708,721,000 | $1,267,118,000 | $850,192,000 | $552,433,000 |

| OnDeck | $350,950,000 | $291,300,000 | $254,700,000 | $158,100,000 | $65,200,000 |

| Kabbage | $200,000,000+* | $171,784,000 | $97,461,712 | $40,193,000 | |

| Bankers Healthcare Group | $160,300,000 | $93,825,129 | $61,332,289 | ||

| Global Lending Services | $125,700,000 | ||||

| National Funding | $94,500,000 | $75,693,096 | $59,075,878 | $39,048,959 | $26,707,000 |

| Reliant Funding | $55,400,000 | $51,946,000 | $11,294,044 | $9,723,924 | $5,968,009 |

| Fora Financial | $50,800,000 | $41,590,720 | $33,974,000 | $26,932,581 | $18,418,300 |

| Forward Financing | $42,100,000 | $28,305,078 | |||

| SmartBiz Loans | $23,600,000 | ||||

| Expansion Capital Group | $23,400,000 | ||||

| 1st Global Capital | $22,600,000 | ||||

| IOU Financial | $17,415,096 | $17,400,527 | $11,971,148 | $6,160,017 | $4,047,105 |

| Quicksilver Capital | $16,500,000 | ||||

| Channel Partners Capital | $14,500,000 | $2,207,927 | $4,013,608 | $3,673,990 | |

| Wellen Capital | $13,200,000 | $15,984,688 | |||

| Lighter Capital | $11,900,000 | $6,364,417 | $4,364,907 | ||

| Lendr | $11,800,000 | ||||

| United Capital Source | $9,735,350 | $8,465,260 | $3,917,193 | ||

| US Business Funding | $9,100,000 | $5,794,936 | |||

| Fundera | $8,800,000 | ||||

| Nav | $5,900,000 | $2,663,344 | |||

| Fund&Grow | $5,700,000 | $4,082,130 | |||

| Shore Funding Solutions | $4,300,000 | ||||

| StreetShares | $3,701,210 | $647,119 | $239,593 | ||

| FitSmallBusiness.com | $3,000,000 | ||||

| Eagle Business Credit | $2,600,000 | ||||

| Swift Capital | $88,600,000 | $51,400,000 | $27,540,900 | $11,703,500 | |

| Blue Bridge Financial | $6,569,714 | $5,470,564 | |||

| Fast Capital 360 | $6,264,924 | ||||

| Cashbloom | $5,404,123 | $4,804,112 | $3,941,819 | $3,823,893 | |

| Priority Funding Solutions | $2,599,931 |

90% of PayPal Merchant Advances and Business Loans Are Performing On Pace

July 28, 2018 As of June 30, 90.6% of PayPal’s merchant advances and business loans were performing within the original expected repayment period, the company disclosed this week. That equated to $1.27 billion worth of deals. Only 4.2% of their merchants were more than 90 days behind their expected pace.

As of June 30, 90.6% of PayPal’s merchant advances and business loans were performing within the original expected repayment period, the company disclosed this week. That equated to $1.27 billion worth of deals. Only 4.2% of their merchants were more than 90 days behind their expected pace.

PayPal had $1.4 billion in outstanding merchant loans, advances, interest and fees receivables.

Swift business loans are charged off when they are more than 180 days past due. The Working Capital products (which can be loans or advances) are charged off when the merchant is 180 days past the company’s original expectations and no payment has been made in the last 60 days OR when the merchant is 360 days beyond the company’s original expectation.

Swift Business loans are generally repayable over 3-12 months. Working Capital advances are generally expected to be satisfied within 9-12 months.

After PayPal acquired Swift Financial, the company began marketing itself to small businesses as LoanBuilder. A flyer obtained by deBanked showed that it was being marketed with loan amounts of $5,000 to $500,000 that could be funded in as quick as 1 business day.

Stacking Lawsuit Results in Settlement Before Trial

June 19, 2018A lawsuit between RapidAdvance and Pearl Capital over tortious interference will not be going to trial after all, deBanked has learned. Originally scheduled to begin on June 25th, the parties have reportedly reached a settlement.

Neither party would respond for comment.

RapidAdvance filed its lawsuit against Pearl in November 2015 with the hope that they could set a precedent against “stacking.”

The suit was filed in the Circuit Court of Maryland under Small Business Financial Solutions, LLC v. Pearl Beta Funding, LLC, Case No. 411478-V.

Settling Up: Debt Settlement Companies Paid Yellowstone Capital and Everest Business Funding a Half Million Dollars to End Lawsuit

June 12, 2018 A group of debt settlement companies and ISOs have entered into a settlement they’re unlikely to forget. A lawsuit that accused Corporate Bailout, Protection Legal Group, Mark Mancino, Michael Hamill and others of tortious interference with merchant cash advance contracts has led to a settlement in which the defendants agreed to pay Yellowstone Capital and Everest Business Funding $500,000. They also agreed not to offer any services to Yellowstone or Everest merchants in the future, deBanked has learned.

A group of debt settlement companies and ISOs have entered into a settlement they’re unlikely to forget. A lawsuit that accused Corporate Bailout, Protection Legal Group, Mark Mancino, Michael Hamill and others of tortious interference with merchant cash advance contracts has led to a settlement in which the defendants agreed to pay Yellowstone Capital and Everest Business Funding $500,000. They also agreed not to offer any services to Yellowstone or Everest merchants in the future, deBanked has learned.

The original complaint alleged that ISOs had partnered with companies that purport to offer debt relief services to merchants with MCAs. In practice, the complaint said, debt relief was a code word for deceiving merchants to breach their existing agreements so that they could pay fees instead to the debt relief companies.

When asked to comment, Yellowstone Capital CEO Isaac Stern said that there were companies that offer this kind of service the right way but that was not the case here. “The way they’re going about it is really wrong,” he said.

Of note is that the bound parties were not just debt settlement companies but also ISOs and a law firm (Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group).

Additional companies not named in the original complaint but nonetheless bound to the settlement are Mainstream Marketing Group and Corporate Client Services LLC. Websites for both companies say that they offer small business debt relief services.

Coast to Coast Funding LLC, who the defendants represented they had no control of, did not participate in the deal.

The settled matter is not the first of its kind. Everest and Yellowstone have been hammering debt settlement companies with lawsuits this year, according to court records examined by deBanked. In January, Everest sued MCA Helpline and Todd Fisch for tortious interference, and just last month Yellowstone filed a Petition to recover funds that were allegedly fraudulently transferred by Settle My Cash Advance.

In the latter case with Settle My Cash Advance, the defendants are alleged to have actively coached a merchant to hide his money in new bank accounts and hide the paper trail rather than pay the money owed to Yellowstone.

Speaking about no case in particular, Stern said “Imagine getting a commission on a deal [where you help a small business get funding] and then sending it to a debt settlement company. If there are ISOs that are doing that, we’re going to come after you hard.”

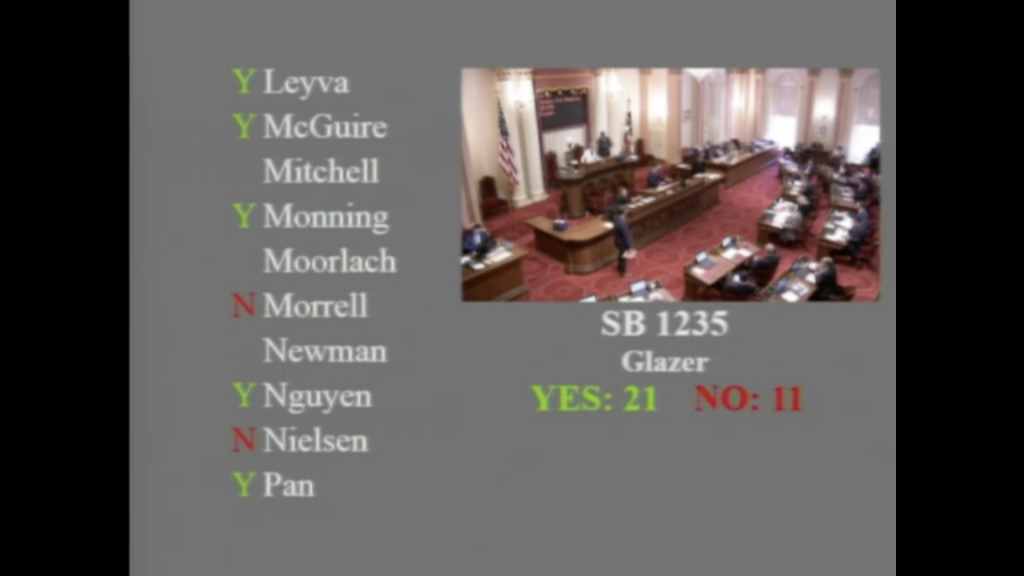

Commercial Financing Disclosures Bill Approved in the CA Senate

May 31, 2018The use of an annualized cost metric on loan and non-loan contracts alike is now one step closer to becoming the law in the State of California. On Thursday, SB 1235 was approved on the Senate floor. The bill calls for commercial finance companies to disclose an Estimated Annualized Cost of Capital. In previous hearings, the bill’s author, Sen. Steve Glazer (D), stated that it was his intention that this apply to merchant cash advances as well.

“This estimate includes all charges and fees incurred for the financing, assuming you make all payments when scheduled and adhere to the terms of the agreement. This number is based on the estimated term. If the actual term is shorter than estimated, the annualized cost of capital may be higher than shown. If the actual term is longer than estimated, the annualized cost of capital may be lower. This is not an Annual Percentage Rate (APR).”

Here is how to calculate the Estimated Annualized Cost of Capital as set forth in the bill:

Here is how to calculate the Estimated Annualized Cost of Capital as set forth in the bill:

(1) Divide the total dollar cost of financing by the total amount of funds provided.

(2) Multiply the result in paragraph (1) by 365.

(3) Divide the result from paragraphs (1) and (2) by the term or estimated term of the financing in days.

(4) Multiply the result from paragraph (3) by 100.

(5) The result from paragraph (4) shall be labeled “The Estimated Annualized Cost of Capital.”

In addition, commercial finance companies will also have to disclose the total dollar cost of the transaction and the total amount of money the merchant will receive net of all fees.

The bill must now pass through the solidly Democrat-controlled Assembly and be signed by the Governor to become the law.