Related Headlines

| 08/11/2022 | Video: Cheryl Tibbs - Fundly Milestones |

Related Videos

The Cheryl Tibbs Story - Fundly Milestones | Cheryl Tibbs of Equipment Lease Co. on the Red Carpet |

Cheryl Tibbs at Broker Fair 2024 | |

Stories

Tips From Tibbs: Vendor Marketing Guide

November 6, 2023 The fine line between being successful and being stagnant in the equipment finance industry can easily be determined by vendor relationships. Cheryl Tibbs (CEO/Owner at Equipment Lease Co.), a veteran in the field, recently released her Vendor Marketing Guide this past October. The ten-chapter booklet covers various aspects, including vendor marketing, contact building, crafting value propositions, and more.

The fine line between being successful and being stagnant in the equipment finance industry can easily be determined by vendor relationships. Cheryl Tibbs (CEO/Owner at Equipment Lease Co.), a veteran in the field, recently released her Vendor Marketing Guide this past October. The ten-chapter booklet covers various aspects, including vendor marketing, contact building, crafting value propositions, and more.

Vendors are businesses authorized to sell equipment to end-users, Tibbs explains, and establishing a relationship with them can take a broker that is used to hunting for individual deals to instead being the recipient of multiple deals per week. But how to get that business is where most brokers get stuck.

“I think a lot of brokers get stuck with, ‘Well, how do I find vendors and what exactly is a vendor?’” she told deBanked. “I think that chapter three sticks out in particular, just making contact, knowing how to find a vendor, what to say when you get a vendor on the hook, and how to engage with that vendor.”

Tibbs said that brokers often assume that vendors already have a bank in-house when that is not always the case. This thinking might also lead them to shoot too low even when they do solicit them.

“A lot of equipment brokers they market to vendors and say, ‘Hey, send me the stuff that your people won’t finance’ and I think if you ask for trash, you’re going to get trash,” said Tibbs. If a relationship is built properly, a broker can get the vendor’s A-paper clients, she added.

Not only does the guide breakdown vendor relationships but also provides examples of how to pursue them, whether it be email, in-person, etc. The guide is not where education ends for brokers, however. Tibbs believes it’s an on-going learning experience.

“I think if you’re making money and you’re building these relationships, that’s motivation in and of itself, to continue to sharpen your knowledge with regard to this,” she said.

Broker Battle Finds a Champion

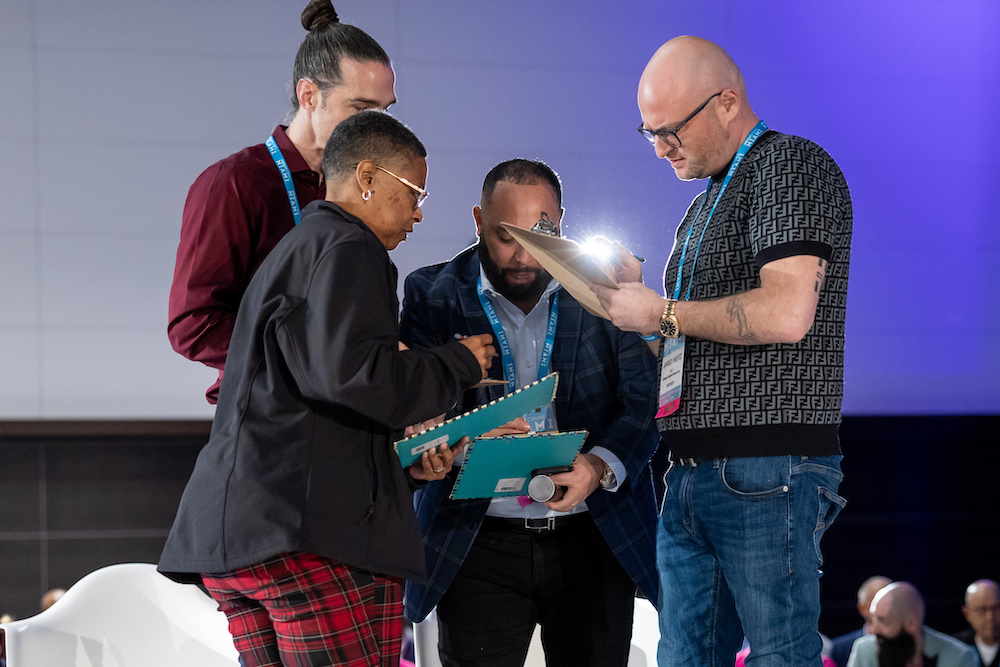

January 14, 2024At the Miami Beach Convention Center in Miami Beach, Florida, thousands of viewers packed a hall to witness the first ever Broker Battle™ at deBanked CONNECT. After the rules of the competition were explained, six broker contestants waited eagerly for their turn to face four judges and with that a chance to win a grand prize of $5,000. Their goal? Choose from one of three pre-defined sales scenarios and show off their knowledge and abilities to the judges. Here’s what happened:

The Broker Battle was introduced

Broker Battle judge Daniel Dames (Bitty Advance) held up a Title belt

Irving Betesh (Advance Funds Network) had the distinction of going first. He came prepared!

The contestants continued one by one alphabetically by last name

The conversational role playing on the stage covered the gamut, ranging from explaining APRs and contract terminology to diagnosing customer needs or trying to earn a customer’s business. Below, judges Jared Weitz (United Capital Source) and Cheryl Tibbs (Equipment LeaseCo Inc) listen in to a contestant’s pitch.

Mike Brooks (Best Connect Capital) came in with his own style

Corey Digi (Lexington Capital Group) put up a strong showing

Stanley Mitchell (CLM Financial) goes to work

Danielle Rivelli (United Capital Source) showed off her experience

Anthony Truglia (CapFront) made it known the competition wasn’t over yet

The judges had to add up their scores for each contestant to find out which TWO would make it into the final championship battle

Second from the right is judge Leo Vargas (Triton Recovery Group).

Anthony Truglia and Danielle Rivelli are declared the two finalists after racking up the highest scores

The final sales scenario is revealed!

Both contestants have to compete on stage at the same time! Oh my!

The contestants are sent offstage so the judges can deliberate

And the winner is…

Anthony Truglia!

All photos from the Broker Battle here

All photos from the rest of deBanked CONNECT MIAMI here

deBanked would like to thank all of the amazing broker contestants for participating in something bold and brand new. Thank you to Anthony Truglia, Danielle Rivelli, Corey Digi, Irving Betesh, Stanley Mitchell, and Mike Brooks. Gratitude is also directed towards the judges for their efforts, Cheryl Tibbs, Daniel Dames, Jared Weitz, and Leo Vargas.

deBanked hopes that this competition inspires all brokers to become better, to further master their knowledge of available products, legal compliance, style, and confidence. A video highlight reel of the competition is in post-production.

Interested in more from deBanked? Contact us at info@debanked.com or call 212-220-9084.

Leveraging ChatGPT for Maximum Productivity

July 28, 2023 “…It’s just been pretty impressive how we have this technology that came out that has literally changed everything, and it was almost overnight,” said Kareem Jernigan, CFO at Leasing Associates Inc.

“…It’s just been pretty impressive how we have this technology that came out that has literally changed everything, and it was almost overnight,” said Kareem Jernigan, CFO at Leasing Associates Inc.

Earlier this week the Black Equipment Finance Network (BEFN) hosted a webinar titled ‘Leveraging ChatGPT for Maximum Productivity’ for the equipment finance space. The panelists were Cheryl Tibbs, George Parker, and Kareem Jernigan.

Jernigan is already using ChatGPT in his daily work life. In one example, he said that he commonly uses it to analyze and find errors in spreadsheets. In another, he’s saving a lot of the time he normally spent on writing.

“…I also run HR, and so I have to craft communications and/or policies,” he said, “so, when you think of crafting a policy or a communication that you have to send out, before ChatGPT that would be something that would take 4 or 5 hours to do. […] That task today I could get that done in 30 minutes.”

Meanwhile, George Parker, Co-CEO at VenSource Capital, said “You can use ChatGPT with training staff. You can develop training material. You can give tests and quizzes. You can design training programs with time as an element, it can do all of that. You can even design courses with ChatGPT. You can tell ChatGPT to come up with a time frame for learning each part of a subject.”

Parker added that ChatGPT can be used for brainstorming, articles, planning, meeting content, customer service responses, and more.

Even in the finer details of equipment financing itself, the panelists said that ChatGPT can produce credit assessment profiles and analysis, analyze and summarize financial data, and scrutinize contracts,

Of course, all of this only works if one understands what to put in and takes the care to evaluate what comes out. It’s all about the proper “prompt.” One example offered of a prompt that wouldn’t work is: “teach me credit analysis.” Something like that would be too vague and would result in a response that was too broad. Part of the reason there are panels and webinars about ChatGPT to begin with is so the industry can learn how to leverage it for maximum productivity.

BEFN: A New Networking Space for Black Equipment Finance Professionals

March 30, 2023 “The event’s theme, ‘forging inclusive excellence in equipment finance,’ set the tone for the group’s mission to advance diversity, equity, and inclusion (DEI) in the industry,” said George Parker, Co-CEO at VenSource Capital LLC.

“The event’s theme, ‘forging inclusive excellence in equipment finance,’ set the tone for the group’s mission to advance diversity, equity, and inclusion (DEI) in the industry,” said George Parker, Co-CEO at VenSource Capital LLC.

Newly formed in January, the Black Equipment Finance Network (BEFN), is a non-profit organization focused on increasing the attendance of black professionals in the equipment finance industry. While providing network opportunities for people in the industry, the organization assists in promoting business collaboration, industry support and outreach, professional development, and Diversity, Equity and Inclusion (DEI) advocacy.

“I think the industry, given the mixer that we had last week in San Diego, is poised for [even more growth]. Many people showed up in support of what we’re looking to do,” said Lovern Gordon, National Sales Executive at Boston Financial & Equity Corp. “And that was a huge, huge, huge show of a vote of confidence that we’re headed in the right direction.”

The organization recently had their first inaugural mixer to kick off NEFA’s 4-day event, last week in San Diego. Filled with members and allies, the mixer dedicated a one-hour block to networking with people of color (POC).

“It was the most people that I and many others in the room have seen in terms of numbers for black people in the equipment finance industry in one space ever,” said Gordon.

For many POC, working in equipment finance can feel intimidating as the field is predominately a white-male led industry. The network is an all-around safe space for people that share in their likeness while being able to address issues of feeling left out of conversations or not feeling understood by their peers. The leadership team alongside Gordon (Secretary/Director), consists of George Park (President), Nancy Robles (Director), Kareem Jernigan (Treasurer/Director), Andre Olaofe (Director), and Eric McGriff (Director).

“This is a long overdue group of primarily black and people of color professionals in the equipment finance industry, that have just come together to form a small group within the industry to create an awareness of the black professional in the equipment finance industry,” said Andre Olaofe, President at Select Funding.

An active member of BEFN will typically attend monthly virtual meetings, have the option to be on panels, opportunity to come to regional and national events, advocate for laws and policies to improve within the industry, have access to the member directory, and mentorship.

“I’m on the steering committee,” said Cheryl Tibbs, CEO at Equipment Lease & Co. “The steering committee, we meet to set the agenda for the organization for our meetings. Just really to set the agenda for the group.”

The support from non-POC peers in the industry has been fantastic, Gordon explained. Several sponsors such as Dedicated Financial GBC, Wells Fargo Capital, North Mill Capital, and Wintrust Specialty Finance attended and donated, which contributed to pulling the mixer off. Tibbs noted the overwhelming response of non-black professionals that wanted to be involved who also saw a need for DEI within these organizations.

“The president of the National Equipment Finance Association, the board members of NEFA, the other members for funding sources, other brokers, all welcomed the group in San Diego, and came out to the mixer,” said Olaofe, “and were actively involved in at least sharing in the celebration of coming together and this inaugural mixer.”

The Buck in Trucking

December 21, 2022 “If you don’t have the marketplace of lenders, yes, it can be problematic,” said Cheryl Tibbs, Owner/CEO at Equipment Lease Co about providing capital to the trucking industry. “If you don’t understand the trucking industry, it can be very problematic.”

“If you don’t have the marketplace of lenders, yes, it can be problematic,” said Cheryl Tibbs, Owner/CEO at Equipment Lease Co about providing capital to the trucking industry. “If you don’t understand the trucking industry, it can be very problematic.”

In the last year, there has been an increasing interest in equipment financing. It was the primary topic of a panel discussion at Broker Fair and the subject of several sidebar conversations throughout the day and thereafter. For Tibbs, who lives and breathes equipment finance and trucking, she said she doesn’t see funding in that space slowing down.

“Every business that’s in business needs some type of equipment to operate,” said Tibbs. “Whether it’s a cell phone, a POS system, a car or truck, excavator, whatever it is, every business has some type of equipment. So I don’t see the industry slowing down at all.”

Tibbs, for her part, says that some companies in her lender network can provide a uniquely beneficial solution, a funding bundle that is part equipment finance and part working capital.

“Some of those customers may need that working capital for a down payment or if you’re buying a truck, for instance,” Tibbs said. “And this working capital comes in handy because if you know anything about trucking, the insurance on those things can be– I’ve seen it go as high as 60,000 a year, almost half the cost of a truck. So that working capital comes in handy.”

And the costs of trucks is in a state of flux. Jonathan Nelson, General Counsel at Dedicated Financial GBC, said the costs of used trucks is rapidly shifting.

“This month, you could get $20,000 for this particular used truck on the East Coast and next month, if you were to sell it on the West Coast, you might get $40,000,” said Nelson. “It’s very volatile at the moment.”

Evan Sowa, Senior Finance Manager at Everlasting Capital, echoed same.

“Depending on the geographical market, prices on the same truck can vary substantially,” he said. “Market prices are as high as I have ever seen them, up to 80% higher than similar units 4 years ago.”

Sowa continued by explaining that demand and prices in the used truck market have been booming but that they’re finally starting to cool off.

David Lee, CEO at North Mill Equipment Finance, said there are some issues in the wider trucking market right now.

“The trucking industry is facing a lot of challenges currently,” Lee said. “In addition to supply disruptions, and an inflation in used asset values and unavailability of newly manufactured equipment combined with significant increases in diesel fuel costs, a number of operators have felt tremendous margin pressure, with load rates having decreased, the cost of the equipment being higher, and the cost of operating the equipment via fuel being higher.”

A lot of those costs have not been able to be passed on to shippers, Lee added, and he said that they’re seeing a material increase in delinquencies and defaults amongst trucking operators.

A lot of those costs have not been able to be passed on to shippers, Lee added, and he said that they’re seeing a material increase in delinquencies and defaults amongst trucking operators.

Nelson at Dedicated, speaking on a much broader level of equipment finance, said that in general the industry has been able to escape the wave of defaults happening in other industries.

“We are a part of the National Equipment Finance Association and the Equipment Leasing and Finance Association to make sure that we understand issues and different trends that are happening in the equipment finance industry, because that’s where most of our clients are,” he said.

Tibbs, who’s a super broker, explained that she has seen lenders and funders tighten up their guidelines post covid.

“It’s not as easy to get plugged in with certain lenders,” she said. “It’s not as easy to get certain deals approved that we probably could have gotten approved pre-pandemic.”

Because of her experience and relationships, however, Tibbs is optimistic about the kind of deals she can get done, especially over newcomers who are at a disadvantage, explaining that she can finance pretty much anybody.

Evan Sowa at Everlasting summed up the state of things as such.

“Still funding trucks every day but the market is crazy right now,” he said.

Monday through Fund-day

September 8, 2022 Nothing screams excitement like a brand-new week filled with endless funding opportunities. Regardless of the type of funding, the ultimate goal is to find clients in need of capital and spring to action quickly.

Nothing screams excitement like a brand-new week filled with endless funding opportunities. Regardless of the type of funding, the ultimate goal is to find clients in need of capital and spring to action quickly.

“I would say Tuesday is like, a day that things get done,” said Michael Krepak, CEO of FlexCap Solutions. “People always talk about Friday’s a closing day. I’ve had a lot of success on Fridays as just like a funding day, like when the deals actually get done afterwards in all the underwriting and the back and forth and stipulations. So, Tuesdays and Fridays…”

Fridays may be hectic for some professionals in the business who are trying to close out a deal before the weekend is over. The pressure to close a deal can create competition within oneself to finish the week off strong or to make sure that nothing ruins it over the weekend.

“There’s always a push to get everyone funded right before the weekend, you don’t want deals rolling over,” said Brendan P. Lynch, CEO at Sharpe Capital. “Too many things can happen: negative days, they can go negative, and then the login, they have to redo it. And you know, the deal can die on Monday. So, you always want to get everything done before the weekend. That’s for sure.”

For equipment finance consultant Cheryl Tibbs, if she is able to finish funding by Thursday, she uses Fridays to either spend quality time with loved ones or to promote her business.

“I’m a bit different than most. I start off strong on Mondays and relax on Friday,” said Tibbs. “When I’m done Thursday, late Thursday evening, Friday is reserved for deals that will fund that day. If I don’t have anything booked for a Friday funding, I usually chill on Fridays and use that for marketing or family time.”

Sonia Alvelo of Latin Financial was non-committal to a day. “What gets us excited is the satisfaction of a job well done…” Alvelo said.

Krepak meanwhile, explained that if you’re working on commission, then there is an incentive to keep going strong every day. “Like every day, you want to do something every day,” he said. “It’s just a competitive face to begin with.”

The Highway to Quality Leads and Closing Deals

July 13, 2022 In the early months of 2020, twenty-two year-old Gary Parker found himself on a nature walk along a stretch of highway in Canada. As a savvy marketer in the medical spa field, the wide grip of Canadian pandemic lockdowns had quickly turned his thriving business into dust.

In the early months of 2020, twenty-two year-old Gary Parker found himself on a nature walk along a stretch of highway in Canada. As a savvy marketer in the medical spa field, the wide grip of Canadian pandemic lockdowns had quickly turned his thriving business into dust.

Swept off of his feet by the suddenness of his predicament, he turned to nature to clear his mind and found his next venture in the unlikeliest of ways.

“I went for a walk outside, and so I saw these trucks,” Parker said, “just like trucks on the road just driving. I was like, ‘everything is shut down but there’s trucks just moving things across the country.'”

Parker’s verbal description of the moment was enhanced by his scenic Zoom background when he was interviewed for the story. Parking his laptop on the hood of his car next to a real life mountain range along a Canadian highway, he explained that he didn’t have to tell me how that walk felt because he could show me. Moving his laptop camera around to show off tractor-trailers behind him in the distance, the inspiration that had come to him in 2020 was still present.

Though the country was supposedly closed for business back then, he couldn’t help but notice how many trucks were still on the highways shuttling supplies around.

“I’m a bit of a curious guy,” Parker said, “so I started Googling, like, ‘How much for a truck this big?’ and you know, they were like 70,000 bucks, 100,000 bucks. And I was like, ‘how do people even purchase these trucks?'”

Parker went on a research mission and discovered that few people, if any, were buying large trucks outright with cash, that so much of it was done through financing.

“And so I look up ‘what’s financing? How do people get truck financing?’ And then I recognized that other than truck-sales groups, there’s a section of people where their job is just to help people find the right financing methods.”

Parker thought he might be able to work with the latter group, given his marketing background, to help connect truckers with financing, but discovered the market in Canada was relatively small.

“Things really started to boom when I met my first USA client,” Parker said, because the demand in the US for truck financing seemed endless. “…in one day you could generate 100 inquiries of people who wanted financing for trucks,” he said.

Parker soon figured out that trucks were just one market in a wider industry of equipment financing, a rabbit hole of endless opportunity that led him to other big name entrepreneurs in the space like Josh Feinberg and Cheryl Tibbs. Feinberg, coincidentally, was a featured cast member in deBanked‘s recently produced equipment finance sales reality show.

Parker found common synergy with both and with their help was further introduced to the entire gamut of small business financing solutions.

“And that’s when I got fully immersed,” he said.

He didn’t want to be a broker or a lender, however, so instead he set out to focus on one very particular area of the process, lead generation. First, he built a system to help others, and then he gravitated towards creating a matchmaking system where brokers could connect with businesses that came to his company for help. The end result is his current company that many brokers have now become aware of, Fundly.

“So Fundly is an online marketplace,” he said, “where we have two things. Right now we have real-time matches, so [merchants] who are looking for funding every single day can come in free-of-charge and submit their inquiries, and we have funding members who can join for $1 a month who can see all these inquiries come in and then decide whether or not they want to pitch or share their profile with someone for five bucks.”

Parker explained it as a Tinder-style system where brokers can see the inquiries but can’t talk to the merchants unless the merchants also choose to engage with them. The upside is that when merchants say ‘yes,’ the brokers get to speak to someone that is interested right at that moment and with them specifically.

But Parker is a marketing guy, not a developer, and the execution of this required additional people to put the vision together.

“So we have a team now. Before when we just started, it was just me,” he explained. “If you’re going to write anything, let them know [about the team], because I have a hard working team who is behind every single thing and it wouldn’t have been possible, the technology wouldn’t have been possible without the team.”

Despite the business being born in Canada, Fundly is only targeting the US market because of its scope. Finding interested business owners is not even the hard part of his job, he explained, but rather the hard part is about educating brokers about how to communicate with businesses.

“I’m trying to teach our community members as they come into our orientation, what they think small business owners care about,” he said.

A big mistake for a broker, he explained, is starting off with a pitch about how many lenders they work with.

“Small business owners do not care about how many lenders you have in your back pocket,” he stated. “We’ve come to recognize a small business cares about one thing, what can you do for them? speak in terms of them.”

He imbues them with this marketing wisdom not just because he wants to improve their success rate, but also because he is adamant about making sure the businesses that come to his company get access to the right people with the right programs and prices. He doesn’t want to see these customers get a bad deal.

That Parker is a 24-year old former medical spa marketer hardly matters to brokers who recognize talent when they see it. When deBanked asked a senior executive of one reputable broker shop off the record what they thought about Parker, they responded by saying “he’s a genius.”

And besides, he’s not exactly that far off from where he started.

“The machines that some of the brokers finance, like laser therapy machines, stuff like that, I was working on the flip side, from the consumer perspective, having people sign up for high ticket packages from these machines,” he said.

And yet he’s very appreciative of how far he’s come since he went for that walk to reflect on his loss.

“God helped me. It was, it was rough, man. Yeah, not going to lie,” he said. “It was really rough.”

Toward the end of the interview, Parker had already shifted into marketing teacher mode.

“What really sets us apart is psychology,” he said. “Most people think that to get a business owner, you have to hit them and say, ‘Are you looking for the lowest terms? And you know, X, Y and Z??'”

The better approach, he explained, is to tell them that you will get them answers quickly.

“That results in a lot more funding,” he said, “because it’s not making a promise upfront, saying ‘let’s get you funds in 24 hours,’ it’s saying ‘let’s get you answers. And here’s someone to help you find these answers.'”

Consultative Selling in Small Business Finance

October 16, 2019

It’s nearly impossible to teach fiscal responsibility to most consumers, according to researchers at universities and nonprofit agencies. But alternative small-business funders and brokers often manage to steer clients toward financial prudence, and imparting pecuniary knowledge can become part of a consultative approach to selling.

It’s nearly impossible to teach fiscal responsibility to most consumers, according to researchers at universities and nonprofit agencies. But alternative small-business funders and brokers often manage to steer clients toward financial prudence, and imparting pecuniary knowledge can become part of a consultative approach to selling.

Still, nobody says it’s easy to convince the public or merchants to handle cash, credit and debt wisely and responsibly. Consider the consumer research cited by Mariel Beasley, principal at the Center for Advanced Hindsight at Duke University and co-director of the Common Cents Lab, which works to improve the financial behavior of low- and moderate-income households.

“For the last 30 years in the U.S. there has been a huge emphasis on increasing financial education, financial literacy,” Beasley says. But it hasn’t really worked. “Content-based financial education classes only accounted for .1 percent variation in financial behavior,” she continues. “We like to joke that it’s not zero but it’s very, very close.” And that’s the average. Online and classroom financial education influences lower-income people even less.

The problem stems from trying to teach financial responsibility too late in life, says Noah Grayson, president and founder of Norwalk, Conn.-based South End Capital. He advocates introducing young people to finance at the same time they’re learning history, algebra and other standard subjects in school.

Yet Grayson and others contend that it’s never too late for motivated entrepreneurs to pick up the basics. Even novice small-business owners tend to possess a little more financial acumen than the average person, they say. That makes entrepreneurs easier to teach than the general public but still in need of coaching in the basics of handling money.

Take the example of a shopkeeper who grabs an offer of $50,000 with no idea how he’ll use the funds to grow the business or how he’ll pay the money back, suggests Cheryl Tibbs, general manager of One Stop Commercial Capital, Douglasville, Ga. “The easy access to credit blinds a lot of merchants,” she notes.

Entrepreneurs often make bad decisions simply because they don’t have a background in business, according to Jared Weitz, CEO of New York based United Capital Source. “Many of the people who come to us are trying their hardest,” he observes.

Entrepreneurs often make bad decisions simply because they don’t have a background in business, according to Jared Weitz, CEO of New York based United Capital Source. “Many of the people who come to us are trying their hardest,” he observes.

Weitz offers the example of his own close relative who’s a veterinarian. That profession attracts some of the brainiest high-school valedictorians but doesn’t mean they know business. “He’s the best doctor ever and he’s not a great businessman because he doesn’t think about those things first. What he thinks about is helping people. That’s why he got into his profession.”

Entrepreneurs often devote themselves to a vision that isn’t businesses-oriented. “They start a business because they have a great idea or a great product, and that’s what excites them,” Grayson says. “They jump in with both feet and don’t think much about the business side.” The business side isn’t as much fun.

Merchants also attend to so many aspects of an enterprise—everything from sales, production and distribution to hiring, payroll and training—that they can’t afford to devote too much time to any single facet, notes Joe Fiorella, principal at Kansas City, Mo.-based Central Funding. Business owners respond to what’s most urgent, not necessarily what’s most important.

For whatever reason, some business owners spiral downward into financial ruin, bouncing checks, stacking merchant cash advances and continually seeking yet another merchant cash advance to bail them out of a precarious situation, says Jeremy Brown, chairman of Bethesda, Md.-based Rapid Advance.

Weitz advises sitting down with those clients and coming to an understanding of the situation. In some cases, enough cash might be coming in but the incoming autopayments aren’t timed to cover the outgoing autopayments, he says by way of example.

Informing clients of such problems makes a demonstrable difference. “We can see that it works because we have clients renewing with us,” says Weitz. “We’re able to swim them upstream to different products” as their finances gradually improve, he says.

The products in that stream begin with relatively higher-cost vehicles like merchant cash advances and proceed to other less-expensive instruments with better terms, says Brown. Those include term loans, Small Business Administration loans, equipment leasing, receivables factoring and, ultimately the goal for any well-capitalized small business—a relationship with the local bank.

Failing to consider those options and instead simply abetting stackers to make a quick buck can give the industry a “black eye,” and it benefits none of the parties involved, Tibbs observes. But merchants deserve as much blame as funders and brokers, she maintains.

Prospective clients who stack MCAs, don’t care about their credit rating and simply want to staunch their financial bleeding probably account for 35 percent to 40 percent of the applicants Tibbs encounters, she says.

Just the same, alt-funders continue to urge clients to hire accountants, consult attorneys, employ helpful software, shore up credit ratings, keep tabs on cash flow, calculate margins, improve distribution chains and outline plans for growth. It’s what helps the industry rise above the “get-money quick” image that it’s outgrowing, Weitz, says. Many funders and brokers consider providing financial advice an essential aspect of consultative selling. It’s an approach that begins with making sure applicants understand the debt they’re taking on, the terms of the payback and how their businesses will benefit from the influx of capital. It continues with a commitment to helping clients not just with funding but also with other types of business consultation.

“It’s not so much selling as building a rapport with clients—serving as a strategic advisor or financial resource for them, identifying their needs and directing them to the right loan product to meet those needs,” says Grayson. “They should feel they can call you about anything specific to their business, not just their loan requests.” He also cautions against providing information the client will not absorb or will find offensive.

Justin Bakes, CEO of Boston-based Forward Financing also advocates consultative selling. “It’s all about questions and getting information on what’s driving the business owner,” he says. “It’s a process.”

Consultative sales hinges on knowing the customer, agrees Jason Solomon, Forward Financing vice president of sales. “Businesses are never similar in the mind of the business owner,” he notes. “To effectively structure a program best-suited to the merchant’s long-time business needs and set a proper path forward to better and better financial products, you need to know who the business owner is and what his long term goals are.”

“It’s taking an approach of actually being a consultant as opposed to a $7 an hour order taker,” Tibbs says of consultative selling. “I like to teach new reps to think of it as if you were a doctor. Doctors ask questions to arrive at a final diagnosis. So if you’re asking your prospective customer questions about their business, about their cash flow, about their intentions of how they’re planning to get back on track.”

Learning about the clients’ business helps brokers recommend the least-expensive funding instrument, Tibbs says. “I really hate to see someone with a 700 credit score come in to get a merchant cash advance,” she maintains. The consultative approach requires knowing the funding products, knowing how to listen to the customer and combining those two elements to make an informed decision on which product to recommend, she notes.

Consultative sales can greatly benefit clients, Weitz maintains. If a pizzeria proprietor asks for an expensive $50,000 cash advance to buy a new oven, a responsible broker may find the applicant qualifies for an equipment loan with single-digit interest and monthly payments over a five-year period that puts less pressure on daily cash flow.

Consultative sales can greatly benefit clients, Weitz maintains. If a pizzeria proprietor asks for an expensive $50,000 cash advance to buy a new oven, a responsible broker may find the applicant qualifies for an equipment loan with single-digit interest and monthly payments over a five-year period that puts less pressure on daily cash flow.

It’s also about pointing out errors. Brokers and funders see common mistakes when they look at tax returns and financial records, says Brown. “The biggest issue is that small-business owners—because they work so hard— make a profit of X amount of money and then take that out of the business,” he notes. Instead, he advises reinvesting a portion of those funds so that they can build equity in the business and avoid the need to seek outside capital at high rates.

Another common error occurs when entrepreneurs take a short-term approach to their businesses instead of making longer-term plans, Brown says. That longer-term vision includes learning what it takes to improve their businesses enough to qualify for lower-cost financing.

Sometimes, small merchants also make the mistake of blending their personal finances and their business dealings. Some do it out of necessity because they’re launching an enterprise on their personal credit cards, and others act of ignorance. “They don’t necessarily know they’re doing something wrong,” Grayson observes. “There are tax ramifications.”

Some just don’t look at their businesses objectively. Take the example of a company that approached Central Funding for capital to buy inventory in Asia. Fiorella studied the numbers and then informed the merchant that it wasn’t a money problem—it was a margins problem. “You could sell three times what you’re wanting to buy, and you still won’t get to where you want to be,” he reports telling the potential customer.

Consultative selling also means establishing a long-term relationship. Forward Financing uses technology to keep in contact with clients regularly, not just when clients need capital, Bakes notes. That cultivates long-lasting relationships and shows the company cares. As the relationship matures it becomes easier to maintain because the customers want to talk to the company. “They’re running to pick up the phone.”

The conversations that don’t hinge on funding usually center on Forward Financing learning more about the customer’s business, says Solomon. That include the client’s needs and how they’ve used the capital they’ve received.

“We have our own internal cadence and guidelines for when we reach out and how often and what happens,” says Solomon. Customer relationship management technology provides triggers when it’s time for the sales team or the account-servicing team to contact clients by phone or email.

Do small-business owners take advice on their finances? Some need a steady infusion of capital at increasingly higher cost and simply won’t heed the best tips, says Solomon. “It’s certainly a mix,” he says. “Not everybody is going to listen.”

Paradoxically, the business owners most open to advice already have the best-run companies, says Fiorella. Those who are closed to counseling often need it the most, he declares.

Moreover, not everybody is taking the consultative approach. “New brokers are so excited to get a commission check they throw the consultative approach out the window,” Tibbs says.

Yet many alt-funders bring consultative experience from other professions into their work with providing funds to small business. Tibbs, for example, previously helped home buyers find the best mortgage.

Consultative selling came naturally to Central Funding because the company started as a business and analytics consultancy called Blue Sea Services and then transformed itself into an alternative funding firm, says Fiorella. Central Funding reviews clients’ financial statements and operations between rounds of funding, he notes.

Consultations with borrowers reach an especially deep level at PledgeCap, a Long Island-based asset-based lender, because clients who default have to forfeit the valuables they put up as collateral—anything from a yacht to a bulldozer—says Gene Ayzenberg, PledgeCap’s chief operating officer. Conversations cover the value of the assets and the risk of losing them as well as the reasons for seeking capital, he notes.

No matter how salespeople arrive at their belief in the consultative approach, they last much longer in the business than their competitors who are merely seeking a quick payoff, Tibbs says. Others contend that it’s clearly the best way to operate these days.

“The consultative approach is the only one that works,” says Weitz. “Today, everything is about the customer experience. People are making more-educated, better informed decisions.” What’s more, with the consultative approach clients just keep getting smarter, he adds.

The days of the hard sell have ended, Grayson agrees. Customers have access to information on the internet, and brokers and funders can prosper by helping customers, he says. “Our compensation doesn’t vary much depending upon which product we put a client in so we can dig deeper into what will fit the client without thinking about what the economic benefit will be to us.”

Even though the public has become familiar with alternative financing in general, most haven’t learned the nuances. That’s where consultative selling can help by outlining the differing products now available for businesses with nearly any type of credit-worthiness. “It’s for everybody,” Weitz says of today’s alternative small business funding, “not just a bank turn-down.”

The CrackDown Is On! Great Article Sean... tibbs, in the september/october issue of debanked magazine. she warned that fake funders can steal deals and pocket the entire commission. they solicit deals in online forums, by email message or over the phone, and then they offer the deals to companies that really do function as direct funders, she said., , while no online forum was specified in the story, at least two forums have responded by cracking down on anonymity by suspending or banning violators., , the age of the gmail funder is coming to a close. dont buy leads from hotleads4u69@hotmail.comand definitely dont syndicate with a company that has no known address.... |

See Post... tibbs being one of them gave her a scenario yesterday and in 10 minutes she responded back very professional., , thanks again , df!!, , richard taylor, vice president of sales, , arcarius llc, direct: 201-676-2137, cell: 201-953-003... |

See Post... tibbs, , , i just want to confirm the difference between the two payoff amounts. there is no additional fee charged if a merchant pays us off through a third p... |