Articles by deBanked Staff

eBay Has Originated More Than $1 Billion in Business Loans & Merchant Cash Advances

April 7, 2026 More than $1 billion of business loans and merchant cash advances have been originated through the eBay Seller Capital program since its inception. The cumulative figure since 2021 was revealed last fall. eBay relies on partners like Liberis to fund the deals.

More than $1 billion of business loans and merchant cash advances have been originated through the eBay Seller Capital program since its inception. The cumulative figure since 2021 was revealed last fall. eBay relies on partners like Liberis to fund the deals.

E-commerce platforms have experienced rapid growth in merchant funding programs over the years. Amazon, Shopify, and LightSpeed, for example, also offer their own financing solutions that generate significant annual volume.

When the eBay partnership with Liberis was announced in 2024, eBay VP & General Manager of Global Payments and Financial Services Avritti Khandurie Mittal, said: “As a pioneer in ecommerce and the home to small businesses in more than 190 markets, eBay understands the challenges small businesses encounter in securing fast, flexible and transparent financing. eBay Seller Capital is aimed at fueling our sellers’ growth by providing them with tailored financing solutions that meet the unique needs of their businesses. The addition of Business Cash Advance to our suite of offerings in partnership with Liberis enables us to expand capital availability for our sellers on flexible terms – when they need it the most.”

Former Operator of NACLB Conference Sentenced to Eight Years in Prison

April 3, 2026Kris Roglieri, the founder, and former operator of the National Alliance of Commercial Loan Brokers (NACLB) Conference, was sentenced to 97 months in prison. Roglieri previously pleaded guilty to wire fraud conspiracy after it was revealed in 2024 that his commercial lending business, Prime Capital Ventures, was actually a ponzi scheme.

Roglieri’s attorney had argued that he should only get 4-6 years but the judge went with 8.

After the conviction this past fall, Acting U.S. Attorney Sarcone stated: “Kris Roglieri brazenly flaunted the proceeds of his scheme—including luxury vehicles, rare watches, and private jet travel—all while feeding his victims bigger and bigger lies to fuel his greed to even greater heights. But the truth stopped him like a brick wall. All those trappings of wealth will be forfeited, and he will be ordered to make his victims whole. I applaud the FBI and the members of my office on this case for unraveling this devastating scheme and bringing its perpetrators to justice.”

Roglieri founded the NACLB Conference in 2015 and operated it until 2023.

Diversity of Products Within Revenue-Based Financing

March 30, 2026Revenue-based financing has become extremely popular; So popular that it’s spawned its own variations of products. Some are loans, some are not. Many of the terms in the public vernacular are simply colloquial. The details are instead in the individual contracts. Refer to those contracts to understand how something works. Loans are absolutely repayable while non-loans structured as purchases tend to not be. The loans tend to have a hard term length built in if a merchant’s sales are well below what was projected even if it was based on a percentage of sales. Below is a small snapshot of how products are marketed with a percentage-of-sales payment mechanism.

One thing is certain. The trend of relying on a merchant’s revenue to determine payments is rapidly expanding.

The 2026 Coleman SBA Lending Awards Recap

March 24, 2026Coleman’s 2026 SBA Lender Professional Awards ceremony took place last week in Miami at the corporate headquarters of Banesco. Bob Coleman, the organizer of the event and founder of the Coleman Report, was the host. The annual Coleman Awards first debuted in 2025. The full list of winners from 2026 can be viewed here.

Among the keynote speakers were NewtekOne CEO Barry Sloane and iBusiness CEO Justin Levy. Sean Murray of deBanked won an award for SBA Best Use of Media. The event was well attended.

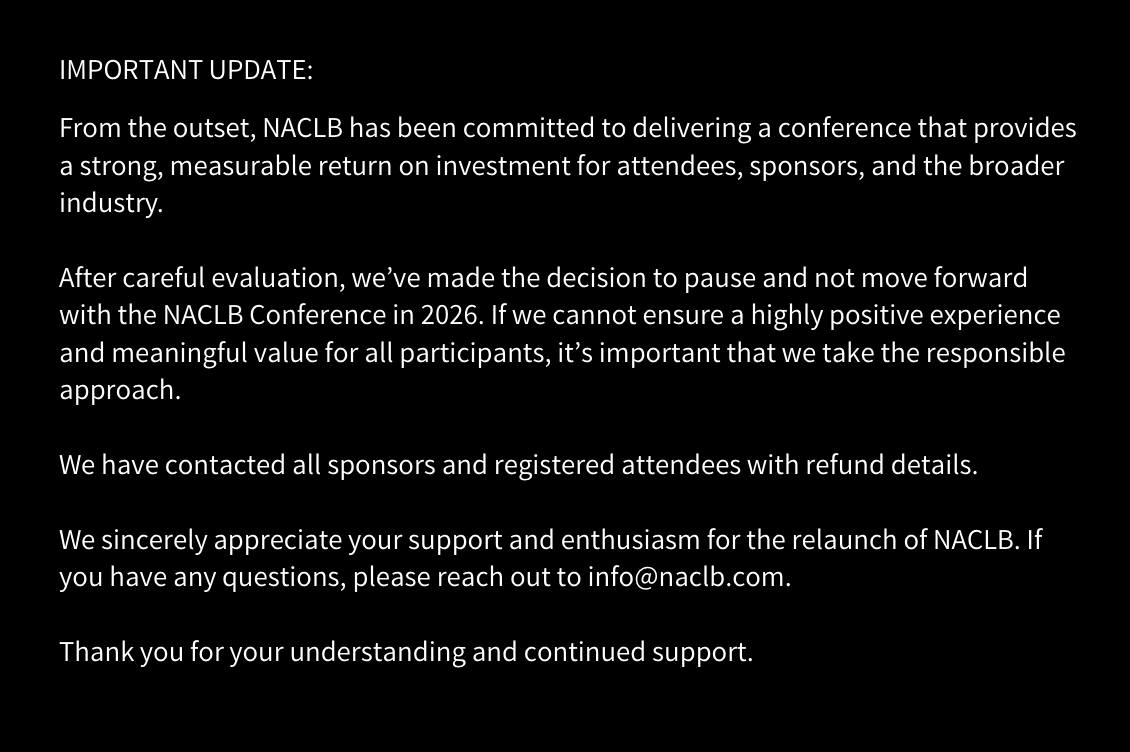

NACLB Conference Canceled

March 24, 2026A company organizing an event under the NACLB conference brand has decided not to go through with it. Initially they had planned to host a conference in Florida this coming June using the NACLB name that convicted felon Kris Roglieri had previously created. The company acquired the rights to that name through Roglieri’s personal bankruptcy proceedings while all the other assets of the original conference were returned to Roglieri.

“After careful evaluation, we’ve made the decision to pause and not move forward with the NACLB Conference in 2026,” the new NACLB website says. “If we cannot ensure a highly positive experience and meaningful value for all participants, it’s important that we take the responsible approach.”

The website says that sponsors and registered attendees will receive a refund.

Upstart: Humans are not very good at underwriting loans so AI won’t be either

March 23, 2026 “…unfortunately, humans have never really been very good at precisely underwriting loans and figuring out the cash flows they’re going to produce for the next 5 years,” said Upstart CEO Paul Gu during the company’s Q4 earnings call in response to an analyst’s question. “That’s something that has always been solved as a big math problem.”

“…unfortunately, humans have never really been very good at precisely underwriting loans and figuring out the cash flows they’re going to produce for the next 5 years,” said Upstart CEO Paul Gu during the company’s Q4 earnings call in response to an analyst’s question. “That’s something that has always been solved as a big math problem.”

Upstart’s innovative consumer credit models preceded the dawn of modern-day LLMs. It has been one of their defining features. Underwriting on their part is a combination of the best data access and math. Because of that, they do not view AI as a threat because AI is only great at replacing what humans are good at and underwriting is not one of those things.

“I mean the simple answer is just that a lot of the advances in AI are really good for work that humans are naturally good at,” said Gu.

Gu used an example of a HELOC in which human processors have to go through process of securing and perfecting a lien, checking property records, etc. “…like a lot of that stuff is a mess in a human way and traditionally comes with very high operations cost because you have a lot of people that are checking to make sure things are right,” Gu said. “Those are actually the perfect problem to throw sort of LLM-style AI against.”

When it comes to AI benefitting their business, that’s how Upstart is approaching it.

“…It’s really important to just remember that the LLM models coming from Anthropic or OpenAI or any of the others, Gemini, they are really good at solving problems that humans are good at solving and they can do it at scale. They can work 24/7. You can spin up 100 of them in parallel and have them work. But no matter how many humans you have, you don’t want that army of humans underwriting loans for you,” Gu said.

Mayor Mamdani: Merchants Should Get Revenue-Based Loans

March 19, 2026 New York City Mayor Mamdani has come out in favor of revenue-based financing. As part of a promotional video for the NYC Future Fund, a government-supported low interest loan program, the touted structural benefit of the program is the fact that the loans are repaid by a percentage of revenue rather than fixed payments.

New York City Mayor Mamdani has come out in favor of revenue-based financing. As part of a promotional video for the NYC Future Fund, a government-supported low interest loan program, the touted structural benefit of the program is the fact that the loans are repaid by a percentage of revenue rather than fixed payments.

“Unlike a traditional term loan, a revenue-based loan enables better cash flow management as principal repayments are based on a percentage of monthly revenue instead of fixed payments,” the Fund’s website says. “When revenue is higher, payments increase, when revenue is lower, payments decrease.”

“We’re building a fairer economy for the entrepreneurs that support our neighborhoods,” Mamdani says in the video alongside Department of Small Business Services (SBS) Commissioner Kenny Minaya.

Compared to previous iterations of the program which took a flat 9.5% of a merchant’s revenue, this new one will take only as low as 2 percent of monthly revenue, depending on loan size and business needs.

Commissioner Minaya says that revenue-based financing is better because it accounts for seasonality in sales like an ice cream shop that may have slower business in the winter.

The NYC Future Fund is a public-private partnership between the City of New York and local Community Development Financial Institutions (CDFIs), including Community Reinvestment Fund, USA (CRF), Accompany Capital, Grow America and Pursuit, to support long-term growth for small business owners.

According to a press release by the city, Mayor Mamdani took the lead on launching this $80M fund for small businesses.

New York City is simply the latest in a series of government-led initiatives to promote and expand revenue-based financing.

Fintech Mortgage Lending Platform Integrates With ChatGPT

March 17, 2026“Can you underwrite this loan?”

That’s an example offered by Better, a fintech mortgage lending platform, in its preview of how its new AI underwriting system can be used conversationally in a chat box. According to the announcement, up to 95% of mortgage applications can be approved instantly using the technology which is geared toward lenders. To use it, companies need only download the app into ChatGPT.

“The mortgage industry is riddled with inefficiencies that hurt consumers, as well as the loan officers and lenders who serve them,” the company said in an announcement. “Big mortgage aggregators in the broker and correspondent channel charge what is essentially a 1-2% tax on each loan just to underwrite a mortgage and deliver it to an institutional investor. That ends now,” said Leah Price, General Manager of Tinman AI Platform. “Loan officer teams and banks can simply log into their ChatGPT Enterprise account, download the Tinman AI credit decision engine app, connect their guidelines, pricing, and CRM to process, underwrite, and fulfill loans nearly instantly; passing thousands of dollars in savings to consumers.”

AI underwriting is being strongly considered in consumer lending but has not gained much traction in small business lending to-date.