Articles by deBanked Staff

Broker Fair’s 2026 Conference Beats All Previous Shows in New York City

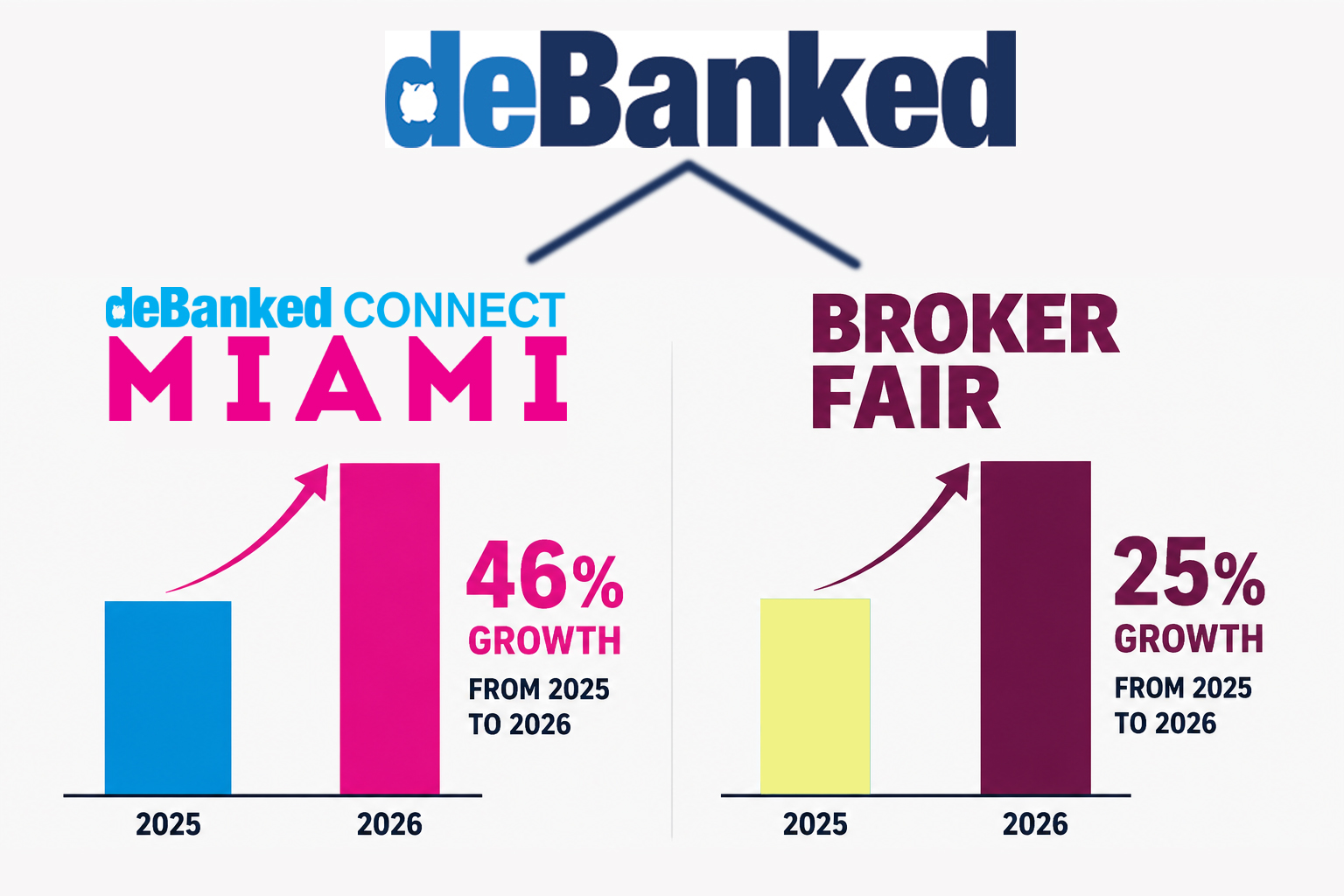

June 2, 2026The industry is full of life! deBanked’s first two conferences of 2026 have set all-time records for tickets. deBanked CONNECT MIAMI grew by 46% year-over-year while Broker Fair in New York City grew by 25%. More than 50% of attendees to this year’s Broker Fair had never attended Broker Fair before in the past despite the annual event having already run for 9 straight years.

The next deBanked affiliated conference, B2B Finance Expo, takes place October 19-21 at the Cosmopolitan of Las Vegas in collaboration with the Small Business Finance Association.

New Faces at Broker Fair 2026

May 30, 2026More than 50% of all ticket-holders registered for Broker Fair on June 1st have never attended Broker Fair in New York City previously. The small business finance conference, which launched in 2018 and has taken place every year in New York since, will therefore bring out a lot of new folks to connect with.

Broker Fair’s agenda can be found here.

Last minute ticket-registration (subject to remaining availability) can be found here.

Broker Fair Preshow Party On Pace for Largest Ever

May 28, 2026Broker Fair’s pre-show event taking place in New York City at Hudson Vu on Sunday, May 31 from 7-9pm (and sponsored by Lendini!) is on pace for the largest turnout in the nine-year history of the tradition. The previous record for pre-show registrations was set in late 2021 at the industry’s first in-person event after a 23 month hiatus due to covid.

Because the pre-show is expecting a large crowd, make sure you have the special pre-show ticket ahead of time since the space could completely sell out. You can order them through the normal registration process here.

MCA Debt Settlement Owner Pleads Guilty to Conspiracy To Commit Wire Fraud

May 27, 2026 The 2024 arrest of Mark Csantaveri, an MCA debt settlement owner tied to MCA Cure LLC, LDMS Group, LLC, and Evergreen Settlement Group LLC, has resulted in a guilty plea. Csantaveri pleaded guilty to conspiracy to commit wire fraud.

The 2024 arrest of Mark Csantaveri, an MCA debt settlement owner tied to MCA Cure LLC, LDMS Group, LLC, and Evergreen Settlement Group LLC, has resulted in a guilty plea. Csantaveri pleaded guilty to conspiracy to commit wire fraud.

In the original charges, investigators said that Csantaveri’s debt settlement websites made claims that they had a “proven proprietary debt restructuring system” that could lower their MCA payments by 80%. As part of the enrollment process, merchants were directed to send funds to an escrow account, where the defendant then misappropriated the funds by transferring them to personal accounts.

Csantaveri is facing up to a statutory maximum of 20 years in prison and has agreed to forfeit the criminal proceeds of $2 million.

deBanked first reported on this case in May 2024.

QuickBooks Capital: ~$1.7B Funded Last Quarter, Repeats that AI is Not a Threat, But Rather an Advantage

May 21, 2026 Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Like other software companies, analysts have been questioning the sustainability of their product offerings as AI looms large as a threat. Like the previous quarter, Goodarzi offered a rebuttal on this subject, expressing that they are effectively the AI solution customers would seek.

“It is important to recognize that businesses, while they use Google, they use LLMs to do searches, do queries, you cannot run your business with an LLM because you are managing your books, you are managing your money, you are managing your payroll, and accuracy and compliance of doing that matters,” Goodarzi said. “And running a business is mission critical. And so psyche of businesses is such that and accountants is that they need us to be their AI platform to provide expertise so they can run and grow their business.” Goodarzi cited Anthropic and OpenAI as partners they are already working with, for example.

Goodarzi also said that winning customers is not necessarily about the best software anyway, but rather about the confidence the assistance with the work instills in the customer. And given the integrations they have, the reputation they have, the AI power that they use, and ability to assist customers, this is where they are actually structurally advantaged.

Deep Search, Merchant Lawsuits, and More

May 19, 2026 The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

QuickVett will spare you the trouble and cut right to the chase. That lawsuit? A dispute over $3k that happened at the tail-end of a large $100k deal. The outcome? A satisfied settlement. It’ll all be right there in its report. No manual lookup on the case required. QuickVett, which describes itself as a merchant intelligence platform, scans state and federal court records across the US. If there’s a hit involving an MCA it will use an MCA-specific AI analysis to present relevant details to an MCA underwriter. An immediate default is distinguishable from one that happened after a long lengthy relationship, for example. Maybe a conflict arising after the 7th renewal provides clarity that otherwise wouldn’t be readily obvious. Most underwriters are already familiar with NYSCEF but if the deal is not in the New York State court system, it’s not going to be found. QuickVett says they’ll find it wherever it is.

QuickVett also does creative searches on its own, such that it will discover if the merchant’s DoorDash account or e-commerce site has gone offline, for example, or if employees of the business recently updated their LinkedIn accounts to say that they no longer work there. QuickVett also pays special attention to the corporate structure and job title of the officers. For example, in an impromptu trial afforded to deBanked for test purposes, QuickVett’s deep search system discovered a sworn affidavit filed by a business owner in an old court case and compared what he said to public records and his LinkedIn profile about his role in the business. The result was that everything matched. But if it hadn’t, an underwriter might have to contend with why a business owner swore he had partners in an obscure court case but listed himself as the 100% owner on a funding application and proceed accordingly.

Overall, “QuickVett scans court records, background databases, corporate filings, social media, and the web — delivering a complete merchant intelligence dossier in under 5 minutes,” the company states. Its AI systems custom tailor the findings to an MCA-style underwriting process.

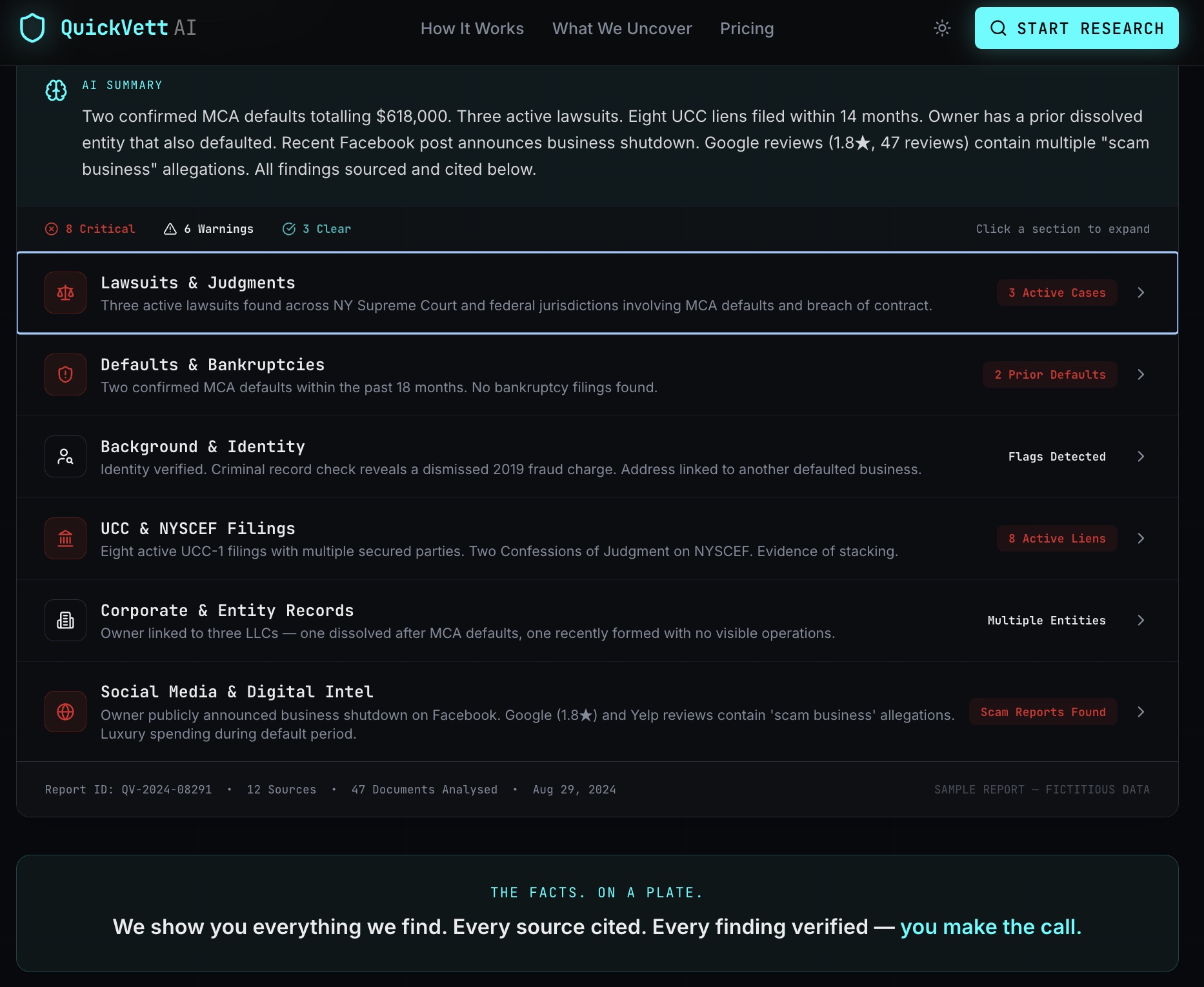

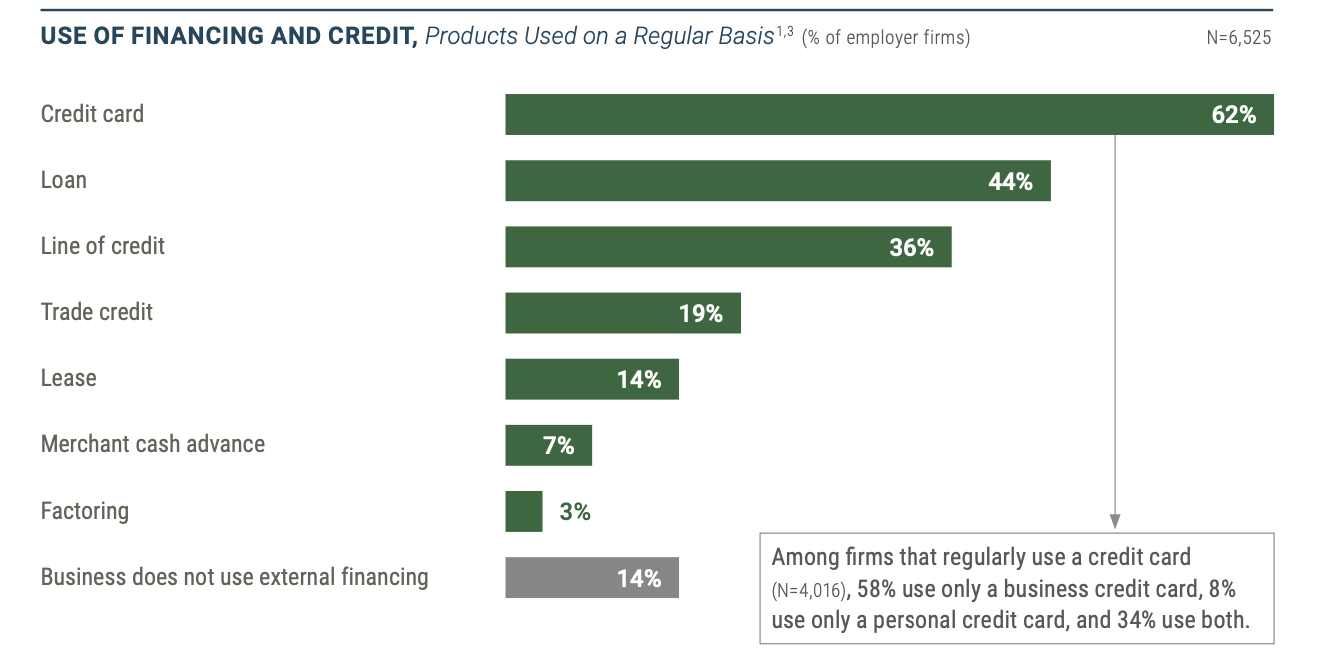

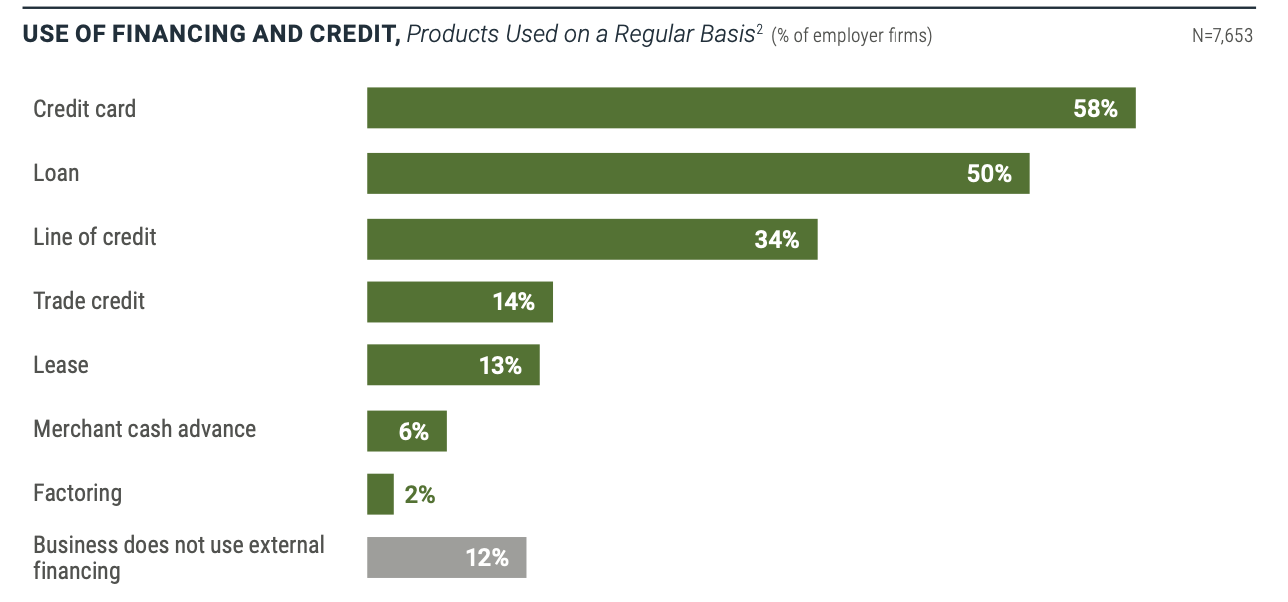

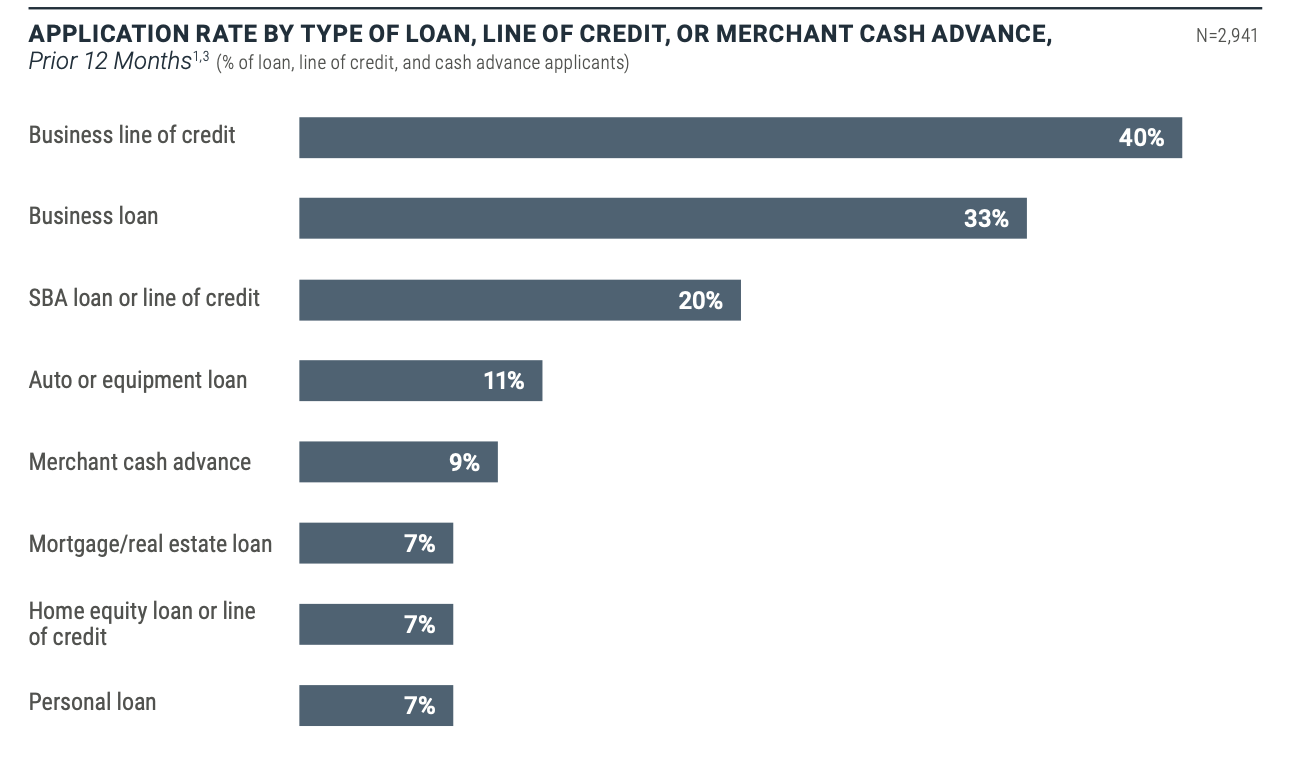

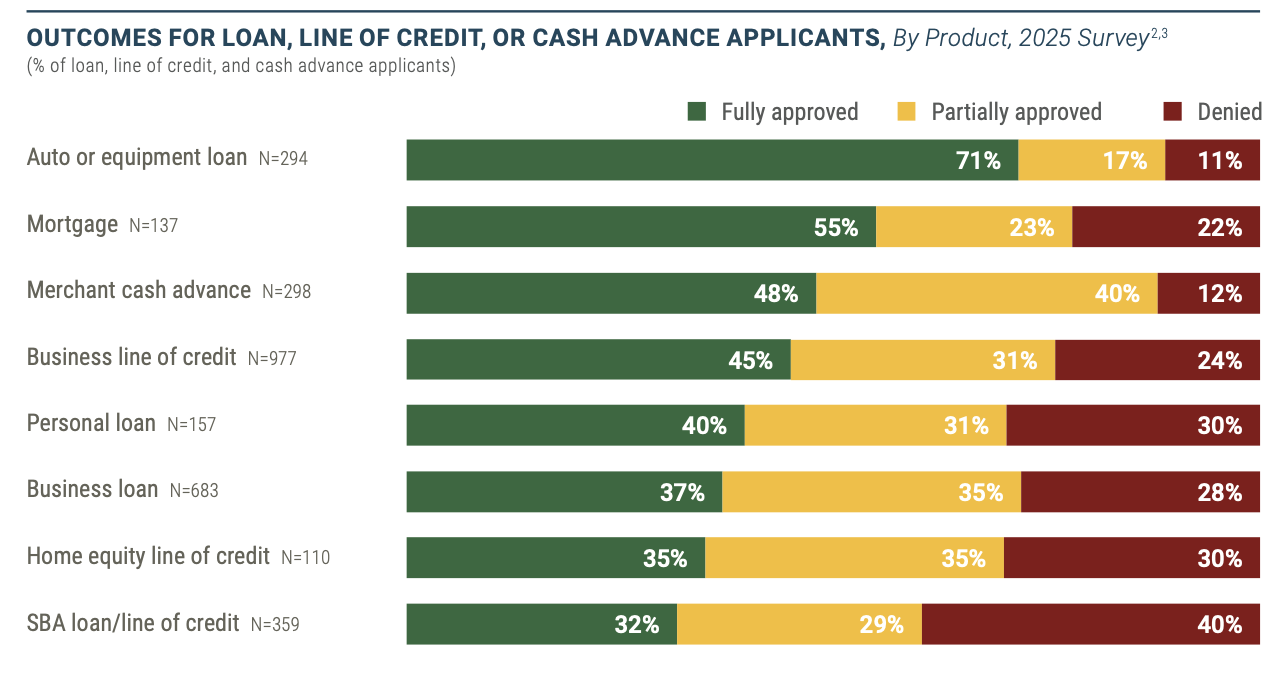

Seven Percent of Small Businesses Use MCAs on a Regular Basis

May 15, 2026According to the latest Small Business Credit Survey taken by the Federal Reserve, 7% of businesses with less than 500 employees use merchant cash advances on a regular basis. This was up from 6% the previous year.

For businesses that applied for financing, 12% applied for an MCA, up from 9% the previous year. Forty-eight percent of those applicants said that they got fully approved for one and 12% said they were declined. This contrasts with last year’s figures of 33% and 9% respectively. These charts are compared below while the full 2026 survey report can be viewed here.

It should be noted that the 2026 data reflects a survey conducted from September 2025 – November 2025 for that trailing 12 month period and the 2025 data reflects a survey conducted September 2024 – November 2024.

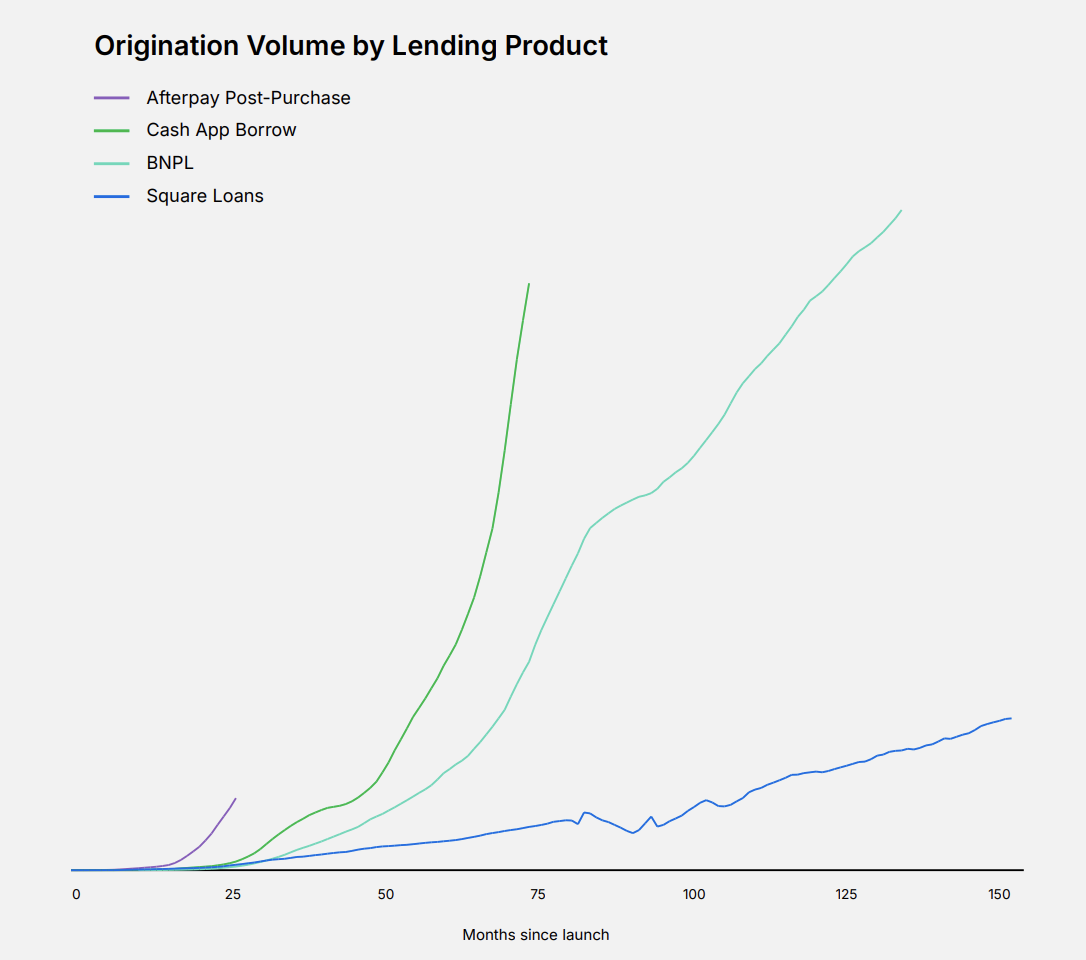

Square’s Q1 Gross Profit Growth Driven by Square Loans

May 12, 2026Block didn’t divulge the precise number of business loans it originated in Q1 2026 but did say that it grew. deBanked, which tracks online small business lender originations, estimates the number to be ~$1.9B.

“Square gross profit grew 9% year over year in the first quarter, driven primarily by Financial Solutions, most notably Square Loans,” the company said.

Lending has become a significant business for the company across all of its verticals. Consumer lending origination volume growth accelerated to 82% YoY, for example. Its “Borrow” product grew by 300% over that time period.

“Each new Block lending product has scaled originations at a faster rate than the last one,” the company revealed in its earnings presentation. A snapshot from that presentation is below: