Articles by deBanked Staff

P2P Lending / Former ‘LendAcademy Forum’ Has Moved Again

June 19, 2025deBanked has migrated the old LendAcademy p2p lending forum it acquired in 2021 to DailyFunder. Due to software compatibility issues, it was frequently offline on deBanked’s servers. It has now been moved to DailyFunder whose software was able to integrate the content somewhat successfully.

The LendAcademy forum, launched in 2011, was the most popular p2p lending forum in the US. An unfortunate incident, however, caused the data to be permanently lost in 2021. When that happened, deBanked used proprietary forensic techniques to restore as much of it as possible in a takeover deal it inked with the former operators.

DailyFunder, launched in 2012, is the oldest and most popular small business finance forum in the US. Any issues relating to it going further should be referred to DailyFunder at webmaster@dailyfunder.com.

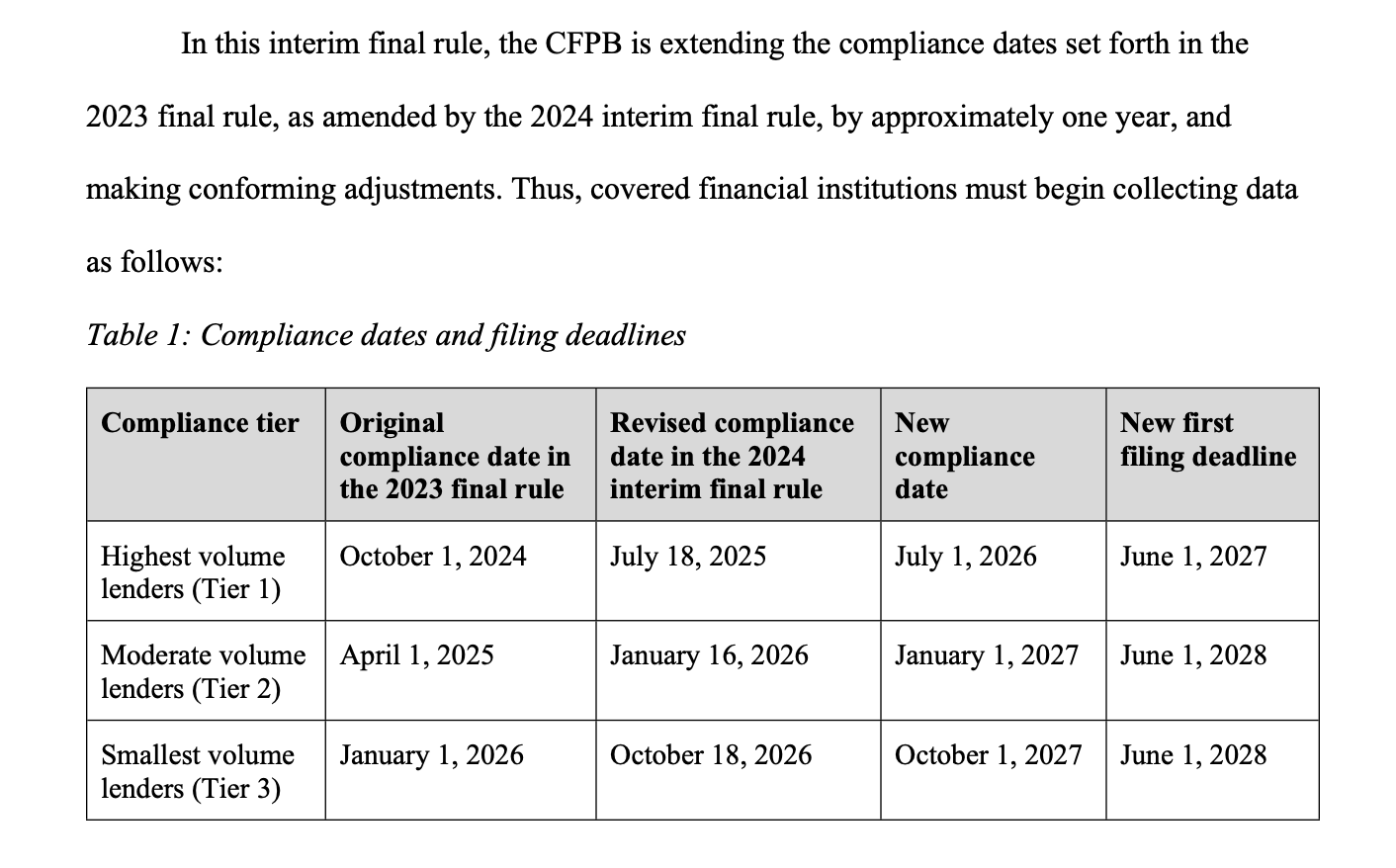

CFPB Small Business Lending Rule Compliance Delayed a Year

June 17, 2025 The CFPB has officially hit the pause button on complying with the small business lending data collection rules. They were supposed to go into effect next month. The Agency, however, announced in April that it planned to rewrite all of the rules and would not enforce them in the interim. Alas, covered parties wondered if they were still required to comply regardless of the whims on enforcement. Consequently, a new deadline for compliance was set for July 1, 2026. That assumes the new rules are ready by then or that there are no further delays.

The CFPB has officially hit the pause button on complying with the small business lending data collection rules. They were supposed to go into effect next month. The Agency, however, announced in April that it planned to rewrite all of the rules and would not enforce them in the interim. Alas, covered parties wondered if they were still required to comply regardless of the whims on enforcement. Consequently, a new deadline for compliance was set for July 1, 2026. That assumes the new rules are ready by then or that there are no further delays.

The rules have technically been delayed by fifteen years already since the law requiring such rules to be implemented was passed in 2010 (Dodd-Frank). Other priorities, politics, debates over the legislation’s scope, and endless litigation relating to it pushed back rule-making and compliance to where it is now. During Trump’s first term, there was even disagreement as to what the CFPB should even be called. deBanked has been covering the law for more than 10 years.

The law had previously been deemed applicable to both loans and merchant cash advances. The rules had been codified in 888 pages of guidelines.

Lightspeed: Potential to do up to $1B in Merchant Cash Advances

June 15, 2025Lightspeed may have only done $45 million in MCAs in FY 2025 but the point-of-sale company is continuing to grow that particular lucrative segment of its business conservatively, and possibly far below its full potential.

“There is a lot of opportunity. We can move faster if we wanted to,” said Lightspeed CFO Asha Bakshani during the company’s most recent earnings call. “When we look at our peers, for example, they are giving out 1% of their [Gross Transaction Volume] in merchant cash advance. Lightspeed is well below that. 1% of our GTV would be almost $1 billion in merchant cash advance. So when we think about the opportunity, it’s there. It’s just that in this macro, we want to move carefully on a product like Capital. Like I mentioned earlier, our default rates are in the very low single digits, and we want to keep it there.”

Lightspeed estimates its MCA program will grow by 30% in FY 2026. Part of the reason the company has grown its MCA business so conservatively is that it funds 100% of them on balance sheet.

The company advertises that MCA payments are enabled by either split or ACH.

Take This Industry Fraud Evaluation Survey

June 11, 2025Fraud is a growing challenge in the alternative lending space, particularly for lenders and funders that serve small businesses. As fraud tactics evolve – from synthetic identities and doctored bank statements to first-party fraud and account takeovers – funders and lenders face heightened risks that can lead to increased defaults, operational losses, and stricter underwriting processes.

MoneyThumb and deBanked have partnered to conduct a survey across lenders, funders, brokers, banks, and the fintech sector to reveal and better understand how fraud is impacting the industry. The goals are to help underscore the problem / shine a spotlight on an increasingly important sector that adversely impacts the industry and provide information on the most common fraud types and the tools strategies lenders are using to mitigate risk.

Your feedback is completely anonymous, and as a thank-you for participating, you’ll receive an exclusive early copy of the full report—plus additional insights not available to the public.

Check out other joint reports deBanked has previously participated in.

|

|

|

QuickBooks Capital Continues to Grow

June 8, 2025Intuit’s small business loan program, QuickBooks Capital, is continuing to grow. It generated $35M more revenue in FY Q3 2025 than it did over the same period last year, according to the company’s latest earnings report. Considering Intuit’s total quarterly revenue was $7.8B, its funding business, a small percentage of the total in comparison, is only mentioned in detailed on occasion.

QuickBooks Capital benefits from having a funding button in the widely used QuickBooks Capital software, a feature so effective that they were effectively the sixth largest online small business lender that deBanked tracked in 2024. Its two main products are a term loan and a line of credit.

Tell Your Merchants to Act on The Texas Legislation

June 5, 2025Unbeknownst to many small businesses in Texas, revenue-based financing will be severely restricted in the state starting September 1, 2025 if the governor permits HB 700 to be finalized into law. For small businesses who might want to have a say on this matter, the Revenue Based Finance Coalition (RBFC) has provided information for merchants to conduct outreach to the appropriate parties. If you have merchants who want to weigh in before it’s too late, please share this link with them.

Govenor Abbott has between now and June 22nd to veto the legislation. If he signs or elects not to sign the bill by that date, the law will take effect on September 1, 2025.

Online Search is King for How Merchants Shop For Funding, Survey Reveals

June 4, 2025Perhaps the most surprising statistic to come out of a 2025 small business lending survey conducted by IOU Financial is that 12% of merchants said they started their search for business funding options from a cold call. But as one might expect, phone calls are not necessarily the direction in which business is moving. Forty-one percent of respondents, for example, complained that they received too many phone calls from multiple reps.

The number one origin point—far above cold calls (12%), friends/referrals (8%), and social media (7%)—was online search (63%). And they’re not just looking at the first website and firing off a form. Fifty-eight percent, for example, said that online reviews were among the most valuable factors in choosing the right business funding provider, while loan calculators and comparison websites/tools also weighed heavily at 49% and 40%, respectively.

Historically, online search primarily meant Google, but according to a TD Bank survey, 30% of small business owners are already turning to AI assistants like ChatGPT for insights on financial health or financing.

And most merchants skip their bank. “More than 70% of small business owners do not apply for business funding with their bank before exploring non-bank options,” the IOU survey found. “This trend highlights a major shift in trust and preference away from traditional banks and toward alternative lenders—which could be driven largely by the desire for speed, flexibility, and ease of access.”

Carl Brabander, EVP of Strategy for IOU Financial, discussed some of the recent findings of this survey at Broker Fair 2025 this past May in New York City.

Texas Commercial Sales-Based Financing Bill Gets Last Minute ACH Ban Amendment

May 27, 2025The Commercial Sales-Based Financing bill that passed through the Texas House of Representatives two weeks ago has now also passed through the Senate, but with a rather controversial amendment. In the Senate version, passed yesterday, and viewable on the right hand side of this document, sales-based financing providers would not be allowed to automatically debit a merchant’s account unless they have a “validly perfected security interest in the recipient’s account under Chapter 9, Business & Commerce Code, with a first priority against the claims of all other persons.” That means any sales-based funding (like an MCA or revenue-based financing loan) would be prohibited from debiting merchants automatically unless they were in true first position. And not just a first position MCA, but first position on all arrangements the merchant has altogether. AND it would have to be perfected in accordance with this statute.

The Senate Amendment:

CERTAIN AUTOMATIC DEBITS PROHIBITED.

A provider or commercial sales-based financing broker may not establish a mechanism for automatically debiting a recipient’s deposit account unless the provider or broker holds a validly perfected security interest in the recipient’s account under Chapter 9, Business & Commerce Code, with a first priority against the claims of all other persons.

Since the main difference between what the Senate and House passed is that one sentence prohibiting automatic debits, they have until June 2nd to decide which version of the passed bill is final.

Sales-based financing is broad. While the term encompasses sales-based purchase transactions (MCAs), firms like Walmart and PayPal engage in loan-based sales-based financing. Both firms, for example, are registered sales-based financing providers in the state of Virginia.

The Texas Senate amendment language is new. It does not resemble anything passed in a state commercial financing disclosure law to date.

An estimated 10% of all sales-based financing in the US takes place with Texas-based businesses.