Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Debunking Jameson Lopp’s Rebuttal on the ‘Jack Dorsey is Satoshi Nakamoto’ Theory

December 1, 2025Back in February 2025, prominent Bitcoiner Jameson Lopp attempted to debunk the theory that Jack Dorsey was Satoshi Nakamoto. Unfortunately, almost all the information he relied on for his arguments were either wrong or required leaps of the imagination. While I addressed this immediately after he posted them here and here, they’re being republished here:

Lopp: “During the time period of 2009 & 2010, Jack Dorsey was not only Chairman of the Board of Twitter, but also the CEO of the fledgling startup Square. It’s quite clear that he was an extremely busy person not only overseeing multiple companies, but traveling around the world meeting important people, doing press interviews, speaking at conferences, promoting philanthropic causes, and more. His activities do not fit the profile of someone who had the time and mental bandwidth to also be building a completely new financial system from scratch while maintaining perfect anonymity.”

Counter:

Twitter: Jack was fired from Twitter in mid-October 2008. He was made “silent” Chairman with no active role in the company and did not return in an active capacity at Twitter until March 28, 2011. So there is no conflict with his role at Twitter as he did not have an official job function there during the time period in question.

Satoshi Nakamoto published the White Paper on October 31, 2008 and sent his last farewell email in April 2011. This reinforces the plausibility that Jack is Satoshi since Satoshi appears right after Jack leaves Twitter and exits right as Jack returns to Twitter. Also, Jack published a reference to the name Satoshi in March 2011, showing that it had been the first tweet ever made by his best friend & love interest (Crystal Taylor) on the beta version of Twitter.

Square: Was Jack too busy launching Square? The company was founded February 11, 2009 and didn’t launch until December 2009. Coincidentally, Satoshi complained about being too busy with work during the same time period.

June 14, 2009 – Satoshi Nakamoto: “Thanks, I’ve been really busy lately.”

July 21, 2009 – Satoshi Nakamoto: “I’m not going to be much help right now either, pretty busy with work, and need a break from it after 18 months development.”

May 16, 2010 – Satoshi Nakamoto: “I’ve also been busy with other things for the last month and a half. I just now downloaded my e-mail since the beginning of April. I mostly have things sorted and should be back to Bitcoin shortly.”

July 8, 2010 – Satoshi Nakamoto: “I’m losing my mind there are so many things that need to be done.”

August 27, 2010 – Satoshi Nakamoto: “Sorry, I’ve been so busy lately I’ve been skimming messages and I still can’t keep up.”

April 23, 2011 – Satoshi Nakamoto: “I’ve moved on to other things. It’s in good hands with Gavin and everyone.”

So if Lopp’s argument is that Jack would’ve been really busy with launching Square then Satoshi complaining about being really busy during the same time period actually reinforces the plausibility of it being Jack.

Lopp: “Jack Dorsey worked with the US Federal Government to visit several countries (Iraq, Mexico, Russia) on behalf of the US tech industry. Does anyone truly believe that Satoshi Nakamoto, who was extremely wary of gaining attention from governments, would be working directly with them?”

Counter: A lot of people truly believe Satoshi worked with the government or was the government. The characterization that Satoshi was “extremely wary of gaining attention from governments” is not based on anything, unless he was referring to the incident in which Satoshi advised people not to donate Bitcoins to WikiLeaks. That incident ironically makes it more plausible that Satoshi was Jack Dorsey because Twitter received a secret court order regarding WikiLeaks (December 14, 2010) a day apart from Satoshi’s last activity on the Bitcoin forum (December 13, 2010). Square was also courting a relationship with Visa, which had made it a policy to restrict funds to WikiLeaks. The Square / Visa partnership was announced on April 27, 2011, four days after Satoshi’s last farewell email.

Lopp: “The first version of the Bitcoin software was Windows only, meaning that Satoshi developed it on Windows. I’m sure Jack used Windows at some point in his life, but he has been a die-hard Apple fan ever since the original iPhone came out. You can find many posts where he refers to various Apple devices he uses. I personally recall speaking with him several years ago and learning that he doesn’t even use laptops or desktops, but sticks to iPhones and iPads. It appears that may have even been true back in 2010. While reading through his 6,200 tweets I saw many referencing Apple products but none regarding Microsoft or Windows.”

Counter: Windows had a 95% share of the entire desktop OS market in 2009. No serious developer that was planning to appeal to mainstream desktop users would’ve developed for anything other than Windows even if they were a “die-hard Apple fan.” Regardless, Jack used Windows, MacOS, FreeBSD, OpenBSD, Blackberry OS, and several flavors of Linux including Gentoo.

Lopp: “I think the best we can do is to show that the person was out and about doing things while Satoshi was known to be sitting at a keyboard.”

Counter: Lopp assumed that posting comments to the internet in 2009 and 2010 required one to be “sitting at a keyboard” despite Jack being a prolific Blackberry user (since at least the year 2000) and later an iPhone user.

Lopp says that Jack can’t be Satoshi because on November 6, 2009 Jack tweeted “Late lunch with @fredwilson” and 5 minutes after that, Satoshi committed code to the Bitcoin SourceForge repository. I’m not sure what this is supposed to imply. Is it not possible that Jack was going to have a late lunch with Fred Wilson but committed code before heading out to do that? Lopp makes the assumption that Jack has to be sitting at the table with Wilson when the tweet is sent for this supposed conflict to be true. Lopp forcing whatever narrow meaning he wanted to tweets to fit his narrative and making the additional assumption that Jack could not post from a smart phone to the internet under the Satoshi name are the basis for his entire rebuttal. Not very good.

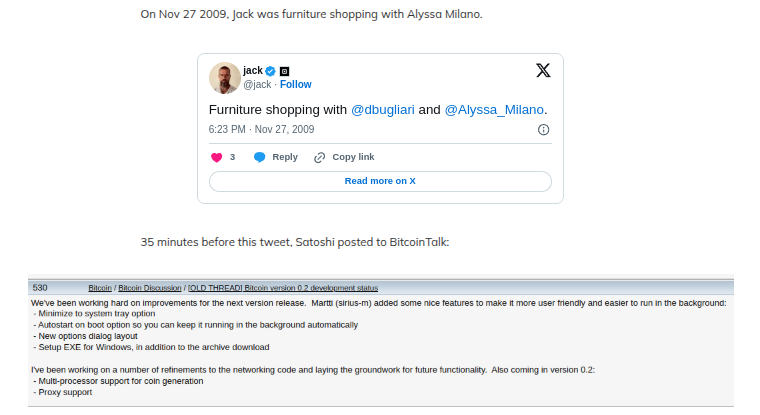

Lopp says that Jack can’t be Satoshi because on November 27, 2009 Jack tweeted that he was furniture shopping with Alyssa Milano and that 35 minutes prior to that Satoshi posted to the forum. Not sure what this is supposed to imply. Satoshi can’t post to a forum and then go shopping? Have people never posted to a forum and then gone somewhere afterwards? Would it not be possible for Satoshi to post to a forum from a phone even if it means he did it while shopping? Ironically, I’ve posted previously about the possibility of Alyssa Milano specifically being in on the Satoshi secret. Not very good.

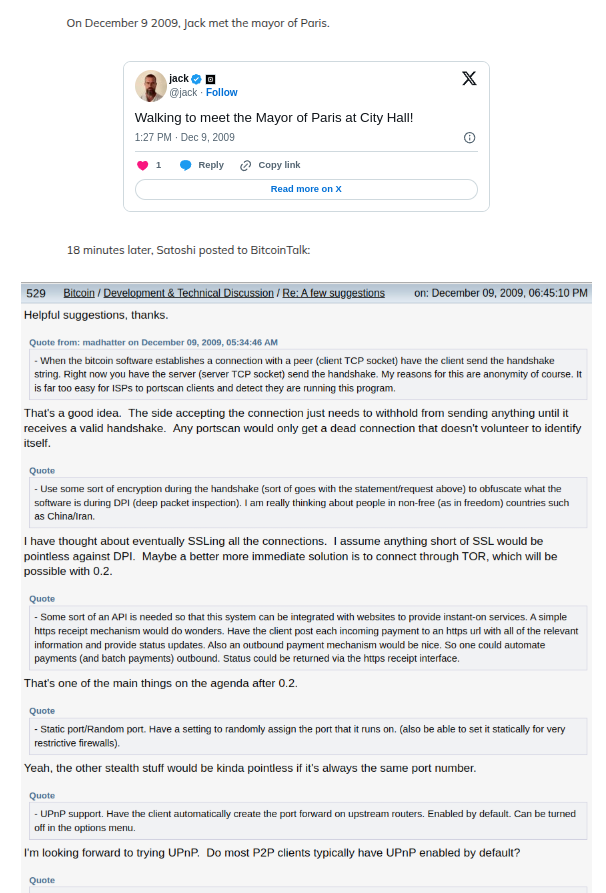

Lopp says that Jack can’t be Satoshi because on December 9, 2009, Jack tweeted that he was walking to meet the Mayor of Paris at City Hall (in Paris) and then 18 minutes later Satoshi posted to the forum. Lopp presumes that Jack was not capable of posting to an online forum while waiting at City Hall to begin the meeting. When did the meeting start? How long did he wait? People post online while they sit and wait for meetings. I have personally sat in government buildings and waited for meetings with officials and passed the time by posting to forums. Why is this considered to be impossible? Answering emails and posts is and was a commonplace thing to pass the time. Not very good.

Lopp says that Jack can’t be Satoshi because he attended a long company meeting on February 26 that ended at 10pm and Satoshi made posts on the forum at 6:17pm and 6:48pm. Okay? He couldn’t have posted before the long meeting? Pretty weak. Not very good.

Lopp says that Jack can’t be Satoshi because on May 20, 2010, Jack tweeted that he was in a car with his brother to go out to dinner with his family and 10 minutes later Satoshi posted to the forum. Was it Jack driving or his brother? Because if it’s his brother, then Jack can post from his phone to the forum while they’re driving. But if it’s Jack driving, then how is he also tweeting? Hmmmm…. Or did they get to the restaurant already and they are waiting and Jack is posting to the forum from the restaurant. I’m still lost on why Jack couldn’t post to a forum from his phone. Why are these things conflicts again? I myself was posting to forums from my phone in 2010. Not very good.

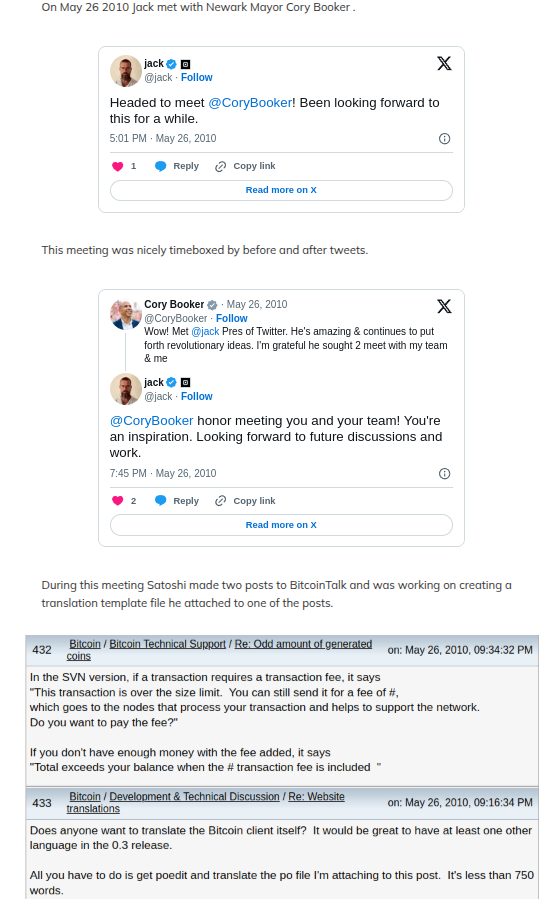

Lopp says that Jack can’t be Satoshi because on May 26, 2010 he tweeted that he was headed to meet Senator Cory Booker at 5:01pm and Satoshi posted to the forum at 5:16pm (with a file attached) and again at 5:34pm. Booker tweets at 7:32pm that he had just met Jack and Jack tweeted at 7:45pm that he had just met Booker. It seems like they actually met late then, perhaps around 7pm. Not sure why it’s considered impossible for Jack to say that he’s headed to a meeting and subsequently post to a forum (with an attachment) before actually being in the meeting itself, which doesn’t appear to have taken place for a while. Maybe Jack left later than he said he was leaving or maybe Jack got there and ended up waiting around for a very long time before the meeting and played on his phone and posted to the forum as people do when they’re bored. Not very good.

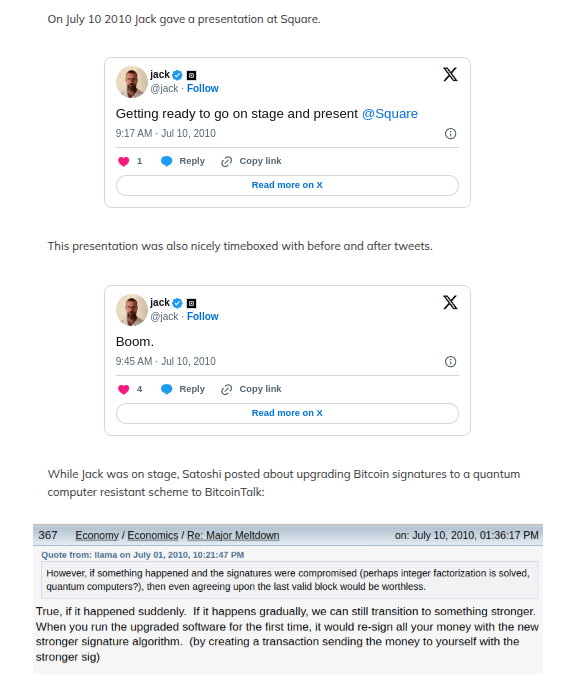

Lopp says that Jack can’t be Satoshi because on Saturday, July 10, 2010, Jack tweeted at 6:17am local time that he was getting ready to go on stage and present Square, followed by Satoshi posting four sentences to the forum at 6:36am local time, followed by Jack tweeting “Boom.” at 6:45am. (The screenshots says 9:17 and 9:45 respectively because they show my timezone) Lopp presumes that “getting ready” means that the presentation, which he believes to be at Square’s headquarters, was starting within minutes or seconds of that first tweet and that the subsequent tweet of “Boom” meant it was over. Satoshi posting in between these times therefore makes it impossible to be Jack.

This presentation was taking place at the Sun Valley Conference in Idaho, an invite-only event for major tech moguls. Jack was even at the Sun Valley on Ice show that evening. There is no evidence I have seen to suggest that “Boom” meant he had finished giving his presentation but Lopp needs us to believe that in order to create a conflict in the timeline to support his argument. Not very good.

Lopp points to the fact that Satoshi posted to the forum precisely during the short window that Jack was meeting with the President of Chile in Santiago on July 14, 2010. Satoshi posted at 9:10pm UTC time on the forum which would have been 5:10pm in Santiago.

Jack:

(1) says at 3:36pm that he’s on the way to meet him and that they will spend an hour together

(2) suggests that their meeting was already over by 5:03pm.

At 4:10pm a tweet goes out from the President’s account about their meeting. It does not confirm they are actually together yet even if it implies they are.

Satoshi posts to the forum at 4:25pm.

Jack signals the meeting is over with a tweet at 5:03. Satoshi posts at 5:10pm local time. While narrowly outside the perceived window, it is outside of it, and we don’t know when the meeting actually ended. It could have been over at 4:45, for example. A tweet at 5:03 doesn’t mean it ended at exactly 5:03.

It is well documented that Jack and the President met but it is not known for precisely how long. It could have been 10 minutes as these are how these things go, particularly with important figures like a head of state. Lopp takes the hour at face value and combines it with his belief that Satoshi did not have access to a cell phone in order to make his debunking work. Besides, couldn’t Jack have typed up his forum post prior to the meeting and then finally posted it after the meeting? Not good enough

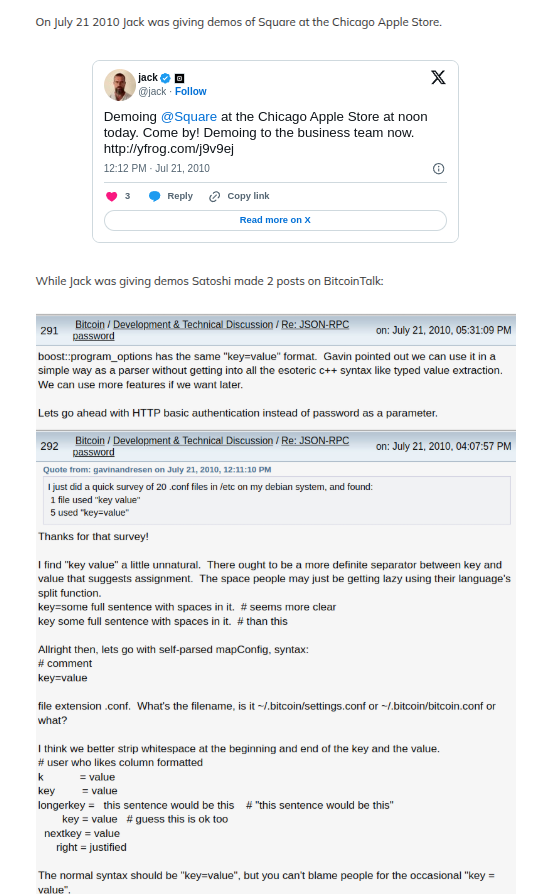

On July 21, 2010, Lopp says that Jack can’t be Satoshi because Jack was at an Apple Store in Chicago where his company was hosting a demo of Square starting at 12 noon all while the forum shows that Satoshi posted at 11:07am and 12:31pm local time that same day. I’m not sure why Satoshi being in a computer store would imply it would be impossible to post a message from a computer or from a phone. The more substantive post of the two that Lopp relied upon was the one that was made an hour before the demo. For this to be a conflict, it would require Jack to literally be doing a Square demo himself during the exact minute of 12:31 when Satoshi posted. Not very good.

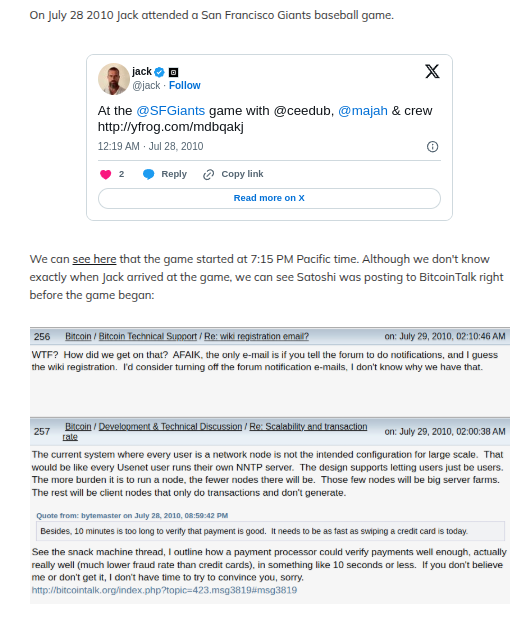

Lopp says that Jack can’t be Satoshi because on July 28, 2010, Jack was attending a baseball game while Satoshi was posting on the 28th. Unfortunately Lopp got the dates wrong. Jack was at the baseball game on the 27th, not the 28th, as evidenced by the 9:19pm PT tweet on July 27, 2010 that he uses as his evidence.

Lopp misread the dates.

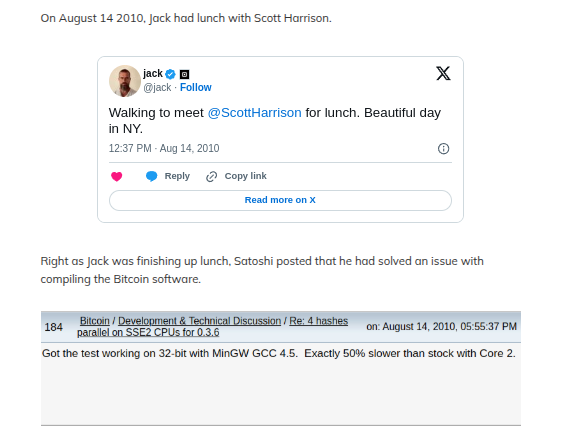

Lopp says that Jack can’t be Satoshi because he tweeted on August 14, 2010 that he was walking to meet with Scott Harrison for lunch and that an hour and 18 minutes later Satoshi posted two sentences on the forum that he had solved an issue with compiling the Bitcoin software. Ok? Which means what? Which means we have to presume that Satoshi had been busy doing this work exactly during the lunch time window and then rushed to post about it immediately to the forum? Satoshi couldn’t have solved it earlier and then posted it on the forum later when he got around to it like right after a lunch meeting? Not very good.

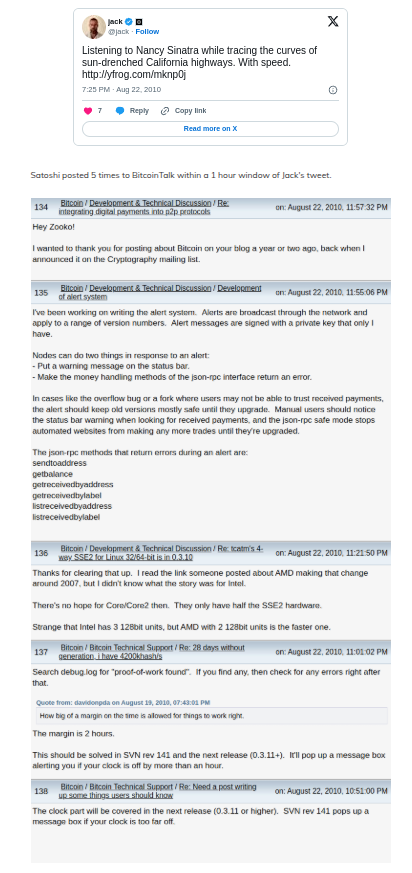

Lopp says that Jack can’t be Satoshi because he tweeted on August 22, 2010 at 4:25pm that he was listening to music while on the highway when Satoshi posted to the forum at 3:51pm, 4:01pm, 4:21pm, 4:55pm, and 4:57pm local time. I like this one to Lopp’s credit because there’s a link in Jack’s tweet to a purported photo of Jack behind the wheel looking out through the windshield. And so the argument here is that Jack can’t be posting to the forum because Jack is too busy driving! But we only know this because Jack is tweeting! And with a photo too? So if Jack is really driving, he is still apparently capable of taking a photo while driving and tweeting while driving, which hurts the case that he couldn’t also be capable of posting to the forum. Or there’s the possibility that someone else was actually driving and he was busy posting to the forum from his phone. Or… that Jack actually made that tweet about being on the highway hours or days after it actually happened. Or it never happened at all and it was online content for engagement or a dream of something nice. But if we give this one the benefit of the doubt and say Jack was really driving at that time, we can’t ignore that the evidence of him driving is a result of him playing on his phone while doing it. These “conflicts” are not very good at debunking Jack as Satoshi because they require leaps of the imagination

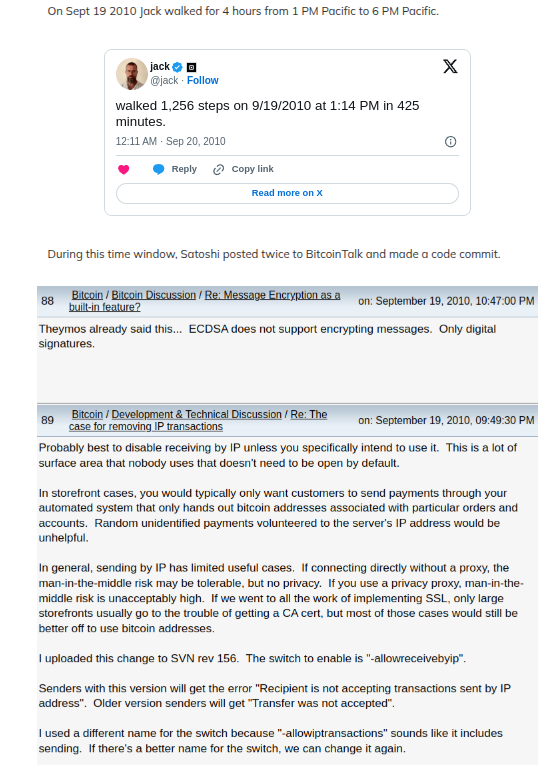

Lopp says that Jack can’t be Satoshi because he tweeted on September 19, 2010 that he walked 1,256 steps in the span of 425 minutes and that Satoshi posted to the forum twice during this time period and made a code commit. I did the math and it seems 1,256 steps is only 0.6 miles and 425 minutes is over 7 hours. This seems to actually support the theory of someone sitting around all day and builds on the case that Jack is Satoshi to make the code commit. Not very good and even supports Jack as Satoshi

Lopp: “I find the aggregate of all the evidence to provide so much doubt that a reasonable person would conclude that it’s far more likely that Satoshi was someone else.”

Counter: Try again.

‘Face-to-Face is a Must In This Industry’: How Julian Hernandez of Idea Financial Earned a Trophy Along The Way

November 24, 2025

“Face-to-face interactions are a must in our industry, and not only through conferences but even though we’re based out of Miami, I’m very familiar with the Long Island Railroad,” said Julian Hernandez, Director of Revenue at Idea Financial.

On multiple occasions, Hernandez has gone from New York City to eastern Long Island and then back again to meet with referral partners. It’s part of his job, meeting face-to-face with ISOs, and working with them to maximize the spread of Idea’s business line of credit products. He says through this experience he’s actually become “best buddies” with the LIRR.

“It’s good for morale, it’s good for relationships. It’s good not only for the reps internally on my end, but I’m sure for the reps on [the ISOs’] end to see and put a face to the lender that they’re always working with,” he said.

Hernandez will go wherever it’s necessary. Just last month that initiative placed him on the opposite side of the country, in a room full of ISOs and competitors that had gathered to play poker on the eve of the big B2B Finance Expo at the Wynn in Las Vegas. For Hernandez, who was born and raised in Colombia and only ever plays poker in a casual setting with friends, he had not gone in with any expectation of winning the friendly tournament. He wanted to network.

“That’s probably one of the main reasons why I wanted to join the tournament,” Hernandez said. “It’s just an opportunity for us, for anyone really that goes to the conference, to connect with either people that they know from the industry, or branch out or meet with new faces in an environment that isn’t so corporate.”

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

While he was happy to earn the rank of #2, it was the social setting of it all that he felt was the best part.

“It’s more of a relaxed environment where people are just having a good time, playing a game, having a drink, and really just getting to know each other on a personal level,” Hernandez said. “That’s the best kind of way to make relationships, right? It’s kind of like when people always say the best kind of business is made on a golf course.”

But in the two days that followed at B2B Finance Expo, Hernandez and the Idea team that was there along with him were in business mode.

“97% of our business is through ISO channels and through all the relationships we’ve established with brokers in our industry, and we’re looking to expand that further,” Hernandez said, noting that there are big growth plans in the works for 2026.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

When deBanked first covered Idea Financial in 2019, Hernandez had not yet joined the company. He came on board the following year during covid and started in an entry level position. He’s since moved up the ranks and now oversees the entire sales and marketing department, which includes anything from ISO relations to marketing. He cites the team and the structure of how it operates as being the key to success. One of the things he first learned when he started was that Idea Financial was always looking to help businesses one way or another.

“I found my way to Idea Financial and have loved it ever since,” Hernandez said.

And while business and networking are important parts of the job, regardless of where that takes him, he is proud of how well he did in that poker tournament at B2B Finance Expo.

“I was happy with my 2nd place trophy,” Hernandez said. “It’s actually right there,” he exclaimed while pointing at it. “It’s back in my office!”

On The Ground at the Lexington Capital Grand Opening Ceremony

November 18, 2025 “Today, I would like to share three stories from my life and the journey of what it took to get here today. The first story is about love and loss. I was lucky. I found what I love to do early in life. That was being an entrepreneur.”

“Today, I would like to share three stories from my life and the journey of what it took to get here today. The first story is about love and loss. I was lucky. I found what I love to do early in life. That was being an entrepreneur.”

So began the speech made by Frankie DiAntonio, the Founder and CEO of Lexington Capital Holdings & Lexington Estates, at the ribbon cutting ceremony for the company’s new commercial property and headquarters in Port Jefferson Station, Long Island.

On the three acre plot with private parking and 16,000 square feet of office space, hundreds of people including 85 employees, their friends, families, and even funding partners, gathered to celebrate the next chapter of Lexington.

“I started my first company when I was 19 years old,” DiAntonio continued. “It was an auto repair shop. I was so excited about it, I told friends, family and the whole entire community. I did not know how to market or generate leads or even how to acquire customers back then.”

Between the live outdoor DJ, a busy food truck operator, and the cacophony of brokers trying to make or close a deal from their cell phone in the parking lot, the activity caught the attention of locals, including a representative from the town’s chamber of commerce who was eager to welcome them.

Between the live outdoor DJ, a busy food truck operator, and the cacophony of brokers trying to make or close a deal from their cell phone in the parking lot, the activity caught the attention of locals, including a representative from the town’s chamber of commerce who was eager to welcome them.

DiAntonio, who actually began the proceedings outside by playing the National Anthem, walked the crowd through his trials and tribulations of entrepreneurship, much of which had humbled him. Lexington Capital Holdings, however, a small business finance marketplace, has been a huge success four years after it started thanks to the people around him.

“Lexington did not get built by me. It got built by us,” DiAntonio said in his speech, “by every person who walked into my life at exactly the right moment, and standing here today opening the doors to this new home, I’m reminded of the biggest lesson the story teaches, the dots always connect, just not always in the moment. They connect when you look back, when you stand somewhere you once dreamed of, you realize every twist, every friendship, every failure, every blessing in disguise brought you exactly where you needed to be.”

DiAntonio attributed much to his sister Nicollete and old friends who are now key operators at the business. Several of them gave speeches.

DiAntonio attributed much to his sister Nicollete and old friends who are now key operators at the business. Several of them gave speeches.

“Working side by side with Frankie truly is a pleasure and an honor, something I look forward to on a daily basis,” said Lexington COO Frank Lewando during his speech. “He’s my best friend, my mentor and my brother, and I’m proud of him for making this big jump and pushing our company to the next level. I patiently wait to see what’s going on next for us. With the opening up of our first commercial property today, we find a new life and direction for the company.”

Inside the building, Lexington is split into different departments. Among others there are separate sales rooms for SBA lending and its new real estate business, Lexington Estates. Purely by observation, the average age of a “Lexonite” appears to be mid-20s. A few of them said off the cuff to deBanked that working at Lexington is the best thing that ever happened to them.

Inside the building, Lexington is split into different departments. Among others there are separate sales rooms for SBA lending and its new real estate business, Lexington Estates. Purely by observation, the average age of a “Lexonite” appears to be mid-20s. A few of them said off the cuff to deBanked that working at Lexington is the best thing that ever happened to them.

When the big moment was coming to an end, DiAntonio cut the ribbon and was presented with a giant gold key and certificate.

“We knew if we worked hard and we stayed true to each other that we would make it,” DiAntonio said in the lead up to the finale. “The first two years were really tough, and we had some really rough days together. Each day was a dog fight to stay in business. I wasn’t concerned about next year, next month or even next week. I just wanted to survive and advance to the next day. By the grace of God and our hard work and efforts, we ended up funding our first deal in our second month, just a domino effect after that. Our second month we funded $71,000. Our third month we funded $193,000. Our fourth month, $400,000 and modern day, we fund nothing less than $15 million every single month for small to medium sized businesses all across the United States.”

How Alexander Klein Took Home the Gold at B2B Finance Expo

November 14, 2025

“I‘ll be honest, I said to one of my co-workers that was there at the conference with us that ‘I’m going to win,'” said Alexander Klein, an ISO Rep at Simply Funding who did in fact win the official B2B Finance Expo 2025 poker tournament. “I said that a little bit facetiously but I think I had a chance.”

Knowing the odds were technically slim and fully cognizant that the annual conference in Las Vegas is really about business in the end, Klein and others made sure to use the opportunity of the poker tournament, at least initially, to socialize with the rest of the table.

“I focused directly on networking with people,” Klein said. “We’re talking sports, talking life, talking business, that was really where it was at the beginning.”

As he started to win some hands and players got knocked out, the tone changed and the table became more quiet and serious. Competitiveness took over. By the end of the night Klein was the last player standing. That made Klein the winner of a 1st place trophy and a B2B gold bracelet. It was his first tournament win and technically the first tournament he’d ever even played in.

Klein learned poker as a teenager and played in a few real games here and there, but that background was apparently enough to beat out some players at the table that played professionally on the side.

“People were immediately coming up to me, saying, ‘wow, I heard you won the poker tournament!’ Guys that were playing, guys that weren’t playing. It definitely got around a little bit and I got some nice connections through it,” Klein said.

And that’s really what it’s all about for someone in his position, the connections made in person.

“Seeing somebody face to face is the most genuine interaction you can possibly have,” Klein said. “You can show somebody that you’re actually serious, that you can actually provide the things that you’re talking about. It’s also just really about building the relationship, and I think you can only do that face to face.”

Klein said that conferences like B2B Finance Expo provide a critical opportunity to meet the right business partners and that it worked well for him and Simply Funding. It was also a good way to get back into the mix considering Klein had taken a hiatus from the industry during Covid and tried a different career path for a few years. Now he’s back. Having worked as a broker previously but working on the funder side these days, he said he appreciates the experience he earned before because he knows what his own ISO clients have to deal with.

One observation he’s made in that regard is that brokers want to see consistency with the funders they work with.

“[Brokers] don’t want to have a deal that is funded in a certain way and then a very similar deal is declined for whatever reason,” Klein said. “They want to see consistency. They want to see consistency in how efficient you are, how fast you respond, and the types of offers they’re getting on certain types of deals, consistency just in all aspects of the job. As long as you stay consistent in this industry, everyone will appreciate what you do, and you’ll also have better relationships and maintain those relationships.”

At Simply Funding, where his job is to bring in new business and work with current partners on deals, he believes they accomplish the consistency element well.

“I just work on helping our ISOs get the best possible deals, best possible offers, make sure everything’s efficient and running smoothly,” Klein said. Speed is also important, he added.

“I just work on helping our ISOs get the best possible deals, best possible offers, make sure everything’s efficient and running smoothly,” Klein said. Speed is also important, he added.

There’s also a mutual respect for the hustle where he says he finds himself and his colleagues working even faster than he had to as a broker to keep up the level of service. And this type of environment is one he wants to stay in for a very long time.

“I have found something that I feel is a great fit for me, that I can do well, and I see myself being able to do this for years to come,” Klein said. “I know there’s a lot of growth opportunity. The industry is only continuously growing, so there’s always more to do. I have that in my mind every single day. There’s always something more I can do. There’s something I can bring to Simply on a daily basis.”

Meanwhile, Klein’s B2B poker trophy currently resides on his desk in Simply Funding’s Jersey City office. He’s confident that it’s just the first of many.

“Shelf is going to go up, and we’re going to hopefully stack [the trophies] up,” Klein said. “That’s the goal.”

‘Like Family’: How Critical Financing Became One of the Fastest Growing ISOs

October 17, 2025When Farmingdale, Long Island-based Critical Financing (CFI) showed up as the 2,671st fastest growing company on the Inc. 5000 list this year, it was a testament to the company’s many years of hard work. Founded in 2017 by its CEO Brandon Garcia, CFI connects small businesses with a variety of unsecured working capital products.

“[Getting that recognition] was great,” said Garcia. “And I think it’s also a testament to the group that we have. It excites the people that work here too. This is a very stressful job, it’s not easy.”

In CFI’s day-to-day, the sales team finds itself competing against multiple companies on almost every deal that comes across their desks. Small businesses regularly put the pressure on them to get the best rate, the fastest funding, or a combination of both. They say this only increases their drive.

“It has definitely helped us in a way,” Garcia said of it. “I mean who doesn’t want a deal that doesn’t have competition, you can kind of take your time with it, right? But I think when there’s urgency, our guys perform better.”

In the very beginning it was just Garcia himself who had worked in the industry since 2012. He was soon after joined by a former colleague, Robert Menzel, and the two set off to really build up a company. That’s easier said than done, especially in a business where trust is paramount. So they looked within their own circle of friends and family to create a solid foundation.

“I felt it was best that we take care of our own,” Garcia said. “Let’s take care of people that we know that are looking for a new opportunity, and we train them the way that we want them to be trained. We want to give that experience and push it over to them.”

Among those they’ve brought on board to their current headcount of sixteen has been Garcia’s own mother, who works as the company’s head processor. And while they are still actively looking to bring on more people, Garcia said that the number of employees isn’t the ultimate metric of success, but rather the abilities of the ones you do have and the relationships they have with everyone else is the key. On this point, CFI is on pace to surpass $100 million in funding this year. It’s because of their continuous progress and results that they finally got the confidence to apply into the Inc. 5000 and were successful in making it.

“To be able to put that Inc. 5000 sticker in your signature, on the website, it just has a different swag to it,” said Garcia’s partner Menzel, “where it just carries a lot of weight, and even the merchants see that.”

When asked if the end goal was to become a lender themselves, both Menzel and Garcia say they’re happy with what they already do now, which is connect the merchants to the most appropriate source.

“While many competitors chase the close, we lead with transparency and real strategy,” Garcia said. “We act as consultants first. Even if a client doesn’t move forward with us, we want them to walk away smarter and more prepared than when they came in.”

“When you are a lender, you don’t really have that close relationship with other lenders because you’re your own lender,” Menzel said. “You’re not talking to them about deals, how to get deals done, ‘what are they doing? What did they change this month compared to what they’ve been doing, what’s working, what’s not.’ I think having those relationships with the lenders and the lenders’ reps, it’s huge and it makes the job fun, because they’re really all great people that we deal with.”

That closeness is what it’s all about for them.

“We are a group of people who genuinely care about each other,” Garcia said. “We’ve celebrated marriages and welcomed new babies. We hang out on weekends, show up for one another, and create a work environment that doesn’t feel transactional.”

The outcome of that are months where the company is exceeding $10 million a month in funding, and they’re now even more fired up after the Inc. 5000 placement.

“You don’t need this massive shop to be successful in this industry,” Garcia reiterated. “It’s really that simple. You just need the right people. You need to be loyal and just really be truthful with everyone. And good things happen. That’s a big thing for us.”

That Fintech Business Loan Performance Should Help You: How Hansa is Giving Both Borrowers and Lenders a Powerful Tool

October 15, 2025“Business owners want to be reported on,” said Henry Magun, founder and CEO of Hansa. “When we do a lot of surveys around this and when we survey small business owners en masse, would they rather borrow from a provider that does report to the business credit bureaus or does not, 85% of business owners say that they would rather borrow from a provider that does report to the business credit bureaus.”

It’s a familiar story: small business borrows from a fintech lender, repays it perfectly, and later on down the road applies for financing elsewhere believing that their previous payment history will support an approval or more favorable terms, only to find out there’s no public record of it at all.

“We hear that all too often,” said Magun. “It’s a very common experience, and that is one of the reasons why we are extremely focused on not only building the back-end pipes to do the furnishment to the bureaus for the lenders and make that process effortless, but also creating a front-end product that makes it a transparent process for the SMBs.”

Hansa, headquartered in New York City, enables lenders to report payment history to the credit bureaus and access existing reports on their customers. The key here is that it’s business credit reporting, not personal. Although most people are familiar with Dun & Bradstreet, Experian and Equifax also have business bureaus specifically for business credit. There’s also consortium-based organizations such as the Small Business Finance Exchange, for example, that take in commercial credit data.

While term loans and cards for SMBs, two rapidly growing products in the fintech space, are their main focus, the Hansa platform can make reporting possible for just about anything.

“We realize that there is such a diversity of product-type in the SMB financing space,” Magun said. “Is it a term loan? Is it a card? Is it an MCA product? You know, are there daily payments, weekly payments, monthly payments? All across the board, we do it all.”

The benefits of reporting business credit are obvious. Lenders can claim that good performance will legitimately build business credit, borrowers benefit from actually building business credit, and lenders can rely on this highly relevant data to drive more informed decisions.

“It’s really about getting the fintech ecosystem towards the future in which companies are focused on supporting financial wellness, and we really view credit furnishment in the SMB space as core to that, ultimately being able to reliably build credit is extremely important for financial mobility, economic mobility because it enables people to [graduate] to bank products and things like that, and being able to take your history with you in order to progress. That’s really important for economic mobility.”

On the flipside, for lenders that have spent years fine-tuning algorithms to predict payment performance outside of traditional credit reports, one area that continues to remain cloaked in obscurity is payment performance with other fintech lenders. Alternative methods, at least within the fintech community, are commonly used to make a best-guess effort, such as employing automated tools to scan an applicant’s bank account deposits with a known list of lender names and then matching them to corresponding bank debits to predict the performance and status of those accounts. But even if one can assess with a high degree of confidence about how those credit lines are performing, it’s not exactly an official affirmation from the lender, and the transaction history might not go far back enough. Besides, these risk assessment methods are entirely personalized to the lender, and don’t necessarily give the business an asset (a universally recognized credit report), that it can furnish elsewhere and benefit from. A business could use a credit report for a trade line or a bank loan or in some other transaction where it could hold weight for them, for example.

On the flipside, for lenders that have spent years fine-tuning algorithms to predict payment performance outside of traditional credit reports, one area that continues to remain cloaked in obscurity is payment performance with other fintech lenders. Alternative methods, at least within the fintech community, are commonly used to make a best-guess effort, such as employing automated tools to scan an applicant’s bank account deposits with a known list of lender names and then matching them to corresponding bank debits to predict the performance and status of those accounts. But even if one can assess with a high degree of confidence about how those credit lines are performing, it’s not exactly an official affirmation from the lender, and the transaction history might not go far back enough. Besides, these risk assessment methods are entirely personalized to the lender, and don’t necessarily give the business an asset (a universally recognized credit report), that it can furnish elsewhere and benefit from. A business could use a credit report for a trade line or a bank loan or in some other transaction where it could hold weight for them, for example.

“It really is a ‘rising tide raises all ships’ scenario in the sense that in a more mature ecosystem where there’s higher ubiquity of reporting, everyone benefits,” Magun said. “It helps all the funders and creditors on their underwriting processes, and it helps the business owners, the applicants, because it increases the portability of your credit history.”

The usefulness speaks for itself. Hansa, for example, has increased the number of reports that they’re furnishing data on by more than 400x since the beginning of this year. And the lenders can show off to their borrowers what they’re reporting and where it’s being reported to in any manner they wish.

“We’ve started to see really great traction amongst these various players, and we’re really excited to be working with them and it works,” said Magun.

Already they are seeing improved payment rates and increased engagement rates between the borrowers and lenders.

“It’s really powerful,” Magun said, “and SMBs really do care about being able to build their credit.”

How Kaaj is Accelerating Small Business Lending

October 8, 2025Utsav Shah first met Kristen Castell at deBanked CONNECT MIAMI this past February. At the time, Shah and his partner Shivi Sharma were freshly promoting a new AI technology to simplify small business lending. It’s called Kaaj, described as a core intelligence layer that bolts into a lender or broker’s CRM and handles all of the early-stage application intake and underwriting work. Shah had been familiar with the fintech accelerator Castell directs, the Center for Advancing Financial Equity (CAFE), which she was speaking about at the conference, but he had never actually met her in person until then.

“That’s really when we learned deeply about what CAFE’s mission is and how it works with a lot of startups, a very unique mission and very unique approach to work with startups and bring the ecosystem together,” said Sharma. “So we loved it and decided to apply this Fall.”

They applied into the exclusive accelerator program and were one of six companies to be selected, an honor considering hundreds of companies apply for entry on a bi-annual basis. As previously noted on deBanked, it’s an eight-week program, some of which takes place on location at the Fintech Innovation Hub on the University of Delaware campus. The rest is virtual but there are in-person field trips like a recent one to Washington DC, for example. deBanked has sponsored the last three accelerator cohorts which in the most recent cohort includes headline names like JPMorgan, PNC, Discover, Barclays, Capital One, M&T Bank, WSFS BANK, BNY Mellon, Prudential, Fulton Bank, County Bank, Best Egg, United Way, NeighborGood Partners, and the Delaware Bankers Association.

Kaaj, based in San Francisco, was already getting noticed beforehand. The company won the Fintech Meetup Startup Pitch Competition in March and secured a $50,000 prize, for example. Their technology is especially suited for equipment financing companies, MCA providers, small business lenders, SBA lenders, factors, and more.

Kaaj, based in San Francisco, was already getting noticed beforehand. The company won the Fintech Meetup Startup Pitch Competition in March and secured a $50,000 prize, for example. Their technology is especially suited for equipment financing companies, MCA providers, small business lenders, SBA lenders, factors, and more.

“So imagine that you’re a lender, and you get hundreds of applications in a day, and you don’t really know where you want to focus your time on,” Shah said to deBanked. “‘What do these 100 deals mean for me, for my business? Are they even qualifying against my criteria, etc.’ So what Kaaj does, it provides very quick intelligence, within the first three minutes.”

Shah explained that as soon as someone submits a package with documents, they get analyzed from top to bottom, like KYC/KYB, the bank statements, and more. This helps lenders (and brokers) decide how to prioritize their time. Utsav’s background in technology has played a major role in building this out as he comes with a decade of AI experience and was building autonomous cars before building Kaaj.

“Time wins deals or time kills deals,” said Shah. “Either way that you want to look at it, if we can give that time back to them, if we can reduce that turnaround time on each individual deal and focus on those higher profitability deals for these companies or these lenders, then they can start really feeding the top line and the bottom line, because they’re not having to hire a bunch of folks.”

Sharma said that equipment finance is slightly more complex than MCA, for example, but that as a $1.4 trillion industry, it’s a market that’s ripe for innovation. Sharma used to work in commercial lending herself and has seen firsthand how manual processes and outdated technology slow things down and hurt not only the lenders but the borrowers in the process.

“I have worked on small business lending, commercial lending, payments fraud, onboarding fraud, a lot of that,” Sharma said. “I spotted a lot of challenges in that space and a clear lack of good technological solutions that really help these lenders scale efficiently.”

Shah, meanwhile, said that ultimately it’s about helping the end-user, the business borrower.

“We are very focused on solving for small businesses, because the final mission of the company is to get better access to capital for small businesses,” he said.

The Great Concession, How the MCA Product Effectively Proved It Was Right All Along

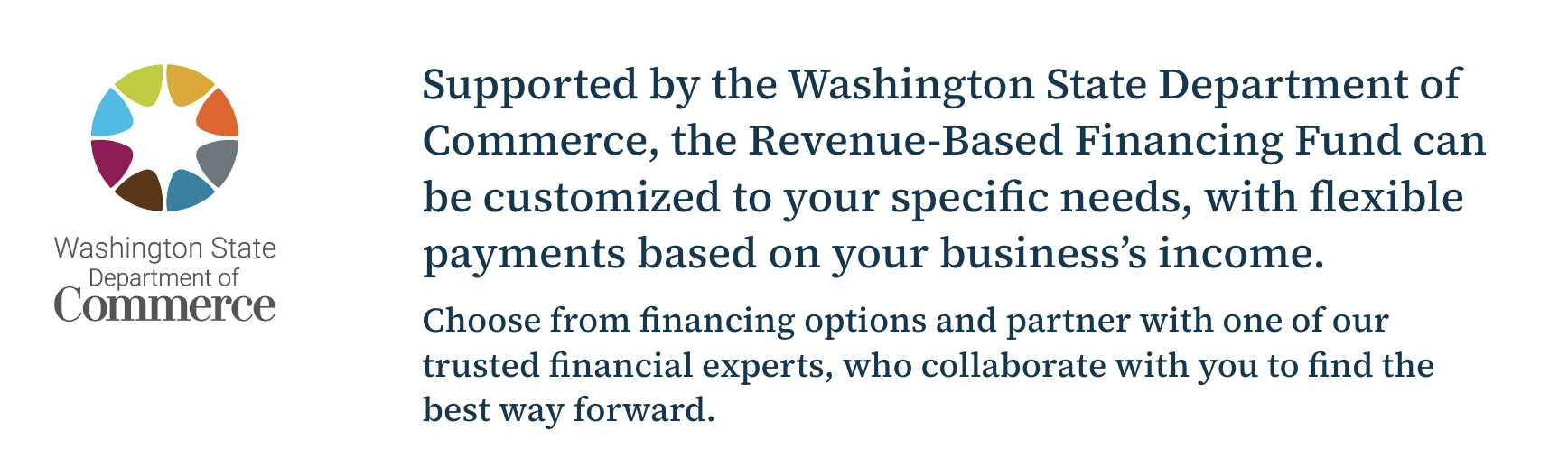

September 26, 2025 There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

How did these states reach the opposite conclusion?

There’s no caveat to how the Washington State program works. The State’s Department of Commerce partnered with Grow America and the operation is backed by a federal grant (SSBCI-21031-0048) to roll out and administer a revenue-based financing program as part of Washington’s State Small Business Credit Initiative. It’s sales-based financing or in this case revenue-based financing (which is the more common phrase these days). Grow America’s revenue-based financing program utters a very familiar phrase in its marketing.

“The months you generate more revenue, you pay a higher amount, when business is slower you pay less,” the company advertises.

This was at one time the signature calling card of a merchant cash advance, but now such features have been repackaged and rebranded into something similar but different, and everybody is doing them.

The Grow America program applies a 20% holdback on adjusted monthly revenue and requires a minimum monthly payment of $1,000 if the 20% holdback does not generate at least $1,000 for the month. Merchants can get approved for anywhere from $50,000 to $1 million. The product is marketed as having a 1.24 factor rate and an estimated 14.27% APR with a 3-year term. As industry participants are aware, increasing sales would translate into increasing payments, which means a rapidly paid off loan could potentially result in a final outcome APR in the triple digits, far and away from the “estimate.”

The irony is that the notable benefits of a similar product, merchant cash advances, which have no minimum monthly payments, no fixed term, and are not absolutely repayable, are eliminated when restructured in this way and presented as “revenue-based financing loans.” Revenue-based financing loans take the underlying structure of MCAs (payments tied to sales) and then strip away the benefits. However, when structured as loans, the argument often goes that they are likely to be cheaper, which may be true on average, but is not always true.

Indeed, Grow America leads specifically with price as for why its product, similar to its privately owned competitors, are the better option:

“There are a lot of online lenders offering revenue-based loans that promise instant approvals, but their terms are intentionally confusing, and the fees are high,” Grow America advertises. “Our lenders aren’t like that. They’re mission driven.”

In Texas, the author of the bill that banned debits from such financing providers “informed the [legislative] committee that commercial sales-based financing has become a popular financing option for small businesses desperate for credit and that, unlike traditional loans, this type of financing is repaid as a percentage of future sales or revenue.”

Indeed, it is very popular. The largest providers or brokers of such financing today whether structured as a purchase or loan, are household names like Amazon, Walmart, Shopify, Intuit, Stripe, DoorDash, PayPal, Square, GoDaddy, Wix, Squarespace and more. Some structure them as a purchase and call it a merchant cash advance and some structure it as a loan and call it revenue-based financing. In either case, payments are tied to the percentage of future sales or revenue.

In egregious cases of wrongdoing one way or another, such incidents have historically been a result of deceptive marketing or payments from a merchant exceeding the contracted amount. In New York, when transactions are structured as a purchase, courts generally look to make sure that the agreements have a reconciliation provision in the agreement, whether the agreement has a finite term, and whether there is any recourse should the merchant declare bankruptcy. Legally speaking, the products have become pretty well defined and understood in the court system.

Like Washington State, GoDaddy, which recently announced its new merchant cash advance program, markets its product in an almost identical fashion.

“If your sales go up, the MCA will be paid sooner; if the sales are slow, it’ll take longer,” GoDaddy says.

Same message.

Washington State requires merchants to make a minimum payment every month and a balloon payment if not fully repaid within 3 years. GoDaddy, by contrast, advertises no minimum payment amount, no set payment schedule, no penalties, and no late fees. One’s a loan, one’s a purchase.

While the best course of action is best left to the merchants, there appears to be a near-universal concession that the underlying nature of how merchant cash advance agreements were contemplated, payments tied to sales, made strong logical business sense all along. Washington State emphasizes this fact.

“We know that your business has its own needs and loans with fixed payment amounts may not be the best option for you,” they advertise. “The revenue-based financing fund offers loans with flexible payback terms so you can grow your business immediately and pay back your loan based on your varying revenue.”

Recent studies also now highlight the benefits of cash-flow-based underwriting.

In Sharpening the Focus: Using Cash-Flow Data to Underwrite Financially Constrained Businesses, “The paper finds that adding cash-flow information substantially increases the predictive signal of models that rely primarily on the business owners’ personal credit scores and firm characteristics.”

There’s also Square, the largest revenue-based financing provider in the US, that has explained why this system just works better. Square says that they can fund more businesses and have higher payment success rates than if they were to follow more conventional methods of underwriting and repayment.

“Square Loans addresses [the credit] gap by using near real-time business data to assess creditworthiness, evaluating metrics such as transaction volume and revenue patterns to offer short-term loans — with repayment on average in 8 months,” Square wrote in a White Paper. “This allows for a more accurate and timely understanding of a business’s capacity to borrow and repay. And loan repayments are higher during periods when business is stronger and reduced when sales are lower.”

What’s the sentiment these days on payments tied to sales revenue? The market has spoken.