Stories

Total Merchant Resources Obtains California Lending License

October 17, 2016Piscataway, N.J. – October 17th 2016 – Total Merchant Resources, a Piscataway based business funder and a veteran in the merchant cash advance space, has obtained their California Lending License to capitalize on providing businesses with working capital in the Nation’s most populous state. This new designation allows TMR to quickly and easily extend money to small and medium sized business throughout the Golden State.

“We are thrilled to have access to this very important market. In addition, TMR is now perfectly positioned to do business in California as we await the imminent and necessary regulation of the industry,” said TMR Co-Founder and CEO Jason Reddish.

Reddish and co-founder and CFO Val Pinkhasov, who were recently featured on CNBC’s ‘Shark Tank’, were among the very first business lenders to enter this space. They are a respected name in the industry and thanks to their major prime time TV appearance, have brought attention to this underutilized model for businesses to obtain working capital.

For more information contact Gary Lane, Director of Business Development at (212) 220-9872.

United Capital Source is Now Licensed in California

July 19, 2016

United Capital Source, the company featured in deBanked’s September/October magazine issue, announced that they’ve become licensed by the State of California Department of Business Oversight as a finance lender and broker. “With its new license, UCS will be writing high quality loans for California small business owners,” Weitz wrote.

California attorney Paul Rianda wrote a guide for deBanked about that process late last year and stressed, “you need to make sure the packet you submit [to the DBO] is perfect.”

In an email, Weitz said that he is “really excited about the opportunity it will create for UCS and for CA merchants to be offered our low rate financing programs.”

California Lending License Questions Answered – Even the Tricky Ones

May 2, 2016 Q: Can a loan broker operate under the authority of a lender that’s licensed in California?

Q: Can a loan broker operate under the authority of a lender that’s licensed in California?

A: “The CFLL requires both lenders and brokers to hold their own licenses.”

That’s one of many responses provided by Department of Business Oversight Commissioner Jan Lynn Owen to a series of questions and hypothetical scenarios posed by the Equipment Leasing and Finance Association. The nine pages of answers, available on Leasing News basically explains that any funny business or creativity to try and circumvent the law will not be tolerated.

Tom McCurnin, an attorney at Barton, Klugman & Oetting, wrote in Leasing News that “disguising the commissions as something else, like a markup or consultation fees, won’t pass muster before the DOB. The parties engaging in this may be subject to a cease and desist order and hefty fines.”

“While many may claim the recent letter is a revelation, I believe it is simply a restatement of what we’ve known all along—get a license or face the consequences,” he concludes.

Loan Brokers: Here’s How to Submit a Deal to a Licensed California Lender

February 24, 2016 Brokers that wish to submit deals to a licensed California lender must also be licensed in the state. This does not apply when the lender is lending via a chartered bank relationship or if the transaction itself is a purchase of future receivables (AKA a traditional merchant cash advance). QuarterSpot for example, recently became a licensed lender (#603-K646) and will be operational to lend in the state starting on March 7th, according to the company.

Brokers that wish to submit deals to a licensed California lender must also be licensed in the state. This does not apply when the lender is lending via a chartered bank relationship or if the transaction itself is a purchase of future receivables (AKA a traditional merchant cash advance). QuarterSpot for example, recently became a licensed lender (#603-K646) and will be operational to lend in the state starting on March 7th, according to the company.

While the process wasn’t easy, they want to make sure that brokers are abiding by the rules as well. To this end, QuarterSpot EVP Mike Green posted a link on the deBanked forum to the licensing form that brokers must complete to apply:

We will require our partners to submit their CFLL License as required by the State. Please send those in ASAP to partners@quarterspot.com

1. Licensing form outlining requirements for licensure – http://www.dbo.ca.gov/forms/Finance_Lenders/DBO_CFLL_1422.pdf

2. Article further explaining legislation – http://www.paulhastings.com/publications-items/details/?id=e867e669-2334-6428-811c-ff00004cbded

In addition to the 31 page application is the payment of a $25,000 Surety Bond. Suffice to say, the process and costs are probably not a good fit for a 2-man upstart loan brokerage with a razor thin budget working out of month-to-month office space. But for a moderately sized operation or bigger, being a licensed broker can potentially be a competitive advantage.

The reason that brokers don’t need to be licensed to send deals to lenders like OnDeck, is because OnDeck operates through a chartered bank relationship and is therefore exempt from licensing requirements. As always, ask an attorney for an opinion if you’re not sure or need help. A broker may be just as culpable for submitting a deal to an unlicensed lender as the lender would be for operating unlicensed.

You can check to see if a lender is licensed at http://www.dbo.ca.gov/fsd/licensees/ but keep in mind that the database is rarely updated (the last time was 2 months ago).

Other helpful information

Can California Lenders Pay Referral Fees to Unlicensed Brokers?

Getting a California Lender’s License

California Lending License Process Isn’t Easy, State Painfully Slow on Paperwork

February 15, 2016Quarterspot recently became a licensed lender in California. And it wasn’t quick, according to Quarterspot’s EVP Mike Green. It took much longer than a year, he says. Their CFLL license # is “603-K646”, but you can’t confirm that with California’s registry because the database hasn’t been updated in 42 days.

Welcome to the State that apparently has an abundance of resources to launch inquiries into marketplace lenders, but little time to work with the ones eager to operate in full compliance.

California attorney Paul Rianda told deBanked back in December that it can take months just to get a reply on a lending license application. And when they do reply, they’re sticklers over details. “I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application,” Rianda wrote. “The name of the company was submitted on the application with ‘Inc’ instead of the complete ‘Inc.’ at the end of the company’s name.”

Yellowstone Capital’s Isaac Stern said it took them 15 or 16 months to get their license and required a lot of legal help from law firm Hudson Cook LLP. The cost, including lawyers’ fees came to about $60,000. “Man, it was like pulling teeth to get that license,” Stern told deBanked last year.

Tom McCurnin, an attorney for Barton, Klugman & Oetting LLP, disagrees. In an op-ed he wrote for Leasing News to counter a story published by deBanked, McCurnin wrote, “I would point out that the process of obtaining a California license is awfully easy, and involves a small filing fee and a bond.”

But for those not from the leasing industry, “easy” is not a word that comes to mind. “They’ll take away your license if you even sneeze the wrong way,” Stern previously told deBanked.

Worse, a change in the law regarding the payment of referral fees has led to a flurry of questions from lenders and commercial finance brokers alike. Law firm Hudson Cook LLP and Patrick Siegfried of the Usury Law Blog, both even had to weigh in on the issue. (See: Can California Lenders Pay Referral Fees to Unlicensed Brokers? | California Finance Lenders Push Legislative Agenda in Response to Growth of Alternative Small Business Finance Industry)

And even more confusing, is whether or not a license can be transferred. In February of 2015 for example, LoanMe Inc was ordered by the Department of Business Oversight to stop using what they claimed was another company’s lending license. But then a month later, the order was paused upon receiving “additional information” and then withdrawn.

As it stands with the State’s marketplace lending inquiry, 14 lenders have to respond by March. Among them is Kabbage Inc., Prosper Marketplace Inc., Avant Inc., On Deck Capital Inc. and Social Finance Inc., according to the Wall Street Journal.

Neither Kabbage or OnDeck are licensed California lenders from what deBanked could ascertain. But both would be legally eligible to make loans in the State through their chartered bank relationships.

“These online lenders are filling a need in today’s economy, and we have no desire to squelch the industry or innovation,” said DBO Commissioner Jan Lynn Owen in a December announcement.

In the meantime, being a licensed lender in the state is being perceived as a competitive advantage. Quarterspot for example, wants brokers to know that they can do loans in California now. Of course, after having waited painfully long to become licensed, it’s disheartening for them to see that the state hasn’t even updated their records since January 4th.

deBanked attempted to reach out to the California Department of Business Oversight a week ago to find out why their data was so slow to be updated. Nobody responded.

Getting a California Lender’s License

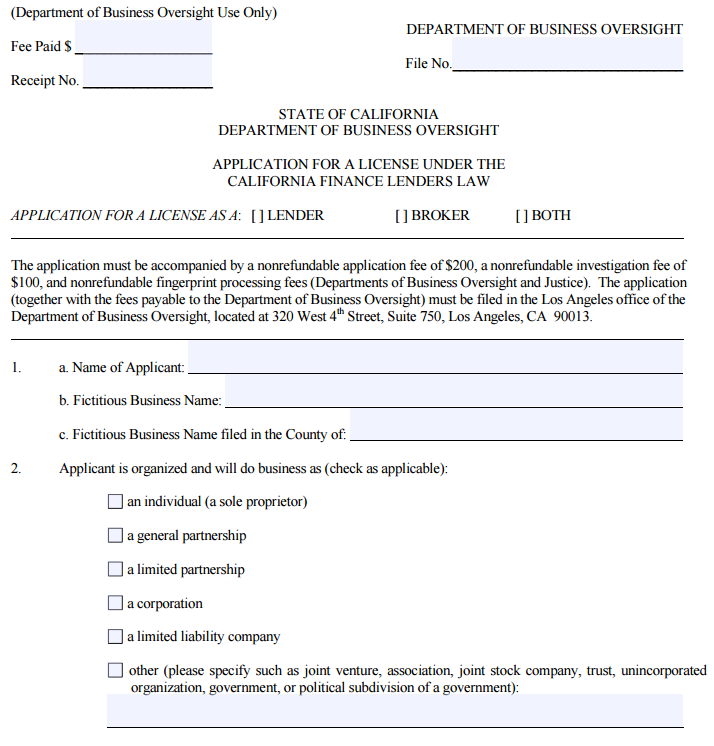

December 17, 2015Given the fact there have been a number of successful lawsuits against cash advance companies in California, many cash advance companies have decided to take a different route and get a lending license to provide loans to merchants in the state. If done correctly, this can allow companies to provide loans to merchants in California at roughly the same profit margins one could expect from a cash advance. Below I will discuss the process for obtaining a California lender’s license and some tips for making that process less painful.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

The first part of the application requests basic information about your company and its officers. In filling out this and other parts of the application, it is essential to respond to all the questions. If you fail to miss just one response the application will be rejected. To that end, even if a question does not apply to you I find it better to respond “N/A” or “not applicable” rather than just leaving a blank. By doing that you force yourself to fill in every blank and therefore reduce the chances for missing a response resulting in a rejection of your application.

Also, you need to be very precise in your responses. I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application. The name of the company was submitted on the application with “Inc” instead of the complete “Inc.” at the end of the company’s name. The examiners are very good at what they do and very thorough. You need to make sure the packet you submit is perfect and also that there are no inconsistencies in the document.

Another important point to remember is that the application requires you to name the person that will be responsible for running the location where the lending is occurring. The main requirement is that the person running the location must be physically present at the location. As a result, you could not manage a California office remotely from New York for instance. In another twist, if your principal location is out of state, you will need to get the license and fill out the main application for that out of state address. For the California location, you will need to fill out the short form application in addition to the main application and submit the short form application as part of the packet to allow the license to apply to the location in the state of California.

There are a number of exhibits you also have to provide as part of the process. Some of them are simple like a balance sheet for the company. It is acceptable that the company is new and has little in the way of assets. You just have to make sure you attach a balance sheet and that it is prepared in compliance with generally accepted accounting principles. I have seen times when the balance sheet was rejected because there was no line items for liabilities for instance, even though the company was new and therefore had none. It is probably wise to engage your accountant to make sure you submit a balance sheet that complies with those guidelines.

You also have to get a surety bond in the amount of $25,000. There are readily available bonding companies that specialize in providing these bonds. In addition, you need some other exhibits like a statement of good standing for your company, authorization for financial disclosure, social security number (on a separate exhibit), organizational chart and a few other documents. As with the rest of the application the key is to make sure you include everything they are asking for exactly as requested.

The most involved exhibit is the “Statement of Identity and Questionnaire.” That exhibit has to be filled out for each owner, officer and manager listed on the application. It requests detailed information going back 10 years for each person for items like residence address and work history.

In addition, there are a series of questions on topics such as whether the person has been involved in lawsuits, had any licenses revoked or declared bankruptcy. Fingerprints are also taken as part of the process. This part of the application is trying to vet the various people working for the company to make sure they are suitable to be in the lending business.

Once you have all the documents prepared, you need to put them together in a packet to send off to the Department of Business Oversight to be reviewed. Again, I cannot overemphasize how important it is to completely and accurately answer the questions and put the packet together. You need to make sure things are in the proper order and complete. Triple check the application for errors and to make sure that packet is presented in the best manner possible. You also need to determine the amount of fees to submit with the application. Then, send the package by overnight delivery to make sure you have proof of delivery.

So what happens next? Well there is usually a bit of a wait. Typically it takes 3 months or more to get a reply. If you have done your homework, you might get lucky and successfully get your license on the first try. If there are any deficiencies, you will get a response letter from the State detailing the items that need to be corrected in the application and a time frame in which you have to respond or the application is abandoned.

On the first go round, you are usually given at least 2 months so you should have plenty of time. Digest the things they want and provide the required information. The deficiency letters are very detailed so it should be easy to make the requested changes. Resubmit the requested items and wait for the next response. It could be in the form of another deficiency letter but it could be an approval of the license. Just keep on trying until you are finally successful.

That’s it, you are finally a licensed lender in California! But that is where the fun begins. You are subject to many laws in California and audits by the State. To get the right to operate as a licensed lender, you need to make sure you prepare your application correctly. Once you have done that, you need to get all your loan documents drafted in compliance with California law. Make sure you have adequate experience and professional help to take on those tasks.

Can California Lenders Pay Referral Fees to Unlicensed Brokers?

December 15, 2015 A new California law is drawing attention to a much-misunderstood issue – whether California Finance Lenders can pay referral fees to unlicensed ISOs. Effective January 1, 2016, the answer is yes, but only for commercial loans with an annual percentage rate of less than 36% where the lender reviews documents to verify the borrower’s ability to repay. These restrictions benefit non-profit lenders making business development loans, and shut out their higher-cost commercial lender competitors from paying referral fees to unlicensed ISOs.

A new California law is drawing attention to a much-misunderstood issue – whether California Finance Lenders can pay referral fees to unlicensed ISOs. Effective January 1, 2016, the answer is yes, but only for commercial loans with an annual percentage rate of less than 36% where the lender reviews documents to verify the borrower’s ability to repay. These restrictions benefit non-profit lenders making business development loans, and shut out their higher-cost commercial lender competitors from paying referral fees to unlicensed ISOs.

Existing regulations under California’s Finance Lender’s Law (“CFLL”) prohibit paying any compensation to unlicensed persons or companies for “soliciting or accepting applications for loans.” 10 CCR 1451(c). This prohibition does not apply to referrals for merchant cash advances or referrals to banks, which are not subject to the CFLL. A number of not-for-profit CFLL lenders offering business development loans complained that it was unfair that they could not pay referral fees to an unlicensed ISO while their higher-cost competitors, the merchant cash advance companies, could.

California SB 197, supported by Opportunity Fund, California’s largest not-for-profit commercial lender, and the California Association of Micro-Enterprise Organizations, a group of more than 170 organizations, agencies, and individuals dedicated to furthering micro-business development in California, aimed to remedy this perceived problem. According to an information sheet on SB 197 available on the Opportunity Fund’s web site:

Often, merchant advance companies offer less favorable terms to small businesses than commercial lenders; however, small businesses never learn about the commercial lenders that offer more favorable terms, because those lenders cannot compensate entities to refer business to them.

http://www.opportunityfund.org/media/blog/introducing-sb-197-(block)!/ (last accessed on December 9, 2015)

The legislature approved SB 197 and Gov. Jerry Brown signed it last October. Starting on January 1, 2016, a CFLL lender can pay a fee to an unlicensed person in connection with a referral of a prospective borrower if:

- The referral by the unlicensed person leads to the consummation of a commercial loan (defined as a loan with a principal amount of $5,000 or more the proceeds of which are intended by the borrower for use primarily for other than personal, family or household purposes);

- The loan contract provides for an annual percentage rate that does not exceed 36%; and

- Before approving the loan, the lender:

- Obtains documentation from the prospective borrower documenting the borrower’s commercial status. Examples of acceptable forms of documentation include, but are not limited to, a seller’s permit, business license, articles of incorporation, income tax returns showing business income, or bank account statements showing business income; and

- Performs underwriting and obtains documentation to ensure that the prospective borrower will have sufficient monthly gross revenue with which to repay the loan pursuant to the loan terms. The lender cannot make a loan if it determines through its underwriting that the prospective borrower’s total monthly expenses, including debt service payments on the loan for which the prospective borrower is being considered, will exceed the prospective borrower’s monthly gross revenue. Examples of acceptable forms of documentation for verifying current and projected gross monthly revenue and monthly expenses include, but are not limited to, tax returns, bank statements, merchant financial statements, business plans, business history, and industry-specific knowledge and experience. If the prospective borrower is a sole proprietor or a corporation and the loan will be secured by a personal guarantee provided by the owner, the lender must consider a credit report from at least one consumer credit reporting agency that compiles and maintains files on consumers on a nationwide basis.

The licensee must also maintain records of all compensation paid to unlicensed persons in connection with the referral of borrowers for a period of at least 4 years.

SB 197 also provides that a lender that pays compensation for a referral to an unlicensed person is liable for “any misrepresentation made to that borrower in connection with that loan.” It is not clear whether the lender is liable only for misrepresentations made by the unlicensed person who receives compensation for the referral, or if the regulator will interpret this provision more broadly. Further, lenders must provide such prospective borrowers this specific written statement in 10-point font or larger at the time the licensee receives an application for the loan:

You have been referred to us by [Name of Unlicensed Person]. If you are approved for the loan, we may pay a fee to [Name of Unlicensed Person] for the successful referral. [Licensee], and not [Name of Unlicensed Person] is the sole party authorized to offer a loan to you. You should ensure that you understand any loan offer we may extend to you before agreeing to the loan terms. If you wish to report a complaint about this loan transaction, you may contact the Department of Business Oversight at 1-866-ASK-CORP (1-866-275-2677), or file your complaint online at www.dbo.ca.gov.

Lenders must require prospective borrowers to acknowledge receipt of the statement in writing.

SB 197 defines “referral” to mean either the introduction of the borrower and the lender or the delivery to the lender of the borrower’s contact information. The following activities by an unlicensed person are not authorized:

- Participating in any loan negotiation;

- Counseling or advising the borrower about a loan;

- Participating in the preparation of any loan documents, including credit applications;

- Contacting the lender on behalf of the borrower other than to refer the borrower;

- Gathering loan documentation from the borrower or delivering the documentation to the lender;

- Communicating lending decisions or inquiries to the borrower;

- Participating in establishing any sales literature or marketing materials; and

- Obtaining the borrower’s signature on documents.

Many for-profit CFLL licensees may find the narrow exemption that permits CFLL licensees making commercial loans to accept referrals from non-licensed entities impractical. The industry may instead choose to focus on the existing prohibition against paying non-licensees for “soliciting or accepting applications for loans” to avoid the limitations on the loan terms.

California Bill Aims to Add Consumer Debt Collection Protections to Commercial Debts

August 20, 2024Among several commercial finance bills currently making their way through the legislature in California is SB1286, which would apply consumer debt collection protections to commercial debts.

If this bill were to eventually pass commercial debt collectors would need to obtain the same license currently required under existing law for consumer collectors. In addition, it would be a crime for a collector of a commercial debt “to send a communication that simulates legal or judicial process or that gives the appearance of being authorized, issued, or approved by a governmental agency or attorney if it is not.”

There are still more components that would require compliance as well. Like the fact that under current law a debt collector is required to stop collecting a consumer debt when an alleged debtor provides the debt collector with certain information, including information relating to the debtor’s status as an alleged victim of identity theft. This would also apply to commercial debts. The full language of the bill can be read here.

Another bill moving along right now is SB1482, which would “would impose various duties on commercial financing providers and brokers, including, among other things, prohibiting the taking of a confession of judgment or power of attorney at any time before a default.”

Although both bills were introduced all the way back in February, they are currently being passed through committees.

Don't miss out on getting Cheap leads. Now is the time to stock up.... california licensed contractors, over 70% cell (all cell on trigger / ucc)., , this is great for a business that wants to undercut all of the other companies that sell leads. , , when things start picking up again in a mon... |

California Deal: Approved for 130k... california license, not including bluevine?, , thank you in advance!... |

See Post... california license needed. only caveat is they take 2 days to do final underwriting.... |