Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Small Business Finance Industry is BACK

June 21, 2021 The industry is back. I say this while sitting in a Miami hotel, my third such trip to Florida since becoming fully vaccinated against Covid in May.

The industry is back. I say this while sitting in a Miami hotel, my third such trip to Florida since becoming fully vaccinated against Covid in May.

There’s a lot of action going on. I’ve sat down in multiple broker shops in both New York and Florida and the phones are ringing off the hook.

The demographic of the average customer in the post-covid recovery seems to vary. Some say the credit quality has gotten better, others have said it’s worse. Some merchants have become used to forgiveable loans and low APR financing while others appear willing to take capital at any price just to keep up with the pace of their growth. It’s one of those things where everyone is just trying to adjust to the new normal, even if there’s little consensus as to what that is.

In New York City, the return of packed bars and overflowing restaurants stands in stark contrast to the rows of abandoned stores and For Lease signs that dot the landscapes around them. And yet if one looks past all that, the only reminder that Covid was ever even there is the requirement that one still wear a mask on the subway even if they’re vaccinated.

In Florida, it’s the opposite. I recently got yelled at by a bus driver for wearing a mask in the first place.

The broker shops I’ve visited still had office space that were filled with teams that were more than happy to be occupying them in person. But at the same time, the industry has become extremely popular with the traditional work-from-home crowd.

Leo Kanell’s 7-day marathon challenge on facebook draws in more eager industry participants than I would’ve ever thought possible, an accomplishment I know to be true because I dropped in on him unannounced late one friday night while he was live.

Similarly, Oz Konar, who I did a livestream interview with in person, has trained more than 3,000 brokers in the industry, many who work for themselves from home.

We’ve also been very busy in the last couple months and have met a lot of brand new entrants on both the funding and broker side.

All this activity is setting the stage well for Broker Fair 2021 on December 6 in New York City. It is perfectly timed to discuss the new disclosure law that goes into effect in New York on Jan 1, 2022, one that is so consequential that at least one company has relocated to New Jersey.

What a time to be in the industry!

Mexican Small Business Lender Buys a Bank, Eyes United States

June 18, 2021 Change is happening south of the border. Online lenders and alternative funders are growing across Mexico much the same way as elsewhere. This week, Credijusto, an online small business lender based in Mexico City, acquired Banco Finterra, marking the first time that a fintech has acquired a bank in the country.

Change is happening south of the border. Online lenders and alternative funders are growing across Mexico much the same way as elsewhere. This week, Credijusto, an online small business lender based in Mexico City, acquired Banco Finterra, marking the first time that a fintech has acquired a bank in the country.

According to Reuters, “Credijusto aims to ramp up services for Mexican companies that sell to the United States, and build a business for U.S. companies that do cross-border trade in Mexico and beyond in Latin America.”

Mexico also has more than 6 million small businesses, a market that is effecively 4-6x larger than Canada’s.

Prior to this, Credijusto had already collectively raised $400M from Goldman Sachs, Credit Suisse, Point72 Ventures, New Residential Investment Corp., Kaszek, QED Investors, John Mack, Ignia, Promecap and LIV Capital.

“The acquisition of Banco Finterra seeks to create the first truly digital banking platform for Mexican companies in the future,” commented Allan Apoj, co-CEO of Credijusto. “This transaction marks an important milestone in Mexico and the region, and we are proud to be revolutionizing the future of banking in Latin America.”

Apoj’s partner, co-CEO David Poritz, hinted to Reuters that in a couple of years it may consider the acquisition of an American bank as well.

Earlier this year, Mexico began to allow fintech companies to obtain a Financial Technology Institution license.

Estamos muy orgullosos de revolucionar el futuro de la banca en México con la adquisición de Banco Finterra y de beneficiar así a las empresas a través de productos financieros de nueva generación. Conoce más de este gran logro: https://t.co/pbGBVyo04p pic.twitter.com/A32vaHDOB1

— Credijusto (@credijusto) June 15, 2021

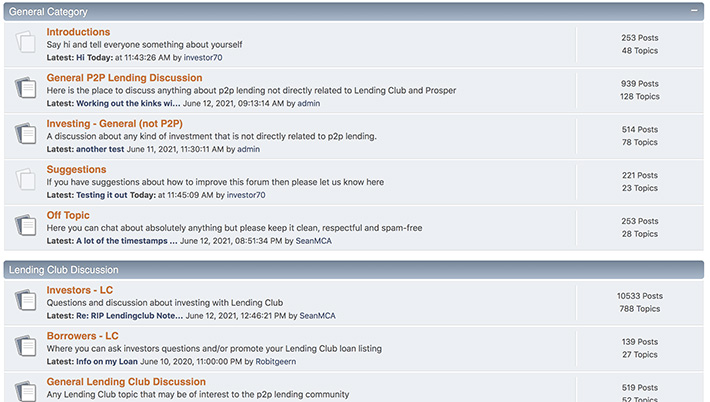

LendAcademy P2P/Investor Forum is Returning

June 14, 2021Update 6/19/25: This forum has migrated to DailyFunder

The P2P Lending/Investor Forum formerly at LendAcademy.com is coming back!

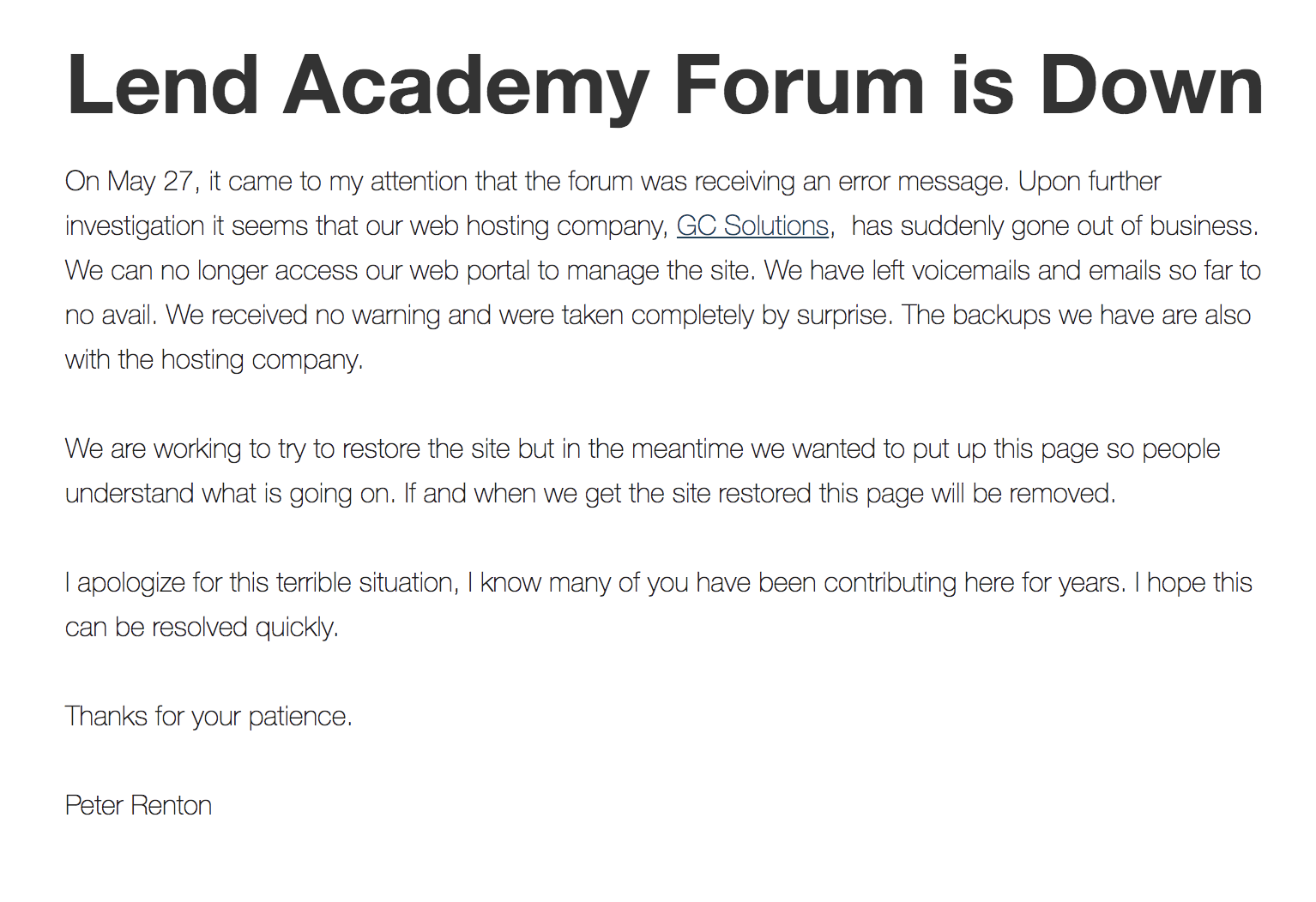

In late May, the online forum at LendAcademy.com went offline. Soon after, the forum URL was redirected to a note from the company that said the server hosting the data was no longer accessible.

In late May, the online forum at LendAcademy.com went offline. Soon after, the forum URL was redirected to a note from the company that said the server hosting the data was no longer accessible.

“Upon further investigation it seems that our web hosting company, GC Solutions, has suddenly gone out of business,” they wrote. “We can no longer access our web portal to manage the site. We have left voicemails and emails so far to no avail. We received no warning and were taken completely by surprise. The backups we have are also with the hosting company.”

With the data seemingly permanently lost, deBanked acquired the rights to it last week (just the forum), with the hope that some proprietary methods of forensic recovery would be successful. A significant portion of the forum has since been restored, hosted now at https://dailyfunder.com/forumdisplay.php/50-Peer-to-Peer-Lending-(Legacy).

It is still a work in progress. There are still formatting issues and a number of missing posts. Passwords were also lost. If you were a user on the forum and wish for your account access to be restored, you must email us at info@debanked.com.

Thank you for your patience.

The original post announcing the loss:

deBanked Celebrates 4,000 Days Since Inception

June 13, 2021

It’s been 4,000 days since deBanked first came online as a blog, originally as MerchantProcessingResource.com in 2010.

I did not anticipate on Day 1 that I would still be here more than 10 years later, but here I am!

Thanks to everyone that has been reading, watching, following along, and attending our events. It has made the journey thus far very enjoyable.

I look forward to seeing you all again in person at Broker Fair 2021 in New York City.

FTC Tries Hand With Gramm-Leach-Bliley

June 7, 2021 Following a pivotal loss of power for the FTC, the agency is hoping for a do-over on at least one case it had originally brought under Section 13(b). In FTC v. RCG Advances, et al, the FTC filed a motion to amend the complaint it had originally brought in June 2020 to include new claims under Gramm-Leach-Bliley. Without doing this, the original case was essentially doomed, thanks to a recent SCOTUS decision.

Following a pivotal loss of power for the FTC, the agency is hoping for a do-over on at least one case it had originally brought under Section 13(b). In FTC v. RCG Advances, et al, the FTC filed a motion to amend the complaint it had originally brought in June 2020 to include new claims under Gramm-Leach-Bliley. Without doing this, the original case was essentially doomed, thanks to a recent SCOTUS decision.

Such claims could be pursued criminally but the DOJ informed the FTC that it did not wish to involve itself in this matter.

The FTC filed its motion to amend on May 14th.

Unsurprisingly, the defendants are unhappy by the sudden divergence of claims.

“If the FTC had a credible cause of action against the Defendants under the Gramm-Leach-Bliley Act, 15 U.S.C. § 6801 (the “GLB Act”) it was incumbent upon them to propound it a year ago when they initiated this action – not now amid the disingenuous pretext that they just purportedly realized it,” they wrote in a response to the motion.

Defendants argue that as a 13(b) case, over 50,000 pages of documents had already been exchanged in discovery and more than two dozen subpoenas issued.

“Despite the sheer volume and nature of such discovery already conducted in the instant matter, granting the FTC leave to amend the Complaint would essentially trigger a reset of the entire case,” they say.

They have asked for the Court to deny the FTC’s motion to amend at this late hour.

Live Stream With Oz Konar

June 2, 2021I will be speaking with Oz Konar, the founder of Business Lending Blueprint, at 12:15pm ET on deBanked TV.

Konar teaches people how to build successful home-based businesses in the alternative finance industry and has a highly popular youtube channel.

Tune in at 12:15 on deBanked TV.

The Mayor of Miami is Hosting a Crypto Conference

June 1, 2021Miami Mayor Francis Suarez has embraced crypto so completely that he’s hosting his own crypto conference on Wednesday, June 2.

Tomorrow I’m hosting my very own Crypto Conference with some of the top players in the DeFi space.

Use the link below or tune into Channel 77 to get in on the action🚀 https://t.co/QnmNa0WxKl pic.twitter.com/N8GSR2UPSa

— Mayor Francis Suarez (@FrancisSuarez) June 1, 2021

The mayor regularly shares photos with crypto executives on social media and his own city government website biography includes a section dedicated to the Bitcoin White paper. The Miami Heat’s home stadium is even being rebraned to the FTX Arena, named after a cryptocurrency exchange (which oddly cannot be accessed by US residents).

The mayor regularly shares photos with crypto executives on social media and his own city government website biography includes a section dedicated to the Bitcoin White paper. The Miami Heat’s home stadium is even being rebraned to the FTX Arena, named after a cryptocurrency exchange (which oddly cannot be accessed by US residents).

Suarez’s June 2nd conference will be 100% virtual and FREE.

In the three days that follow, the largest ever in-person Bitcoin conference will take place at the Mana Convention Center in Miami’s Wynwood neighborhood.

It’s not just crypto. Suarez has been heavily accommodating to the tech and finance industries with the hope that they might relocate their businesses to Miami.

In that vein, deBanked sat down with the mayor in person back in March.

Kabbage Spotted in American Express Cardholder Dashboard

May 27, 2021 American Express business cardholders may be seeing a notification from Kabbage in their online dashboards. This writer did today.

American Express business cardholders may be seeing a notification from Kabbage in their online dashboards. This writer did today.

“Introducing Kabbage®, now an American Express company. Streamline your business banking with Kabbage Checking™ and earn 1.10% APY on balances of up to $100,000, with no monthly maintenance fees. It’s digital checking for the way you work today. Terms apply. Learn More.”

The Learn More link goes to the Kabbage website where users can apply. The product itself may not be ready yet however, as clicking the application link tells users that they can join the waitlist because they’re “not currently accepting new customers.”

The rollout is consistent with statements that American Express has made about Kabbage’s role in the company.