Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Why Lexington Capital Holdings is Expanding Into the Real Estate Business

September 24, 2025Lexington Capital Holdings is expanding beyond small business lending and into real estate, the company recently revealed. Lexington, a Long Island-based financial marketplace and brokerage led by CEO Frankie DiAntonio, is launching Lexington Estates to buy, sell, rehab, and hold properties long term.

According to DiAntonio, deals involving real estate have already been a part of their regular broker product mix for a long time, but when deciding whether or not they wanted to lend against real estate on their own or become the actual buyers and builders, they felt the latter would be more impactful. A syndication fund for these real estate deals, for example, will be open to employees of the firm to participate in. Lexington’s existing operation already has about 50 sales reps. Two from that group will move over to the real estate side to join a number of new hires they’re bringing on board to carry this plan out.

“Business is a team sport and I wouldn’t have been able to do any of this without the amazing Lexington team behind me,” DiAntonio said of the company’s success to-date.

Lexington Estates is already closing on its first property on Long Island. While they will make their focus local right out of the gate, they plan to work on deals both residential and commercial throughout the United States within 12 months. DiAntonio cut his teeth on real estate deals by participating in them personally outside of his business and now he’s making it a corporate endeavor. Whether it’s residential, retail, office space, industrial space, or anything else, they plan to evaluate it on the merits of the potential profits.

“I’m looking for deals,” DiAntonio said. “I’m looking for what’s the best bang for our buck.”

DiAntonio views this ambitious plan as one of absolute necessity given the challenges that the younger generation faces with the cost of living going up.

“I strive so hard to put my people in a position where they can make more money than the average American because you can’t even live the average American life and be average anymore,” DiAntonio said. “You actually have to be great just to live an average American life.”

Lexington Estates plans to officially launch on October 12th.

Is Jack Dorsey Satoshi Nakamoto? I Say Yes

September 20, 2025I’m the originator of the theory that Jack Dorsey is Satoshi Nakamoto, the creator of Bitcoin, which I first considered in February 2024. After extensive research, the theory has now been firmed up with incredible circumstantial evidence. I was the first person to discover that Dorsey was registered on the cypherpunk mailing list under two different email addresses, the first to recover Dorsey’s personal webpage dedicated to cryptography in 1997 (and his home page here), and basically connect all the dots that I compiled in my tweet below:

THE NEWEST WHY JACK DORSEY IS SATOSHI NAKAMOTO

C++ for Bitcoin source code

Now confirmed Jack coded in C++ as far back as mid-90sC in the White Paper

Now confirmed Jack coded in C as far back as mid-90s.Satoshi pseudonym

"Satoshi" was the first tweet Jack's best friend…— Seán Murray (@financeguy74) August 2, 2025

Catching Up With Kalamata

September 18, 2025 Kalamata Capital Group is continuing to fund in Texas through one of its affiliated entities, the company confirms. Kalamata, which recently upsized its 2024 securitization by 25% with notes expandable up to $500 million, offers a variety of funding products to small businesses around the United States. A new law that recently went into effect in Texas has prompted Kalamata and companies like theirs to get the word out to their partners about any applicable adjustments.

Kalamata Capital Group is continuing to fund in Texas through one of its affiliated entities, the company confirms. Kalamata, which recently upsized its 2024 securitization by 25% with notes expandable up to $500 million, offers a variety of funding products to small businesses around the United States. A new law that recently went into effect in Texas has prompted Kalamata and companies like theirs to get the word out to their partners about any applicable adjustments.

More front and center for the company, however, is the introduction and evolution of Kalamata Cash, its in-house proprietary software.

“We went live with everything, including our syndicator profiles and access to the outside world as well, and that’s been a really exciting development for the company,” said Brandon Laks, co-president at Kalamata, “because instead of licensing software, which the software we were on was great before, it gives us the ability to roadmap exactly what we want to do.”

Kalamata, for example, is 100% broker-driven, and they can custom-tailor the process to best suit their relationships.

“Our brokers can come in and see live calculators,” Laks said, “so when they submit a deal and we send an offer, they can get a live view of what steps are outstanding, they can play around with the sliders and choose their offers.”

And there’s a lot more on the horizon that they’re integrating with and adding on.

Guggenheim Securities served as sole structuring advisor and the sole initial purchaser of the notes in the Kalamata securitization deal. At the time of the announcement, Laks said, “The access to additional capital will allow Kalamata to continue supporting Small Businesses and invest more capital in proprietary technology to stay at the forefront of the small business financing industry.”

The Merchant’s Paying, The Bank Statements Were Fraudulent: Talking With MoneyThumb

September 16, 2025Small funders trying to tackle fraudulent submissions with no tools stand almost no chance in today’s environment. A recent survey conducted by both MoneyThumb and deBanked, for example, found that small funders experience fraud in 11.8% of applications on average, more than double the rate of larger funders. In the past, detecting altered documents such as bank statements, was best managed by experienced underwriters, but now with technology and AI in the palm of everyone’s hands, today’s fraud is often imperceptible to the naked eye.

“If you go back to 2020 when we created this [Thumbprint technology], I would say about 80 to 85% of bank statements that were fraudulent we would look at and say, ‘there’s the fraud,'” said Ryan Campbell, CEO of MoneyThumb. “Now it’s sub-5% that I can identify just with the human eye, and so technology has just absolutely created an environment where people can create fraud in a way that they never could.”

Thumbprint is MoneyThumb’s patented fraud detection tool. It can bolt into any industry CRM. Historically, an immediate default was the first clue that a fraudulent app had slipped through the cracks, but even accounts in good standing may not be what they seem.

“[What] we’ve seen is people take a smaller loan, then a slightly larger loan, and then the big one, the third loan—default,” said Campbell.

Bank statements that are otherwise in perfect order may have had their transaction descriptions edited so that loan deposits from third parties look like revenue or round-trip payments with the owner’s personal account are reclassified to look like daily sales. For fraud like this, the numbers are real, the statements are real, but what’s revenue and not revenue is obfuscated. And when the deal is approved based on the misleading metrics the scammers can actually stick around to pay for a while to convince the underwriters that they’re worthy of more.

Bank statements that are otherwise in perfect order may have had their transaction descriptions edited so that loan deposits from third parties look like revenue or round-trip payments with the owner’s personal account are reclassified to look like daily sales. For fraud like this, the numbers are real, the statements are real, but what’s revenue and not revenue is obfuscated. And when the deal is approved based on the misleading metrics the scammers can actually stick around to pay for a while to convince the underwriters that they’re worthy of more.

“We’ve run quite a few portfolio analyses for our funders, and so we’ll review all of the statements that they have, all of the funded deals that they’ve done, and many are surprised to find out that they actually have fraudulent paying accounts on their books,” Campbell said.

Since the rate of fraudulent applications is so material, catching the fraud as early as possible is paramount. This saves cost on underwriting, reduces time spent on deals that won’t move forward, and spares referral partners the pain of a deal getting killed at the finish line for an uncurable problem.

“As soon as it comes in, rather than wasting time on ‘are we collecting this? Are we extending offers?’ because think, it’s not just the fraud,” said Campbell. “Even if you can catch the fraud at the very end, somehow it’s not the catching part, it’s the fact that your staff is working a fraudulent deal for some matter of days. And Thumbprint just says, ‘get it out. It’s gone, done,’ and right at the beginning of the process.”

Don’t Wait, Arbitrate: New Era ADR and MCA Claims

September 10, 2025 “New Era, in a nutshell, is 100 days in arbitration, so legally enforceable arbitration, all for one flat fee, all on our platform,” says Rich Lee, CEO of New Era ADR. “This is deliberately built for the bulk of litigation, the stuff that organizations and people just want to get resolved fast, and they don’t want to just accept sub-optimal outcomes like walking away from a collection or settling an employment claim when they didn’t do anything wrong.”

“New Era, in a nutshell, is 100 days in arbitration, so legally enforceable arbitration, all for one flat fee, all on our platform,” says Rich Lee, CEO of New Era ADR. “This is deliberately built for the bulk of litigation, the stuff that organizations and people just want to get resolved fast, and they don’t want to just accept sub-optimal outcomes like walking away from a collection or settling an employment claim when they didn’t do anything wrong.”

Many industries, including automakers, banks, real estate companies, sports teams, and even the Olympics, rely on the New Era platform to handle arbitration cases. MCA companies too are using New Era, according to Lee. While arbitration as an established process to resolve contract breach claims is not new in MCA, the workloads experienced by certain court systems can make the speed and efficiency of arbitration a preferred alternative. New Era’s arbitration is all virtual so one party is not prejudiced by having to travel a long distance to go through it. And the process, managed by arbitrators that are knowledgeable in the specific area of law a claim calls for, is fast enough that if an award is issued in favor of a funder, they’ll be able to act on it quickly.

“If you started in court, because of the congestion, a lot of courts you’re waiting sometimes a year to get that court order,” Lee says. “But on our platform, inside of about 100 days, you’re getting the arbitration award and then maybe you’re tacking on an extra 30 days just for the court to give you the corresponding order. So that’s how it works. And so we’re actually seeing these MCA clients, their awards now on New Era are getting enforced and they’re getting the corresponding court orders.”

Beyond the 100 day resolutions, they actually have some funders who are getting arbitration awards for uncontested disputes in far less than 100 days, some in 30 days. Given that the arbitrators are neutral, even these situations are scrutinized, but it is done in an efficient manner.

New Era has over a hundred arbitrators on their tech-first arbitration platform which benefits from scale. “Even though it’s 90% faster and cheaper, [it’s the] same quality arbitrators and mediators you’d find anywhere else,” he says.

Those arbitrators are not just the standard style retired practitioner either. While New Era has many retired judges and lawyers on their bench of arbitrators and mediators, they also have many who are highly-experienced lawyers who are still practicing law. These people who are partners in law firms, in-house counsel at companies who are already very experienced lawyers in their space who are hearing these cases.

Lee says there’s always a conflict check before anyone is assigned and the benefit is an arbitrator familiar with the active area of law.

“So we’re able to put only employment arbitrators and mediators on employment cases. If an MCA came in they would never see one of our employment arbitrators, they would only see the folks who know finance, who know this space,” Lee says. “Our arbitrators for MCA disputes not only have finance experience, but specifically MCA-specific experience and many have New York-specific jurisdiction experience.”

New Era’s virtual platform enables resolution in all states and jurisdictions, not just New York, as they have neutrals across the country.

Lee is a former corporate and IP attorney himself and his three co-founders are also lawyers or have worked in a legal environment. And what he experienced from his career is that not every litigation should be as time-intensive as something like Google fighting Uber on a big stage, for example.

“The fact is like 99% of litigation doesn’t need the kind of two to three years that are synonymous with our court system and traditional arbitration systems, or even a year,” Lee says. “Examples in the employment world is, companies end up settling cases when they didn’t do anything wrong. Employees end up not bringing cases if they’ve actually been wronged. And then for the lender world they end up just charging off a lot of this debt because there’s no point in going and pursuing a case in court, many times spending all that time–the time is almost the worst part, right? The money too. But then by the time you get your court order, especially in the MCA world, a lot of these are unsecured cash advances and so you’re kind of left with no recourse and the cash is gone. And that’s kind of really messed up because that all comes back to like, ‘well, the systems that exist aren’t there for this 99%’ and so that’s what New Era is.”

Business Finance Brokers in 2025

August 15, 2025

We’re now ten years out from the original “Year of the Broker” article in deBanked Magazine. Brokers are still here, the business has just changed slightly. Here’s some of the top line differences vs. 2015:

Cold Calling: 12% of merchants say they started their search for business funding options from a cold call.

Google Search: Organic search rankings beginning to diminish in favor of AI Q&As.

Training: AI can now listen to every call and grade you on every component of it.

CRMs: Pen and paper are over. Every touch on a deal should be traced and automated and deal tracking organized in a system.

Competition: Every POS solution and merchant fintech software now has a funding button embedded into it.

Commissions: Still high.

Funding Options: Lines of credit, term loans, MCAs, SBA, equipment financing, real estate lending, and more.

Regulations: There are now numerous state registration and disclosure requirements. (See the map here).

Leads: Referral networks are now more valuable than ever. Referrals from CPAs, lawyers, trade associations, chambers of commerce, and more.

Gates: You may have to go through a super broker to get access to a top tier funder.

Startup Costs: The registration requirements in several states has significantly increased the cost of starting a new broker shop today.

Adding Event Connections to DailyFunder

August 12, 2025MY BIG PET PEEVES WITH “EVENT APPS” ARE:

1. 95% of users stop using them after the event is over.

2. Most are white labeled from a third party with no customizable solutions.

3. They are generally zero-sum in that everyone can see you’re going or no one can. People want to choose their own visibility.

4. If a boss buys 10 tickets under their name for their team, it makes it hard for the individual team members to be able to access the app because their info isn’t in the system.

5. There are generally no moderation capabilities to limit or stop abuse.

6. Redundancy.

We had a deBanked Events App (2018 – 2023 white labeled), a deBanked App (2015 – 2017 white labeled), and a DailyFunder App (2013 – 2017 white labeled), but we recently rebooted a DailyFunder App only.

Why DailyFunder? With 17,000+ members, 3 million+ annual page views, and an average session > 10 minutes, it seems the most logical starting point to tackle point 1 above, which is keeping a party going 24/7 instead of just a few days before an event and never again right after. We’ve moved development in-house, no more white labels. We can put events in there whether they’re affiliated with us or not. You can let people know if you’re going or not. You can dm other people that plan to go. You can follow up with them afterwards. You can see the sponsors. We can put video content in there like tech companies that demoed or the interviews on the red carpets. No, you won’t see the whole attendee list, but you’ll be able to see those that want other people to connect with them at each one. You can use your real name or be pseudonymous. We can remove fakers. You can post on the forum. You can see what people are saying. It doesn’t all end when the event ends. You can see news headlines from deBanked and other video content we choose to put on there.

This is a work-in-progress but currently live in the Apple App Store and Google Play Store. If you have ideas or suggestions, email them to webmaster@dailyfunder.com. There’s some bugs we’re aware of. You must have a DailyFunder account already to log in. The registration process is still only on the website but we’ll change that.

Some thoughts are being able to add events like a Title sponsor’s cocktail party, a related golf-outing, etc. People are always asking which company is having a party after an event or before.

So instead of having to go on the forum, facebook groups, linkedin, or the whatsapp chats to be like “yo, xyz is happening.” or “who’s going?” we can just add it in here and then everyone can see them in one place to communicate with each other about them if they want to.

Open to suggestions.

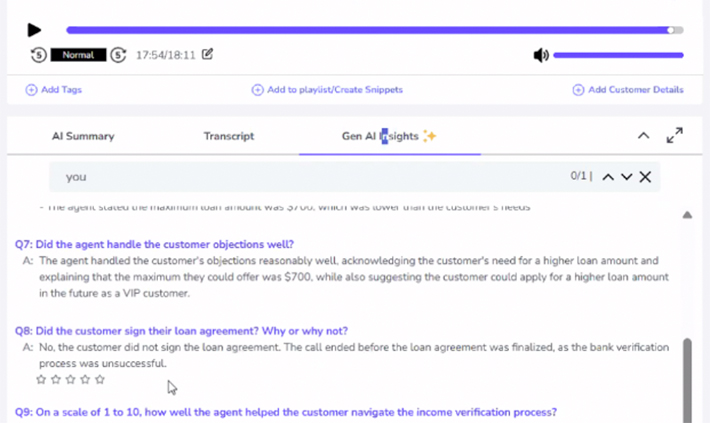

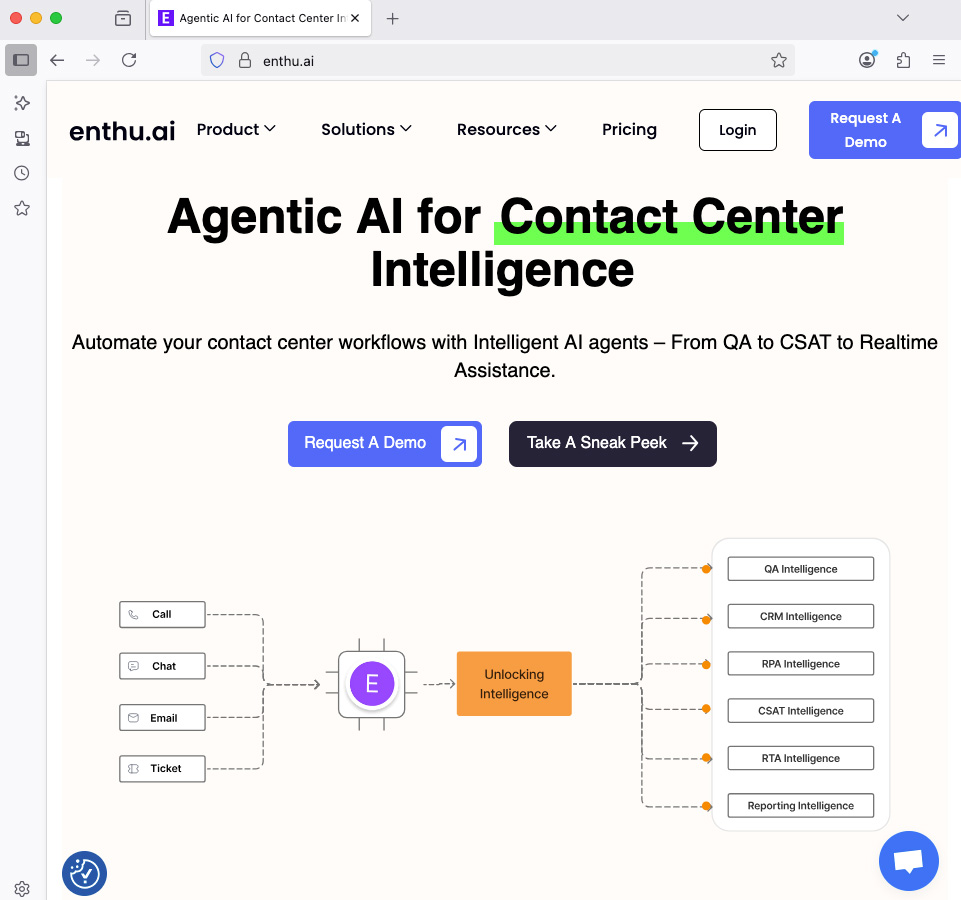

How Are Your Sales Calls Going? How One AI System Can Score Performance

July 21, 2025 The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

“The way [our] platform works is we integrate with the dialer,” says Atul Grover, Co-founder and VP of Sales for Enthu.AI. “Typically, what we have seen with our clients, the calls are automatically pushed within two or three minutes after the conversations are done.”

With Enthu, a company’s call recordings go through their AI system to be analyzed based on either their own scorecard, the client’s, or both. Whatever the outcome of the call, lost sale, closed deal, or neither, management receives a report to see how the rep performed. Did the rep try to build rapport? What were the objections? Did they handle objections well? Did the rep sound confident when answering difficult questions? Across hundreds or thousands of calls each week, any rep can get an unbiased report card of their strengths and weaknesses. These metrics can then be compared with peers, without the worry of human bias deciding the outcome. They can’t blame the boss for simply favoring another rep, for example.

Originally, when Enthu started, they focused mainly on keyword spotting for compliance purposes, evaluating whether or not reps were saying what they were supposed to across thousands of calls. But that had its limitations.

“That’s how we started our journey, using purely keyword spotting,” Grover says, “but the challenge over there is that you can’t basically expand or scale it. So that’s why we use our AI approach, where it’s primarily intent-based rather than keyword-based. So we look at the intent of all the conversations.”

Rather than AI replacing sales reps, as some theorize might happen over time, it can be used to make them a whole lot better. And this is already being employed today. Enthu, for example, is currently being used in financial services, healthcare, home industries, property management, and more. Grover says clients are already using it to measure disparities in call performance and then using those insights to coach reps who score on the lower end.

“Our platform also offers the ability to create a playlist for the good recordings, which you can use to train your new agents,” Grover says. “So rather than training in general that’s like, ‘okay, this is our company product, this is our company offerings, you should talk like this,’ they can share those good recordings with the new agents so they can listen to how their good sales agents are doing, and then get trained on the real data.”

Recording calls and finding good ones is not a new capability, anyone can do that. But it’s the ability to identify certain call situations at scale that makes all the difference when trying to evaluate and coach. If a new objection is tripping up the team, management can pull every instance it has come up, calculate its frequency, and use that information to determine the best path forward. These are things that would typically rely on the “vibe and feel” of the sales floor, as reps relay information to the boss, who must then assess whether the trend is legitimate or just a statistical blip.

Independent analysis can also be critical when a company is evaluating a lead source or referral partner, especially if that partner is also expecting to be judged objectively. And when the lead source changes, the AI can be told in advance whether the calls are outbound or inbound, hot or cold, or how they differ from other types of calls the company handles. The resulting evaluations can then reflect those circumstances.

Success, in this way, can be gamified, allowing reps to strive for higher grades across all areas of a call and objectively compare themselves to colleagues in an emotion-free environment. The AI can score each call or aspect of a call on a scale from 1 to 10 and produce a summary score for each rep over a day, week, or month, unlocking new motivational challenges. An underperforming rep could be recognized for a top score in overcoming objections, for example, even if they didn’t close the most deals. Picture a Broker Battle, but the judge is an AI.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

“It’s definitely going to be great help for the sales organization,” Grover says. “And if we talk about the lending industry, you talk about compliance and everything, or let’s say the collections department, because they want to make sure that their agents are not screwing up, because there’s legalities involved if they mess up anything. So that’s what our system will flag, where they are doing right or where they’re doing wrong.”

If a client wants to keep keyword spotting as part of the analysis, they can. Grover says pre-set words can be marked as zero-tolerance or flagged for management. The more data and calls the system analyzes, the better it gets.

Grover adds that even if a client isn’t ready to fully integrate Enthu, they can still use old call recordings to access analytics.

“We have some customers in that space where they don’t have a dialer but they still have the recording,” Grover says. “So our platform also allows to upload the recordings directly by the client itself, on the platform itself, where they can upload the calls manually, then you’re still going to get the same intelligence, same analytics, same scorecard mechanism, even if you upload it manually.”