Articles by deBanked Staff

NY Bankruptcy Court Rules Funder’s MCAs Were Really Loans

July 28, 2026A judge presiding over an action brought by the Chapter 7 Trustee of the Estate of Kossoff PLLC against an MCA funder, issued a 36-page analysis on Monday that reclassified 19 MCAs (for $10.8 million) the funder made between 2016 and 2020 as loans. The Trustee’s complaint argues that the MCAs the funder made to Kossoff PLLC were criminally usurious and should therefore be deemed void ab initio.

Enova Originated $1.6B in Small Business Loans in Q2

July 27, 2026Enova’s small business loan originations increased 29% year-over-year, coming in at $1.6 billion for Q2. Enova owns OnDeck and Headway Capital.

During the Q&A session of the company’s quarterly earnings call, Enova CEO Steve Cunningham was asked about the performance of their small business loan portfolio.

“I think on the SMB side, it’s been remarkably stable,” Cunningham said. “You can see quarter-to-quarter, we can have some growth variations, but we’ve been very healthy growth. Our net charge-off ratio has been hanging within the 4%-5% range that we would expect every quarter for quite some time.”

Stripe Capital, PayPal Working Capital Could Merge If Acquisition Offer is Accepted

July 19, 2026The old rumor that Stripe was interested in acquiring PayPal was apparently true. Partially anyway. This past April, Stripe, along with Block and Advent (a private equity firm), let PayPal know they were jointly interested in acquiring it. But Block dropped out of the deal and the newest acquisition offer, now public, comes from just Stripe and Advent together. While Stripe and PayPal are obviously known as payment processing companies, the two originate more than $3 billion a year in MCAs and short term business loans a year combined.

PayPal is one of the few online payment platforms to struggle with bad debt in its merchant funding program and the company had never weaponized its lending offerings to grow PayPal’s business. Nevertheless, its origination volume outpaced Stripe’s in 2025. Stripe and Advent offered $53 billion to acquire PayPal. It remains to be seen if a deal will actually happen.

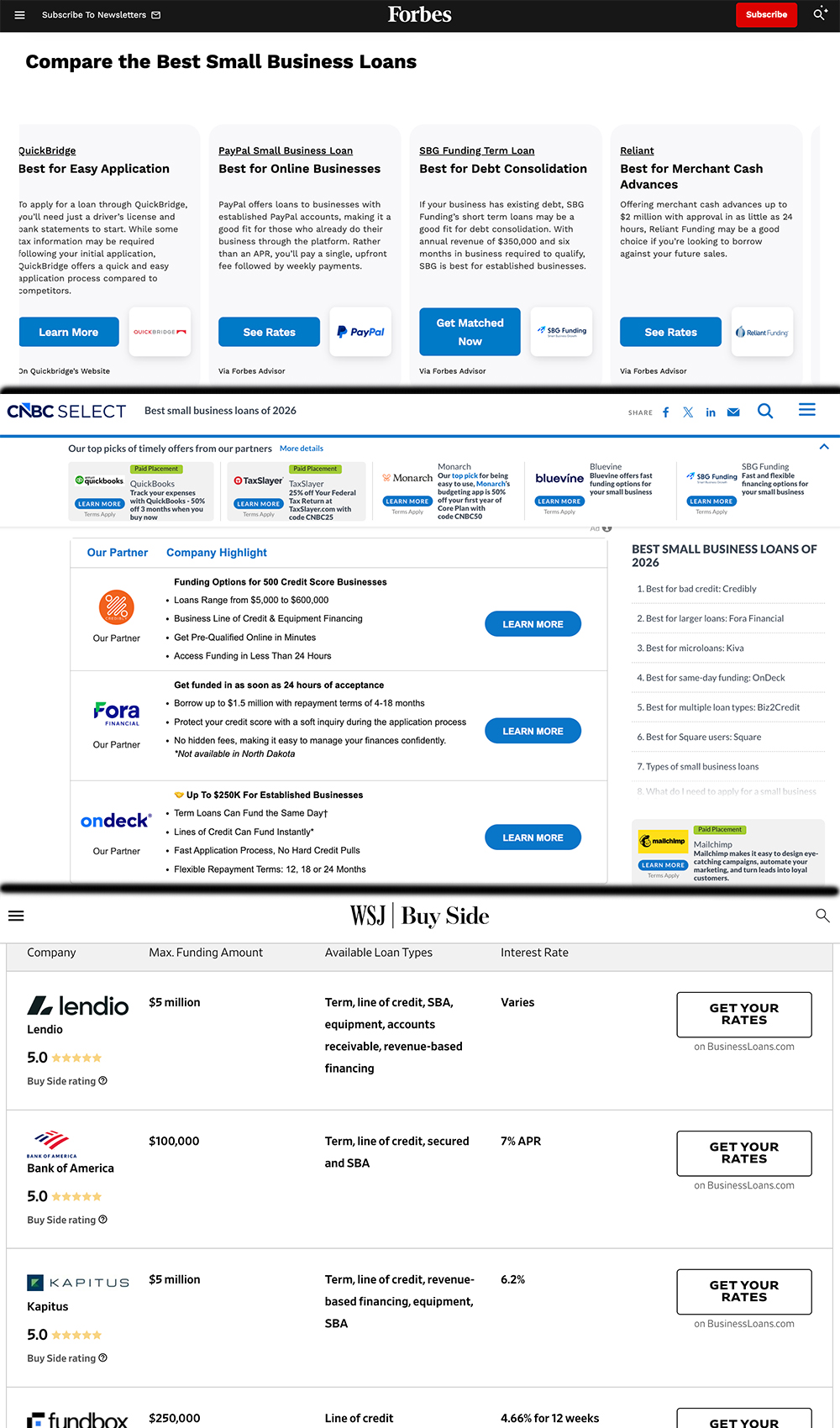

Wall Street Journal, CNBC, Forbes, and More Operate Small Business Funding Referral Marketplaces

July 16, 2026Walmart‘s not the only household brand name that’s running a small business funding marketplace. A cursory Google search shows that the Wall Street Journal, CNBC, and Forbes, among others, are also capturing traffic and earning commissions by referring merchants for business loans, revenue-based financing, and other products.

The WSJ says it earns commissions when merchants click links to apply for revenue-based financing, lines of credit, and other small business loans. “Revenue-based financing might be a good option if you don’t qualify for a business term loan,” the WSJ states on its review page.

Forbes operates with paid placements and links that generate affiliate commissions. The CNBC Select site says that the company earns commissions. WSJ, Forbes, and CNBC compete with other platforms like Nerdwallet, LendingTree, and Bankrate for business loan traffic online.

Meanwhile, Walmart’s business loan marketplace consists of Payoneer, Parafin, Slope, and Uncapped. Three of those partners offer merchant cash advances.

TCPA Lawsuits Up By 30%, According to WebRecon

July 14, 2026As of the end of May 2026, TCPA lawsuits were on pace to grow by 30% over 2025, according to WebRecon. This was across the board nationally, not specific to a single industry. WebRecon tracks consumer lawsuits on a monthly basis.

Complaints made to the CFPB were also up, on pace to be 34.8% higher than the previous year. The CFPB complaint database is public, but complaints are only published after the company responds or after 15 calendar days, whichever comes first. The CFPB removes complaints if they do not meet all of the publication criteria.

Soon, We’ll All Be Able to Charge AI Bots for Scraping Data

July 8, 2026 In 2025, an online small business forum went offline. It had been operating for 15 years and generated just enough ad revenue to cover the hosting costs. Until it didn’t. The problem was bots. So many bots. And not the spamming kind, but the AI kind. LLMs were mining them for training data first and then actively pinging them all day every day to tap into live conversations taking place in the small business owner community. And so the forum eventually added Cloudflare as a protective measure to try and slow the velocity of the traffic. Enough AI bot traffic still got through, however, and the strain on the bandwidth pushed the hosting costs beyond the revenue.

In 2025, an online small business forum went offline. It had been operating for 15 years and generated just enough ad revenue to cover the hosting costs. Until it didn’t. The problem was bots. So many bots. And not the spamming kind, but the AI kind. LLMs were mining them for training data first and then actively pinging them all day every day to tap into live conversations taking place in the small business owner community. And so the forum eventually added Cloudflare as a protective measure to try and slow the velocity of the traffic. Enough AI bot traffic still got through, however, and the strain on the bandwidth pushed the hosting costs beyond the revenue.

It was a good deal for the LLMs because when people asked their local chatbot a question, it had oddly specific conversational exchanges between business owners to draw from. Eventually, the forum owner realized that their real customer wasn’t advertisers or even small business owners anymore, but LLMs that wanted to mine what small business owners talked about on a live basis. If only there had been a way for a little small forum owner to charge that customer.

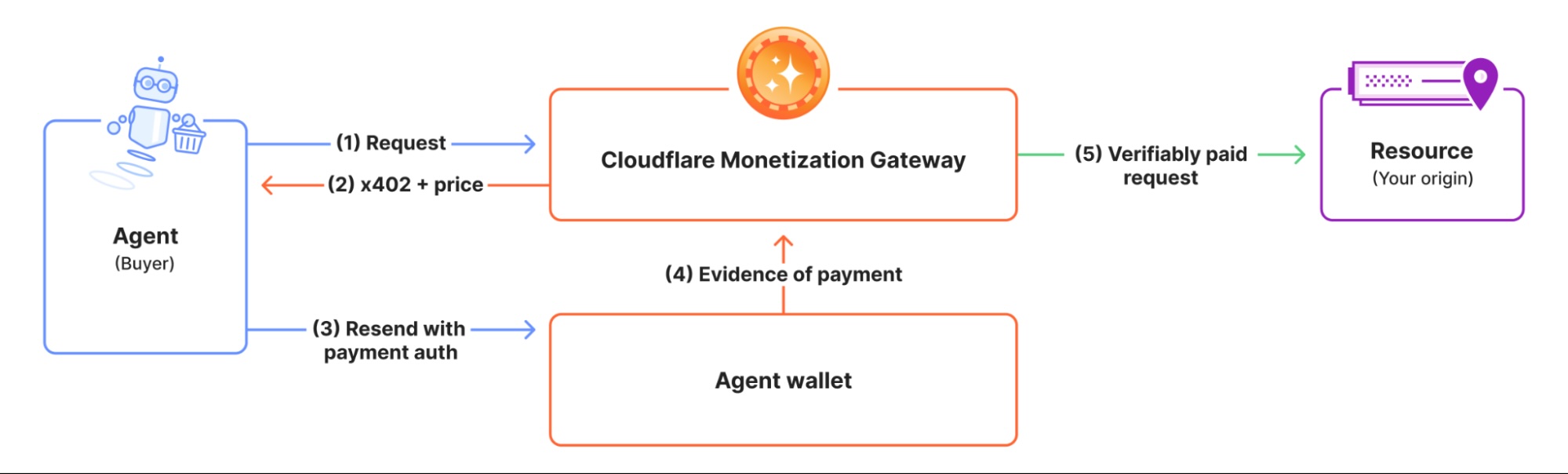

Now, there will be. On July 1, 2026, Cloudflare announced its new Monetization Gateway that will give Cloudflare customers “the ability to charge for any asset protected by Cloudflare: web pages, datasets, APIs, or MCP tools.”

It works as such: When an AI bot pings a url it is met with an http 402 code. Under the 402 protocol, the bot is presented with a price in real time of how much it will cost to access that data. If accepted, the bot pays in stablecoins, and they are passed through to the endpoint. This would all take place in less than a second with Cloudflare managing all the payments and settlements on blockchain rails. By using stablecoins, micropayments become highly feasible. Cloudflare uses an an example of a $0.001 base fee for example, 1/10th of 1 cent for a single call.

“An agent does not look at ads or need to maintain a monthly subscription to all the tools it wants to access,” Cloudflare said. “It reads a page or consumes a data feed once, takes what it needs, and moves on. Across the web, AI crawlers already request content anywhere from a hundred to tens of thousands of times for every visitor they send back.”

“This reality demands a new model: usage-based pricing for everything. If attention and e-commerce are moving from websites to AI harnesses and AI-written software, then agents should pay for the inputs they need — training data, inference content, developer tooling, and API usage.

Historically, usage-based billing was difficult to implement. Businesses needed to effectively become payments companies, running their own accounting to track internal usage in a robust and auditable way. Tracking this usage required significant overhauls of backend systems. Many instead chose per-seat pricing because it is simpler and frequently more profitable.

Agents flip this dynamic. A single agent can do the work of an entire team around the clock, making a flat one-time fee disconnected from actual consumption. At the same time, an agent can make thousands of micropayments without friction, while asking a person to approve each payment would be impossibly burdensome. Usage-based price points are where agents live and where stablecoin-based micropayments shine. That’s because stablecoins (such as Open USD and USDC) allow buyers to transfer tiny sums across the Internet, incurring negligible fees and settling in less than a second. This is not feasible with other payment rails today.”

– Cloudflare

“There is an enormous amount of value moving across the Internet today that goes unmonetized or undermonetized, not because no one would pay for it, but because the tools to charge for it have never existed,” Cloudflare further said.

And so while that forum remains offline, AI bots still ping the urls daily hoping it has come back. If in the near future the companies behind those bots decide the data is worth paying for, then perhaps the forum will eventually have a path for a return, and many other web-based businesses are finally able to charge who their real customers are, AI bots.

SoFi’s Small Business Loan Product Details

July 2, 2026SoFi is now a small business lender, according to their most recent announcement.

But they’ve been in this market for a while. They first flirted with the idea in February 2023 and then launched a marketplace in January 2024 to warm up to it. As a marketplace, they referred their own customers to other direct providers of capital, including MCA companies. Under this new program, applicants will be evaluated for a SoFi business loan first and then referred to their marketplace if they don’t qualify, second. Fundbox is referenced by name as one of the possible destinations for these applicants.

SoFi’s in-house business loan comes with a max APR of 36% and dollar ranges of $2,500 – $250,000. They’re personally guaranteed and have max terms of 2 years. Applicants need not be a SoFi customer to apply and funding can take place in as little as 24 hours.

Factoring to Take MCA Fight to Federal Level

July 2, 2026In the wake of new merchant cash advance laws passed in Texas and Vermont, American Factoring Association President Cole Harmonson posted the next step is to take the fight against MCAs to the federal level.

Post below: